- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Asset Integrity Management Market Forecast 2034 | CAGR 5.3%

Global Oil and Gas Asset Integrity Management Market Size, Share, Growth & Industry Analysis By Service Type (Inspection, Testing, Certification, Maintenance, Consulting Services), By Operation (Upstream, Midstream, Downstream), By Technology (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User (Oil & Gas Operators, EPC Contractors, Others) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

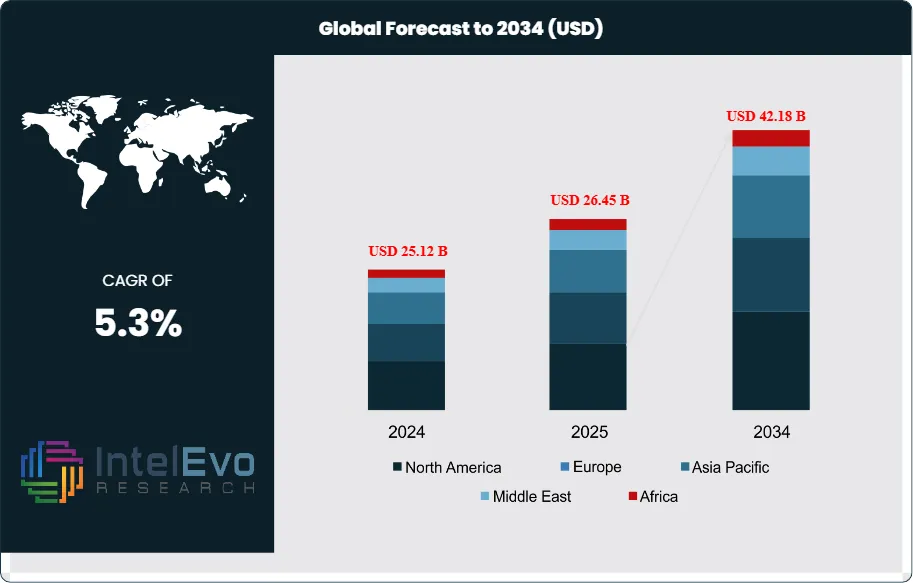

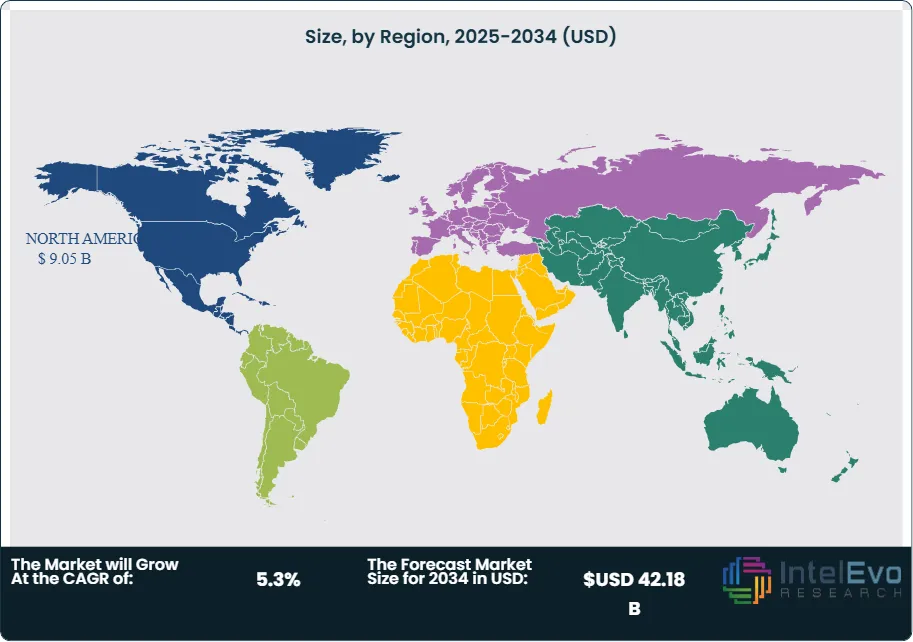

| USD 26.45 Billion | USD 42.18 Billion | 5.3% | North America, 34.2% |

The Oil and Gas Asset Integrity Management Market was valued at approximately USD 25.12 Billion in 2024 and reached USD 26.45 Billion in 2025. The market is projected to grow to USD 42.18 Billion by 2034, expanding at a CAGR of 5.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.73 billion over the analysis period. The oil and gas asset integrity management market encompasses inspection, testing, certification, and maintenance services that ensure safe, reliable, and compliant operations across upstream, midstream, and downstream infrastructure.

Get More Information about this report -

Request Free Sample ReportAging infrastructure across mature oil and gas basins drives sustained demand for asset integrity management services. The American Petroleum Institute estimates that 45% of U.S. refinery capacity operates equipment installed before 1980, requiring continuous integrity assessment to prevent failures. Pipeline operators in North America manage over 2.6 million miles of transmission and gathering lines, many exceeding 50 years of service life. PHMSA regulations mandate regular inline inspections and integrity verification programs that generate recurring revenue for specialized service providers. Offshore platforms in the North Sea, Gulf of Mexico, and West Africa face corrosion, fatigue, and structural degradation that demand systematic integrity monitoring programs.

The oil and gas asset integrity management market benefits from strict regulatory enforcement that penalizes integrity failures. EPA enforcement actions following refinery incidents have resulted in penalties exceeding USD 500 million over the past five years. BSEE regulations for offshore facilities require comprehensive safety and environmental management systems with third-party verification. The EU Offshore Safety Directive mandates independent verification of safety-critical elements for all North Sea installations. These regulatory drivers create non-discretionary demand for integrity services regardless of commodity price cycles.

Digital transformation is reshaping the asset integrity management sector. Operators increasingly deploy IoT sensors, drones, and AI-powered analytics to transition from calendar-based to condition-based maintenance strategies. Risk-based inspection programs that prioritize resources on highest-consequence equipment reduce total cost of ownership while maintaining safety performance. The integration of digital twins with integrity data enables predictive maintenance that extends asset life and prevents unplanned shutdowns. North America leads the market with 34.2% share, generating USD 9.05 billion in 2025. Europe follows at 27.8% share, while the Middle East and Africa accounts for 19.4% driven by national oil company infrastructure investments in Saudi Arabia and the UAE.

, By Operation (Upstream, Midstream, Downstream), By Technology (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User (Oil & Gas Operators, EPC Contractors, Others) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas asset integrity management market is projected to expand from USD 26.45 billion in 2025 to USD 42.18 billion by 2034, achieving a CAGR of 5.3% during the 2025-2034 forecast period.

- Segment Dominance (By Service Type): Inspection services command the largest segment share at 38.6% in 2025, generating USD 10.21 billion, driven by regulatory mandates for periodic equipment assessment across refineries, pipelines, and offshore platforms.

- Segment Dominance (By Operation): Upstream operations account for 44.2% of market revenue in 2025, valued at USD 11.69 billion, as aging production infrastructure and offshore platform maintenance requirements drive inspection demand.

- Driver: Regulatory compliance mandates have intensified asset integrity spending, with PHMSA pipeline integrity management requirements generating 12% annual growth in inline inspection services since 2022.

- Restraint: Skilled workforce shortages constrain market expansion, with 28% of inspection companies reporting difficulty filling certified NDT technician positions in 2025.

- Opportunity: Digitalization of integrity management presents a USD 4.8 billion incremental opportunity by 2034, as operators transition to AI-powered predictive maintenance and remote monitoring solutions.

- Trend: Drone-based inspection adoption has accelerated to 34% of offshore platform surveys in 2025, up from 8% in 2020, reducing inspection costs by 40% while improving data quality.

- Regional Analysis: North America maintains market leadership with 34.2% share and USD 9.05 billion revenue in 2025, driven by extensive pipeline networks, mature refinery infrastructure, and Gulf of Mexico offshore operations.

Competitive Landscape Overview

The oil and gas asset integrity management market exhibits moderate consolidation, with the top four service providers capturing approximately 42% of global revenue in 2025. Competition centers on technical capabilities, geographic coverage, and digital platform differentiation. SLB and Baker Hughes lead through integrated service offerings that combine inspection, data analytics, and operational consulting. TIC companies including DNV, Bureau Veritas, and SGS compete on certification authority and global inspection networks. Recent M&A activity has intensified as oilfield service majors acquire specialized integrity and NDT capabilities. The April 2025 SLB-ChampionX merger at USD 7.8 billion created the largest pure-play production and integrity services provider globally.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | ARMS Asset Risk Management | Global | Acquired ChampionX for USD 7.8B (Apr 2025) |

| Baker Hughes | US | Leader | Cordant AIM Platform | North America | Launched AI integrity analytics (Jan 2026) |

| Halliburton | US | Leader | Landmark DecisionSpace | North America | Expanded digital twin offerings (Mar 2025) |

| TechnipFMC | UK | Leader | iProduction Suite | Europe | Partnered with Aker BP for subsea AIM (Feb 2025) |

| DNV | Norway | Challenger | Veracity AIM Platform | Europe | Acquired Nixu Cybersecurity (Dec 2024) |

| Bureau Veritas | France | Challenger | VERISTAR AIM | Europe | Expanded Middle East inspection hubs (Jun 2025) |

| SGS | Switzerland | Challenger | SGS Oil & Gas Integrity | Europe | Launched drone inspection services (Sep 2025) |

| Intertek | UK | Challenger | AIM Total Quality Assurance | Europe | Opened Houston integrity center (Aug 2025) |

| Oceaneering | US | Niche Player | Subsea Integrity Solutions | North America | Deployed autonomous inspection ROVs (May 2025) |

| MISTRAS Group | US | Niche Player | OneSuite AIM Platform | North America | Acquired NDT Global assets (Nov 2024) |

By Service Type

The oil and gas asset integrity management market segments by service type into inspection, testing, certification, maintenance, and consulting services. Inspection services dominate with 38.6% market share in 2025, generating USD 10.21 billion in revenue. This segment encompasses visual inspection, non-destructive testing, inline inspection of pipelines, and structural assessment of offshore platforms. Regulatory mandates from API, ASME, and PHMSA require periodic equipment inspection at defined intervals, creating recurring demand. Advanced inspection technologies including phased array ultrasonics, guided wave testing, and digital radiography enable detection of defects before failure occurs. Baker Hughes, SLB, and specialized NDT contractors including MISTRAS and Applus+ lead this segment.

Testing services hold 24.3% share, valued at USD 6.43 billion in 2025. This segment includes pressure testing, hydrostatic testing, material testing, and performance verification. Downstream refineries require extensive testing during turnaround maintenance cycles, with major turnarounds generating USD 5-15 million in testing services per facility. Certification services account for 15.8% share at USD 4.18 billion, dominated by TIC companies that provide independent verification of equipment compliance with API, ASME, and ISO standards. DNV and Bureau Veritas maintain strong positions in offshore certification where regulatory frameworks require third-party verification. Maintenance services capture 14.2% share, generating USD 3.76 billion through corrosion management, cathodic protection, and coating application. Consulting services comprise 7.1% at USD 1.88 billion, providing risk-based inspection program development and integrity management system design.

By Operation

Upstream operations represent the largest operational segment with 44.2% share in 2025, valued at USD 11.69 billion. Exploration and production infrastructure including wellheads, separators, production platforms, and gathering systems require continuous integrity monitoring. Offshore platforms present complex integrity challenges involving structural fatigue, marine corrosion, and subsea equipment degradation. The average offshore platform inspection program costs USD 2-5 million annually depending on installation size and water depth. Onshore production facilities face integrity issues related to pressure containment, corrosion under insulation, and mechanical fatigue of rotating equipment.

Midstream operations hold 28.4% share at USD 7.51 billion in 2025. Pipeline integrity management programs mandated by PHMSA and equivalent international regulators require inline inspection, direct assessment, and pressure testing. The U.S. pipeline network alone generates over USD 2.5 billion in annual integrity spending. Storage terminals, compressor stations, and LNG facilities add substantial midstream integrity requirements. Downstream operations capture 27.4% share, generating USD 7.25 billion. Refineries, petrochemical plants, and distribution terminals require extensive inspection during scheduled turnarounds. The average refinery turnaround includes USD 8-20 million in inspection and testing services. Downstream integrity spending correlates with refinery utilization rates and turnaround frequency.

By Technology

Non-destructive testing technologies lead the asset integrity management market with 46.2% share in 2025, generating USD 12.22 billion. Ultrasonic testing accounts for 35% of NDT revenue, followed by radiographic testing at 22%, magnetic particle testing at 18%, and penetrant testing at 12%. Advanced NDT methods including phased array, time-of-flight diffraction, and computed radiography command premium pricing and are growing at 8% annually. Corrosion management technologies hold 24.6% share at USD 6.51 billion, encompassing cathodic protection, coating systems, and corrosion inhibitor applications. Structural monitoring technologies capture 16.8% share, valued at USD 4.44 billion, including strain gauging, vibration analysis, and acoustic emission monitoring. Remote inspection technologies account for 12.4% share at USD 3.28 billion, driven by rapid adoption of drones, ROVs, and robotic crawlers that reduce human entry requirements in confined spaces and hazardous environments.

By End-User

Oil and gas operators generate 72.4% of asset integrity management demand in 2025, valued at USD 19.15 billion. National oil companies including Saudi Aramco, ADNOC, and Petrobras maintain large in-house integrity capabilities supplemented by third-party specialized services. International oil companies including ExxonMobil, Shell, and Chevron outsource significant integrity workloads to specialized contractors. Independent producers typically outsource 80% or more of integrity services. Engineering, procurement, and construction contractors account for 15.8% of market demand at USD 4.18 billion, procuring integrity services for new facility construction and commissioning. The remaining 11.8% share, valued at USD 3.12 billion, comes from equipment manufacturers, insurance companies, and regulatory bodies requiring independent verification.

Regional Analysis

North America

North America commands 34.2% of the oil and gas asset integrity management market in 2025, generating USD 9.05 billion in revenue. The United States accounts for 84% of regional revenue, driven by extensive infrastructure requiring continuous integrity monitoring. Over 190 refineries, 2.6 million miles of pipelines, and thousands of offshore platforms in the Gulf of Mexico create sustained demand for inspection and maintenance services. PHMSA pipeline integrity management regulations mandate inline inspection every seven years for hazardous liquid lines, generating predictable recurring revenue. The Gulf of Mexico offshore sector faces heightened regulatory scrutiny following historical incidents, with BSEE requiring comprehensive safety and environmental management systems. Canada contributes 12% of North American revenue through oil sands infrastructure, offshore Atlantic projects, and extensive pipeline networks connecting production to markets. Mexico accounts for 4% as Pemex modernization programs increase third-party integrity service procurement following energy reform.

Europe

Europe holds 27.8% market share in 2025, valued at USD 7.35 billion. The United Kingdom leads with 32% of regional revenue as North Sea operators manage aging platforms averaging 30+ years in service. The UK Oil and Gas Authority requires safety case submissions with independent verification of safety-critical elements. Norway contributes 28% of European revenue with the Norwegian Petroleum Safety Authority enforcing rigorous integrity standards for North Sea and Barents Sea operations. Equinor, Aker BP, and international operators maintain extensive integrity programs for mature and new field developments. Germany accounts for 14% driven by refinery and petrochemical infrastructure in the Rhine-Ruhr region. The Netherlands and France together contribute 16% as integrated refineries and gas storage facilities require continuous monitoring. The EU Offshore Safety Directive harmonizes integrity requirements across member states, requiring independent verification and creating opportunities for TIC companies.

Middle East and Africa

The Middle East and Africa region represents 19.4% of the global market in 2025, generating USD 5.13 billion in revenue. Saudi Arabia dominates with 38% of regional revenue as Saudi Aramco operates the world's largest oil production and refining infrastructure. Aramco's USD 100+ billion capital program through 2030 includes substantial integrity management components for existing and new facilities. The UAE contributes 26% with ADNOC's extensive onshore and offshore infrastructure requiring comprehensive integrity programs. Qatar accounts for 12% driven by the world's largest LNG production facilities at Ras Laffan. African markets including Nigeria, Angola, and Egypt comprise 15% of regional revenue, with offshore deepwater developments in West Africa generating substantial subsea integrity requirements. The remaining GCC markets including Kuwait, Oman, and Bahrain contribute 9% with growing integrity spending as production infrastructure matures.

Asia Pacific

Asia Pacific captures 12.6% of the global oil and gas asset integrity management market in 2025, valued at USD 3.33 billion, while achieving the fastest regional growth at 6.8% CAGR through 2034. China leads with 42% of regional revenue as CNPC, Sinopec, and CNOOC expand integrity programs across aging refineries and growing offshore production. India contributes 24% with Indian Oil Corporation, Reliance Industries, and ONGC investing in refinery modernization and offshore integrity management. Australia accounts for 18% as LNG operators including Woodside, Santos, and Chevron maintain extensive integrity programs for offshore production and onshore processing facilities. Southeast Asian markets including Indonesia, Malaysia, and Thailand comprise 12% of regional revenue with mature offshore fields requiring life extension assessments and aging refinery infrastructure needing enhanced monitoring.

Latin America

Latin America accounts for 6.0% of the global market in 2025, valued at USD 1.59 billion. Brazil dominates with 58% of regional revenue as Petrobras and international partners operating pre-salt fields deploy extensive subsea and FPSO integrity programs. Pre-salt FPSOs represent some of the most complex floating production systems globally, requiring specialized integrity monitoring for risers, mooring systems, and process equipment. Argentina contributes 20% with Vaca Muerta shale development driving integrity requirements for gathering systems and processing facilities. Mexico accounts for 14% as Pemex infrastructure rehabilitation programs address deferred maintenance across aging refineries and offshore platforms. Colombia and other Andean markets comprise 8% with growing integrity spending among national oil companies and international operators in mature producing basins.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Inspection Services

- Testing Services

- Certification Services

- Maintenance Services

- Consulting Services

By Operation

- Upstream

- Midstream

- Downstream

By Technology

- Non-Destructive Testing

- Corrosion Management

- Structural Monitoring

- Remote Inspection Technologies

By End-User

- Oil and Gas Operators

- EPC Contractors

- Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 26.45 B |

| Forecast Revenue (2034) | USD 42.18 B |

| CAGR (2025-2034) | 5.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Inspection Services, Testing Services, Certification Services, Maintenance Services, Consulting Services), By Operation, (Upstream, Midstream, Downstream), By Technology, (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User, (Oil and Gas Operators, EPC Contractors, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, BAKER HUGHES, HALLIBURTON, TECHNIPFMC, DNV, BUREAU VERITAS, SGS, INTERTEK, OCEANEERING, MISTRAS GROUP, APPLUS+, DEKRA, RINA, LLOYD'S REGISTER, TEAM INDUSTRIAL SERVICES, AKER SOLUTIONS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Operation (Upstream, Midstream, Downstream), By Technology (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User (Oil & Gas Operators, EPC Contractors, Others) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Technology (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User (Oil & Gas Operators, EPC Contractors, Others) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Technology (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User (Oil & Gas Operators, EPC Contractors, Others) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the ?

Global Oil & gas asset integrity management market valued at USD 25.12B in 2024, reaching USD 42.18B by 2034, growing at a CAGR of 5.3% from 2026–2034.

Who are the major players in the ?

SLB, BAKER HUGHES, HALLIBURTON, TECHNIPFMC, DNV, BUREAU VERITAS, SGS, INTERTEK, OCEANEERING, MISTRAS GROUP, APPLUS+, DEKRA, RINA, LLOYD'S REGISTER, TEAM INDUSTRIAL SERVICES, AKER SOLUTIONS, Others

Which segments covered the ?

By Service Type, (Inspection Services, Testing Services, Certification Services, Maintenance Services, Consulting Services), By Operation, (Upstream, Midstream, Downstream), By Technology, (Non-Destructive Testing, Corrosion Management, Structural Monitoring, Remote Inspection Technologies), By End-User, (Oil and Gas Operators, EPC Contractors, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Asset Integrity Management Market

Published Date : 03 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date