- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Cloud Computing Market Size & Forecast 2034 | CAGR 13.6%

Global Oil and Gas Cloud Computing Market Size, Share, Growth & Industry Analysis By Service Model (SaaS, IaaS, PaaS), By Operation (Upstream, Midstream, Downstream), By Deployment (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights, Key Players & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 7.2 Billion | USD 22.8 Billion | 13.6% | North America, 40.3% |

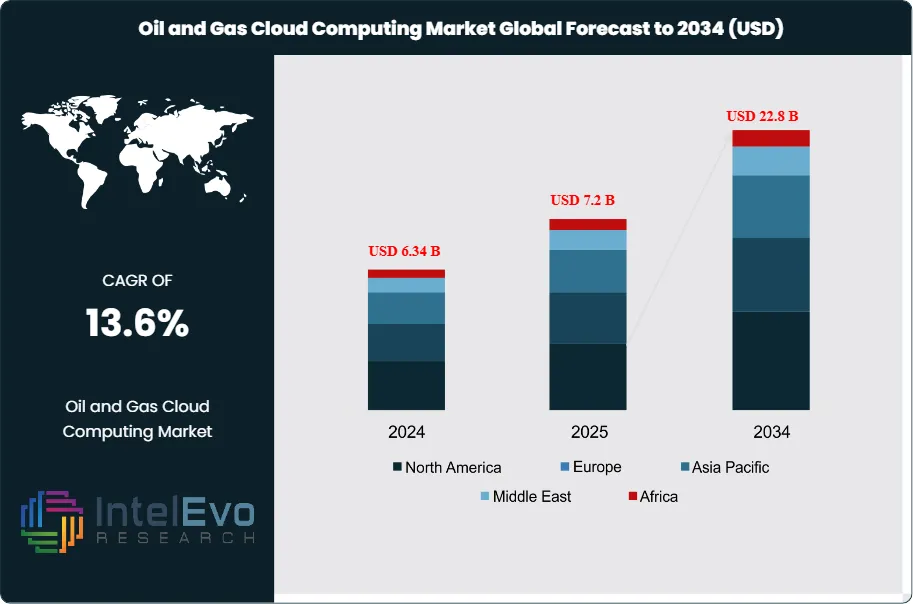

The Oil and Gas Cloud Computing Market was valued at approximately USD 6.34 Billion in 2024 and reached USD 7.2 Billion in 2025. The market is projected to grow to USD 22.8 Billion by 2034, expanding at a CAGR of 13.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.6 Billion over the analysis period. Cloud computing in the oil and gas sector encompasses infrastructure-as-a-service (IaaS), platform-as-a-service (PaaS), and software-as-a-service (SaaS) solutions tailored for upstream exploration and production, midstream pipeline and logistics operations, and downstream refining and distribution workflows. The migration from on-premise data centers to cloud environments enables operators to process seismic datasets exceeding 50 petabytes, run reservoir simulations at 10 times the speed of legacy systems, and reduce IT infrastructure CAPEX by 30–45%.

Get More Information about this report -

Request Free Sample ReportThe oil and gas cloud computing market draws structural momentum from three converging forces. First, the volume of operational data generated across the hydrocarbon value chain doubled between 2021 and 2025, reaching an estimated 2.5 exabytes per year across the global industry. Legacy on-premise storage and compute infrastructure cannot handle this data volume cost-effectively. Second, EPA emissions reporting mandates under NSPS OOOOb/c and the EU Methane Regulation require near-real-time data aggregation from thousands of sensors per facility; cloud platforms provide the elastic compute needed for continuous environmental compliance monitoring. Third, OPEC+ production management complexity increased after 2023, with national oil companies requiring cloud-based production forecasting and allocation models to manage quota compliance across hundreds of fields.

North America accounted for 40.3% of oil and gas cloud computing market revenue in 2025, driven by hyperscaler investment in energy-specific cloud services and aggressive adoption across the Permian Basin, Gulf of Mexico, and Montney play operators. Europe held 24.1%, led by North Sea digital transformation programs at Equinor, Shell, and BP. Asia Pacific captured 19.6%, where CNOOC, Petronas, and ONGC committed to cloud-first IT strategies for offshore and onshore production management. The Middle East represented the fastest-growing region, with Saudi Aramco, ADNOC, and Qatar Energy each allocating over USD 300 Million to cloud migration programs between 2024 and 2026. The oil and gas cloud computing market is shifting from experimental pilots to enterprise-scale deployment, with average cloud spend per operator increasing 38% year over year in 2025.

, By Operation (Upstream, Midstream, Downstream), By Deployment (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights, Key Players & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas cloud computing market was valued at USD 7.2 Billion in 2025 and is projected to reach USD 22.8 Billion by 2034, expanding at a CAGR of 13.6% over the 2025–2034 forecast period.

- Segment Dominance (By Service Model): The SaaS segment led the market with a 46.5% share in 2025, generating USD 3.35 Billion as operators prioritized subscription-based applications for production surveillance, asset management, and regulatory reporting.

- Segment Dominance (By Operation): Upstream operations captured the largest share at 44.8% in 2025, valued at USD 3.23 Billion, driven by cloud-based seismic processing, reservoir simulation, and drilling analytics.

- Driver: The explosion of oilfield data to 2.5 exabytes per year in 2025 exceeded on-premise compute capacity, pushing 62% of large E&P operators to adopt cloud for core geoscience and production workflows.

- Restraint: Cybersecurity concerns and data sovereignty regulations restrict cloud adoption among national oil companies; 38% of NOCs cited data residency as the primary barrier to full cloud migration in 2025.

- Opportunity: Cloud-native edge computing for remote and offshore assets represents a USD 4.1 Billion addressable opportunity by 2034, targeting the 65% of offshore platforms that lacked reliable cloud connectivity in 2025.

- Trend: Generative AI and large language model deployment on cloud platforms for automated well log interpretation and production report generation reached 29% adoption among large-cap operators in 2025.

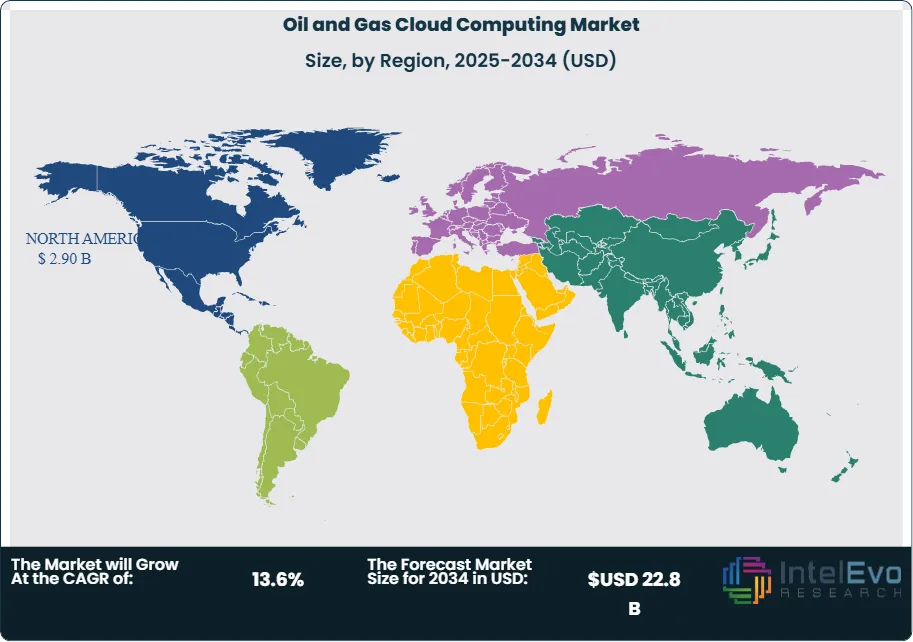

- Regional Analysis: North America dominated with a 40.3% share and USD 2.90 Billion in revenue in 2025, anchored by hyperscaler partnerships with Permian Basin and Gulf of Mexico operators.

Competitive Landscape Overview

The oil and gas cloud computing market is moderately consolidated, with the top four players; Microsoft Azure, AWS, Google Cloud, and SAP; commanding a combined 52.7% market share in 2025. Competition is platform-driven, centered on energy-specific data services, AI/ML integration depth, and certified compliance with industry standards including API, BSEE, and EPA frameworks. Eight acquisitions exceeding USD 100 Million each occurred between 2024 and 2025 as hyperscalers and enterprise software firms absorbed oilfield data analytics startups. Oilfield service companies including SLB and Halliburton have intensified competition by building proprietary cloud platforms that combine domain expertise with hyperscaler infrastructure.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Microsoft Azure | US | Leader | Azure Energy Data Services | North America | Launched AI-driven reservoir simulation on Azure HPC (Jan 2026) |

| Amazon Web Services | US | Leader | AWS for Energy (O&G Data Lake) | North America | Partnered with SLB for cloud-native E&P data platform (Mar 2025) |

| Google Cloud | US | Leader | Google Cloud Seismic AI Suite | North America | Released subsurface interpretation engine with TotalEnergies (Jun 2025) |

| SAP SE | Germany | Leader | SAP S/4HANA for Oil & Gas | Europe | Migrated ADNOC enterprise operations to SAP cloud (Sep 2025) |

| IBM | US | Challenger | IBM Maximo for Asset Management | North America | Integrated Watson AI into predictive maintenance cloud for refineries (Apr 2025) |

| Oracle | US | Challenger | Oracle Energy & Water Cloud | North America | Launched autonomous database for pipeline SCADA analytics (Dec 2024) |

| Accenture | Ireland | Challenger | Accenture Cloud for Energy | Europe | Acquired Flutura Decision Sciences for industrial AI cloud (Feb 2025) |

| Halliburton | US | Challenger | Halliburton iEnergy Cloud | Middle East | Deployed cloud-based drilling optimization across 6 NOC clients (Aug 2025) |

| SLB (Schlumberger) | US | Challenger | SLB Delfi Cloud Platform | Middle East | Expanded Delfi to 15 new E&P operators on AWS (Mar 2025) |

| Informatica | US | Niche Player | Informatica IDMC for Energy | North America | Released master data management cloud for midstream operators (Nov 2025) |

By Service Model:

The SaaS segment captured 46.5% of the oil and gas cloud computing market in 2025, generating USD 3.35 Billion. SaaS applications in the oil and gas sector include production surveillance dashboards, equipment health monitoring platforms, regulatory emissions reporting tools, and supply chain management systems. SAP S/4HANA Cloud, Oracle Energy Cloud, and IBM Maximo dominate the enterprise SaaS tier for downstream and midstream operations. SLB Delfi and Halliburton iEnergy serve upstream-specific SaaS workloads. Subscription-based pricing reduced upfront IT expenditure by 40–55% for operators transitioning from perpetual license models. Average annual SaaS spend per large operator reached USD 12 Million in 2025, up from USD 7.4 Million in 2022.

The IaaS segment held 31.2% share, valued at USD 2.25 Billion in 2025. Infrastructure services provide the elastic compute, GPU clusters, and high-performance storage required for seismic data processing, reservoir simulation, and computational fluid dynamics. AWS, Microsoft Azure, and Google Cloud compete directly in this tier, each offering energy-optimized virtual machine configurations and data lake architectures. Seismic processing workloads that previously required 6–8 weeks on proprietary supercomputers now complete in 3–5 days on cloud HPC clusters. The PaaS segment captured 22.3%, valued at USD 1.61 Billion. PaaS solutions provide development environments, data integration middleware, and API management tools that enable operators and service companies to build custom applications on cloud infrastructure. OSDU (Open Subsurface Data Universe) compatibility has become a baseline requirement for PaaS offerings targeting upstream operators.

By Operation:

Upstream operations dominated with 44.8% of oil and gas cloud computing market revenue in 2025, valued at USD 3.23 Billion. Cloud platforms serve upstream workflows including seismic interpretation, well planning, reservoir characterization, drilling optimization, and production forecasting. The shift to cloud-based geoscience reduced data access latency from days to minutes for distributed asset teams. Permian Basin operators processed 2.3 petabytes of seismic data on cloud platforms in 2025 alone. Cloud-based reservoir simulation models now run 1,000+ scenario iterations in hours rather than weeks, enabling faster field development plan decisions.

Midstream operations held 24.6% share, generating USD 1.77 Billion in 2025. Pipeline operators use cloud platforms for SCADA data aggregation, flow assurance modeling, leak detection analytics, and gas processing plant optimization. PHMSA pipeline integrity reporting requirements in the United States favor cloud-hosted data management systems that consolidate inspection, corrosion, and pressure records across thousands of pipeline miles. Downstream operations captured 30.6%, valued at USD 2.20 Billion. Refineries and petrochemical complexes deploy cloud solutions for advanced process control, turnaround planning, crude assay management, and product blending optimization. The downstream segment benefits from SAP and Oracle’s established ERP cloud presence, which provides a migration pathway from legacy on-premise refinery management systems.

By Deployment:

Public cloud deployment captured 48.3% of the oil and gas cloud computing market in 2025. Public cloud adoption accelerated as AWS, Azure, and Google Cloud achieved SOC 2, ISO 27001, and FedRAMP certifications relevant to energy sector compliance requirements. Public cloud offers the lowest-cost compute for burst workloads such as seismic reprocessing and Monte Carlo reservoir simulations. Hybrid cloud held 34.5%, favored by operators that maintain on-premise SCADA and real-time control systems while offloading analytics and archival workloads to public cloud environments. Hybrid architectures address latency requirements for safety-critical offshore operations where satellite connectivity introduces 400–800 millisecond delays. Private cloud captured 17.2%, concentrated among national oil companies with sovereign data requirements. Saudi Aramco, ADNOC, and Petrobras operate private cloud infrastructure within national data centers, processing classified subsurface and reserves data.

By Enterprise Size:

Large enterprises accounted for 72.8% of the oil and gas cloud computing market in 2025, spending USD 5.24 Billion. Supermajors and NOCs drive the majority of cloud procurement, with ExxonMobil, Shell, Chevron, BP, and TotalEnergies each reporting cloud IT budgets exceeding USD 200 Million annually. Large operators benefit from dedicated hyperscaler account teams, custom SLA agreements, and co-development partnerships for energy-specific AI services. Small and medium enterprises held 27.2% share, valued at USD 1.96 Billion. Independent E&P operators and regional service companies adopted cloud primarily through SaaS subscriptions and managed cloud services, avoiding the complexity of self-managed IaaS deployments. Average cloud spend among mid-cap independents reached USD 3.8 Million per year in 2025.

Regional Analysis

North America Oil and Gas Cloud Computing Market:

North America commanded a 40.3% share of the global oil and gas cloud computing market in 2025, generating USD 2.90 Billion in revenue. The United States contributed 86% of regional spending, driven by hyperscaler proximity to major basins and a mature enterprise cloud adoption culture. Permian Basin operators migrated 58% of geoscience workloads to cloud platforms by 2025. Gulf of Mexico deepwater operators adopted cloud-based digital twins for FPSO production management, connecting topside sensor data to onshore analytics centers via satellite-to-cloud pathways. ExxonMobil’s partnership with Microsoft Azure for upstream data management set the benchmark for supermajor-scale cloud deployments. Canada’s oil sands operators, including Suncor and CNRL, use cloud for SAGD process optimization and greenhouse gas reporting. Mexico’s Pemex initiated cloud migration for its downstream operations at the Dos Bocas and Tula refineries in 2025. The presence of AWS, Azure, and Google Cloud data centers in Texas, Virginia, and Oregon provides sub-10-millisecond latency for North American oil and gas clients.

Europe Oil and Gas Cloud Computing Market:

Europe held 24.1% of the oil and gas cloud computing market in 2025, valued at USD 1.74 Billion. The United Kingdom and Norway together accounted for 59% of European spending. North Sea operators adopted cloud-hosted asset management systems to extend the productive life of aging platforms. Equinor’s cloud-first strategy, built on Microsoft Azure, processes production data from 35 operated fields. Shell’s cloud migration covered its entire European refining and chemicals portfolio by 2025. BP deployed Google Cloud AI for predictive maintenance across its North Sea assets. Germany’s downstream sector used SAP S/4HANA Cloud for refinery ERP modernization, with BASF and Covestro leading adoption. Norway’s petroleum directorate mandated digital reporting formats compatible with OSDU cloud data standards, accelerating adoption. The EU Methane Regulation required continuous emissions monitoring, driving demand for cloud-based methane detection and reporting platforms across European operators.

Asia Pacific Oil and Gas Cloud Computing Market:

Asia Pacific captured 19.6% of market share in 2025, generating USD 1.41 Billion. China led the region with 39% of Asia Pacific revenue as CNOOC, PetroChina, and Sinopec deployed cloud platforms for offshore production management and refinery optimization. CNOOC’s partnership with Alibaba Cloud for South China Sea asset data processing established a regional reference deployment. Japan’s INPEX adopted AWS for Ichthys LNG operational analytics, processing 1.2 terabytes of daily production data. India’s ONGC and Reliance Industries initiated cloud migration for upstream data management in the Krishna-Godavari Basin and Jamnagar refinery complex. South Korea’s HD Hyundai used cloud platforms for FPSO construction project management and commissioning data workflows. Australia’s Woodside Energy operates on Google Cloud, running subsurface and production AI workloads for its Pluto and Scarborough LNG assets.

Latin America Oil and Gas Cloud Computing Market:

Latin America accounted for 8.5% of the global oil and gas cloud computing market in 2025, valued at USD 0.61 Billion. Brazil dominated with 61% of regional revenue, driven by Petrobras’s cloud strategy for pre-salt FPSO production data management. Petrobras migrated 42% of its upstream data workloads to cloud by 2025, processing production data from 15 FPSO units in the Santos and Campos basins. AWS and Azure established edge zones in São Paulo to support Brazilian energy clients with low-latency compute. Mexico’s Pemex adopted SaaS-based refinery management tools as part of its downstream modernization program. Argentina’s Vaca Muerta shale operators, including YPF and Vista Energy, deployed cloud-based drilling analytics to reduce non-productive time. Colombia’s Ecopetrol initiated a multi-cloud strategy across upstream and refining operations.

Middle East and Africa Oil and Gas Cloud Computing Market:

The Middle East and Africa held 7.5% of market share in 2025, generating USD 0.54 Billion, and represented the fastest-growing region with a projected CAGR of 17.8% through 2034. Saudi Aramco committed USD 500 Million to cloud infrastructure development under its In-Kingdom digitalization mandate, partnering with Google Cloud and AWS to build sovereign cloud zones within Saudi Arabia. ADNOC allocated USD 350 Million to its Panorama digital command center’s cloud migration, processing operational data from 16 production concessions and 4 refinery complexes. Qatar Energy deployed cloud-based LNG production optimization for the North Field East expansion, the largest LNG project globally. The UAE’s artificial intelligence strategy positioned Abu Dhabi as a cloud services hub for the broader Middle East energy sector. South Africa’s Sasol piloted cloud analytics for its Secunda complex, and Nigeria’s Dangote Refinery evaluated cloud-based process control for commissioning support. Data residency concerns are being addressed through in-country cloud zones established by AWS, Azure, and Oracle in Riyadh, Abu Dhabi, and Doha.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Model

- SaaS (Software-as-a-Service)

- IaaS (Infrastructure-as-a-Service)

- PaaS (Platform-as-a-Service)

By Operation

- Upstream

- Midstream

- Downstream

By Deployment

- Public Cloud

- Hybrid Cloud

- Private Cloud

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.2 B |

| Forecast Revenue (2034) | USD 22.8 B |

| CAGR (2025-2034) | 13.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Model , (SaaS (Software-as-a-Service), IaaS (Infrastructure-as-a-Service), PaaS (Platform-as-a-Service)), By Operation , (Upstream, Midstream, Downstream), By Deployment , (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size , (Large Enterprises, Small and Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT AZURE, AMAZON WEB SERVICES (AWS), GOOGLE CLOUD, SAP SE, IBM, ORACLE, ACCENTURE, HALLIBURTON, SLB (SCHLUMBERGER), INFORMATICA, COGNIZANT, WIPRO, TATA CONSULTANCY SERVICES, HEWLETT PACKARD ENTERPRISE, C3.AI, SNOWFLAKE, DATABRICKS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Operation (Upstream, Midstream, Downstream), By Deployment (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights, Key Players & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Deployment (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights, Key Players & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Deployment (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights, Key Players & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Cloud Computing Market?

Oil & gas cloud computing market valued at USD 6.34B in 2024, reaching USD 22.8B by 2034, growing at a CAGR of 13.6% from 2026–2034.

Who are the major players in the Oil and Gas Cloud Computing Market?

MICROSOFT AZURE, AMAZON WEB SERVICES (AWS), GOOGLE CLOUD, SAP SE, IBM, ORACLE, ACCENTURE, HALLIBURTON, SLB (SCHLUMBERGER), INFORMATICA, COGNIZANT, WIPRO, TATA CONSULTANCY SERVICES, HEWLETT PACKARD ENTERPRISE, C3.AI, SNOWFLAKE, DATABRICKS, Others

Which segments covered the Oil and Gas Cloud Computing Market?

By Service Model , (SaaS (Software-as-a-Service), IaaS (Infrastructure-as-a-Service), PaaS (Platform-as-a-Service)), By Operation , (Upstream, Midstream, Downstream), By Deployment , (Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size , (Large Enterprises, Small and Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Cloud Computing Market

Published Date : 31 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date