- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Cybersecurity Market Size & Forecast 2034 | CAGR 12.1%

Global Oil and Gas Cybersecurity Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Operation (Upstream Exploration & Production, Midstream, Downstream Refining & Petrochemical) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 3.2 Billion | USD 8.9 Billion | 12.1% | North America, 41.2% |

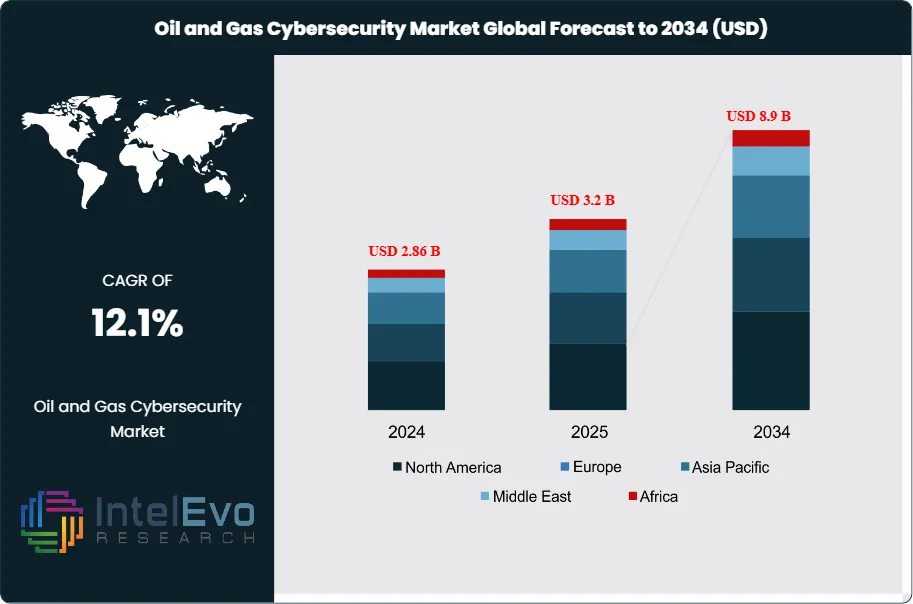

The Oil and Gas Cybersecurity Market was valued at approximately USD 2.86 Billion in 2024 and reached USD 3.2 Billion in 2025. The market is projected to grow to USD 8.9 Billion by 2034, expanding at a CAGR of 12.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.7 billion over the analysis period. Oil and gas cybersecurity encompasses specialized security solutions designed to protect critical infrastructure across upstream exploration and production, midstream pipeline transportation, and downstream refining operations from increasingly sophisticated cyber threats targeting operational technology (OT) and industrial control systems (ICS).

Get More Information about this report -

Request Free Sample ReportRising cyberattack frequency against energy infrastructure drives urgent security investments across the petroleum value chain. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) recorded a 47% increase in reported incidents targeting oil and gas facilities between 2023 and 2025. Ransomware attacks on pipeline operators, state-sponsored intrusions into refinery control systems, and supply chain compromises affecting drilling operations have elevated cybersecurity from an IT concern to a board-level priority. Major operators now allocate 3.5-4.2% of total IT budgets to OT security, up from 2.1% in 2022. The convergence of information technology and operational technology networks creates expanded attack surfaces that legacy security architectures cannot adequately protect.

Regulatory mandates accelerate market expansion across key producing regions. The U.S. Transportation Security Administration (TSA) issued binding directives requiring pipeline operators to implement specific cybersecurity measures following the Colonial Pipeline incident. The European Union's NIS2 Directive designates oil and gas operators as essential entities subject to stringent security requirements. Saudi Arabia's National Cybersecurity Authority mandates compliance frameworks for all energy sector participants. These regulatory pressures compel operators to deploy network segmentation, intrusion detection systems, and security operations center capabilities. The oil and gas cybersecurity market benefits directly from compliance-driven spending that carries multi-year implementation timelines.

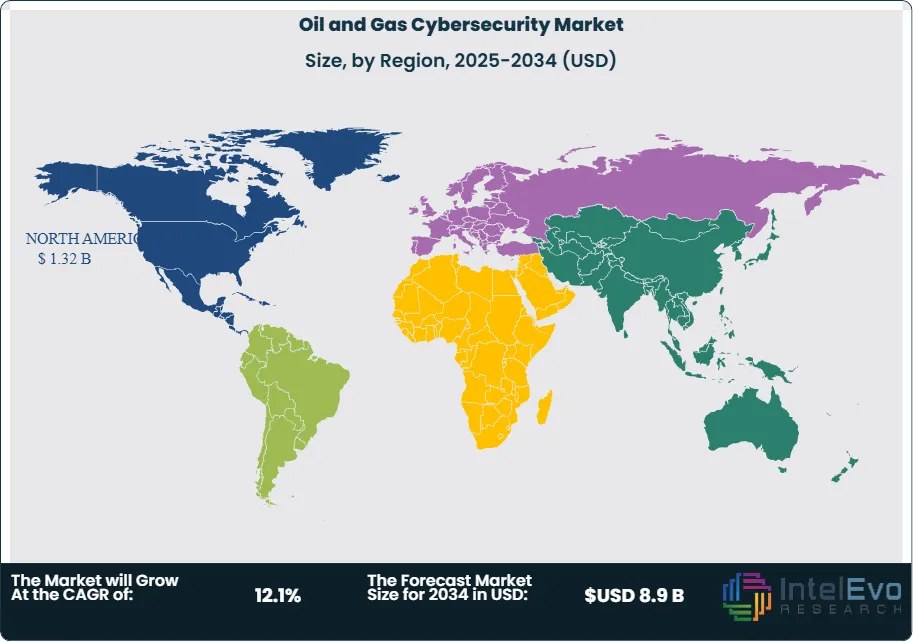

Technology evolution shapes competitive dynamics within the market. Artificial intelligence and machine learning enable anomaly detection across vast sensor networks monitoring drilling rigs, pipelines, and processing facilities. Zero trust architectures replace perimeter-based security models inadequate for distributed oilfield operations. Managed security service providers gain traction among mid-sized operators lacking in-house expertise. North America commands 41.2% of global revenue (USD 1.32 billion, 2025), driven by regulatory intensity and high-profile incident awareness. The Middle East represents the fastest-growing region as national oil companies prioritize digital transformation security. Asia Pacific operators accelerate spending following attacks on regional LNG facilities and offshore platforms.

Investment patterns reflect differentiated priorities across operational segments. Upstream operators focus on securing SCADA systems controlling wellhead operations, drilling automation, and reservoir monitoring. Midstream players prioritize pipeline control system protection and leak detection integrity. Downstream refineries and petrochemical facilities invest in process safety system security and compliance management. Managed detection and response services capture growing share as operators seek 24/7 threat monitoring without building dedicated security operations centers. The competitive field includes established IT security vendors expanding into OT markets, specialized industrial cybersecurity firms, and oilfield service companies integrating security into digital offerings.

, By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Operation (Upstream Exploration & Production, Midstream, Downstream Refining & Petrochemical) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas cybersecurity market will expand from USD 3.2 billion in 2025 to USD 8.9 billion by 2034, reflecting a CAGR of 12.1% across the nine-year forecast period.

- Segment Dominance: Solutions held 62.4% market share in 2025, generating USD 2.0 billion in revenue as operators prioritized network security, endpoint protection, and SIEM platform deployments.

- Segment Dominance: Upstream exploration and production applications accounted for 44.8% of market revenue (USD 1.43 billion, 2025), driven by SCADA protection requirements and drilling system security.

- Driver: Escalating cyberattack frequency increased reported incidents against oil and gas infrastructure by 47% between 2023 and 2025, compelling USD 2.8 billion in incremental security investments.

- Restraint: Skilled OT security workforce shortages limit deployment capacity; 58% of oil and gas operators report unfilled cybersecurity positions averaging 9-month vacancy durations.

- Opportunity: Managed security services for mid-sized operators represent a USD 1.8 billion addressable opportunity through 2034 as outsourcing models mature and service coverage expands.

- Trend: AI-powered threat detection adoption accelerated; 43% of large operators deployed machine learning anomaly detection in 2025 versus 19% in 2023.

- Regional Analysis: North America led with 41.2% share and USD 1.32 billion revenue in 2025, supported by TSA pipeline directives and SEC cyber disclosure requirements.

Competitive Landscape Overview

The oil and gas cybersecurity market exhibits moderate fragmentation, with the top four players commanding approximately 38% combined market share in 2025. Competition centers on OT-specific expertise, integration capabilities with industrial control systems, and managed service delivery models. Strategic M&A activity intensified as general-purpose security vendors acquired OT specialists; four acquisitions exceeding USD 200 million each closed between December 2024 and March 2026. Partnerships between cybersecurity firms and oilfield service companies accelerate go-to-market execution. New entrants from defense and government cybersecurity backgrounds target the energy sector, intensifying competitive pressure on incumbents.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Fortinet | US | Leader | FortiGate OT Security | North America | Launched OT-specific threat intelligence feed (Feb 2025) |

| Palo Alto Networks | US | Leader | Prisma OT Security | North America | Acquired Talon Cyber for USD 625M (Dec 2024) |

| Claroty | US | Leader | Claroty xDome | Global | Signed USD 180M ADNOC enterprise deal (Mar 2025) |

| Dragos | US | Leader | Dragos Platform | North America | Expanded to Middle East with Aramco partnership (Jun 2025) |

| Nozomi Networks | US | Challenger | Guardian Platform | Europe | Raised USD 100M Series E funding (Sep 2025) |

| Honeywell | US | Challenger | Forge Cybersecurity | Middle East | Launched managed OT SOC service (Jan 2026) |

| Cisco Systems | US | Challenger | Cyber Vision | North America | Integrated OT visibility into SecureX platform (Aug 2025) |

| Tenable | US | Challenger | Tenable OT Security | North America | Added ICS vulnerability prioritization engine (Apr 2025) |

| Check Point | Israel | Niche Player | Quantum IoT Protect | Europe | Won BP North Sea security contract (Nov 2025) |

| Opswat | US | Niche Player | MetaDefender OT | Asia Pacific | Expanded Petronas partnership scope (Oct 2025) |

Segmentation Analysis

Oil and gas cybersecurity market segmentation reveals distinct adoption patterns across solution types, security categories, deployment models, and operational segments. Each segment exhibits unique growth drivers, competitive dynamics, and regional concentration that shape vendor strategies and investment priorities.

By Offering

Solutions dominated the oil and gas cybersecurity market with a 62.4% share generating USD 2.0 billion in 2025. This segment encompasses network security appliances, endpoint protection platforms, security information and event management (SIEM) systems, and specialized OT security tools. Network security solutions captured the largest revenue share within solutions as operators deployed next-generation firewalls and intrusion prevention systems specifically configured for industrial protocols including Modbus, DNP3, and OPC-UA. Endpoint protection expanded rapidly as drilling contractors and pipeline operators secured thousands of distributed devices across remote locations. SIEM platforms tailored for OT environments gained adoption among large operators seeking centralized visibility across geographically dispersed assets. Services contributed 37.6% (USD 1.2 billion, 2025) encompassing managed security services, professional consulting, and incident response capabilities. Managed security services appeal to mid-sized operators lacking resources for dedicated security operations centers. Professional services support compliance assessments, security architecture design, and integration projects. Incident response retainers provide rapid expert assistance following security events.

By Security Type

Network security held 34.2% market share (USD 1.09 billion, 2025) as operators prioritized perimeter defense and network segmentation between IT and OT environments. Industrial firewalls protecting SCADA networks and pipeline control systems drive segment growth. Endpoint security captured 23.8% share (USD 0.76 billion, 2025), reflecting expansion of protection to field devices, human-machine interfaces, and engineering workstations. Application security accounted for 18.4% (USD 0.59 billion, 2025), covering security testing for custom applications controlling drilling operations and refinery processes. Cloud security represented 13.6% (USD 0.44 billion, 2025) as operators migrated analytics workloads and historian data to cloud environments. Data security held 10.0% share (USD 0.32 billion, 2025), encompassing encryption, data loss prevention, and access controls protecting proprietary reservoir data and operational information.

By Deployment Mode

On-premises deployment captured 58.3% market share (USD 1.87 billion, 2025) as operators maintained security infrastructure within facility boundaries to protect air-gapped OT networks. Critical infrastructure regulations in multiple jurisdictions mandate on-premises deployment for specific security functions. Large operators with existing data center infrastructure favor on-premises models that integrate with established IT management frameworks. Cloud-based deployment held 28.4% share (USD 0.91 billion, 2025), gaining traction for threat intelligence, security analytics, and managed detection services where cloud elasticity provides cost advantages. Hybrid deployment accounted for 13.3% (USD 0.42 billion, 2025), enabling operators to maintain on-premises controls for critical OT systems while leveraging cloud platforms for advanced analytics and global threat intelligence correlation.

By Operation

Upstream exploration and production represented 44.8% of market revenue (USD 1.43 billion, 2025), driven by SCADA security requirements for wellhead automation, drilling system protection, and offshore platform network defense. Permian Basin operators deploy comprehensive security stacks across thousands of connected wells. Offshore platforms in the Gulf of Mexico and North Sea invest in maritime-specific cybersecurity addressing unique vessel-to-shore communication vulnerabilities. Midstream operations accounted for 31.5% (USD 1.01 billion, 2025), dominated by pipeline control system security investments following high-profile attacks and TSA directive mandates. Gas processing facilities and storage terminals contribute to midstream security spending. Downstream refining and petrochemical operations held 23.7% share (USD 0.76 billion, 2025), focusing on distributed control system protection, safety instrumented system integrity, and compliance with chemical facility anti-terrorism standards.

Regional Analysis

North America

North America commanded 41.2% of the oil and gas cybersecurity market with USD 1.32 billion revenue in 2025. The United States dominates regional demand, contributing 87% of North American cybersecurity spending driven by TSA Security Directives for pipeline operators and SEC cyber disclosure requirements for public companies. The Colonial Pipeline attack permanently elevated board-level attention to OT security across U.S. energy operators. Permian Basin producers deploy network segmentation and monitoring across distributed well networks. Gulf of Mexico deepwater operators invest in secure remote access solutions for offshore platforms. Canada's oil sands operators and Montney gas producers accelerate security programs following cross-border threat intelligence sharing. Mexico's PEMEX faces elevated attack volumes, though budget constraints limit response capacity. U.S.-headquartered cybersecurity vendors including Fortinet, Palo Alto Networks, Claroty, and Dragos maintain competitive advantages through domestic relationships and regulatory expertise.

Europe

Europe accounted for 24.6% of global market share (USD 0.79 billion, 2025), anchored by North Sea operators implementing NIS2 Directive compliance programs. The United Kingdom's National Cyber Security Centre issues sector-specific guidance for oil and gas operators that shapes security architectures. Norway's offshore operators including Equinor deploy advanced OT monitoring across platform networks. The Netherlands' Rotterdam refinery complex represents concentrated downstream security investment. Germany's pipeline operators accelerate spending following European energy security concerns. The European Union's designation of oil and gas as essential infrastructure under NIS2 creates binding compliance requirements effective 2025, driving multi-year security program investments. European operators favor vendors with local presence and GDPR-compliant data handling capabilities. Kongsberg Digital and Siemens compete effectively in regional markets through established industrial relationships.

Asia Pacific

Asia Pacific held 18.7% market share (USD 0.60 billion, 2025), led by Australia's LNG operators implementing cyber resilience frameworks and China's national oil companies securing critical infrastructure. Japan's refinery operators invest in safety system protection following regional threat actor targeting. India's Oil and Natural Gas Corporation and Reliance Industries deploy security upgrades across aging infrastructure. Southeast Asian operators including Malaysia's Petronas, Indonesia's Pertamina, and Thailand's PTTEP accelerate security investments following attacks on regional facilities. Singapore serves as the regional hub for managed security services delivery. Asia Pacific growth outpaces global averages as regulatory frameworks mature and incident awareness increases among regional operators. Local system integrators partner with global security vendors to address language and support requirements.

Latin America

Latin America represented 8.3% of global revenue (USD 0.27 billion, 2025), dominated by Brazil's Petrobras cybersecurity modernization program. Pre-salt offshore operations require secure remote monitoring and vessel communications. Argentina's Vaca Muerta shale operators import security practices from North American partners. Colombia's Ecopetrol invests in pipeline monitoring following historical infrastructure targeting. Mexico's PEMEX faces significant security challenges with limited budget allocation despite high attack volumes. Regional growth prospects depend on commodity price recovery and national oil company capital availability. International operators bring global security standards to regional joint ventures, indirectly expanding the addressable market. Managed security services gain traction as cost-effective alternatives to building in-house capabilities.

Middle East and Africa

The Middle East and Africa region captured 7.2% market share (USD 0.23 billion, 2025) but exhibits strong growth potential as national oil companies prioritize digital transformation security. Saudi Aramco's cybersecurity program represents the region's largest investment, deploying defense-in-depth architectures across the world's largest conventional oil production complex. ADNOC's USD 180 million security program with Claroty establishes a regional benchmark. Qatar Energy invests in LNG facility protection ahead of North Field expansion. Kuwait Oil Company and Iraq's national operators represent emerging opportunities despite operational challenges. Sub-Saharan Africa's market concentrates on offshore Nigeria and Angola, where international operators apply global security standards. The Middle East's rapid digitalization creates expanding attack surfaces that national cybersecurity authorities mandate for protection. Regional demand for Arabic-language security operations and local data residency shapes vendor strategies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions

- Services

By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Data Security

By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid

By Operation

- Upstream Exploration and Production

- Midstream Operations

- Downstream Refining and Petrochemical

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.2 B |

| Forecast Revenue (2034) | USD 8.9 B |

| CAGR (2025-2034) | 12.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Solutions, Services), By Security Type, (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode, (On-Premises, Cloud-Based, Hybrid), By Operation, (Upstream Exploration and Production, Midstream Operations, Downstream Refining and Petrochemical) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | FORTINET, PALO ALTO NETWORKS, CLAROTY, DRAGOS, NOZOMI NETWORKS, HONEYWELL INTERNATIONAL, CISCO SYSTEMS, TENABLE, CHECK POINT SOFTWARE, OPSWAT, MICROSOFT, SIEMENS, ABB, SCHNEIDER ELECTRIC, ARMIS, CROWDSTRIKE, TRELLIX, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Operation (Upstream Exploration & Production, Midstream, Downstream Refining & Petrochemical) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Operation (Upstream Exploration & Production, Midstream, Downstream Refining & Petrochemical) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By Operation (Upstream Exploration & Production, Midstream, Downstream Refining & Petrochemical) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Cybersecurity Market?

Global Oil & gas cybersecurity market valued at USD 2.86B in 2024, reaching USD 8.9B by 2034, growing at a CAGR of 12.1% from 2026–2034.

Who are the major players in the Oil and Gas Cybersecurity Market?

FORTINET, PALO ALTO NETWORKS, CLAROTY, DRAGOS, NOZOMI NETWORKS, HONEYWELL INTERNATIONAL, CISCO SYSTEMS, TENABLE, CHECK POINT SOFTWARE, OPSWAT, MICROSOFT, SIEMENS, ABB, SCHNEIDER ELECTRIC, ARMIS, CROWDSTRIKE, TRELLIX, Others

Which segments covered the Oil and Gas Cybersecurity Market?

By Offering, (Solutions, Services), By Security Type, (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security), By Deployment Mode, (On-Premises, Cloud-Based, Hybrid), By Operation, (Upstream Exploration and Production, Midstream Operations, Downstream Refining and Petrochemical)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Cybersecurity Market

Published Date : 01 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date