- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Offshore Decommissioning Services Market Size, Share | CAGR 7.8%

Global Offshore Decommissioning Services Market Size, Share, Growth Analysis By Service Type (Well Plugging & Abandonment, Subsea Infrastructure Removal, Topside Removal, Jacket & Foundation Removal), By Structure (Topside, Substructure, Jackets, Pipelines & Umbilicals), By Water Depth (Shallow, Deepwater, Ultra-Deepwater), By Removal Mode, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 8.52 Billion | USD 16.75 Billion | 7.8% | Europe, 49.7% |

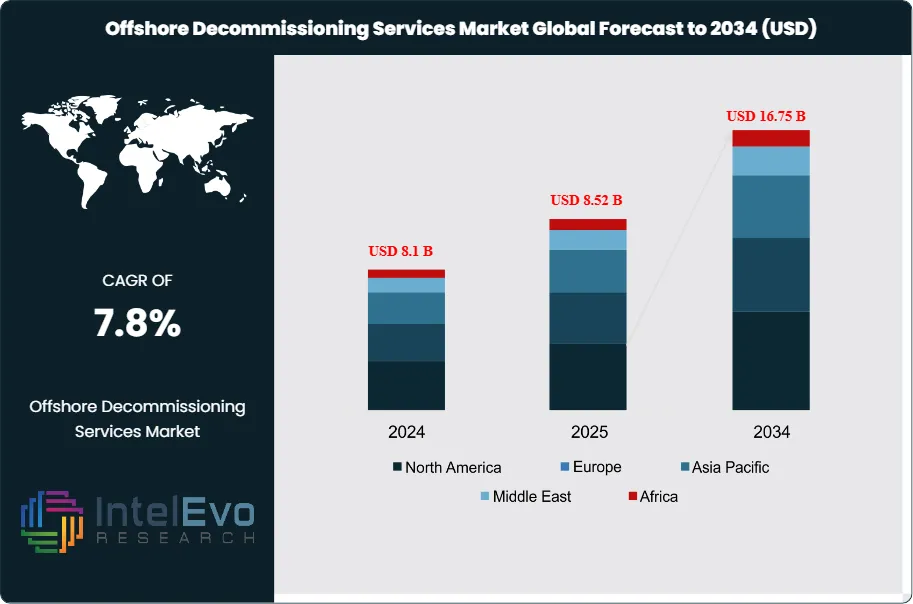

The Global Offshore Decommissioning Services Market was valued at approximately USD 8.1 Billion in 2024 and increased to USD 8.52 Billion in 2025. The market is projected to reach nearly USD 16.75 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 7.8% during the forecast period from 2026 to 2034. Published market estimates vary because some providers include broader offshore decommissioning scope, while others isolate service revenue only. This report uses the USD 8.52 Billion, 2025 base and a USD 16.75 Billion, 2034 forecast because that pair is mathematically consistent with a 7.8% nine-year CAGR.

Get More Information about this report -

Request Free Sample ReportThe offshore decommissioning services market is moving from a niche late-life activity to a major capital program across mature offshore basins. Europe remains the core revenue center because the North Sea has the oldest and densest concentration of offshore infrastructure now moving into end-of-life planning. The North Sea Transition Authority said in July 2025 that UK Continental Shelf decommissioning spend is forecast at GBP 27 billion across 2023-2032, up GBP 3 billion from the prior update. That cost inflation is lifting demand for specialist engineering, heavy lift, well plugging and abandonment, subsea removal, recycling, and project management services.

North America remains the second-largest offshore decommissioning services market because the Gulf of Mexico holds a large inventory of aging assets and delayed removal obligations. BSEE says about 75% of the 1,430 existing OCS platforms are more than 25 years old and that the industry has averaged 127 platform removals per year over the past decade. GAO found that, as of June 2023, more than 2,700 wells and 500 platforms in the Gulf of Mexico were overdue for decommissioning. Those figures keep regulatory pressure high for plugging, abandonment, and structure removal.

Asia Pacific is the fastest-rising offshore decommissioning services market. Australia’s NOPSEMA is running a five-year decommissioning compliance strategy, while ExxonMobil’s Esso Australia awarded Allseas a Bass Strait campaign to remove up to 12 retired platforms with combined weight of about 60,000 tonnes. Latin America is supported by Petrobras plans, even after the company cut 2025-2029 decommissioning investment to USD 9.9 billion. The Middle East and Africa remain smaller today, but new work is forming, including QatarEnergy’s first major offshore decommissioning initiative. Across all regions, automation, robotics, digital twins, subsea inspection tools, and high-capacity single-lift vessels are reducing offshore time, tightening safety control, and improving recovery rates.

, By Structure (Topside, Substructure, Jackets, Pipelines & Umbilicals), By Water Depth (Shallow, Deepwater, Ultra-Deepwater), By Removal Mode, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The offshore decommissioning services market stands at USD 8.52 Billion, 2025 and is projected to reach USD 16.75 Billion, 2034 at a 7.8% CAGR across 2026-2034 under this report’s normalized services model.

- Segment Dominance: Well plugging and abandonment is the largest service segment with 34.2% share, equal to about USD 2.91 Billion, 2025.

- Segment Dominance: Topside-related work is the largest structure-led application segment with 47.8% share, or about USD 4.07 Billion, 2025.

- Driver: The main driver is mandatory retirement of aging offshore infrastructure. About 75% of existing OCS platforms are more than 25 years old, and more than 2,700 wells and 500 Gulf platforms were overdue for decommissioning as of June 2023.

- Restraint: The main restraint is cost inflation and schedule complexity. UKCS decommissioning spend expectations for 2023-2032 rose to GBP 27 billion in 2025, up GBP 3 billion from the prior update.

- Opportunity: The largest opportunity sits in long-cycle basin programs rather than isolated removals. Global decommissioning spend is expected to reach USD 103 billion over 2025-2034.

- Trend: The strongest trend is integrated heavy-lift and recycling execution. Allseas markets single-lift topside capacity up to 60,000 tonnes and jacket capacity up to 20,000 tonnes, while Aker Solutions reported a 98.5% recycling rate on the Gyda project in 2025.

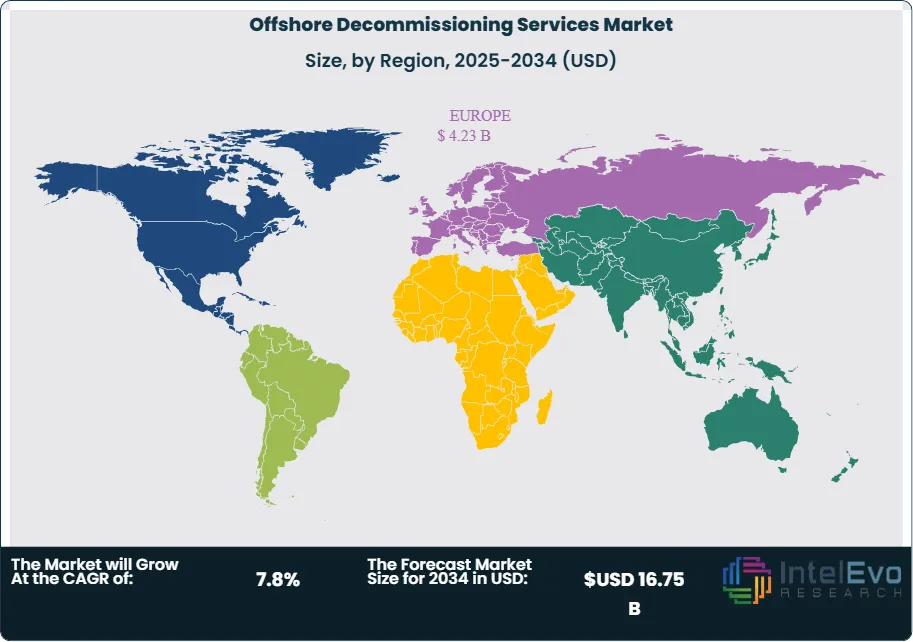

- Regional Analysis: Europe leads the offshore decommissioning services market with 49.7% share and USD 4.23 Billion revenue, 2025.

Market Competitive Landscape

The offshore decommissioning services market is fragmented to moderately consolidated. The top four players account for an estimated 33.5% of 2025 revenue. Competition is capability-driven and geographic rather than price-led because operators buy around heavy-lift capacity, P&A execution depth, subsea spread access, basin permits, and recycling routes. Competitive intensity increased in 2025 and early 2026 as Allseas secured Australia’s largest offshore removal campaign, Saipem and Subsea7 advanced their merger plan, Heerema won bp’s Andrew platform removal contract, and AF Offshore Decom added a new North Sea recycling award.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| ALLSEAS | Switzerland | Leader | Pioneering Spirit single-lift decommissioning | Europe, Asia Pacific | Won Esso Australia contract in Dec 2024 to remove up to 12 Bass Strait platforms totaling about 60,000 tonnes |

| SUBSEA7 | United Kingdom | Leader | Subsea decommissioning and seabed clearance services | Europe, North America | Won Ithaca Energy decommissioning scope offshore UK in Dec 2025 covering pipeline flushing, DSV services, and seabed clearance |

| SAIPEM | Italy | Leader | Integrated offshore decommissioning engineering and removal | Europe, Middle East | Confirmed merger path with Subsea7 in Jul 2025 to create Saipem7 |

| HEEREMA | Netherlands | Challenger | Heavy-lift platform removal and EPR services | Europe | Won bp Andrew platform topside and jacket removal contract in Oct 2025 |

| AKER SOLUTIONS | Norway | Challenger | Decommissioning and recycling execution | Europe | Completed Gyda decommissioning in Mar 2025 with 28,000 tonnes dismantled and 98.5% recycling rate |

| AF OFFSHORE DECOM | Norway | Challenger | Onshore dismantling and recycling platform | Europe | Won Ithaca Energy FSU dismantling and recycling contract in Feb 2026 for a 24,000-tonne unit |

| BOSKALIS | Netherlands | Challenger | End-to-end offshore decommissioning and subsea removal | Europe, Middle East | Launched The Decommissioning Collective in Feb 2026 for North Sea subsea campaigns |

| MCDERMOTT | United States | Niche Player | Offshore decommissioning definition engineering | Middle East | Won QatarEnergy’s first major offshore decommissioning definition engineering contract in Feb 2026 |

| OCEANEERING | United States | Niche Player | Decommissioning support, vessel and subsea services | Europe, Latin America | Added vessel services work in 2025 and multiple UK North Sea decommissioning scopes |

| TECHNIPFMC | United Kingdom | Niche Player | Subsea engineering and decommissioning support | Latin America, North America | Extended long-term Petrobras-linked contracts in 2025 covering decommissioning and subsea work |

Analysis by Service

Well plugging and abandonment leads the offshore decommissioning services market by service with 34.2% share, or USD 2.91 Billion, 2025. This reflects the fact that every field retirement starts with permanent well isolation and regulators treat overdue wells as the highest-risk backlog. Subsea infrastructure removal follows at 27.8%, or USD 2.37 Billion, 2025, because pipelines, umbilicals, manifolds, and seabed hardware create long-tail offshore work after wells are secured. Topside removal accounts for 20.6%, or USD 1.76 Billion, 2025, while jacket and foundation removal represents 17.4%, or USD 1.48 Billion, 2025. Competitive strength differs by subsegment. Subsea7, Saipem, and TechnipFMC are stronger in subsea spreads and engineering-intensive scopes, while Allseas and Heerema dominate the heaviest lift campaigns. Aker Solutions and AF Offshore Decom are stronger once offshore removal transfers into dismantling and recycling yards.

Analysis by Structure

Topside structures form the largest structure-based revenue block in the offshore decommissioning services market with 47.8% share, or USD 4.07 Billion, 2025. Sub-infrastructure, including subsea trees, manifolds, risers, umbilicals, and associated field architecture, holds 28.7%, or USD 2.45 Billion, 2025. Jackets account for 14.3%, or USD 1.22 Billion, 2025, while pipelines and umbilicals represent 9.2%, or USD 0.78 Billion, 2025. This split explains why Europe dominates the market. Mature North Sea developments contain large topsides and dense subsea tie-back systems that require multi-year campaigns rather than simple removals. Single-lift vessels matter commercially because they reduce offshore duration and weather exposure on large integrated removals.

Analysis by Water Depth

Shallow-water projects dominate the offshore decommissioning services market by water depth with 58.1% share, or USD 4.95 Billion, 2025. Deepwater accounts for 24.9%, or USD 2.12 Billion, 2025, while ultra-deepwater represents 17.0%, or USD 1.45 Billion, 2025. The earliest offshore oil and gas fields were developed in shallow water, especially in the North Sea, Gulf of Mexico, and parts of Asia Pacific. Those fields now form the largest retirement backlog. Deepwater and ultra-deepwater remain smaller in current share but more technically demanding, especially for subsea wells, floating systems, and long tie-back infrastructure.

Analysis by Removal Mode

Complete removal is the largest removal-mode segment in the offshore decommissioning services market with 61.4% share, or USD 5.23 Billion, 2025. Partial removal represents 23.6%, or USD 2.01 Billion, 2025, while rigs-to-reefs and alternative end-state solutions represent 15.0%, or USD 1.28 Billion, 2025. Complete removal favors heavy-lift, P&A, and yard-recycling specialists. Partial removal and reefing favor engineering-led scopes, seabed studies, and regulatory strategy. The result is a market where policy detail can shift service mix even when total spending remains high.

Regional Analysis

North America

North America accounts for 22.4% of the offshore decommissioning services market, equal to USD 1.91 Billion, 2025. The United States dominates the region because the Gulf of Mexico has a large backlog of overdue offshore retirement work. About 75% of the 1,430 existing OCS platforms are more than 25 years old, and more than 2,700 wells and 500 platforms in the Gulf of Mexico were overdue for decommissioning as of June 2023. The United States represents about 82% of the North American market in 2025, Canada about 11%, Mexico about 5%, and the rest of North America about 2%. The region favors contractors with subsea intervention spreads, regulatory familiarity, and strong P&A capability.

Europe

Europe leads the offshore decommissioning services market with 49.7% share and USD 4.23 Billion revenue, 2025. The UK is the largest single country market in Europe, followed by Norway. Germany and France are smaller direct offshore decommissioning markets, but both matter through engineering, fabrication, recycling, marine logistics, and industrial service supply. The UK represents about 52% of Europe’s offshore decommissioning services revenue in 2025, Norway about 24%, Germany about 8%, France about 5%, and the rest of Europe about 11%. Europe hosts the strongest contractor cluster, including Allseas, Heerema, Saipem, Subsea7, Aker Solutions, AF Offshore Decom, and Boskalis.

Asia Pacific

Asia Pacific holds 16.8% of the offshore decommissioning services market, equal to USD 1.43 Billion, 2025. Australia is the main driver. NOPSEMA is implementing a five-year decommissioning compliance strategy, and Esso Australia awarded Allseas a contract in December 2024 to remove up to 12 retired platforms in Bass Strait with combined weight of approximately 60,000 tonnes. Australia accounts for about 39% of regional revenue, India 22%, China 20%, Japan 9%, and the rest of Asia Pacific 10% in 2025. Asia Pacific growth is being shaped by first-wave regulation, large single-client programs, and rising yard capacity.

Latin America

Latin America represents 6.0% of the offshore decommissioning services market, or USD 0.51 Billion, 2025. Brazil is the clear regional leader because Petrobras controls the largest late-life offshore asset base in the region. Petrobras reduced planned 2025-2029 decommissioning investment to USD 9.9 billion and cut the number of targeted platforms from 23 to 10, yet the addressable market remains large. Brazil represents about 71% of Latin America’s offshore decommissioning services revenue in 2025, Mexico about 17%, Argentina about 7%, and the rest of Latin America about 5%.

Middle East & Africa

The Middle East & Africa account for 5.2% of the offshore decommissioning services market, equal to USD 0.44 Billion, 2025. Saudi Arabia is the largest country market in the region in 2025, followed by the UAE and South Africa, while Qatar becomes the fastest-rising project center from a low base. Saudi Arabia accounts for about 28% of MEA revenue, the UAE 16%, South Africa 12%, Qatar 10%, and the rest of MEA 34%. The region’s service demand is still early-stage, which favors engineering, planning, and regulatory-support work before large physical removal cycles reach scale.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service

- Well Plugging and Abandonment

- Subsea Infrastructure Removal

- Topside Removal

- Jacket and Foundation Removal

By Structure

- Topside Structures

- Sub-Infrastructure

- Jackets

- Pipelines and Umbilicals

By Water Depth

- Shallow Water

- Deepwater

- Ultra-Deepwater

By Removal Mode

- Complete Removal

- Partial Removal

- Rigs-to-Reefs and Alternative End-State

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.52 B |

| Forecast Revenue (2034) | USD 16.75 B |

| CAGR (2025-2034) | 7.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service, (Well Plugging and Abandonment, Subsea Infrastructure Removal, Topside Removal, Jacket and Foundation Removal), By Structure, (Topside Structures, Sub-Infrastructure, Jackets, Pipelines and Umbilicals), By Water Depth, (Shallow Water, Deepwater, Ultra-Deepwater), By Removal Mode, (Complete Removal, Partial Removal, Rigs-to-Reefs and Alternative End-State) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ALLSEAS, SUBSEA7, SAIPEM, HEEREMA, AKER SOLUTIONS, AF OFFSHORE DECOM, BOSKALIS, MCDERMOTT, OCEANEERING, TECHNIPFMC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Structure (Topside, Substructure, Jackets, Pipelines & Umbilicals), By Water Depth (Shallow, Deepwater, Ultra-Deepwater), By Removal Mode, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Structure (Topside, Substructure, Jackets, Pipelines & Umbilicals), By Water Depth (Shallow, Deepwater, Ultra-Deepwater), By Removal Mode, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Structure (Topside, Substructure, Jackets, Pipelines & Umbilicals), By Water Depth (Shallow, Deepwater, Ultra-Deepwater), By Removal Mode, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Offshore Decommissioning Services Market?

The Global Offshore Decommissioning Services Market was valued at USD 8.52 Billion in 2025, projected to reach USD 16.75 Billion by 2034, growing at a CAGR of 7.8% from 2026–2034, driven by aging offshore assets, strict regulations, and rising investments in decommissioning and infrastructure removal.

Who are the major players in the Offshore Decommissioning Services Market?

ALLSEAS, SUBSEA7, SAIPEM, HEEREMA, AKER SOLUTIONS, AF OFFSHORE DECOM, BOSKALIS, MCDERMOTT, OCEANEERING, TECHNIPFMC, Others

Which segments covered the Offshore Decommissioning Services Market?

By Service, (Well Plugging and Abandonment, Subsea Infrastructure Removal, Topside Removal, Jacket and Foundation Removal), By Structure, (Topside Structures, Sub-Infrastructure, Jackets, Pipelines and Umbilicals), By Water Depth, (Shallow Water, Deepwater, Ultra-Deepwater), By Removal Mode, (Complete Removal, Partial Removal, Rigs-to-Reefs and Alternative End-State)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Offshore Decommissioning Services Market

Published Date : 23 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date