- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Offshore Drilling Rig Market Size, Share & Growth Analysis | CAGR 5.6%

Global Offshore Drilling Rig Market Size, Share, Analysis By Rig Type (Jack-Up Rigs, Drillships, Semisubmersibles, Tender Rigs and Others), By Water Depth Application (Shallow-Water, Deepwater, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug & Abandonment, Intervention Support), By Contract Structure (Standard Dayrate, Performance-Linked & Integrated Contracts, Managed & Hybrid Models) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Technology Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

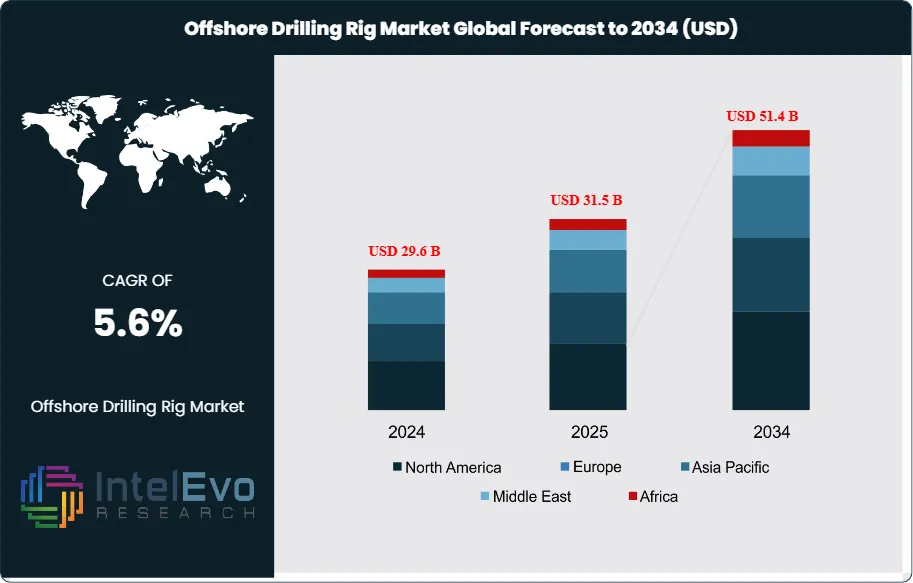

| USD 31.5 Billion, 2025 | USD 51.4 Billion, 2034 | 5.6%, 2026–2034 | APAC, 29.0%, 2025 |

The Offshore Drilling Rig Market was valued at approximately USD 29.6 Billion in 2024 and increased to USD 31.5 Billion in 2025. The market is projected to reach nearly USD 51.4 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.6% during the forecast period from 2026 to 2034. Market growth is primarily driven by increasing offshore exploration and production activities, particularly in deepwater and ultra-deepwater regions, along with rising global energy demand. Additionally, advancements in drilling technologies, increasing investments in offshore oil and gas projects, and the development of new offshore reserves in regions such as Brazil, West Africa, and the Gulf of Mexico are expected to further support market expansion.

Get More Information about this report -

Request Free Sample ReportThe Offshore Drilling Rig Market entered 2025 with firmer long-cycle demand than most onshore rig segments. The market is supported by deepwater field development in Brazil, West Africa, the U.S. Gulf, and selected harsh-environment activity in Norway and the North Atlantic. The market also benefits from gas-led offshore campaigns in Southeast Asia and the Middle East. This report models the Offshore Drilling Rig Market on rig contract revenue, fleet utilization, and offshore project sanction momentum in 2025. The market remains cyclical, but the current cycle rests on tighter supply of premium drillships and harsh-environment floaters than in prior upturns. Transocean reported USD 4.0 Billion in 2025 contract drilling revenue, Noble reported USD 3.3 Billion, and Seadrill added USD 0.5 Billion of new backlog across seven rigs heading into 2026. These figures confirm that offshore rig demand stayed commercially relevant despite softer pockets in parts of the floater market.

The Offshore Drilling Rig Market in 2025 was shaped by two opposing forces. On the demand side, national oil companies and supermajors continued to back offshore supply security, deepwater reserve replacement, and large gas developments. Rystad Energy estimated about USD 50 Billion of conventional project sanctions in the Middle East in 2025 alone. Reuters also reported USD 1.5 Billion of planned ExxonMobil deepwater spending in Nigeria and rising U.S. Gulf output to 1.89 million barrels per day in 2025. On the supply side, contractors faced softer 2025 dayrates than 2024 in some segments. Westwood estimated jack-up dayrates fell 20.6% in 2025 and drillship dayrates fell 8.2%, while semisubmersible dayrates held firmer in harsh-environment work. That combination kept utilization healthy for premium assets but limited pricing power for older or regionally exposed rigs.

Technology is changing the Offshore Drilling Rig Market more than headline rig counts suggest. Operators now want higher automation, predictive maintenance, digital twins, real-time well control support, and lower-emission offshore operations. COSL Drilling Europe continues to market low-emission rig capability, while Transocean and Seadrill are pushing higher revenue efficiency and tighter fleet scheduling. AI does not replace offshore crews. It improves maintenance planning, drilling parameter control, fuel efficiency, and non-productive time management. These gains matter because a modern drillship can command more than USD 600,000 per day in strong contract windows, and a few points of uptime can materially alter EBITDA.

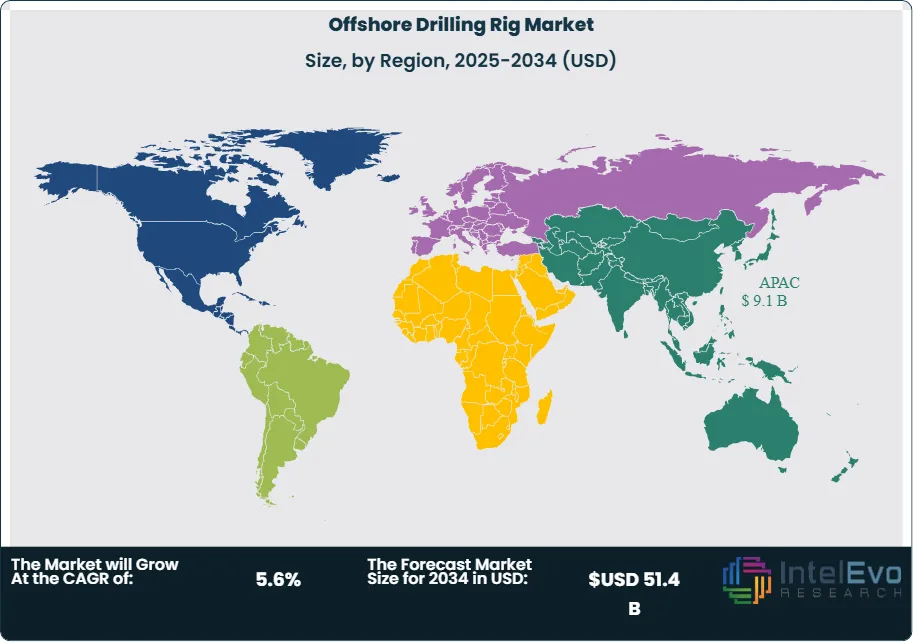

Regionally, Asia Pacific held 29.0% of the Offshore Drilling Rig Market in 2025, equal to USD 9.1 Billion, supported by Southeast Asia jack-up demand, China’s offshore production push, and Australian gas-linked drilling. North America held 25.0%, or USD 7.9 Billion, backed by the U.S. Gulf and Mexico. Middle East & Africa accounted for 18.0%, or USD 5.7 Billion, with Saudi, UAE, West Africa, and Namibia-linked activity. Europe represented 16.0%, or USD 5.0 Billion, driven by Norway and the UK, while Latin America held 12.0%, or USD 3.8 Billion, led by Brazil. Regulatory risk remains high. Decommissioning rules, emissions limits, local-content mandates, and offshore lease policy shifts can alter fleet deployment and contract timing.

, By Water Depth Application (Shallow-Water, Deepwater, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug & Abandonment, Intervention Support), By Contract Structure (Standard Dayrate, Performance-Linked & Integrated Contracts, Managed & Hybrid Models) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Technology Trends & Forecast 2026–2034")

Key Takeaways

| Market Growth | The Offshore Drilling Rig Market stood at USD 31.5 Billion in 2025 and is projected to reach USD 51.4 Billion by 2034, advancing at a 5.6% CAGR during 2026–2034. The growth path reflects disciplined fleet supply, multi-year offshore development programs, and stronger gas-led offshore drilling demand. |

| Segment Dominance | By rig type, jack-up rigs led with 44.0% share in 2025, equivalent to USD 13.9 Billion. Jack-ups remained the volume leader because shallow-water developments across Asia Pacific, the Middle East, and parts of the North Sea sustained broad utilization. |

| Segment Dominance | By water depth application, shallow-water drilling held the largest share at 48.0% in 2025, or USD 15.1 Billion. This segment stayed ahead because national oil companies continued to fund lower-risk, shorter-cycle offshore work with faster payback periods. |

| Driver | The main driver is renewed long-cycle offshore project sanctioning. Around USD 50 Billion of conventional Middle East sanctions during 2025 and USD 1.5 Billion of planned ExxonMobil deepwater spending in Nigeria lifted multi-year rig demand. |

| Restraint | The main restraint is dayrate softness in parts of the fleet. Westwood estimated 2025 jack-up dayrates declined 20.6% and drillship dayrates declined 8.2% from 2024 levels, limiting revenue expansion for contractors without premium assets or long backlog cover. |

| Opportunity | The strongest opportunity sits in frontier and gas-heavy basins across Namibia, Saudi Arabia, Malaysia, and the eastern Mediterranean. These offshore campaigns can add more than USD 8.0 Billion in incremental addressable rig demand between 2025 and 2034. |

| Trend | Consolidation and contract visibility define the leading trend. The proposed USD 5.8 Billion Transocean-Valaris deal and Seadrill’s USD 0.5 Billion in new awards show that scale, fleet quality, and backlog depth now shape competition more than simple fleet size. |

| Regional Analysis | Asia Pacific led the Offshore Drilling Rig Market with 29.0% share and USD 9.1 Billion revenue in 2025. India, Malaysia, China, and Southeast Asia supported this lead through shallow-water drilling, gas campaigns, and national energy security programs. |

Competitive Landscape

The Offshore Drilling Rig Market is moderately consolidated. The top four companies controlled an estimated 36.0% of 2025 market revenue. Competition is driven by fleet quality, contract backlog, water-depth capability, regional presence, and uptime rather than headline rig count alone. Competitive intensity rose sharply in 2025 and early 2026 as contractors pursued consolidation, longer-duration awards, and selective fleet upgrades. The proposed USD 5.8 Billion Transocean-Valaris merger, Noble’s USD 1.3 Billion in new awards entering Norway, and Seadrill’s USD 0.5 Billion backlog additions illustrate a market that now rewards scale and premium asset positioning.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| TRANSOCEAN | Switzerland | Leader | Ultra-Deepwater Drillship Fleet | North America, Brazil, West Africa | Agreed to acquire Valaris for USD 5.8 Billion in Feb 2026. |

| NOBLE CORPORATION | UK | Leader | High-Spec Floaters and CJ70 Jackups | North Sea, U.S. Gulf, Middle East | Announced USD 1.3 Billion in new awards and entry into Norwegian floater market in Jan 2026. |

| VALARIS | Bermuda | Leader | VALARIS DS-8 / DS-16 / DS-18 Drillship Fleet | Brazil, U.S. Gulf, global deepwater | Won Shell Brazil multi-year drillship award worth about USD 300 Million in Dec 2025. |

| SEADRILL | Bermuda | Leader | West Saturn and West Capella Drillships | Brazil, Southeast Asia, Gulf of Mexico | Added USD 0.5 Billion of backlog across seven rigs in Feb 2026. |

| BORR DRILLING | Bermuda | Challenger | Premium Jack-Up Fleet | Middle East, Southeast Asia, West Africa | Completed acquisition of five premium jack-ups from Noble for USD 360 Million in Jan 2026. |

| SHELF DRILLING | UAE | Challenger | J.T. Angel Jack-Up | India, Middle East, West Africa | Secured a three-year ONGC award in India worth about USD 40 Million in Jul 2025. |

| ODFJELL DRILLING | Norway | Challenger | Deepsea Aberdeen / Deepsea Mira | Norway, Namibia, harsh environment | Signed Equinor contract for Deepsea Aberdeen in Dec 2025. |

| COSL DRILLING EUROPE | Norway | Niche Player | Low-Emission Harsh-Environment Semisubs | Norway, North Sea | Continued positioning around low-emission harsh-environment rigs through 2025 and 2026. |

| ARABIAN DRILLING | Saudi Arabia | Niche Player | Offshore Jack-Up Fleet | Saudi Arabia, GCC | Secured first international offshore contract in Jul 2025. |

| VELESTO ENERGY | Malaysia | Niche Player | NAGA 2 Jack-Up | Malaysia, Southeast Asia | Won five-year PETRONAS Carigali contract starting Feb 2026. |

By Rig Type

By rig type, jack-up rigs accounted for 44.0% of the Offshore Drilling Rig Market in 2025, or USD 13.9 Billion. Jack-ups remained the largest segment because they serve the broadest installed base of shallow-water development drilling across Southeast Asia, India, the Middle East, and selected North Sea programs. They also offer lower mobilization and operating cost than deepwater floaters, which keeps them relevant in price-sensitive offshore projects. Shelf Drilling, Borr Drilling, Arabian Drilling, and regional contractors compete aggressively here, but premium modern jack-ups hold the strongest pricing power. The segment still faced pressure in 2025 as dayrates softened, yet long-duration awards in India and Malaysia show that quality assets continue to secure backlog. Drillships held 34.0%, equal to USD 10.7 Billion, and represent the highest-value revenue pool per rig. This segment is driven by Brazil, the U.S. Gulf, West Africa, and frontier deepwater basins, with Transocean, Valaris, Noble, and Seadrill controlling much of the premium fleet. Semisubmersibles accounted for 15.0%, or USD 4.7 Billion, with their strongest role in harsh-environment Norway and specialized deepwater assignments. Tender rigs and others represented 7.0%, or USD 2.2 Billion, and remain relevant in selected Southeast Asian niches but carry lower strategic weight in the current market cycle.

By Water Depth Application

By water depth application, shallow-water drilling led the Offshore Drilling Rig Market with 48.0% share in 2025, or USD 15.1 Billion. This segment includes shelf developments, gas maintenance drilling, and lower-risk oilfield campaigns where operators favor capital discipline and faster project payback. National oil companies in Asia Pacific and the Middle East remain central to this demand. The segment is broad, but it is not low value by default. Modern premium jack-ups and upgraded shallow-water fleets can still generate strong returns when utilization is high and contract terms extend beyond 12 months. Deepwater drilling held 32.0% of the market, or USD 10.1 Billion, and remains the profit center for high-spec drillships and premium semisubmersibles. Brazil, the U.S. Gulf, and West Africa sit at the center of this segment. Ultra-deepwater drilling represented 20.0%, or USD 6.3 Billion, but it posts the strongest structural upside through 2034 because frontier gas, pre-salt, and high-pressure developments require premium rigs with tighter operating envelopes. This segment also sees the strongest effect from automation, digital well control, and predictive maintenance, since downtime cost per day is highest at the ultra-deepwater end of the market.

By End Use

By end use, development drilling dominated the Offshore Drilling Rig Market with 58.0% share in 2025, equivalent to USD 18.3 Billion. This reflects the shift from pure exploration toward reserve development, infill drilling, and production support in proven offshore basins. Operators prefer development campaigns because reservoir risk is lower, economics are clearer, and infrastructure often already exists. Brazil’s pre-salt, the U.S. Gulf, Malaysia, and the Middle East all fit this pattern. Development drilling also favors contractors with strong uptime records and repeat operator relationships, which helps larger fleets maintain backlog. Exploration drilling held 27.0%, or USD 8.5 Billion. Although smaller, it remains strategically important because Namibia, Somalia, the eastern Mediterranean, and selected Atlantic margin basins can create future rig demand waves. Plug and abandonment, intervention support, and other offshore well services represented 15.0%, or USD 4.7 Billion. This smaller segment benefits from regulatory pressure, field maturity, and lower-emission offshore asset use, but it does not yet shape market direction as strongly as development and exploration drilling.

By Contract Structure

By contract structure, standard dayrate contracts accounted for 62.0% of the Offshore Drilling Rig Market in 2025, equal to USD 19.5 Billion. This remained the dominant commercial model because it offers clear visibility on rig pricing, uptime incentives, and reimbursable cost allocation. Dayrate contracts are still the backbone for most deepwater and jack-up awards. Performance-linked and integrated contracts held 21.0%, or USD 6.6 Billion. This segment is gaining ground as operators ask contractors to tie compensation more closely to efficiency, fuel use, emissions, uptime, and project execution. Larger contractors benefit most because they can bundle drilling support, digital tools, maintenance analytics, and broader offshore operations around the rig itself. Managed, bareboat, and hybrid structures represented 17.0%, or USD 5.4 Billion. These structures remain relevant in national oil company relationships, regional partnerships, and fleet transition arrangements. Through 2034, standard dayrates will remain dominant, but performance-linked contracts should gain share as offshore operators focus harder on uptime, emissions, and full-well cost rather than just published daily rates.

Regional Analysis

North America Offshore Drilling Rig Market

North America held 25.0% of the Offshore Drilling Rig Market in 2025, equal to USD 7.9 Billion. The United States led the region, followed by Mexico and Canada. The U.S. Gulf remained the core market driver, with output expected to rise to 1.89 million barrels per day in 2025, supported by improved drilling and new project activity. This gives North America one of the highest concentrations of premium drillship demand in the world. Transocean, Noble, Valaris, and Seadrill all have strong exposure here, and long-duration contracts in the Gulf continue to support backlog quality. Mexico remains relevant through offshore activity and shallow-water demand, although budget pressure and project timing remain less predictable than in the U.S. Canada contributes only marginal direct offshore rig demand compared with the Atlantic and Gulf markets farther south. The region combines high rig capability with mature offshore infrastructure, strong contract transparency, and deep service ecosystems. Policy risk remains present, but capital now concentrates in advantaged basins rather than across every lease frontier. North America stays deepwater-heavy, contractor-rich, and highly competitive.

Europe Offshore Drilling Rig Market

Europe accounted for 16.0% of the Offshore Drilling Rig Market in 2025, or USD 5.0 Billion. Norway led the region, followed by the UK, Germany, and the Netherlands. Norway is the key profit pool because it supports harsh-environment semisubmersibles, premium jack-ups, and long-duration development drilling backed by Equinor, Aker BP, and Vår Energi. Odfjell Drilling signed the Deepsea Aberdeen contract with Equinor in December 2025, while Noble won a three-year award for Noble GreatWhite in Norway valued at about USD 473 Million. These deals show that the Norwegian Continental Shelf remains one of the highest-barrier, highest-spec offshore rig markets in the world. The UK also sustains meaningful offshore demand, though at smaller scale and with stronger late-life asset exposure. Europe’s offshore rig demand is shaped by regulation more than any other major region. Emissions intensity, safety performance, local competence, and environmental oversight directly influence contract awards. This benefits contractors such as Odfjell and COSL that emphasize harsh-environment and lower-emission rig capability.

Asia Pacific Offshore Drilling Rig Market

Asia Pacific held 29.0% of the Offshore Drilling Rig Market in 2025, equal to USD 9.1 Billion. China, India, Malaysia, and Australia were the most relevant countries. The region led the global market because it combines large shallow-water drilling activity with sustained offshore gas demand. India remained active through ONGC offshore work, including Shelf Drilling’s three-year jack-up award in Mumbai High. Malaysia strengthened regional visibility in 2026 after Velesto secured a five-year contract for the NAGA 2 jack-up with PETRONAS Carigali. China also remains central because offshore projects represented a large share of reserves brought onstream and CNOOC targeted higher 2025 production. Australia supports the regional mix through offshore gas and LNG-linked drilling, while Southeast Asia continues to rely on jack-up and shallow-water fleets for supply security. Asia Pacific is the most balanced offshore rig market by fleet mix and should keep its lead through much of the forecast period.

Latin America Offshore Drilling Rig Market

Latin America represented 12.0% of the Offshore Drilling Rig Market in 2025, or USD 3.8 Billion. Brazil dominated the region, followed by Mexico, Guyana, and Argentina. Brazil is the clear anchor because its pre-salt and post-salt programs create multi-year deepwater rig demand with strong revenue per contracted unit. Valaris secured a Shell Brazil drillship award worth about USD 300 Million in December 2025, while Seadrill’s Petrobras-linked awards from late 2024 added about USD 1.0 Billion of backlog. These contract values show how concentrated and valuable Brazilian offshore demand has become. Mexico adds offshore activity, but funding consistency remains a bigger concern. Guyana remains smaller in current rig revenue, yet it influences regional fleet tightness because operators increasingly look at adjacent Atlantic margin opportunities. Latin America is structurally attractive because offshore break-even economics in Brazil remain competitive and project timelines are long enough to support long contract terms. Through 2034, the region should post one of the strongest growth profiles in the Offshore Drilling Rig Market.

Middle East & Africa Offshore Drilling Rig Market

Middle East & Africa held 18.0% of the Offshore Drilling Rig Market in 2025, equal to USD 5.7 Billion. Saudi Arabia, the UAE, South Africa, and Namibia were the most relevant strategic countries, with West Africa also contributing meaningful demand through Nigeria and Angola. The Middle East side of the market is still more jack-up and shallow-water weighted than Latin America, but it is expanding through large gas and offshore development campaigns. Saudi Arabia’s Jafurah development is expected to produce 2 billion standard cubic feet per day by 2030 and has already seen more than USD 26 Billion in awarded contracts. In Africa, Namibia remains the standout frontier story, with renewed drilling plans and first-oil ambitions by 2030. Nigeria also remains relevant as ExxonMobil planned USD 1.5 Billion of deepwater spending. This region mixes stable national oil company work with frontier offshore upside and should be one of the fastest-growing regional markets through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Rig Type

- Jack-Up Rigs

- Drillships

- Semisubmersibles

- Tender Rigs

- Others

By Water Depth Application

- Shallow-Water Drilling

- Deepwater Drilling

- Ultra-Deepwater Drilling

By End Use

- Development Drilling

- Exploration Drilling

- Plug and Abandonment, Intervention Support

- Others

By Contract Structure

- Standard Dayrate Contracts

- Performance-Linked and Integrated Contracts

- Managed, Bareboat, and Hybrid Structures

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 31.5 B |

| Forecast Revenue (2034) | USD 51.4 B |

| CAGR (2025-2034) | 5.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Rig Type (Jack-Up Rigs, Drillships, Semisubmersibles, Tender Rigs and Others), By Water Depth Application (Shallow-Water Drilling, Deepwater Drilling, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug and Abandonment, Intervention Support, and Others), By Contract Structure (Standard Dayrate Contracts, Performance-Linked and Integrated Contracts, Managed, Bareboat, and Hybrid Structures) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TRANSOCEAN, NOBLE CORPORATION, VALARIS, SEADRILL, BORR DRILLING, SHELF DRILLING, ODFJELL DRILLING, COSL DRILLING EUROPE, ARABIAN DRILLING, VELESTO ENERGY, NORTHERN OCEAN, STENA DRILLING, VANTAGE DRILLING, SAIPEM, JAPAN DRILLING COMPANY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Water Depth Application (Shallow-Water, Deepwater, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug & Abandonment, Intervention Support), By Contract Structure (Standard Dayrate, Performance-Linked & Integrated Contracts, Managed & Hybrid Models) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Technology Trends & Forecast 2026–2034")

, By Water Depth Application (Shallow-Water, Deepwater, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug & Abandonment, Intervention Support), By Contract Structure (Standard Dayrate, Performance-Linked & Integrated Contracts, Managed & Hybrid Models) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Technology Trends & Forecast 2026–2034")

, By Water Depth Application (Shallow-Water, Deepwater, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug & Abandonment, Intervention Support), By Contract Structure (Standard Dayrate, Performance-Linked & Integrated Contracts, Managed & Hybrid Models) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Offshore Drilling Rig Market?

The Global Offshore Drilling Rig Market was valued at USD 31.5 Billion in 2025, projected to reach USD 51.4 Billion by 2034 at a CAGR of 5.6% from 2026–2034. Growth is driven by rising offshore exploration, deepwater and ultra-deepwater drilling activities, increasing energy demand, and advancements in offshore drilling technologies.

Who are the major players in the Offshore Drilling Rig Market?

TRANSOCEAN, NOBLE CORPORATION, VALARIS, SEADRILL, BORR DRILLING, SHELF DRILLING, ODFJELL DRILLING, COSL DRILLING EUROPE, ARABIAN DRILLING, VELESTO ENERGY, NORTHERN OCEAN, STENA DRILLING, VANTAGE DRILLING, SAIPEM, JAPAN DRILLING COMPANY, Others

Which segments covered the Offshore Drilling Rig Market?

By Rig Type (Jack-Up Rigs, Drillships, Semisubmersibles, Tender Rigs and Others), By Water Depth Application (Shallow-Water Drilling, Deepwater Drilling, Ultra-Deepwater Drilling), By End Use (Development Drilling, Exploration Drilling, Plug and Abandonment, Intervention Support, and Others), By Contract Structure (Standard Dayrate Contracts, Performance-Linked and Integrated Contracts, Managed, Bareboat, and Hybrid Structures)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Offshore Drilling Rig Market

Published Date : 17 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date