- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

North America Generative AI in Insurance Market Size & Forecast | 33.1% CAGR

North America Generative AI in Insurance Market Size, Share, Industry Analysis By Component (Solutions, Services), By Deployment (Cloud-Based, On-Premise), By Application (Claims Processing, Underwriting Automation, Customer Service, Fraud Detection, Risk Assessment, Document Extraction & Classification), By Enterprise Size (Large Enterprises, SMEs), Regional Insights, Competitive Landscape, Market Dynamics, Strategic Developments & Forecast 2025–2034

Report Overview

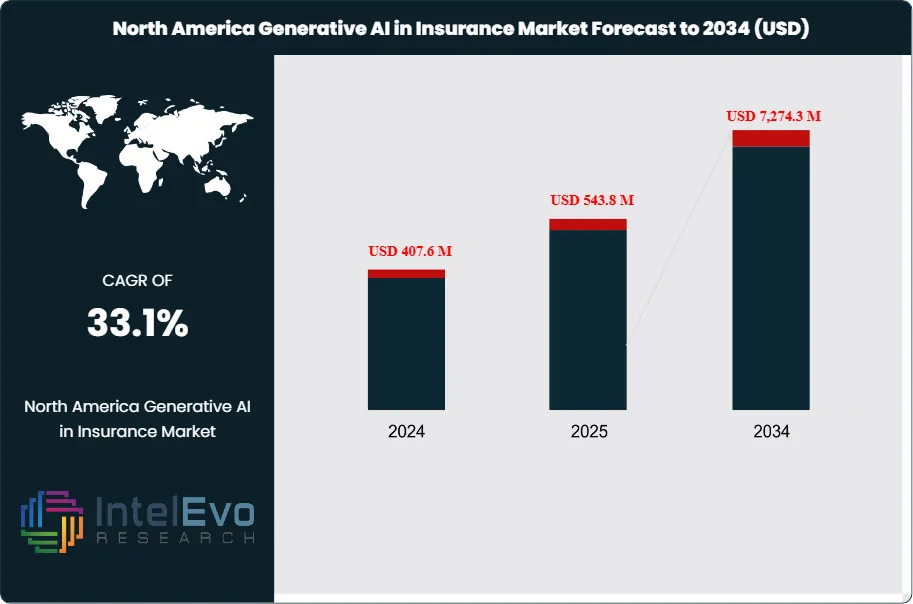

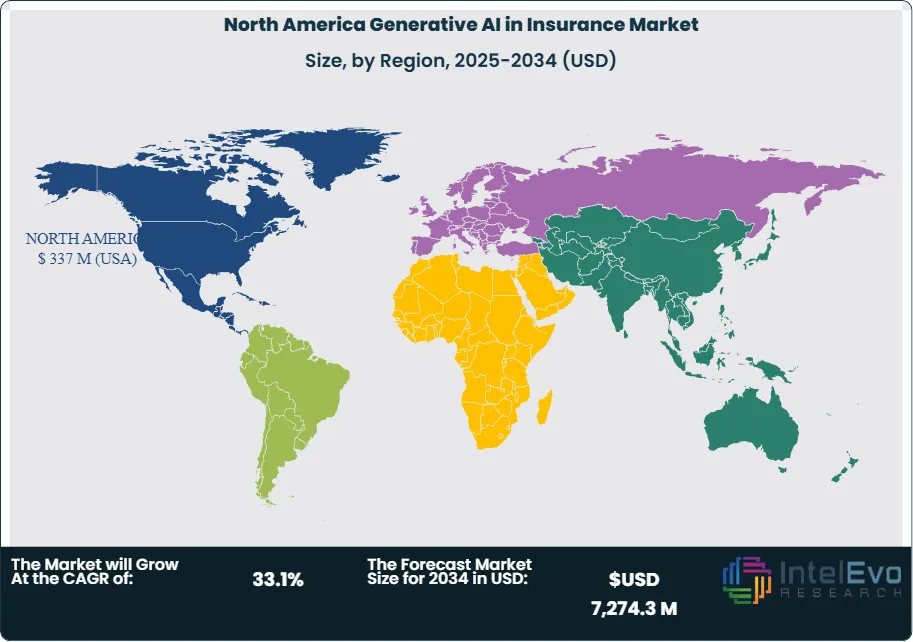

The North America Generative AI in Insurance Market was valued at USD 407.6 Million in 2024 and is projected to reach approximately USD 7,274.3 Million by 2034. The market is estimated to grow to around USD 543.8 Million in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 33.1% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportGenerative AI is shifting from proofs of concept to scaled deployments across underwriting, claims, and customer engagement in North American insurers. Carriers use large language and multimodal models to structure unstructured data, draft policy and claims communications, and simulate loss scenarios for faster decisions. In 2024, the U.S. held a dominant regional position with a 33.2% share and USD 377.5 million in revenue, reflecting high digital adoption and sustained investment in data platforms. The region also benefits from a dense ecosystem of insurtechs and cloud providers that accelerates implementation and shortens time-to-value.

Demand rises as insurers confront rising claim complexity, higher fraud pressure, and tighter expectations for personalized products. Generative AI reduces manual effort in intake, document review, and adjuster workflows, and it supports more granular risk assessment for tailored pricing and coverage design. Global benchmarks reinforce the trajectory: the generative AI in insurance market is projected to expand from USD 731.7 million in 2023 to about USD 13,862.7 million by 2033, at a 34.2% CAGR, with North America holding more than 43.75% of share in 2023. Cloud-based deployments lead because they scale compute on demand, speed integration through managed services, and simplify model updates across distributed operations.

Regulatory and governance factors now shape adoption curves. State-level insurance oversight, privacy obligations, and emerging AI guidance are driving stricter model risk management, audit trails, and documented human review for high-impact use cases such as underwriting and claims decisions. Execution risk remains material. Insurers must control hallucinated outputs, data leakage, bias exposure, and third-party concentration, while managing inference costs as usage scales. Security teams also face new attack surfaces, including prompt injection and data exfiltration routes in agentic workflows.

Investment momentum is concentrating in U.S. and Canadian technology corridors where carriers partner with hyperscalers and specialist vendors to build secure, compliant pipelines. Near-term spending is clustering around claims automation, fraud detection, and agent-assist copilots, where productivity gains and loss reduction can fund broader modernization. Over the forecast period, competitive outcomes will depend on proprietary data quality, governance discipline, and the ability to operationalize generative AI alongside automation and digital distribution at scale.

, By Deployment (Cloud-Based, On-Premise), By Application (Claims Processing, Underwriting Automation, Customer Service, Fraud Detection, Risk Assessment, Document Extraction & Classification), By Enterprise Size (Large Enterprises, SMEs), Regional Insights, Competitive Landscape, Market Dynamics, Strategic Developments & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 407.6 million USD, 2024 to 7,274.3 million USD, 2034, delivering 33.4% CAGR, 2024-2034. The U.S. scales from 337.5 million USD, 2024 to 5,933.7 million USD, 2034, sustaining 33.2% CAGR, 2024-2034.

- Segment Dominance : Solutions lead at 65.7% share, 2024 as insurers deploy AI chatbots and automation toolkits. This segment reaches estimated: 4,778.2 million USD, 2034 based on share carry-forward from 7,274.3 million USD, 2034.

- Segment Dominance: Cloud-based deployments command 73.5% share, 2024 as carriers prioritize scalable infrastructure and real-time analytics. Cloud reaches estimated: 5,346.6 million USD, 2034 based on share carry-forward from 7,274.3 million USD, 2034.

- Driver: Insurers accelerate adoption to automate claims, underwriting, and fraud workflows as the market runs at 33.4% CAGR, 2024-2034. The U.S. market lifts from 449.5 million USD, 2025 to 5,933.7 million USD, 2034 as deployments scale.

- Restraint: On-premise share contracts from 26.9% share, 2024 to 26.5% share, estimated: 2025-2034 as organizations shift budgets toward cloud. On-premise footprint still equals estimated: 1,927.2 million USD, 2034 assuming 26.5% of 7,274.3 million USD, 2034.

- Opportunity: SMEs grow from 30.5% share, 2024 to 30.8% share, estimated: 2025-2034 as packaged solutions lower adoption barriers. SMEs represent estimated: 2,240.5 million USD, 2034 assuming 30.8% of 7,274.3 million USD, 2034.

- Trend: Claims processing remains a primary use case at 25.7% share, 2024 as generative AI speeds adjudication and flags fraud. This use case reaches estimated: 1,869.5 million USD, 2034 assuming 25.7% of 7,274.3 million USD, 2034.

- Regional Analysis: The U.S. anchors regional scale at 337.5 million USD, 2024 and reaches 5,933.7 million USD, 2034, indicating sustained leadership. The remaining North America market equals estimated: 1,340.6 million USD, 2034 (7,274.3 million USD, 2034 minus 5,933.7 million USD, 2034).

By Component

In 2025 and beyond, solutions continue to account for the majority of spending in the North American generative AI in insurance market, representing about 65.7 percent of total revenue in 2024. Core demand centers on end-to-end platforms that automate claims intake, underwriting workflows, fraud screening, and customer interaction. Insurers prioritize solutions because they deliver direct productivity gains and measurable cost reduction across high-volume processes.

These platforms rely on large language models, machine learning, and natural language processing to analyze structured and unstructured data at scale. As a result, carriers achieve tighter risk selection, more consistent pricing, and faster policy issuance. Market data indicate that insurers deploying generative AI solutions report processing time reductions of 30 to 40 percent in claims-heavy lines by early 2025.

Services, including integration, model training, governance, and support, form the remaining share. Their role is expanding as regulatory scrutiny increases and insurers require stronger controls, auditability, and human review mechanisms to support production use.

By Deployment

Cloud-based deployment dominates the market, accounting for roughly 73.5 percent of total share in 2024, and this lead is expected to widen through 2034. Insurers favor cloud environments for rapid deployment, elastic compute access, and lower capital expenditure. These attributes align with the computational intensity of generative AI workloads and ongoing model updates.

Cloud platforms also enable real-time data ingestion from policy, claims, and third-party sources, which supports continuous learning and scenario modeling. By 2025, most tier-one insurers in the U.S. operate hybrid or cloud-first AI architectures. On-premise deployments are gradually declining, with share easing from about 26.9 percent in 2024 toward 26.5 percent as legacy systems phase out.

By Application

Claims processing leads application adoption, holding approximately 25.7 percent market share in 2024. Generative AI shortens settlement cycles, improves document classification accuracy, and flags anomalies linked to fraud. Several large insurers report double-digit reductions in claims leakage after deploying AI-assisted review systems.

Underwriting and fraud detection follow closely, driven by the need for faster risk evaluation and tighter loss control. Customer service adoption also rises steadily as virtual agents manage policy inquiries and status updates, reducing call center volumes by an estimated 20 percent by 2025.

By Enterprise Size

Large enterprises account for about 69.2 percent of market revenue, reflecting stronger budgets, broader data assets, and complex operational needs. These insurers deploy AI across multiple lines and geographies, supporting consistent decision-making at scale.

SMEs hold a smaller but rising share, increasing from roughly 30.5 percent in 2024. Adoption improves as cloud-based offerings lower entry costs and reduce implementation timelines.

By Region

The U.S. remains the regional anchor, generating over USD 337 million in 2024 and projected to exceed USD 5.9 billion by 2034. Canada follows with steady growth, supported by digital insurance penetration and regulatory clarity. Across North America, investment concentrates on claims automation and fraud mitigation, positioning the region as a global reference market through the forecast period.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Solutions

- Services

By Deployment

- On-Premise

- Cloud-based

By Application

- Claims Processing

- Underwriting

- Customer Service

- Fraud Detection

- Risk Assessment

- Document Extraction & Classification

- Others

By Enterprise Size

- Large Enterprises

- SMEs

Regions

- North America

- USA

- Canada

- Mexico

| Report Attribute | Details |

| Market size (2025) | USD 543.8 M |

| Forecast Revenue (2034) | USD 7,274.3 M |

| CAGR (2025-2034) | 33.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Solutions, Services), By Deployment (On-Premise, Cloud-based), By Application (Claims Processing, Underwriting, Customer Service, Fraud Detection, Risk Assessment, Document Extraction & Classification, Others), By Enterprise Size (Large Enterprises, SMEs) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Shift Technology, Appian, GEICO, Snorkel, Hexaware, Lemonade, Sixfold, AWS Marketplace |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-Based, On-Premise), By Application (Claims Processing, Underwriting Automation, Customer Service, Fraud Detection, Risk Assessment, Document Extraction & Classification), By Enterprise Size (Large Enterprises, SMEs), Regional Insights, Competitive Landscape, Market Dynamics, Strategic Developments & Forecast 2025–2034")

, By Deployment (Cloud-Based, On-Premise), By Application (Claims Processing, Underwriting Automation, Customer Service, Fraud Detection, Risk Assessment, Document Extraction & Classification), By Enterprise Size (Large Enterprises, SMEs), Regional Insights, Competitive Landscape, Market Dynamics, Strategic Developments & Forecast 2025–2034")

, By Deployment (Cloud-Based, On-Premise), By Application (Claims Processing, Underwriting Automation, Customer Service, Fraud Detection, Risk Assessment, Document Extraction & Classification), By Enterprise Size (Large Enterprises, SMEs), Regional Insights, Competitive Landscape, Market Dynamics, Strategic Developments & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

North America Generative AI in Insurance Market

Published Date : 04 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date