- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Next Generation Sequencing Market Size, Share & Forecast | CAGR 21.5%

Global Next Generation Sequencing Market Size, Share, Analysis By Product Type (Consumables, Sample Preparation, Target Enrichment, Sequencing Platforms, Data Analysis), By Technology (Targeted Sequencing, Whole Genome Sequencing, Whole Exome Sequencing, RNA Sequencing), By Application (Oncology, Diagnostics, Reproductive Health, Infectious Diseases, Agrigenomics), By End-User, Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 12.5 Billion | USD 72.2 Billion | 21.5% | North America, 48.7% |

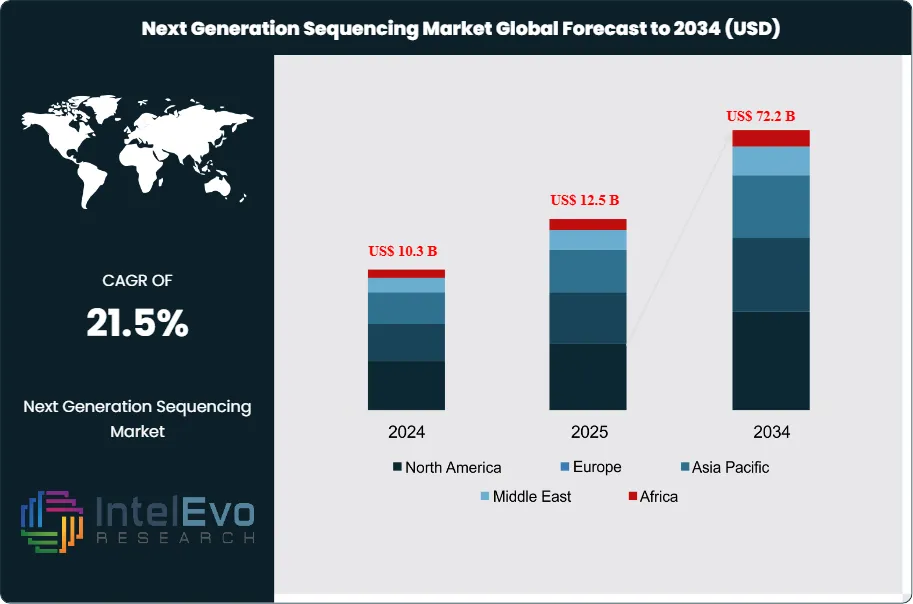

The Next Generation Sequencing Market is estimated at US$ 10.3 Billion in 2024 and is on track to reach roughly US$ 72.2 Billion by 2034, The market is further estimated to reach approximately US$ 12.5 Billion in 2025, and is expected to expand at a compound annual growth rate (CAGR) of around 21.5% during the forecast period from 2026 to 2034. Growth is driven by increasing adoption of precision medicine, rising demand for genomic sequencing in oncology and rare disease diagnostics, and expanding applications in clinical research, drug discovery, and agriculture. Additionally, advancements in sequencing technologies, declining sequencing costs, and integration of AI-driven bioinformatics are further accelerating market expansion globally.

Get More Information about this report -

Request Free Sample ReportThis expansion reflects a structural shift in how healthcare systems, life science firms, and public agencies generate and apply genomic data. Oncology remains the largest revenue engine, supported by higher cancer testing volumes and broader use of tumor profiling in treatment selection. Rare disease diagnostics, reproductive health screening, and infectious disease surveillance add durable demand. Payers and providers increasingly prioritize evidence-based pathways, which raises the value of sequencing when it reduces time to diagnosis or improves therapy alignment. Even with price declines per genome, total spending rises as test volumes grow and sequencing moves upstream into routine clinical workflows.

Supply-side capacity continues to scale through instrument installations, reagent supply, and lab automation. Leading vendors defend share through integrated platforms, long-term reagent contracts, and informatics ecosystems that reduce friction from sample to report. AI-enabled variant interpretation and automated quality control shorten analysis cycles and lower labor intensity, which supports higher throughput per lab. Digitalization also tightens chain-of-custody and auditability, which matters as laboratories expand decentralized testing networks. At the same time, the market faces ongoing constraints, including shortages of specialized bioinformatics talent, uneven reimbursement, and sensitivity to capital spending cycles at research institutes.

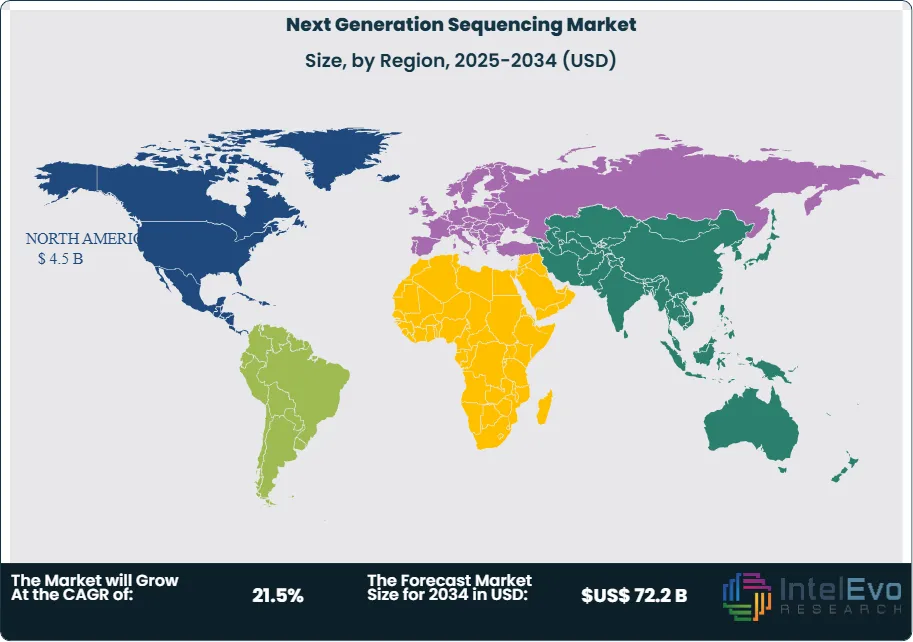

North America remains the profit center, capturing more than a 48.7% share and representing about US$ 5 billion in 2024 value, supported by strong biopharma R&D, clinical adoption, and established reimbursement channels. Europe follows with an estimated mid-20% share, aided by national genomics programs and hospital modernization. Asia Pacific shows the fastest momentum, with investment hotspots in China, India, Singapore, Japan, and South Korea as governments expand precision medicine budgets and local manufacturing capacity improves. Regulatory oversight will intensify around data privacy, cross-border data transfer, and validation standards for clinical-grade pipelines. Execution risk concentrates in compliance, cybersecurity, and evidentiary requirements for payer coverage, but scale efficiencies and software-led productivity gains sustain the decade-long growth trajectory.

, By Technology (Targeted Sequencing, Whole Genome Sequencing, Whole Exome Sequencing, RNA Sequencing), By Application (Oncology, Diagnostics, Reproductive Health, Infectious Diseases, Agrigenomics), By End-User, Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market generated 10.3 billion USD, 2024 and is projected to reach 72.2 billion USD, 2034, reflecting a 21.5% CAGR, 2024-2034.

- Segment Dominance : Consumables led the product type mix with 56.7%, 2023, supported by recurring reagent demand at scale.

- Segment Dominance: Targeted sequencing & resequencing held 38.5%, 2023, and oncology led applications with 35.5%, 2023, reinforcing focus on high-throughput clinical use cases.

- Driver: Sequencing dominated the workflow with 53.4%, 2023, as labs prioritize throughput and standardized run performance.

- Restraint: The market faced cost and data-processing constraints, estimated: 0.8 billion USD, 2024, in incremental informatics and storage burden across high-volume programs.

- Opportunity: Academic research held 38.8%, 2023, and expanding translational pipelines creates headroom, estimated: 12.0%, 2026, in incremental adoption within clinical research and biopharma programs.

- Trend: AI-enabled NGS data analysis adoption rises, estimated: 35.0%, 2025, as automation shortens interpretation cycles and improves variant triage.

- Regional Analysis: North America led with 48.7%, 2023, supported by high-capacity sequencing ecosystems and sustained funding, estimated: 4.5 billion USD, 2024, in regional spend.

Competitive Landscape

The Global Next Generation Sequencing (NGS) Market is moderately consolidated, with the top four players controlling an estimated 55.0%–62.0% of 2025 market revenue. Competition is technology-driven and platform-centric, where sequencing accuracy, throughput, cost per genome, and integration with bioinformatics ecosystems shape market share more than pricing alone. Competitive intensity increased in 2025–2026 as companies accelerated innovation in long-read sequencing, AI-driven analytics, and clinical-grade platforms, while strategic collaborations expanded access to large-scale genomics programs and precision medicine initiatives.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| ILLUMINA | US | Leader | High-throughput sequencing platforms and consumables | North America, Europe, Global | Expanded NovaSeq and clinical sequencing portfolio in 2025. |

| THERMO FISHER SCIENTIFIC | US | Leader | Ion Torrent sequencing systems and genomic solutions | North America, Europe, Asia | Strengthened clinical diagnostics and NGS workflow solutions in 2025. |

| BGI GROUP | China | Leader | Sequencing platforms and large-scale genomics services | Asia-Pacific, Global | Expanded global sequencing service capacity and partnerships in 2025. |

| ROCHE | Switzerland | Leader | Sequencing platforms and molecular diagnostics integration | Europe, North America | Advanced NGS-based diagnostics and companion diagnostic platforms in 2025. |

| OXFORD NANOPORE TECHNOLOGIES | UK | Challenger | Long-read sequencing and portable sequencing devices | Europe, North America | Expanded real-time sequencing and portable device adoption in 2025. |

| QIAGEN | Netherlands | Challenger | Sample prep, bioinformatics, and sequencing workflow solutions | Europe, Global | Strengthened bioinformatics and companion diagnostic capabilities in 2025. |

| BIO-RAD LABORATORIES | US | Challenger | Genomic analysis tools and PCR/NGS solutions | North America, Europe | Expanded digital PCR and genomic workflow integration in 2025. |

| EUROFINS SCIENTIFIC | Luxembourg | Challenger | Genomic testing and sequencing services | Europe, North America | Expanded clinical genomics and testing services globally in 2025. |

| PACIFIC BIOSCIENCES (PACBIO) | US | Niche Player | Long-read sequencing systems (HiFi sequencing) | North America | Advanced high-accuracy long-read sequencing platforms in 2025. |

| AGILENT TECHNOLOGIES | US | Niche Player | Sample preparation, target enrichment, and analytics tools | North America, Global | Strengthened NGS workflow and sample preparation solutions in 2025. |

Summary Insight:

The market is evolving toward high-throughput sequencing platforms, long-read technologies, and integrated bioinformatics ecosystems. Companies with strong platform innovation, consumables revenue models, and clinical validation capabilities are gaining share, while smaller players compete through niche technologies and specialized applications. Strategic collaborations in precision medicine and population genomics will define competitive positioning through 2034.

By Type

Consumables continue to account for the majority of revenue within the Next Generation Sequencing market, representing about 56.7 percent of total spending in recent assessments. Reagents, library preparation kits, flow cells, and cartridges drive this position because every sequencing run depends on recurring consumable usage. As sequencing volumes rise across clinical diagnostics and translational research, repeat purchasing outweighs one-time platform investments, anchoring steady cash flow for suppliers.

Ongoing progress in chemistry design, error reduction, and run efficiency has increased per-sample throughput while sustaining demand for higher-quality inputs. In clinical settings, consumables benefit from the expansion of molecular diagnostics, particularly in oncology panels and inherited disease testing. Platform systems remain essential, but replacement cycles are longer and capital budgets remain sensitive, which reinforces the structural advantage of consumables through 2030 and beyond.

By Application

Oncology remains the primary application area, accounting for roughly 35 to 38 percent of global NGS revenues in the mid-2020s. Sequencing supports tumor profiling, minimal residual disease monitoring, and therapy selection based on actionable mutations. The growth of precision oncology programs and an expanding pipeline of biomarker-driven trials continue to sustain high test volumes across solid tumors and hematologic cancers.

Beyond oncology, clinical investigation, reproductive health, and epidemiology show accelerating uptake. Infectious disease surveillance and drug development applications gained momentum after 2020 and remain embedded in public health strategies. Consumer genomics and agrigenomics contribute smaller but stable shares, supported by declining per-sample costs and broader awareness of genomic testing benefits.

By End-Use

Academic research institutions represent the largest end-user group, holding close to 38.8 percent share. Universities and publicly funded laboratories drive early-stage discovery, method development, and population-scale studies. Large cohort projects in cancer, rare diseases, and human genetics continue to generate sustained sequencing demand.

Clinical research organizations, hospitals, and biopharma companies are expanding faster in relative terms. Hospitals integrate sequencing into routine diagnostics, while pharmaceutical firms apply NGS across target discovery, companion diagnostics, and patient stratification. This shift signals a gradual rebalancing from discovery-focused usage toward regulated clinical and commercial environments.

By Region

North America leads the global market with about 48.7 percent share, supported by mature reimbursement frameworks, strong biopharma investment, and regulatory clarity around clinical sequencing. Federal funding and companion diagnostic approvals continue to support adoption across hospitals and reference laboratories, reinforcing regional scale advantages.

Asia Pacific is expected to post the highest growth rate through the forecast horizon. Government-backed genomics initiatives in China, Japan, South Korea, and India are expanding centralized sequencing capacity and local manufacturing. Europe maintains steady growth through national genomics programs, while Latin America and the Middle East and Africa show gradual progress driven by infectious disease monitoring and selective oncology investments.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Consumables

- Sample Preparation

- Target Enrichment

- Others

- Platform

- Sequencing

- Data Analysis

By Technology

- Targeted Sequencing & Resequencing

- DNA-based

- RNA-based

- WGS

- Whole Exome Sequencing

- Others

By Application

- Oncology

- Diagnostics and Screening

- Oncology Screening

- Companion Diagnostics

- Other Diagnostics

- Research Studies

- Consumer Genomics

- Clinical Investigation

- Infectious Diseases

- Inherited Diseases

- Idiopathic Diseases

- Non-Communicable/Other Diseases

- Reproductive Health

- NIPT

- Aneuploidy

- Microdeletions

- PGT

- Newborn Genetic Screening

- Single Gene Analysis

- HLA Typing/Immune System Monitoring

- Metagenomics, Epidemiology & Drug Development

- Agrigenomics & Forensics

By Workflow

- Sequencing

- NGS Data Analysis

- Pre-Sequencing

- NGS Library Preparation Kits

- Semi-automated Library Preparation

- Automated Library Preparation

By End-user

- Academic Research

- Clinical Research

- Hospitals & Clinics

- Pharma & Biotech Entities

- Other Users

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | US$ 12.5 B |

| Forecast Revenue (2034) | US$ 72.2 B |

| CAGR (2025-2034) | 21.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Consumables, Platform), By Technology, (Targeted Sequencing & Resequencing, WGS, Whole Exome Sequencing, Others), By Application, (Oncology, Diagnostics and Screening, Research Studies, Consumer Genomics, Clinical Investigation, Infectious Diseases, Inherited Diseases, Idiopathic Diseases, Non-Communicable/Other Diseases, Reproductive Health, Single Gene Analysis, HLA Typing/Immune System Monitoring, Metagenomics, Epidemiology & Drug Development, Agrigenomics & Forensics), By Workflow, (Sequencing, NGS Data Analysis, Pre-Sequencing), By End-user, (Academic Research, Clinical Research, Hospitals & Clinics, Pharma & Biotech Entities, Other Users) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Illumina, BGI, Thermo Fisher Scientific, Inc., Oxford Nanopore Technologies, Hoffman-La Roche Ltd, Bio-Rad Laboratories, Inc., QIAGEN, Eurofins GATC Biotech GmbH, PierianDx, Genomatix GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Targeted Sequencing, Whole Genome Sequencing, Whole Exome Sequencing, RNA Sequencing), By Application (Oncology, Diagnostics, Reproductive Health, Infectious Diseases, Agrigenomics), By End-User, Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

, By Technology (Targeted Sequencing, Whole Genome Sequencing, Whole Exome Sequencing, RNA Sequencing), By Application (Oncology, Diagnostics, Reproductive Health, Infectious Diseases, Agrigenomics), By End-User, Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

, By Technology (Targeted Sequencing, Whole Genome Sequencing, Whole Exome Sequencing, RNA Sequencing), By Application (Oncology, Diagnostics, Reproductive Health, Infectious Diseases, Agrigenomics), By End-User, Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Next Generation Sequencing Market?

The Global Next Generation Sequencing Market was valued at US$ 12.5 Billion in 2025, projected to hit US$ 72.2 Billion by 2034, growing at a CAGR of 21.5% from 2026–2034, driven by precision medicine, oncology diagnostics, and advancements in genomic technologies.

Who are the major players in the Next Generation Sequencing Market?

Illumina, BGI, Thermo Fisher Scientific, Inc., Oxford Nanopore Technologies, Hoffman-La Roche Ltd, Bio-Rad Laboratories, Inc., QIAGEN, Eurofins GATC Biotech GmbH, PierianDx, Genomatix GmbH

Which segments covered the Next Generation Sequencing Market?

By Product Type, (Consumables, Platform), By Technology, (Targeted Sequencing & Resequencing, WGS, Whole Exome Sequencing, Others), By Application, (Oncology, Diagnostics and Screening, Research Studies, Consumer Genomics, Clinical Investigation, Infectious Diseases, Inherited Diseases, Idiopathic Diseases, Non-Communicable/Other Diseases, Reproductive Health, Single Gene Analysis, HLA Typing/Immune System Monitoring, Metagenomics, Epidemiology & Drug Development, Agrigenomics & Forensics), By Workflow, (Sequencing, NGS Data Analysis, Pre-Sequencing), By End-user, (Academic Research, Clinical Research, Hospitals & Clinics, Pharma & Biotech Entities, Other Users)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Next Generation Sequencing Market

Published Date : 26 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date