- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Neobank Platform Market Size, Share & Forecast | CAGR 49.1%

Global Neobank Platform Market Size, Share, Analysis By Account Type (Personal Neobank Accounts, Business Neobank Accounts, Savings Accounts, Current/Checking Accounts, Multi-Currency Accounts, Youth & Student Accounts, Premium Accounts), By Service (Payments, Lending, Wealth Management, BNPL, BaaS), By Application (Retail Banking, SMEs, Corporate Banking, Cross-Border Remittances), By Technology, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 210.16 Billion | USD 7,661.57 Billion | 49.1% | Europe, 37.2% |

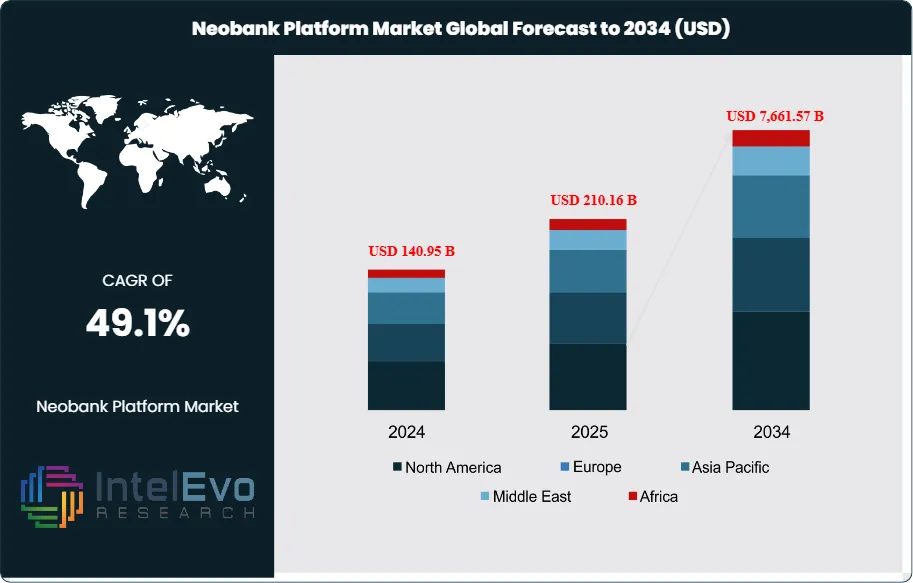

The Neobank Platform Market was valued at approximately USD 140.95 Billion in 2024 and reached USD 210.16 Billion in 2025. The market is projected to surge to USD 7,661.57 Billion by 2034, expanding at a remarkable CAGR of 49.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7,451.41 Billion over the analysis period. The Neobank Platform Market covers digital-only banking platforms operating without physical branches, providing checking and savings accounts, debit and credit cards, lending, payments, foreign exchange, investing, and adjacent financial services through mobile applications and web interfaces licensed under banking charters or banking-as-a-service partnerships.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in three structural shifts. First, over 350 neobanks operate across more than 70 countries serving over 600 million customers worldwide in 2025, with digital banking adoption exceeding 4.8 billion global internet users and 6.6 billion mobile subscribers. Second, the Federal Deposit Insurance Corporation (FDIC), the European Central Bank (ECB), and the Reserve Bank of India (RBI) have progressively modernized regulatory frameworks, including the European Banking Authority's specialized banking licenses for digital banks and the RBI's April 2023 grant of an NBFC license to Jupiter enabling direct lending. Third, the World Bank estimates 1.5 billion unbanked and 2.8 billion underbanked adults globally, creating structural long-term demand for digital-first banking serving previously excluded populations.

Leading platforms accelerated sharply through 2024-2025. Nu Holdings (Nubank) reported Q1 2025 results showing 118.6 million customers, approximately USD 3.25 billion in quarterly revenue, USD 557 million in quarterly profit, and a 24.7% efficiency ratio, applying for a US OCC national bank charter in October 2025. Revolut passed 60 million customers by mid-2025, targeting 100 million by 2027 across 38 countries, and pursued a US banking license. Chime Financial filed Form S-1 with the SEC in May 2025 at a USD 25 billion IPO valuation, serving 22.3 million US customers. Monzo reported 12 million global customers and GBP 113.9 million pre-tax profit in 2025. Starling Bank's Engine BaaS platform and WeBank's AI-driven credit scoring represent the technology productization frontier.

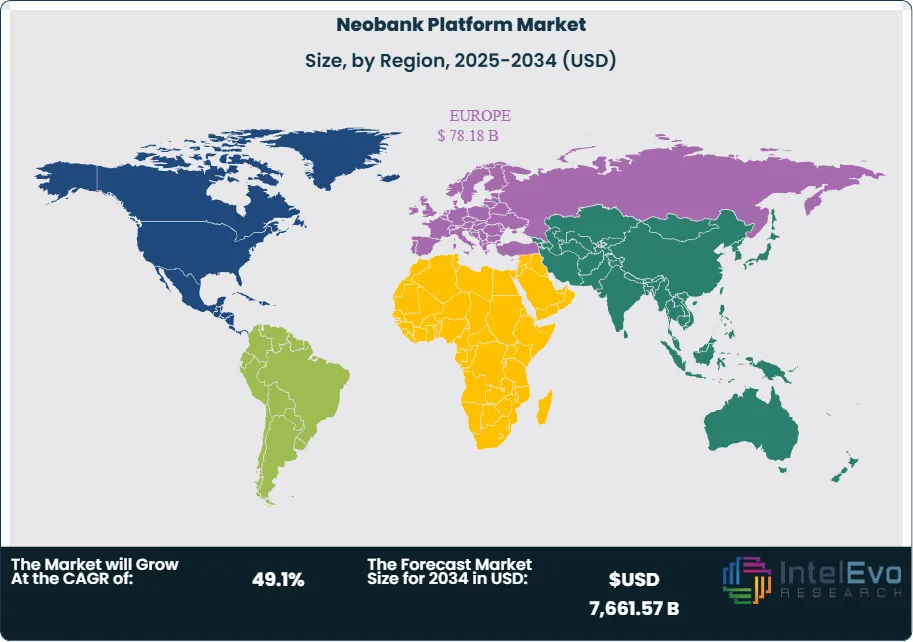

Europe held 37.2% of global Neobank Platform Market revenue in 2025, equivalent to USD 78.18 Billion, anchored by Revolut, N26, Monzo, Starling Bank, Atom Bank, and Bunq under European Central Bank and national regulator frameworks. Asia Pacific captured approximately 32% share at USD 67.25 Billion, led by WeBank, MyBank, KakaoBank, and emerging Indian neobanks operating under RBI Non-Banking Financial Company licenses and Unified Payments Interface (UPI) rails processing over 75% of Indian digital payments. North America held 20% share at USD 42.03 Billion, led by Chime, SoFi, Varo, Dave, and MoneyLion. Latin America captured 8% share at USD 16.81 Billion, anchored by Nubank's Brazil dominance serving 55% of the Brazilian adult population.

Forward visibility through 2034 rests on three catalysts. First, neobank venture funding reached USD 13.2 billion globally in 2025 despite broader fintech market cooling, reflecting sustained investor confidence in the category. Second, AI integration accelerated with 63% of neobanks deploying AI-driven financial tools and 58% focusing on personalized wealth management through embedded finance per 2025 industry surveys. Third, regulatory convergence including the EU Digital Operational Resilience Act (DORA) effective January 2025, the Consumer Financial Protection Bureau (CFPB) Section 1033 open banking rule, and Markets in Crypto-Assets Regulation (MiCA) create infrastructure for cross-border expansion. These forces together support the 49.1% forecast CAGR in the Neobank Platform Market through 2034, though profitability remains concentrated among fewer than 20% of category participants.

Market Definition & Scope

The Neobank Platform Market is defined as the commercial space for digital-only banking platforms that deliver retail and small business banking services through mobile applications and web interfaces without physical branch networks. The market encompasses three core operating models: fully licensed digital banks holding national or specialized banking charters (WeBank, Starling, Varo, SoFi, Monzo), banking-as-a-service (BaaS) dependent neobanks operating through partner bank relationships (Chime, Dave, Mercury through partner banks), and hybrid fintechs expanding from adjacent categories (SoFi from lending, Robinhood from trading, PayPal from payments).

This analysis includes consumer checking and savings accounts, debit and credit cards, personal and small business lending, cross-border payments and FX services, embedded investing and crypto services, and AI-driven financial wellness tools delivered through app-based channels. The scope explicitly excludes traditional banks' digital channels without separate neobank branding (JPMorgan Chase Mobile, Bank of America Mobile), standalone payment processors without banking functionality (Adyen, Stripe), wealth management platforms without banking accounts (Betterment without Cash Reserve context), and cryptocurrency exchanges without fiat banking functionality. The parent banking services industry reached approximately USD 8.2 trillion globally in 2025, with the Neobank Platform Market representing the fastest-growing digital-native subset at approximately 2.6% of parent category in 2025, expanding toward double-digit parent share through 2034.

, By Service (Payments, Lending, Wealth Management, BNPL, BaaS), By Application (Retail Banking, SMEs, Corporate Banking, Cross-Border Remittances), By Technology, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Neobank Platform Market grew from USD 210.16 Billion in 2025 to a projected USD 7,661.57 Billion in 2034, expanding at a 49.1% CAGR.

- Segment Dominance (By Application): The enterprise segment captured 51.7% revenue share in 2025, reflecting concentrated SME and business banking adoption across multi-user accounts, automated expense management, and integrated accounting.

- Segment Dominance (By Account Type): The business account segment led with 64.71% revenue share in 2025, driven by SME preference for digital-first payroll, vendor payments, and cross-border transaction capabilities.

- Driver: Nu Holdings (Nubank) reported Q1 2025 results of 118.6 million customers, USD 3.25 billion quarterly revenue, USD 557 million quarterly profit, and 24.7% efficiency ratio, demonstrating the profitability potential of the category.

- Restraint: Approximately 76% of neobanks remained unprofitable in 2025 per industry surveys, with only 18% projected to break even, reflecting structural customer acquisition cost and lending margin pressure.

- Opportunity: The World Bank estimates 1.5 billion unbanked and 2.8 billion underbanked adults globally, with Nubank demonstrating this opportunity by reaching 55% of Brazilian adults in six years of domestic focus.

- Trend: Revolut targets 100 million customers by mid-2027 across more than 30 new markets by 2030, representing the super-app global expansion model with multi-currency, trading, credit, crypto, and mortgage integration.

- Regional: Europe held 37.2% revenue share in 2025 at USD 78.18 Billion per Fortune Business Insights, anchored by Revolut, N26, Monzo, Starling, Atom, and Bunq under ECB and national regulator frameworks.

Key Insights Summary

- Nu Holdings (Nubank) reported 118.6 million customers, approximately USD 13 billion in annualized revenue, USD 557 million in quarterly profit, and a 24.7% efficiency ratio in Q1 2025, and applied for a US OCC national bank charter in October 2025.

- Revolut Ltd. finished 2024 with 52 million retail customers, GBP 30 billion in customer balances, GBP 3.1 billion in revenue, and GBP 790 million in net profit, surpassing 60 million customers by mid-2025 with a 2027 target of 100 million.

- Chime Financial filed Form S-1 with the US SEC in May 2025 at a USD 25 billion IPO valuation, serving 22.3 million US customers, following full-year 2024 profitability.

- TymeBank (Tyme Group) raised a USD 250 million Series D round led by Nubank in December 2024 at a USD 1.5 billion valuation, expanding South African and Philippine digital banking operations.

- Monzo Bank reported 12 million global customers and GBP 113.9 million pre-tax profit in 2025, demonstrating the profitable UK super-app model across savings, investments, pensions, credit cards, consumer loans, and home insurance.

- The global neobank industry attracted USD 13.2 billion in venture funding in 2025 per industry surveys, reflecting sustained investor confidence despite broader fintech market cooling after 2022-2023 correction.

- The European Union Digital Operational Resilience Act (DORA) became effective in January 2025, imposing operational resilience, third-party risk, and incident reporting requirements on all EU-operating neobanks.

Competitive Landscape Overview

The Neobank Platform Market is moderately consolidated at the revenue tier with the top four companies including Nu Holdings (Nubank), Revolut, SoFi, and WeBank collectively holding an estimated 40 to 46% of global revenue in 2025, though fragmented at the platform count tier with over 350 operating neobanks globally. Competition is structured across three tiers: profitable scale leaders with USD 1+ billion annual revenue including Nubank, Revolut, SoFi, WeBank, and Monzo; growth-stage challengers targeting profitability including N26, Chime, Starling, Bunq, KakaoBank, and Varo; and specialty vertical players including Mercury (startups), Current (youth), Dave (cash advances), and TymeBank (emerging markets).

The competitive environment shifted sharply through 2024-2025 toward profitability-first strategies after the 2022-2023 venture funding correction. Geographic champions dominate distinct regions: Nubank leads Latin America with approximately 125 million customers, Revolut leads Europe with over 60 million users, Chime captures US mass market with 22.3 million customers, and WeBank dominates China with hundreds of millions. Super-app strategies (Revolut, SoFi) and vertical specialization (Mercury with 100,000+ startups generating USD 500 million ARR, Current with 4 million youth customers) drive the strongest growth. Banking charter acquisition became a strategic priority, with Varo (2020), SoFi (2022), and Nubank (October 2025 OCC application) pursuing charter-based competitive moats. The 2024 collapse of Synapse BaaS platform disrupted fintechs relying on partner banks like Evolve Bank and Trust, accelerating charter pursuit across the category.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Nu Holdings Ltd. (Nubank) | Sao Paulo, Brazil | Global Leader | Nubank mobile banking; credit cards; lending; Ultravioleta premium tier | Brazil, Mexico, Colombia | Applied for OCC US national bank charter in October 2025; 118.6 million customers Q1 2025 |

| Revolut Ltd. | London, United Kingdom | Leader (EU/Global) | Revolut super-app; multi-currency accounts; stocks; crypto; mortgages | Europe, Global (38 countries) | Passed 60 million customers mid-2025; targeting 100 million by 2027; pursuing US banking license |

| Chime Financial, Inc. | San Francisco, CA, USA | Leader (US) | Chime Checking; SpotMe overdraft; Credit Builder card | United States | Filed SEC Form S-1 registration statement in May 2025 at USD 25 billion IPO valuation |

| SoFi Technologies, Inc. | San Francisco, CA, USA | Leader (US) | SoFi Bank; lending; investing; insurance; Galileo BaaS | United States | Public on NASDAQ (SOFI); approximately USD 14 billion market cap; national bank charter acquired 2022 |

| WeBank Co., Ltd. | Shenzhen, China | Leader (APAC) | WeBank consumer lending; SME banking; AI-driven credit | China (Tencent-backed) | Continued AI-driven financial inclusion expansion serving hundreds of millions of Chinese customers 2025 |

| N26 AG | Berlin, Germany | Challenger (EU) | N26 You; N26 Metal; crypto trading; business accounts | Europe | Continued European market expansion and BaFin regulatory compliance remediation through 2025 |

| Monzo Bank Limited | London, United Kingdom | Challenger (UK) | Monzo Plus; Monzo Premium; lending; investments; pensions | United Kingdom, US | Reported 12 million customers and GBP 113.9 million pre-tax profit in 2025 |

| Starling Bank Limited | London, United Kingdom | Challenger (UK) | Starling personal and business banking; Engine BaaS platform | United Kingdom | Continued profitability and Engine BaaS platform licensing to international partner banks 2025 |

| Varo Bank, N.A. | San Francisco, CA, USA | Niche (US charter) | Varo checking; savings; Varo Advance short-term credit | United States | First US consumer fintech to receive national bank charter (2020); continued product expansion 2025 |

| TymeBank (Tyme Group) | Cape Town, South Africa | Challenger (EMEA/APAC) | TymeBank EveryDay; GoalSave; MoreTyme BNPL; GOtyme (Philippines) | South Africa, Philippines | Raised USD 250 million Series D led by Nubank in December 2024 at USD 1.5 billion valuation |

Segmentation Analysis

The Neobank Platform Market segments across account type, service, end-user, technology platform, and geography. Procurement leaders at corporate treasury teams and investors building a neobank platform procurement checklist should benchmark providers on banking charter status versus BaaS dependency, deposit insurance coverage (FDIC, FSCS, or equivalent), regulatory compliance framework (BSA/AML, KYC), fee structure versus legacy banking benchmarks, API breadth for enterprise integration, and unit economics across customer acquisition cost, lifetime value, and interchange revenue per customer.

By Account Type

Business accounts led the Neobank Platform Market with 64.71% revenue share in 2025 per Grand View Research, equivalent to approximately USD 136.00 Billion. SME adoption drove the concentration, with small and medium enterprises preferring digital-first payroll, vendor disbursements, and cross-border FX over traditional bank fee structures. Mercury serves over 100,000 startups generating approximately USD 500 million in ARR, while Brex, Revolut Business, Monzo Business, and Nubank PJ anchor the segment. Savings accounts captured the remaining 35.29% share at USD 74.16 Billion, with premium-tier subscription accounts (Revolut Premium, Monzo Plus, N26 You) representing 23% of all neobank accounts and basic savings accounts comprising 62% of offerings per industry surveys.

By Service

Digital checking and savings accounts led the Neobank Platform Market with approximately 38% revenue share in 2025, anchored by FDIC-insured accounts at Chime, Varo, SoFi, and Ally in the US, Financial Services Compensation Scheme (FSCS)-protected accounts at Monzo and Starling in the UK, and Brazilian Central Bank-regulated accounts at Nubank. Lending and credit services captured 27% share at approximately USD 56.74 Billion, primarily anchored by Nubank's credit card and personal loan portfolio generating the majority of its USD 13 billion annualized revenue. Payment services and money transfers held 18% share, led by Revolut's multi-currency FX and Wise's cross-border corridor strength. Investment and wealth management captured 11% share through SoFi Invest, Revolut stocks and crypto, Robinhood, and N26 Crypto. Insurance services captured the remaining 6% share through Monzo, Revolut, and Lemonade partnership integrations.

By Application

Enterprises led the Neobank Platform Market with 51.7% revenue share in 2025 per Grand View Research, driven by SME and mid-market business banking adoption. Enterprise services include multi-user account access, automated expense management, real-time transaction tracking, integrated accounting tools (QuickBooks, Xero), and cross-border transaction capabilities. Personal segment captured approximately 44% share, growing fastest at sub-50% CAGR and anchored by millennial and Gen Z consumer adoption where 72% of millennials prefer digital-only banks per industry surveys. Government and institutional applications held the remaining 4% share through specialized business banking for non-profit and public sector organizations. Neobank compliance requirements including BSA/AML, KYC, OFAC sanctions screening, and beneficial ownership reporting under the Corporate Transparency Act create ongoing operational investment pressure across the category.

By Technology

Cloud-native microservices architectures led the Neobank Platform Market with approximately 68% deployment share in 2025, anchored by AWS, Google Cloud Platform, and Microsoft Azure hosting. Core banking platforms including Mambu, Thought Machine Vault, Temenos T24 Transact, Finacle, and Tuum power approximately 55% of new neobank launches. AI and machine learning integration reached 63% of neobanks for credit scoring, fraud detection, customer service chatbots, and personalized recommendations. Open banking API integration covered 45% of platforms through PSD2 in Europe, Open Banking Implementation Entity (OBIE) standards in the UK, and CFPB Section 1033 emerging in the US. Biometric authentication adoption reached 48% deployment including facial recognition, fingerprint, and voice recognition. Blockchain and tokenization integration reached 15% primarily through crypto trading and stablecoin settlement features. Neobank implementation timelines typically range from 12 to 24 months for BaaS-dependent launches and 24 to 48 months for charter-licensed operations.

Regional Analysis

The Neobank Platform Market divides across Europe, Asia Pacific, North America, Latin America, and Middle East & Africa, with Europe leading in 2025 and Latin America and Asia Pacific growing fastest through 2034.

Europe

Europe held 37.2% of global Neobank Platform Market revenue in 2025, equivalent to USD 78.18 Billion. The United Kingdom anchors regional adoption accounting for approximately 42% of European users, followed by Germany, France, the Netherlands, and Spain. The European Central Bank (ECB), European Banking Authority (EBA), and national competent authorities including Germany's BaFin, the UK's Financial Conduct Authority (FCA), and France's ACPR coordinate regulatory oversight. The Digital Operational Resilience Act (DORA) effective January 2025 imposes operational resilience, ICT risk management, and third-party monitoring requirements. The Markets in Crypto-Assets Regulation (MiCA) fully applied from December 2024. Payment Services Directive (PSD2) and proposed PSD3 provide open banking frameworks. Major European neobanks include Revolut (UK), N26 (Germany), Monzo (UK), Starling (UK), Atom Bank (UK), Bunq (Netherlands), and Lunar (Denmark).

Asia Pacific

Asia Pacific held approximately 32.0% share in 2025 at USD 67.25 Billion and is projected to grow fastest at approximately 50% CAGR through 2034. China anchors regional adoption with WeBank (Tencent-backed) and MyBank (Alibaba-backed) collectively serving hundreds of millions of customers under China Banking and Insurance Regulatory Commission (CBIRC) oversight. Japan's Financial Services Agency (FSA) regulates domestic neobanks including Rakuten Bank and PayPay Bank. South Korea's Financial Services Commission (FSC) oversees KakaoBank with approximately 24 million customers. India's Reserve Bank of India (RBI) granted an NBFC license to Jupiter in April 2023, enabling direct lending, with Niyo, Fi Money, Open, and RazorpayX leading domestic adoption. The Unified Payments Interface (UPI) processed over 75% of Indian digital payments in 2025, with India's neobank user growth reaching 52% in 2025 per industry surveys. Australia's APRA-regulated neobanks including Judo Bank and Up anchor Australian adoption.

North America

North America captured 20.0% share in 2025 at USD 42.03 Billion, with the United States contributing 94% of regional revenue, Canada at 5%, and Mexico at 1%. The Office of the Comptroller of the Currency (OCC), Federal Deposit Insurance Corporation (FDIC), Consumer Financial Protection Bureau (CFPB), and state banking regulators coordinate US oversight. US neobank adoption grew from 29.8 million accounts in 2021 to 53.7 million by 2025, with 45% of millennials preferring neobanks over traditional banks. Major US players include Chime (22.3 million customers), SoFi (public at USD 14 billion market cap), Varo (first US fintech national bank charter in 2020), Dave, MoneyLion, Mercury, Current, Aspiration, and Upgrade. Canadian neobanks include Neo Financial (CAD 68.5 million Series raised January 2025), Wealthsimple Cash, KOHO, and EQ Bank under Office of the Superintendent of Financial Institutions (OSFI) oversight. US fintech investments surpassed USD 50 billion annually supporting neobank infrastructure.

Latin America

Latin America held 8.0% share in 2025 at USD 16.81 Billion and is projected to grow fastest in absolute revenue terms, anchored by Nubank's regional dominance. Brazil captured 85% of regional revenue at approximately USD 14.29 Billion, driven by Nubank serving 55% of Brazilian adults as of Q1 2025, complemented by Inter, C6 Bank, PicPay, and Banco Original. The Banco Central do Brasil operates the Pix instant payment system that processes billions of monthly transactions, creating infrastructure supporting fintech scale. Mexico held 9% regional share, with Nubank Mexico and Ualá leading. Colombia at 4% anchored by Nubank Colombia. Argentina's Ualá, Brubank, and Naranja X lead domestic adoption under Banco Central de la Republica Argentina oversight. Regional growth is driven by large unbanked populations, rapid smartphone adoption, and progressive central bank policies enabling fintech competition.

Middle East & Africa

The Middle East & Africa region held 2.8% share in 2025 at approximately USD 5.88 Billion and is projected to grow at approximately 45% CAGR through 2034. The United Arab Emirates led regional adoption with Liv. (Emirates NBD), Mashreq NEO, and ADIB al hilal serving GCC expatriate and local populations under Central Bank of the UAE regulation. Saudi Arabia's Saudi Central Bank (SAMA) licensed STC Pay, SABB Neo, and Mozn. Egypt's Central Bank licensed Telda under the 2021 banking law reform. South Africa's TymeBank raised USD 250 million Series D led by Nubank in December 2024 at USD 1.5 billion valuation, operating in South Africa and Philippines (GOtyme) under South African Reserve Bank oversight. Nigeria's Kuda Bank, OPay, and Carbon lead West African adoption under Central Bank of Nigeria regulations. Kenya's M-Shwari, Equitel, and Branch anchor East African mobile financial services. Israel's Pepper (Bank Leumi subsidiary) and One Zero Digital Bank serve domestic neobanking demand.

Country Analysis

The Neobank Platform Market concentrates in four national markets that together contribute more than 60% of 2025 global revenue: the United States, the United Kingdom, China, and Brazil.

United States

The United States generated approximately USD 39.51 Billion in Neobank Platform Market revenue in 2025, with a country CAGR of approximately 34.6% through 2034 per industry surveys. US digital-only bank account holders grew from 29.8 million in 2021 to 53.7 million by 2025 per Unit 21 data, with 45% of millennials preferring neobanks over traditional banks. The Office of the Comptroller of the Currency (OCC), Federal Deposit Insurance Corporation (FDIC), and Consumer Financial Protection Bureau (CFPB) regulate federal neobanks. Chime's May 2025 Form S-1 filing at USD 25 billion valuation marked a landmark IPO in the category. Varo Bank achieved the first US consumer fintech national bank charter in 2020, followed by SoFi in 2022. Nubank applied for an OCC national bank charter in October 2025, and Revolut has pursued a US banking license. The 2024 collapse of Synapse BaaS platform disrupted fintechs relying on partner banks like Evolve Bank and Trust.

United Kingdom

The United Kingdom contributed approximately USD 32.83 Billion in Neobank Platform Market revenue in 2025, representing approximately 42% of European share, with a country CAGR of 48% through 2034. The Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) regulate UK neobanks, with the Financial Services Compensation Scheme (FSCS) providing GBP 85,000 deposit protection per account. Major UK players include Revolut (London-headquartered, 60+ million global customers), Monzo (12 million global customers, GBP 113.9 million pre-tax profit in 2025), Starling Bank (profitable since 2021, Engine BaaS platform licensing), Atom Bank, Kroo Bank, Zopa Bank, and Tide (SMB focus). Open Banking Implementation Entity (OBIE) standards enable API-based third-party provider access. The Authorised Push Payment (APP) Fraud reimbursement rules effective October 2024 impose new consumer protection costs on UK neobanks. Brexit regulatory divergence from EU frameworks creates distinct compliance obligations.

China

China contributed approximately USD 40.35 Billion in Neobank Platform Market revenue in 2025, with a country CAGR of approximately 50% through 2034. China's neobank market is anchored by WeBank (Tencent-backed, established 2014 as China's first private online bank) and MyBank (Alibaba-backed, established 2015), collectively serving hundreds of millions of consumer and SME customers. The China Banking and Insurance Regulatory Commission (CBIRC) oversees private internet banks under separate licensing from traditional commercial banks. WeBank leverages AI-driven credit scoring for financial inclusion serving the underbanked Chinese population per McKinsey 2022 analysis. The People's Bank of China (PBOC) operates the Digital Yuan (e-CNY) pilot in select cities, creating infrastructure for programmable money integration. Regulatory tightening under the 2021 Antitrust and Data Security Laws constrains aggressive customer acquisition practices, shifting competition toward credit quality and technology differentiation.

Brazil

Brazil contributed approximately USD 14.29 Billion in Neobank Platform Market revenue in 2025, with a country CAGR of approximately 42% through 2034. Brazil is the global leader in neobank penetration, with Nubank alone serving 118.6 million customers globally and approximately 95 million Brazilian customers representing 55% of the adult population. The Banco Central do Brasil operates the Pix instant payment system handling billions of monthly transactions since its November 2020 launch, providing critical infrastructure for fintech scale. Major Brazilian players include Nubank (publicly listed on NYSE as NU Holdings, approximately USD 13 billion annualized revenue Q1 2025), Inter (publicly listed on B3 and NASDAQ), C6 Bank, PicPay, and Banco Original. The Central Bank's open banking framework launched in phases through 2021-2024 enables API-based competition. Tax reform proposals under the Lula administration in 2024-2025 create fiscal uncertainty around fintech business models. Brazilian neobank efficiency ratios including Nubank's 24.7% significantly outperform traditional Brazilian banking benchmarks of 45-55%.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Account Type

- Personal Neobank Accounts

- Business Neobank Accounts

- Savings Accounts

- Current/Checking Accounts

- Multi-Currency Accounts

- Joint Accounts

- Youth and Student Accounts

- Premium and Wealth Management Accounts

By Service

- Payments and Money Transfers

- Savings and Deposit Services

- Lending and Credit Services

- Debit and Prepaid Card Services

- Foreign Exchange and Multi-Currency Services

- Wealth Management and Investment Services

- Insurance Services

- Personal Finance Management

- Buy Now, Pay Later (BNPL) Services

- Banking-as-a-Service (BaaS)

By Application

- Retail Banking

- Small and Medium-Sized Enterprises (SMEs)

- Freelancers and Gig Economy Workers

- Corporate Banking

- Cross-Border Banking and Remittances

- Digital Payments and E-Commerce

- Wealth and Financial Management

- Financial Inclusion Initiatives

By Technology

- Artificial Intelligence (AI) and Machine Learning

- Open Banking APIs

- Cloud Computing

- Blockchain and Distributed Ledger Technology

- Big Data and Advanced Analytics

- Biometric Authentication

- Robotic Process Automation (RPA)

- Real-Time Payment Technologies

- Cybersecurity and Fraud Detection Solutions

- Embedded Finance Technologies

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 210.16 B |

| Forecast Revenue (2034) | USD 7,661.57 B |

| CAGR (2025-2034) | 49.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Account Type, (Personal Neobank Accounts, Business Neobank Accounts, Savings Accounts, Current/Checking Accounts, Multi-Currency Accounts, Joint Accounts, Youth and Student Accounts, Premium and Wealth Management Accounts), By Service, (Payments and Money Transfers, Savings and Deposit Services, Lending and Credit Services, Debit and Prepaid Card Services, Foreign Exchange and Multi-Currency Services, Wealth Management and Investment Services, Insurance Services, Personal Finance Management, Buy Now, Pay Later (BNPL) Services, Banking-as-a-Service (BaaS)), By Application, (Retail Banking, Small and Medium-Sized Enterprises (SMEs), Freelancers and Gig Economy Workers, Corporate Banking, Cross-Border Banking and Remittances, Digital Payments and E-Commerce, Wealth and Financial Management, Financial Inclusion Initiatives), By Technology, (Artificial Intelligence (AI) and Machine Learning, Open Banking APIs, Cloud Computing, Blockchain and Distributed Ledger Technology, Big Data and Advanced Analytics, Biometric Authentication, Robotic Process Automation (RPA), Real-Time Payment Technologies, Cybersecurity and Fraud Detection Solutions, Embedded Finance Technologies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NU HOLDINGS LTD. (NUBANK), REVOLUT LTD., CHIME FINANCIAL, INC., SOFI TECHNOLOGIES, INC., WEBANK CO., LTD., N26 AG, MONZO BANK LIMITED, STARLING BANK LIMITED, VARO BANK, N.A., TYMEBANK (TYME GROUP), ATOM BANK PLC, KAKAOBANK CORP., BUNQ B.V., MYBANK, MERCURY TECHNOLOGIES, INC., CURRENT, DAVE INC., MONEYLION INC., UPGRADE, INC., FIDOR SOLUTIONS AG, JUDO BANK, LUNAR BANK, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Service (Payments, Lending, Wealth Management, BNPL, BaaS), By Application (Retail Banking, SMEs, Corporate Banking, Cross-Border Remittances), By Technology, Industry Trends & Forecast 2026-2034")

, By Service (Payments, Lending, Wealth Management, BNPL, BaaS), By Application (Retail Banking, SMEs, Corporate Banking, Cross-Border Remittances), By Technology, Industry Trends & Forecast 2026-2034")

, By Service (Payments, Lending, Wealth Management, BNPL, BaaS), By Application (Retail Banking, SMEs, Corporate Banking, Cross-Border Remittances), By Technology, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Neobank Platform Market?

The Global Neobank Platform Market was valued at USD 140.95 Billion in 2024 and is projected to reach USD 7,661.57 Billion by 2034, growing at a CAGR of 49.1% from 2026 to 2034. Growth is driven by rising digital banking adoption, increasing smartphone penetration, expanding fintech investments, Banking-as-a-Service (BaaS) innovation, open banking initiatives, AI-powered personalized financial services, embedded finance, and the growing demand for seamless, branchless banking experiences worldwide.

Who are the major players in the Neobank Platform Market?

NU HOLDINGS LTD. (NUBANK), REVOLUT LTD., CHIME FINANCIAL, INC., SOFI TECHNOLOGIES, INC., WEBANK CO., LTD., N26 AG, MONZO BANK LIMITED, STARLING BANK LIMITED, VARO BANK, N.A., TYMEBANK (TYME GROUP), ATOM BANK PLC, KAKAOBANK CORP., BUNQ B.V., MYBANK, MERCURY TECHNOLOGIES, INC., CURRENT, DAVE INC., MONEYLION INC., UPGRADE, INC., FIDOR SOLUTIONS AG, JUDO BANK, LUNAR BANK, Others

Which segments covered the Neobank Platform Market?

By Account Type, (Personal Neobank Accounts, Business Neobank Accounts, Savings Accounts, Current/Checking Accounts, Multi-Currency Accounts, Joint Accounts, Youth and Student Accounts, Premium and Wealth Management Accounts), By Service, (Payments and Money Transfers, Savings and Deposit Services, Lending and Credit Services, Debit and Prepaid Card Services, Foreign Exchange and Multi-Currency Services, Wealth Management and Investment Services, Insurance Services, Personal Finance Management, Buy Now, Pay Later (BNPL) Services, Banking-as-a-Service (BaaS)), By Application, (Retail Banking, Small and Medium-Sized Enterprises (SMEs), Freelancers and Gig Economy Workers, Corporate Banking, Cross-Border Banking and Remittances, Digital Payments and E-Commerce, Wealth and Financial Management, Financial Inclusion Initiatives), By Technology, (Artificial Intelligence (AI) and Machine Learning, Open Banking APIs, Cloud Computing, Blockchain and Distributed Ledger Technology, Big Data and Advanced Analytics, Biometric Authentication, Robotic Process Automation (RPA), Real-Time Payment Technologies, Cybersecurity and Fraud Detection Solutions, Embedded Finance Technologies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date