- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Corrosion Inhibitor Market Size 2034 | CAGR 5.1%

Global Oil and Gas Corrosion Inhibitor Market Size, Share, Growth & Industry Analysis By Inhibitor Type (Film-Forming Inhibitors, Neutralizing Inhibitors, Volatile Corrosion Inhibitors, Specialty Inhibitors), By Application (Production & Extraction, Pipeline Transportation, Refineries & Processing, Storage & Terminals), By Product Form (Liquid, Solid, Gas-Phase), By End-User (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 8.4 Billion | USD 13.2 Billion | 5.1% | North America, 34.2% |

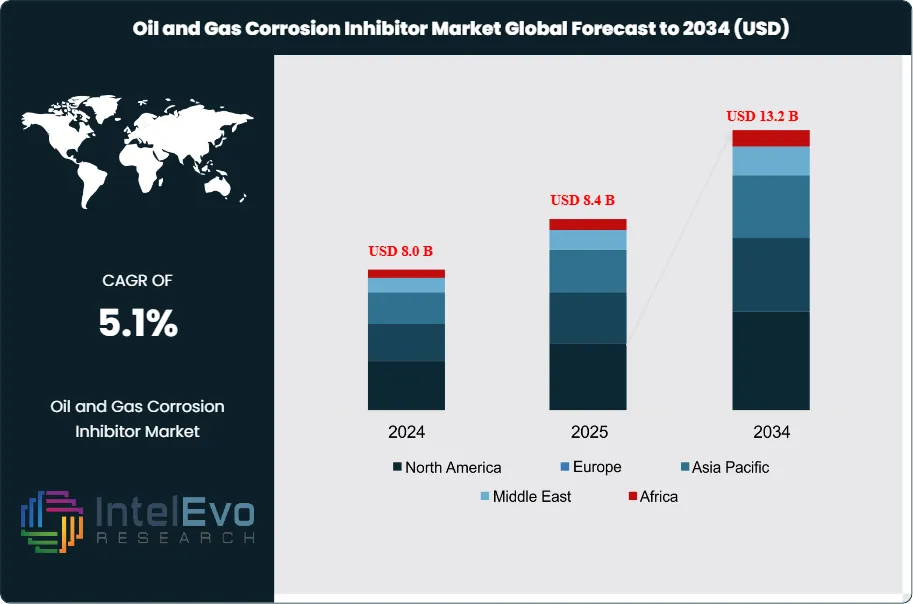

The Oil and Gas Corrosion Inhibitor Market was valued at approximately USD 8.0 Billion in 2024 and reached USD 8.4 Billion in 2025. The market is projected to grow to USD 13.2 Billion by 2034, expanding at a CAGR of 5.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.8 Billion over the analysis period. Corrosion inhibitors remain critical chemical solutions across upstream, midstream, and downstream oil and gas operations, protecting pipelines, storage tanks, refineries, and offshore platforms from degradation caused by hydrogen sulfide, carbon dioxide, oxygen, and chloride-bearing fluids.

Get More Information about this report -

Request Free Sample ReportMarket expansion is driven by aging infrastructure requiring enhanced protection, rising deepwater and ultra-deepwater exploration activities, and stricter environmental regulations mandating corrosion prevention to avoid leaks and spills. The American Petroleum Institute (API) standards and NACE International guidelines continue to shape product specifications, while operators increasingly demand environmentally compliant formulations that meet EPA discharge requirements and OSPAR Convention standards for offshore operations.

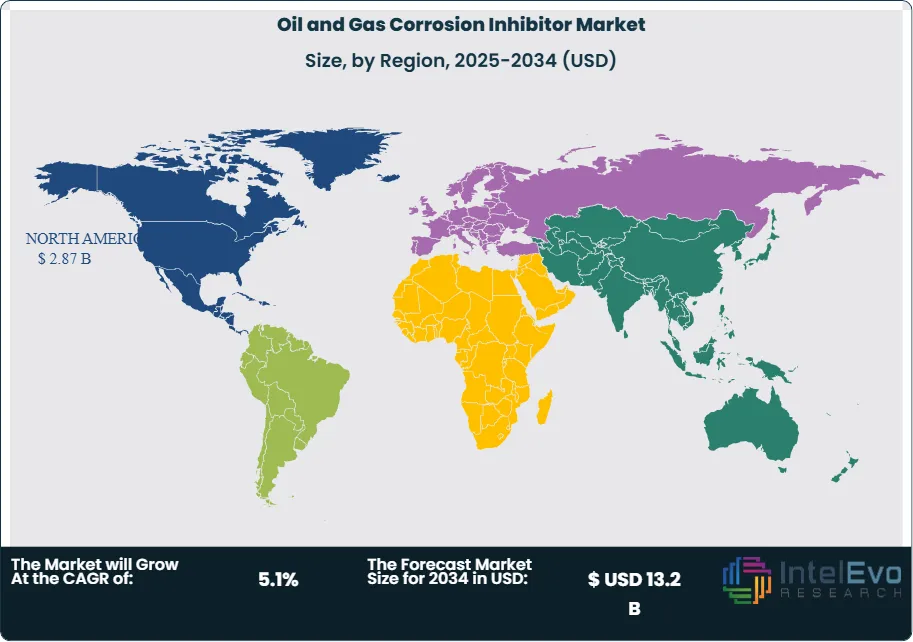

North America dominates the oil and gas corrosion inhibitor market with a 34.2% revenue share in 2025, valued at USD 2.87 Billion. The Permian Basin and Gulf of Mexico remain primary demand centers. The Middle East follows with 24.8% share, driven by sustained production from Saudi Aramco, ADNOC, and QatarEnergy. Asia Pacific captures 21.5% as refinery capacity expansions in China and India accelerate consumption of downstream corrosion control solutions.

Technology adoption is accelerating across the industry. Digital corrosion monitoring systems now integrate real-time sensors with predictive analytics, enabling operators to optimize inhibitor dosing and reduce chemical consumption by 15-25%. Film-forming amines and imidazoline-based chemistries lead product preferences for pipeline applications, while phosphate esters dominate refinery cooling water systems. The shift toward green chemistry has spurred development of bio-based inhibitors derived from plant extracts and amino acids, though performance validation in high-temperature, high-pressure (HTHP) environments remains ongoing. Offshore decommissioning activity in the North Sea and Gulf of Mexico is generating new demand for inhibitor treatments during well abandonment procedures.

, By Application (Production & Extraction, Pipeline Transportation, Refineries & Processing, Storage & Terminals), By Product Form (Liquid, Solid, Gas-Phase), By End-User (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas corrosion inhibitor market is projected to expand from USD 8.4 Billion in 2025 to USD 13.2 Billion by 2034, registering a CAGR of 5.1% during 2025-2034.

- Segment Dominance (By Type): Film-forming inhibitors command 42.3% market share in 2025, valued at USD 3.55 Billion, due to superior protective barrier capabilities in pipeline and production tubing applications.

- Segment Dominance (By Application): Production and extraction operations represent 38.7% of market demand in 2025 at USD 3.25 Billion, driven by corrosive conditions in wellbores and gathering systems.

- Driver: Aging pipeline infrastructure in North America and Europe requires corrosion management solutions. Over 65% of US transmission pipelines are more than 40 years old, creating sustained inhibitor demand.

- Restraint: Environmental regulations restricting certain chemical compounds, particularly BTEX-containing formulations, increase compliance costs by 12-18% and limit product options for operators.

- Opportunity: Bio-based and green corrosion inhibitors present a USD 1.2 Billion addressable market by 2034 as operators prioritize ESG compliance and reduced environmental footprints.

- Trend: Digital monitoring and automated dosing systems are being adopted by 35% of major operators in 2025, enabling real-time corrosion rate measurement and optimized chemical injection.

- Regional Analysis: North America leads the global market with 34.2% share and USD 2.87 Billion revenue in 2025, supported by extensive midstream infrastructure and active shale production.

Competitive Landscape Overview

The oil and gas corrosion inhibitor market exhibits moderate consolidation, with the top four players capturing approximately 52% combined market share in 2025. Ecolab Inc. leads through its Nalco Champion division, followed by BASF SE, Schlumberger (via M-I SWACO), and Halliburton. Competition centers on technology differentiation, with suppliers emphasizing digital integration, environmental compliance, and performance in sour service conditions. Recent strategic activity has intensified, including three acquisitions exceeding USD 500 million and multiple capacity expansions across the Middle East and Asia Pacific.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| ECOLAB INC. | US | Leader | Nalco Champion Platform | North America | Expanded digital corrosion monitoring suite (Feb 2025) |

| BASF SE | Germany | Leader | Corrprotec Series | Europe | Launched bio-based inhibitor line (Jan 2026) |

| SCHLUMBERGER (SLB) | US | Leader | M-I SWACO Corrosion Solutions | Global | Acquired specialty chemicals firm for USD 890M (Dec 2024) |

| HALLIBURTON | US | Challenger | Baroid Corrosion Control | North America | Integrated AI-driven dosing systems (Mar 2025) |

| BAKER HUGHES | US | Challenger | Tretolite Inhibitors | Middle East | Partnership with ADNOC for localized production (Jun 2025) |

| CLARIANT AG | Switzerland | Challenger | OilChem Protect Range | Europe | Opened new R&D center in Abu Dhabi (Sep 2025) |

| NOURYON | Netherlands | Niche Player | Berol Corrosion Inhibitors | Asia Pacific | Expanded capacity in Singapore facility (Nov 2025) |

| KEMIRA OYJ | Finland | Niche Player | KemGuard CI Series | Nordics | Launched low-toxicity offshore formulations (Jan 2026) |

By Inhibitor Type

The oil and gas corrosion inhibitor market segmentation by type reveals film-forming inhibitors as the dominant category with 42.3% share valued at USD 3.55 Billion in 2025. These inhibitors create protective barriers on metal surfaces through adsorption of organic molecules, particularly effective in pipeline and production tubing applications where continuous protection is required. Imidazoline and quaternary amine chemistries lead this segment. Neutralizing inhibitors hold 28.4% market share at USD 2.39 Billion, primarily addressing acid gas corrosion in production fluids containing H2S and CO2. These products function by raising pH levels and precipitating protective scales. Volatile corrosion inhibitors account for 18.1% share at USD 1.52 Billion, finding application in storage tanks, vapor spaces, and equipment preservation during shutdown periods. Specialty inhibitors including biocides with corrosion-inhibiting properties and scale-corrosion combination products comprise the remaining 11.2% at USD 0.94 Billion.

By Application

Application-based segmentation of the oil and gas corrosion inhibitor market positions production and extraction operations as the largest segment with 38.7% share worth USD 3.25 Billion in 2025. Corrosive conditions in wellbores, gathering systems, and separator equipment drive sustained demand for inhibitor treatments, particularly in sour gas fields and CO2-rich reservoirs. Pipeline transportation applications represent 31.2% share at USD 2.62 Billion, covering transmission pipelines, distribution networks, and export lines. Refineries and processing facilities account for 22.4% at USD 1.88 Billion, addressing corrosion in crude distillation units, hydrotreaters, and cooling water systems. Storage and terminal operations comprise 7.7% at USD 0.65 Billion, focusing on tank bottom protection and vapor phase corrosion control.

By Product Form

Product form analysis shows liquid inhibitors commanding 76.8% of the oil and gas corrosion inhibitor market in 2025, valued at USD 6.45 Billion. Liquid formulations enable precise dosing through chemical injection systems and batch treatments, supporting both continuous and intermittent application strategies. Water-soluble and oil-soluble variants address different fluid phase requirements. Solid inhibitors account for 14.3% share at USD 1.20 Billion, primarily deployed as sticks, pellets, or dissolvable capsules for downhole applications where liquid injection is impractical. These products suit remote wells and locations lacking chemical injection infrastructure. Gas-phase inhibitors represent 8.9% at USD 0.75 Billion, used for vapor space protection in storage vessels, pipelines during layup, and equipment preservation.

By End-User

End-user segmentation of the oil and gas corrosion inhibitor market reveals upstream operators as the primary consumers with 44.5% share at USD 3.74 Billion in 2025. National oil companies including Saudi Aramco, ADNOC, and Petrobras drive significant volume, alongside international majors and independent producers operating in corrosive environments. Midstream companies represent 32.8% at USD 2.76 Billion, with pipeline operators such as Kinder Morgan, Enterprise Products, and Transneft maintaining extensive corrosion management programs. Downstream refiners and petrochemical operators account for 22.7% at USD 1.90 Billion, addressing process unit corrosion, cooling system protection, and tankage integrity.

Regional Analysis

North America

North America commands 34.2% of the global oil and gas corrosion inhibitor market with USD 2.87 Billion revenue in 2025. The United States dominates regional consumption at 82% share, driven by extensive pipeline networks exceeding 2.6 million miles and active shale production in the Permian Basin, Eagle Ford, and Bakken formations. The Pipeline and Hazardous Materials Safety Administration (PHMSA) mandates corrosion control programs, sustaining inhibitor demand. Aging infrastructure presents particular challenges; over 65% of US transmission pipelines were constructed before 1985. Canada contributes 14% of regional demand, with oil sands operations in Alberta and offshore production off Newfoundland requiring specialized high-temperature formulations. Mexico accounts for 4% as Pemex maintenance programs and new private operator activity drive consumption. Digital corrosion monitoring adoption leads globally, with 42% of major US operators implementing real-time sensing and automated dosing systems.

Europe

Europe represents 14.3% of the oil and gas corrosion inhibitor market with USD 1.20 Billion in 2025. The United Kingdom leads regional demand at 28% share, driven by North Sea production and significant decommissioning activity requiring corrosion management during well abandonment. Norway follows at 24%, with Equinor and Aker BP maintaining extensive corrosion control programs across offshore platforms. Germany accounts for 18% through refinery operations and natural gas transmission networks. The Netherlands contributes 12% from the Groningen field operations and Rotterdam refining complex. OSPAR Convention compliance shapes product requirements, restricting certain chemical compounds in offshore discharge waters. The European Chemicals Agency (ECHA) REACH regulations mandate extensive documentation for corrosion inhibitor products, increasing compliance costs but also driving innovation toward green chemistry solutions.

Asia Pacific

Asia Pacific captures 21.5% of the oil and gas corrosion inhibitor market with USD 1.81 Billion in 2025 and represents the fastest-growing region at 6.3% CAGR through 2034. China leads at 38% regional share, driven by refinery capacity exceeding 17 million barrels per day and extensive pipeline buildout under the West-East Gas Pipeline network. India follows at 22%, with downstream capacity additions and aging refinery infrastructure creating sustained demand. Australia contributes 16% through LNG export facilities in Western Australia and Queensland, where seawater cooling systems require specialized inhibitor treatments. Japan accounts for 12% via refinery operations and chemical processing. Southeast Asian producers in Indonesia, Malaysia, and Vietnam collectively represent 12% as offshore production in the South China Sea expands. Local manufacturing capacity is increasing, with BASF, Clariant, and regional producers establishing production facilities in China and Singapore.

Latin America

Latin America accounts for 8.4% of the oil and gas corrosion inhibitor market with USD 0.71 Billion in 2025. Brazil dominates at 52% regional share, with Petrobras pre-salt operations requiring advanced corrosion management for deepwater production in highly corrosive CO2-rich environments. Water depths exceeding 2,000 meters and reservoir temperatures above 65 degrees Celsius demand specialized inhibitor formulations. Mexico represents 28% as Pemex refinery rehabilitation programs and private operator activity in shallow water Campeche Bay drive demand. Argentina contributes 12% through Vaca Muerta shale development and conventional production in the Neuquen Basin. Colombia accounts for 8% via pipeline operations and refinery consumption. Regional growth is supported by infrastructure investment programs, though economic volatility in Argentina and regulatory uncertainty in Mexico create demand fluctuations.

Middle East and Africa

The Middle East and Africa region holds 21.6% of the oil and gas corrosion inhibitor market with USD 1.81 Billion in 2025. Saudi Arabia leads at 35% regional share, with Saudi Aramco operating extensive production and pipeline networks requiring comprehensive corrosion management. The Kingdom's Vision 2030 downstream expansion programs are adding refinery capacity and petrochemical complexes. The UAE follows at 24%, with ADNOC's production operations and Ruwais refinery complex driving demand. Qatar contributes 15% through LNG production at Ras Laffan and domestic gas network operations. Kuwait accounts for 10% via refinery operations and production facilities. Nigeria represents the primary African demand center at 8% regional share, with Shell, TotalEnergies, and NNPC managing corrosion challenges in the Niger Delta. The region benefits from localized production, with suppliers establishing blending facilities in Dubai, Saudi Arabia, and Abu Dhabi to serve regional markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Inhibitor Type

- Film-Forming Inhibitors

- Neutralizing Inhibitors

- Volatile Corrosion Inhibitors

- Specialty Inhibitors

By Application

- Production and Extraction

- Pipeline Transportation

- Refineries and Processing

- Storage and Terminals

By Product Form

- Liquid Inhibitors

- Solid Inhibitors

- Gas-Phase Inhibitors

By End-User

- Upstream Operators

- Midstream Companies

- Downstream Refiners

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.4 B |

| Forecast Revenue (2034) | USD 13.2 B |

| CAGR (2025-2034) | 5.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Inhibitor Type, (Film-Forming Inhibitors, Neutralizing Inhibitors, Volatile Corrosion Inhibitors, Specialty Inhibitors), By Application, (Production and Extraction, Pipeline Transportation, Refineries and Processing, Storage and Terminals), By Product Form, (Liquid Inhibitors, Solid Inhibitors, Gas-Phase Inhibitors), By End-User, (Upstream Operators, Midstream Companies, Downstream Refiners) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ECOLAB INC., BASF SE, SCHLUMBERGER (SLB), HALLIBURTON, BAKER HUGHES, CLARIANT AG, NOURYON, KEMIRA OYJ, INNOSPEC INC., CHAMPIONX CORPORATION, EVONIK INDUSTRIES AG, AKZONOBEL N.V., CRODA INTERNATIONAL PLC, SOLVAY S.A., HUNTSMAN CORPORATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Production & Extraction, Pipeline Transportation, Refineries & Processing, Storage & Terminals), By Product Form (Liquid, Solid, Gas-Phase), By End-User (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Application (Production & Extraction, Pipeline Transportation, Refineries & Processing, Storage & Terminals), By Product Form (Liquid, Solid, Gas-Phase), By End-User (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Application (Production & Extraction, Pipeline Transportation, Refineries & Processing, Storage & Terminals), By Product Form (Liquid, Solid, Gas-Phase), By End-User (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Corrosion Inhibitor Market?

Global oil & gas corrosion inhibitor market was valued at USD 8.0B in 2024, reaching USD 13.2B by 2034, growing at a CAGR of 5.1% from 2026–2034.

Who are the major players in the Oil and Gas Corrosion Inhibitor Market?

ECOLAB INC., BASF SE, SCHLUMBERGER (SLB), HALLIBURTON, BAKER HUGHES, CLARIANT AG, NOURYON, KEMIRA OYJ, INNOSPEC INC., CHAMPIONX CORPORATION, EVONIK INDUSTRIES AG, AKZONOBEL N.V., CRODA INTERNATIONAL PLC, SOLVAY S.A., HUNTSMAN CORPORATION, Others

Which segments covered the Oil and Gas Corrosion Inhibitor Market?

By Inhibitor Type, (Film-Forming Inhibitors, Neutralizing Inhibitors, Volatile Corrosion Inhibitors, Specialty Inhibitors), By Application, (Production and Extraction, Pipeline Transportation, Refineries and Processing, Storage and Terminals), By Product Form, (Liquid Inhibitors, Solid Inhibitors, Gas-Phase Inhibitors), By End-User, (Upstream Operators, Midstream Companies, Downstream Refiners)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Corrosion Inhibitor Market

Published Date : 27 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date