- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Neural Processing Unit Market

Global Neural Processing Unit Market Size, Share, Growth Analysis By Product Type (Edge NPU, Cloud & Data Center NPU, Automotive NPU, Industrial & Medical NPU), By Application (Consumer Electronics, Cloud Infrastructure, Automotive, Robotics & Factory Automation, Healthcare Imaging), By Node Technology (Sub-5nm, 5nm–7nm, 10nm & Above), AI Semiconductor Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 7.84 Billion | USD 39.60 Billion | 19.6% | Asia Pacific, 42.3% |

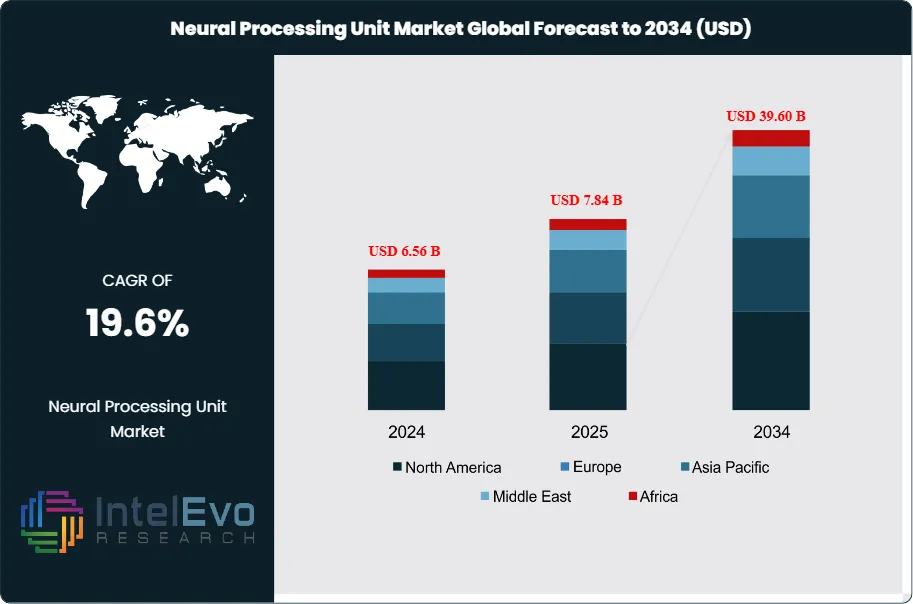

The Neural Processing Unit Market was valued at approximately USD 6.56 Billion in 2024 and reached USD 7.84 Billion in 2025. The market is projected to grow to USD 39.60 Billion by 2034, expanding at a CAGR of 19.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 31.76 Billion over the analysis period, making neural processing units one of the most capital-intensive and strategically critical semiconductor segments of the current decade.

Get More Information about this report -

Request Free Sample ReportNeural processing units are purpose-built silicon architectures designed to accelerate matrix multiplication, convolution operations, and tensor computations that underpin modern artificial intelligence workloads. Unlike central processing units optimized for sequential logic or graphics processing units built for parallel floating-point throughput, NPUs deliver orders-of-magnitude improvements in per-watt AI inference performance. This architectural advantage translates directly into commercial value: device manufacturers embedding NPUs achieve longer battery life, faster on-device inference, and the ability to run large language models and computer vision pipelines without relying on cloud connectivity.

Demand for neural processing unit solutions accelerated sharply from 2022 onward, driven by three converging forces. First, the proliferation of generative AI applications created sustained enterprise appetite for edge inference hardware capable of handling billions of parameters. Second, smartphone original equipment manufacturers embedded NPUs as flagship differentiators, with major handset platforms deploying units reaching 35–45 TOPS (tera-operations per second) of dedicated AI throughput. Third, automotive sector requirements for Advanced Driver Assistance Systems and Level 3 autonomy created a new class of automotive-grade NPU demand, a segment projected to reach USD 4.1 Billion by 2034 within the overall Neural Processing Unit market.

Regulatory signals reinforce the commercial trajectory. The CHIPS and Science Act in the United States directed over USD 52 Billion toward domestic semiconductor manufacturing and R&D, with a material share targeting AI silicon. The European Chips Act similarly committed EUR 43 Billion to build sovereign semiconductor capacity, indirectly accelerating NPU investment across the European supply chain. China's domestic semiconductor push under its 14th Five-Year Plan maintains government-backed development programs for AI chipsets, intensifying competitive pressure globally.

Asia Pacific leads the Neural Processing Unit market with a 42.3% revenue share in 2025, anchored by high-volume consumer electronics manufacturing in South Korea, Taiwan, and China. North America commands 28.7% share, concentrated in hyperscaler data center deployments and edge AI computing platforms. Supply chain considerations and geopolitical tensions around advanced node fabrication below 5nm are reshaping sourcing strategies for leading NPU developers, with diversification toward mature fabs complementing leading-edge production.

, By Application (Consumer Electronics, Cloud Infrastructure, Automotive, Robotics & Factory Automation, Healthcare Imaging), By Node Technology (Sub-5nm, 5nm–7nm, 10nm & Above), AI Semiconductor Trends & Forecast 2026-2034")

Key Takeaways

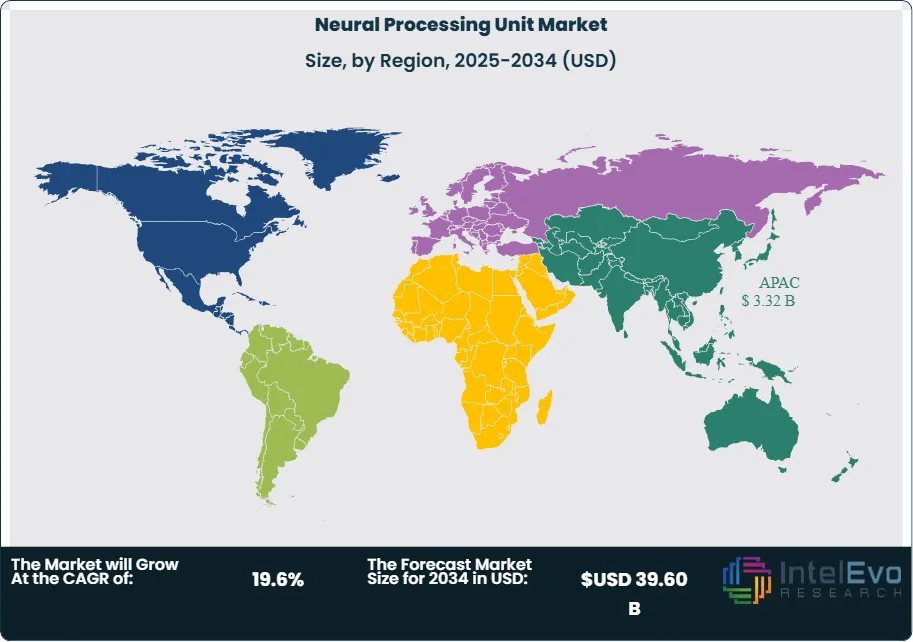

- Market Growth: The global Neural Processing Unit market was valued at USD 7.84 Billion in 2025 and is forecast to reach USD 39.60 Billion by 2034, expanding at a CAGR of 19.6% over the forecast period 2026–2034.

- Segment Dominance: By product type, the Edge NPU segment leads with a 47.2% revenue share in 2025, driven by rapid adoption in smartphones, wearables, and IoT devices requiring on-device AI inference.

- Segment Dominance: By application, the consumer electronics vertical accounts for 38.6% of Neural Processing Unit market revenue in 2025, underpinned by NPU integration in flagship Android and iOS-class devices.

- Driver: Surging on-device generative AI inference demand is the primary growth driver, with global AI-capable device shipments projected to exceed 1.4 Billion units annually by 2027, each requiring dedicated NPU throughput of 30 TOPS or higher.

- Restraint: High design complexity and advanced node dependency constrain market entry. Tape-out costs for NPU designs at 3nm and below exceed USD 500 Million, limiting meaningful competition to a small number of vertically integrated chipmakers.

- Opportunity: The automotive NPU segment presents the largest incremental opportunity, with an addressable value estimated at USD 4.1 Billion by 2034 as ADAS and autonomous driving architectures mandate dedicated AI acceleration across sensor fusion, path planning, and perception workloads.

- Trend: The dominant 2025 trend is the shift from standalone NPU dies to heterogeneous system-on-chip integration, with over 78% of mobile NPU designs shipping as part of a multi-core SoC integrating CPU, GPU, and NPU tiles on a single package as of 2025.

- Regional Analysis: Asia Pacific commands the largest Neural Processing Unit market share at 42.3% in 2025, equivalent to USD 3.32 Billion, led by South Korea, Taiwan, and China across both chip design and high-volume consumer electronics assembly.

Competitive Landscape Overview

The Neural Processing Unit market is moderately consolidated, with the top four players collectively accounting for approximately 58.4% of global revenue in 2025. Competition is primarily technology-driven, with differentiation centered on TOPS-per-watt performance ratios, software development kit maturity, and SoC integration depth. The competitive intensity increased markedly in 2024–2025 as hyperscalers accelerated custom silicon programs, and fabless challengers from China accelerated domestic NPU roadmaps under government-backed programs. Merger and acquisition activity remains selective; strategic partnerships between NPU IP licensors and foundry partners have emerged as the preferred route to accelerating time-to-market.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

|---|---|---|---|---|---|

| Apple Inc. | USA | Leader | Apple Neural Engine (A-series / M-series) | North America, Asia Pacific | Launched M4 chip with 38 TOPS NPU; expanded on-device AI for Apple Intelligence suite (2024) |

| Qualcomm | USA | Leader | Hexagon NPU (Snapdragon 8 Elite) | North America, Asia Pacific | Announced Snapdragon X Elite NPU at 45 TOPS for PC AI workloads; partnered with Microsoft Copilot+ platform (2025) |

| NVIDIA | USA | Leader | Jetson Orin NX / DLA cores | North America, Europe | Launched Jetson Thor for automotive AI; secured design wins with four Tier-1 automotive OEMs (2025) |

| MediaTek | Taiwan | Leader | APU 790 (Dimensity 9400) | Asia Pacific | APU 790 achieved 50 TOPS rating; expanded licensing agreements with five Chinese OEMs (2025) |

| Samsung Electronics | South Korea | Challenger | Mach-1 NPU (Exynos 2500) | Asia Pacific, Europe | Taped out Exynos 2500 with 3nm GAA process featuring enhanced NPU tile architecture (2024) |

| Huawei (HiSilicon) | China | Challenger | Da Vinci NPU (Ascend / Kirin) | Asia Pacific (China) | Released Kirin 9020 with integrated Da Vinci NPU for domestic Android ecosystem amid export restrictions (2025) |

| Intel | USA | Challenger | Intel AI Boost (Core Ultra) | North America, Europe | Shipped 40M+ Core Ultra units with integrated NPU; achieved Microsoft Copilot+ hardware certification (2025) |

| Arm Holdings | UK | Niche Player | Ethos NPU IP (U85) | Global (IP licensor) | Released Ethos-U85 IP core with 4x performance uplift over prior generation; expanded licensee base to 30+ OEMs (2025) |

By Product Type

The Edge NPU segment is the largest product category within the Neural Processing Unit market, representing 47.2% of total revenue in 2025 at an estimated USD 3.70 Billion. Edge NPUs are integrated into smartphones, AR/VR headsets, smart home devices, and embedded IoT endpoints where power budgets are measured in milliwatts and cloud round-trip latency is commercially unacceptable. The architectural philosophy here prioritizes energy efficiency and low-precision integer quantized inference, typically INT8 and INT4 operations, rather than the high-precision floating-point throughput demanded by training workloads. Key growth factors include the smartphone replacement cycle aligning with AI feature launches, with average NPU performance in flagship handsets increasing at approximately 35% annually between 2022 and 2025. The maturation of on-device large language model inference, particularly models in the 3–7 billion parameter range running entirely in device DRAM, is creating a hardware refresh catalyst that extends beyond the traditional two-year smartphone upgrade cycle.

Cloud and Data Center NPUs represent 31.8% of the Neural Processing Unit market in 2025, equating to USD 2.49 Billion. These silicon blocks target hyperscale inference farms where billions of API calls are processed daily across conversational AI, recommendation, and image generation services. Unlike edge designs, data center NPUs emphasize high-throughput FP16 and BF16 matrix multiply, massive on-chip SRAM for weight caching, and high-bandwidth memory interfaces. The economics of data center NPU deployment are compelling: purpose-built AI inference silicon achieves 3–8 times better throughput-per-dollar versus general-purpose GPU inference for transformer workloads. Hyperscalers including Amazon Web Services, Google, and Microsoft have invested cumulatively over USD 20 Billion in proprietary NPU programs through 2025, reflecting the strategic priority of reducing per-token inference costs.

Automotive NPUs account for 13.6% of the Neural Processing Unit market in 2025 at USD 1.07 Billion. Automotive-grade NPU adoption is directly tied to the expanding penetration of Level 2+ and Level 3 ADAS systems, which require real-time inference across camera, radar, and LiDAR sensor streams under functional safety constraints governed by ISO 26262 and SOTIF standards. The performance requirements are severe: automotive NPU platforms must sustain 250–500 TOPS of AI throughput while maintaining ASIL-D safety ratings. The remaining 7.4% of the Neural Processing Unit market is captured by industrial and medical embedded NPU applications, which prioritize long product lifecycle support, wide operating temperature ranges, and regulatory compliance over raw performance advancement.

By Application

Consumer electronics is the dominant application vertical for neural processing units, accounting for 38.6% of global market revenue in 2025, equivalent to USD 3.03 Billion. The primary demand vector is flagship smartphone integration, where Apple, Samsung, Qualcomm, and MediaTek compete on published TOPS benchmarks as proxy marketing metrics for AI capability. Secondary demand within consumer electronics comes from laptop and personal computer platforms, where the Copilot+ hardware certification program created a formal minimum NPU specification of 40 TOPS that manufacturers must meet for Windows AI feature eligibility. Smart speakers, wearables, and consumer drones represent smaller but fast-growing sub-segments within consumer electronics, with aggregate NPU content value per device rising from approximately USD 4 in 2022 to USD 9 in 2025.

The data center and cloud infrastructure application segment represents 29.4% of the Neural Processing Unit market in 2025 at USD 2.31 Billion. Revenue is concentrated among a small number of hyperscale cloud providers deploying custom NPU silicon at petabyte-scale inference workloads. The cost economics are transformative: proprietary inference chips deployed by leading hyperscalers reduced per-query AI inference costs by an estimated 60–75% compared to GPU-based inference over the 2021–2025 period, validating the continued capital investment in custom NPU programs. The automotive application segment claims 14.2% share in 2025, while industrial robotics and factory automation accounts for 10.3%, driven by machine vision and predictive maintenance inference workloads. Healthcare and medical imaging applications represent 4.8% of the Neural Processing Unit market in 2025, a segment growing above the market average as FDA-cleared AI diagnostic tools proliferate in radiology and pathology workflows.

By Node Technology

The sub-5nm node segment commands 41.3% of the Neural Processing Unit market in 2025, reflecting the migration of leading-edge mobile and data center NPU designs to TSMC's N3E and Samsung Foundry's 3GAE processes. These advanced nodes deliver critical power efficiency improvements, enabling the industry's drive toward 30–50 TOPS-per-watt efficiency targets that are commercially necessary for passively cooled edge devices. The 5nm-to-7nm node segment holds 33.9% share in 2025, representing the productive mainstream tier where NPU designs for mid-range smartphones, industrial systems, and cost-sensitive edge deployments are manufactured. The 10nm-and-above node tier accounts for the remaining 24.8%, predominantly serving legacy automotive platforms, industrial microcontrollers, and price-sensitive consumer IoT applications where performance requirements are modest and long-lifecycle process availability is prioritized.

Regional Analysis

Asia Pacific

Asia Pacific leads the global Neural Processing Unit market with a 42.3% revenue share in 2025, equivalent to USD 3.32 Billion. The region's dominance reflects its dual role as both the largest consumer electronics manufacturing hub and home to leading semiconductor foundries. Taiwan hosts TSMC, which manufactures the majority of leading-edge NPU dies for Apple, Qualcomm, MediaTek, and NVIDIA at 3nm and 5nm nodes. South Korea anchors Samsung Electronics' Exynos NPU development and SK Hynix's high-bandwidth memory supply, which is critical for NPU memory subsystems. China's domestic NPU ecosystem, anchored by Huawei's HiSilicon division and emerging players such as Cambricon and Biren Technology, is developing rapidly under government stimulus programs. Japan contributes through precision equipment and materials supply chains, with companies such as Tokyo Electron providing critical deposition and etch tools for NPU wafer fabrication. The Asia Pacific Neural Processing Unit market is projected to grow at a CAGR of 21.2% through 2034, outpacing the global average, as regional smartphone shipment volumes of approximately 900 Million units annually sustain consistent NPU silicon demand.

North America

North America accounts for 28.7% of the Neural Processing Unit market in 2025, generating approximately USD 2.25 Billion. The United States is the dominant country within the region, housing the world's largest concentration of NPU chip designers including Qualcomm, Apple, NVIDIA, Intel, and AMD, as well as hyperscale cloud providers deploying custom NPU silicon at unprecedented scale. The CHIPS and Science Act's USD 52.7 Billion semiconductor investment commitment has catalyzed domestic fab expansion, with Intel's Ohio campus and TSMC's Arizona facility expected to begin advanced node production from 2026 onward, providing North American NPU developers with partial supply chain insulation from geopolitical risk. Canada contributes through AI research infrastructure at institutions including the Vector Institute and MILA, which generate intellectual property relevant to NPU algorithmic efficiency. The data center NPU sub-segment is proportionally largest in North America compared to other regions, reflecting the hyperscaler concentration in Virginia, Oregon, and Iowa. North America's Neural Processing Unit market is forecast to sustain a CAGR of 18.3% through 2034.

Europe

Europe holds a 16.4% share of the Neural Processing Unit market in 2025, generating USD 1.29 Billion. The region's strength lies in automotive-grade NPU applications, industrial AI, and semiconductor equipment supply chains rather than high-volume consumer silicon. Germany is the largest national market within Europe for NPU adoption, driven by automotive OEM deployments in BMW, Volkswagen, and Mercedes-Benz platforms requiring ADAS and autonomous driving AI silicon. The Netherlands, home to ASML, provides the extreme ultraviolet lithography equipment essential for manufacturing the sub-5nm nodes on which leading NPU designs depend. France and the United Kingdom contribute through AI research and NPU-adjacent semiconductor IP development. The European Chips Act, committing EUR 43 Billion through 2030, includes provisions supporting AI processor research and pilot fabrication facilities. The EU AI Act regulatory framework, which entered phased implementation in 2024, is indirectly driving NPU adoption by creating compliance requirements for AI systems that incentivize on-device inference over privacy-sensitive cloud processing. Europe's NPU market is forecast to grow at a CAGR of 17.1% through 2034.

Latin America

Latin America represents 7.1% of the global Neural Processing Unit market in 2025, with revenues of approximately USD 557 Million. Brazil is the dominant market within the region, accounting for over 45% of Latin American NPU-related device consumption, driven by strong smartphone penetration and a growing digital economy. Mexico serves as an important assembly and final-goods testing hub for consumer electronics destined for North American markets, with nearshoring trends creating incremental demand for NPU-equipped devices assembled locally. Colombia and Argentina represent emerging demand centers as affordable NPU-enabled smartphones penetrate middle-income consumer segments. Infrastructure constraints and currency volatility modestly temper growth rates, though the region's Neural Processing Unit market is still projected to expand at a CAGR of 16.8% through 2034. Government-backed digital transformation programs in Brazil and Mexico targeting industrial automation and smart city deployments represent a secondary demand driver for edge NPU platforms.

Middle East & Africa

The Middle East and Africa region accounts for 5.5% of the Neural Processing Unit market in 2025, representing approximately USD 432 Million. The United Arab Emirates leads within MEA, with Dubai and Abu Dhabi positioning themselves as AI hub destinations backed by sovereign wealth fund investment in AI infrastructure and government contracts for smart city applications requiring edge NPU processing. Saudi Arabia's Vision 2030 program includes explicit technology indigenization goals, with NEOM and related smart infrastructure projects creating demand for AI edge compute hardware. South Africa represents the largest sub-Saharan African market, with telecom operators and financial services firms among early adopters of NPU-accelerated AI workloads. The region's growth is constrained by limited local semiconductor manufacturing and hardware import dependencies, but the Neural Processing Unit market within MEA is projected to expand at a CAGR of 18.9% through 2034, supported by rapid 5G infrastructure buildout and increasing government AI mandates.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Edge NPU

- Cloud / Data Center NPU

- Automotive NPU

- Industrial & Medical NPU

By Application

- Consumer Electronics

- Data Center & Cloud Infrastructure

- Automotive & Transportation

- Industrial Robotics & Factory Automation

- Healthcare & Medical Imaging

By Node Technology

- Sub-5nm (3nm, 4nm)

- 5nm to 7nm

- 10nm and above

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.84 B |

| Forecast Revenue (2034) | USD 39.60 B |

| CAGR (2025-2034) | 19.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Edge NPU, Cloud / Data Center NPU, Automotive NPU, Industrial & Medical NPU), By Application, (Consumer Electronics, Data Center & Cloud Infrastructure, Automotive & Transportation, Industrial Robotics & Factory Automation, Healthcare & Medical Imaging), By Node Technology, (Sub-5nm (3nm, 4nm), 5nm to 7nm, 10nm and above) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | APPLE INC., QUALCOMM INCORPORATED, NVIDIA CORPORATION, MEDIATEK INC., SAMSUNG ELECTRONICS CO., LTD. (HISILICON / EXYNOS), HUAWEI TECHNOLOGIES CO., LTD. (HISILICON), INTEL CORPORATION, ARM HOLDINGS PLC, ADVANCED MICRO DEVICES, INC. (AMD), GOOGLE LLC (TENSOR / TPU), AMAZON WEB SERVICES (AWS TRAINIUM / INFERENTIA), MICROSOFT CORPORATION (MAIA / AZURE NPU), CAMBRICON TECHNOLOGIES CORPORATION LTD., BIREN TECHNOLOGY CO., LTD., MARVELL TECHNOLOGY, INC., TESLA, INC. (DOJO D1 / FSD CHIP), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Consumer Electronics, Cloud Infrastructure, Automotive, Robotics & Factory Automation, Healthcare Imaging), By Node Technology (Sub-5nm, 5nm–7nm, 10nm & Above), AI Semiconductor Trends & Forecast 2026-2034")

, By Application (Consumer Electronics, Cloud Infrastructure, Automotive, Robotics & Factory Automation, Healthcare Imaging), By Node Technology (Sub-5nm, 5nm–7nm, 10nm & Above), AI Semiconductor Trends & Forecast 2026-2034")

, By Application (Consumer Electronics, Cloud Infrastructure, Automotive, Robotics & Factory Automation, Healthcare Imaging), By Node Technology (Sub-5nm, 5nm–7nm, 10nm & Above), AI Semiconductor Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Neural Processing Unit Market?

Neural Processing Unit Market

Who are the major players in the Neural Processing Unit Market?

APPLE INC., QUALCOMM INCORPORATED, NVIDIA CORPORATION, MEDIATEK INC., SAMSUNG ELECTRONICS CO., LTD. (HISILICON / EXYNOS), HUAWEI TECHNOLOGIES CO., LTD. (HISILICON), INTEL CORPORATION, ARM HOLDINGS PLC, ADVANCED MICRO DEVICES, INC. (AMD), GOOGLE LLC (TENSOR / TPU), AMAZON WEB SERVICES (AWS TRAINIUM / INFERENTIA), MICROSOFT CORPORATION (MAIA / AZURE NPU), CAMBRICON TECHNOLOGIES CORPORATION LTD., BIREN TECHNOLOGY CO., LTD., MARVELL TECHNOLOGY, INC., TESLA, INC. (DOJO D1 / FSD CHIP), OTHERS

Which segments covered the Neural Processing Unit Market?

By Product Type, (Edge NPU, Cloud / Data Center NPU, Automotive NPU, Industrial & Medical NPU), By Application, (Consumer Electronics, Data Center & Cloud Infrastructure, Automotive & Transportation, Industrial Robotics & Factory Automation, Healthcare & Medical Imaging), By Node Technology, (Sub-5nm (3nm, 4nm), 5nm to 7nm, 10nm and above)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Neural Processing Unit Market

Published Date : 16 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date