- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Decommissioning Market Forecast 2034 | CAGR 7.3%

Global Oil & Gas Decommissioning Market Size, Share, Growth & Industry Analysis By Service Type (Well Plugging & Abandonment, Platform Removal, Pipeline Decommissioning, Conductor & Casing Removal, Site Remediation), By Location (Offshore, Onshore), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater) Industry Trends, Competitive Landscape, Market Dynamics, Investment Analysis & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 8.4 Billion | USD 15.8 Billion | 7.3% | Europe, 42.5% |

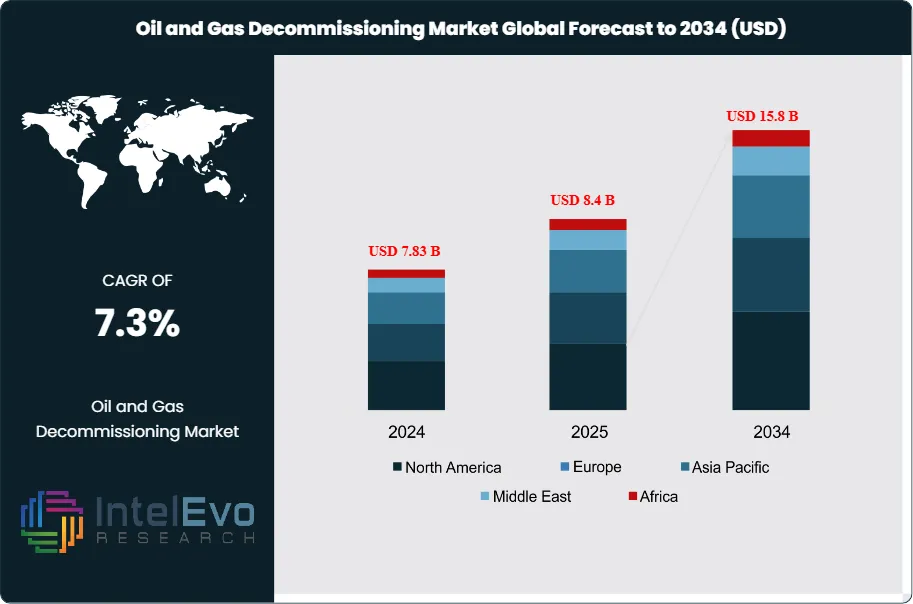

The Oil and Gas Decommissioning Market was valued at approximately USD 7.83 Billion in 2024 and reached USD 8.4 Billion in 2025. The market is projected to grow to USD 15.8 Billion by 2034, expanding at a CAGR of 7.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.4 Billion over the analysis period. The oil and gas decommissioning sector encompasses the complete removal, disposal, and site remediation of offshore and onshore petroleum infrastructure that has reached end of productive life. Operators face mounting regulatory pressure from agencies including BSEE, OSPAR, and NOPSEMA to permanently plug wells, remove platforms, and restore seabed conditions within mandated timeframes.

Get More Information about this report -

Request Free Sample ReportThe North Sea region drives global decommissioning activity, with over 470 platforms scheduled for removal by 2035 under OSPAR Decision 98/3 requirements. The United Kingdom alone has committed approximately USD 52 Billion in total decommissioning liability across its continental shelf, with annual expenditure projected to exceed USD 2.3 Billion through the forecast period. Norway, the second largest European market, has allocated USD 18 Billion for Cessation of Production activities through 2040. These regulatory mandates create a predictable, backlog-driven demand structure distinct from exploration and production spending cycles.

The Gulf of Mexico represents the second largest regional market, where BSEE regulations require idle iron removal within defined timeframes. Over 1,800 platforms currently operate in US federal waters, with an estimated 35% approaching end-of-life status by 2030. Brazil's Pre-Salt fields present emerging decommissioning requirements as first-generation FPSOs reach 25-year design limits. Asia Pacific decommissioning activity accelerates in Malaysia, Indonesia, and Australia, where mature fields from 1970s and 1980s development enter final production decline.

Technology advances are reducing per-unit decommissioning costs by 15–20% through single-lift removal methods, modular processing of topsides, and improved well plug and abandonment techniques. Digital twins and AI-based planning tools have decreased project execution times by 12% since 2022. Environmental regulations governing drill cuttings disposal, produced water treatment, and seabed debris clearance continue to tighten across all major jurisdictions. The oil and gas decommissioning market will expand substantially as the global installed base of aging infrastructure reaches mandatory retirement thresholds.

, By Location (Offshore, Onshore), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater) Industry Trends, Competitive Landscape, Market Dynamics, Investment Analysis & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas decommissioning market is projected to grow from USD 8.4 Billion in 2025 to USD 15.8 Billion by 2034, registering a CAGR of 7.3% during the forecast period.

- Segment Dominance (Service Type): Well plugging and abandonment services lead the market with a 38.2% share in 2025, driven by regulatory mandates requiring permanent well isolation before structure removal.

- Segment Dominance (Location): Offshore decommissioning dominates with a 72.8% market share in 2025, reflecting the concentration of end-of-life infrastructure in shallow and deepwater marine environments.

- Driver: Regulatory enforcement timelines have accelerated decommissioning activity by 28% since 2020, with BSEE and OSPAR mandating specific removal deadlines for idle infrastructure.

- Restraint: Specialized heavy-lift vessel availability constraints add 8–12 months to project schedules, with global fleet utilization exceeding 85% during peak summer work seasons.

- Opportunity: Rigs-to-reefs conversion programs represent a USD 1.8 Billion addressable market opportunity through 2034, with 12 US states now permitting artificial reef placement.

- Trend: Late-life asset consolidation increased 42% between 2020 and 2025, with specialist operators acquiring mature fields to capture decommissioning synergies across clustered infrastructure.

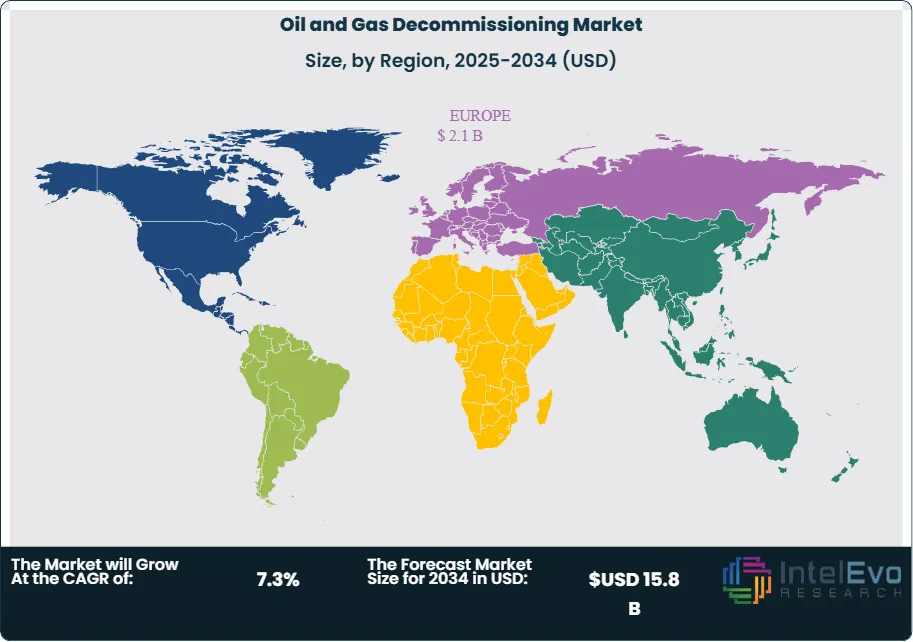

- Regional Analysis: Europe leads the market with a 42.5% share, equivalent to USD 3.6 Billion in 2025, driven by North Sea platform removal mandates under OSPAR regulations.

Competitive Landscape Overview

The oil and gas decommissioning market exhibits moderate fragmentation, with the top four players commanding approximately 32% of global revenue in 2025. Competition is capability-driven, with heavy-lift vessel access, well abandonment expertise, and regulatory track records determining contract awards. Recent industry consolidation includes multiple acquisitions aimed at expanding integrated service offerings. New market entrants from marine salvage and offshore wind decommissioning sectors have increased competitive intensity in shallow water segments.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| TechnipFMC | UK | Leader | Subsea Decommissioning | Global | Acquired DOF Subsea decommissioning unit for USD 420M (Feb 2025) |

| Petrofac | UK | Leader | Late Life Management | North Sea | Secured GBP 580M North Sea decommissioning contract (Mar 2025) |

| Aker Solutions | Norway | Leader | Platform Removal Services | Europe | Expanded Norwegian Cessation of Production capacity (Jan 2025) |

| Wood PLC | UK | Leader | Well P&A Services | Europe/Americas | Launched digital decommissioning planning platform (Dec 2024) |

| SLB | US | Challenger | Integrated Well Services | Global | Signed Gulf of Mexico P&A framework agreement (Apr 2025) |

| Helix Energy | US | Challenger | Well Intervention Vessels | Americas | Deployed Q7000 for deepwater P&A campaign (Jun 2025) |

| AF Gruppen | Norway | Niche | Onshore Recycling Yards | Norway | Opened 280,000 sqm decommissioning facility (Sep 2025) |

| Allseas | Netherlands | Niche | Heavy Lift Removal | Europe | Completed single-lift platform removal record (Nov 2025) |

| Heerema | Netherlands | Challenger | Offshore Heavy Lift | Global | Awarded Shell North Sea removal contract (Jan 2026) |

| Acteon Group | UK | Niche | Subsea Asset Integrity | Europe/APAC | Launched autonomous seabed clearance system (Feb 2026) |

Segmentation Analysis

The oil and gas decommissioning market segments by service type into well plugging and abandonment, platform removal, pipeline decommissioning, conductor and casing removal, and site remediation. Each service category addresses distinct phases of the decommissioning lifecycle, from initial well isolation through final seabed clearance. The market further segments by location into offshore and onshore operations, and by water depth into shallow water, deepwater, and ultra-deepwater categories.

By Service Type

Well plugging and abandonment services command the largest market share at 38.2%, generating USD 3.2 Billion in 2025. P&A operations involve permanent isolation of hydrocarbon zones through cement plugs, mechanical barriers, and casing cuts at specified depths below mudline. Regulatory requirements from BSEE, OSPAR, and NOPSEMA mandate specific barrier verification protocols prior to structure removal. Average well P&A costs range from USD 1.5 Million for shallow water wells to USD 15 Million for deepwater completions, with multi-lateral and high-pressure wells commanding premium pricing. The backlog of temporarily abandoned wells requiring permanent P&A exceeds 2,800 units across the Gulf of Mexico alone.

Platform removal services hold a 28.4% market share, equivalent to USD 2.4 Billion in 2025. Removal operations encompass topside module separation, jacket cutting, and heavy-lift transportation to onshore dismantling yards. Single-lift removal techniques using heavy-lift vessels such as Pioneering Spirit have reduced per-platform costs by 25% compared to traditional reverse installation methods. The North Sea contains 470 platforms scheduled for removal through 2035, while the Gulf of Mexico holds over 650 end-of-life structures. Platform removal requires coordination with heavy-lift vessel schedules, with global fleet capacity constraints creating 12–18 month lead times for major projects.

Pipeline decommissioning captures 16.8% of market value at USD 1.4 Billion in 2025. Options include complete removal, leave-in-place with cleaning, and burial for large-diameter trunk lines. OSPAR guidelines generally favor complete removal for pipelines under 16 inches diameter, while larger lines may receive derogation for in-situ decommissioning following cleaning and rock dumping. Pipeline decommissioning costs average USD 3–5 Million per kilometer depending on diameter, burial depth, and seabed conditions. The North Sea pipeline network exceeds 45,000 kilometers, with significant portions approaching end-of-design-life status.

Conductor and casing removal accounts for 10.2% of market value at USD 0.9 Billion in 2025. Post-P&A operations require cutting conductors and casings at specified depths below mudline to eliminate seabed obstructions. Abrasive water jet cutting and mechanical cutting methods have improved efficiency by 30% since 2020. Regulatory requirements vary by jurisdiction, with BSEE mandating 15-foot below-mudline cuts and OSPAR requiring removal to natural seabed level.

Site remediation represents 6.4% of market share at USD 0.5 Billion in 2025. Final decommissioning phases involve seabed debris clearance, drill cuttings pile assessment, and habitat restoration where required. Autonomous underwater vehicle surveys verify site clearance to regulatory standards. Drill cuttings piles at older North Sea platforms contain legacy hydrocarbon contamination requiring monitoring or active remediation in some cases.

By Location

Offshore decommissioning dominates the market with a 72.8% share, reflecting the concentration of end-of-life infrastructure in marine environments. The global offshore platform inventory exceeds 7,500 installations, with approximately 2,500 structures expected to require decommissioning by 2035. Offshore operations face unique logistical challenges including weather windows, marine vessel coordination, and environmental monitoring requirements. Shallow water structures in depths under 50 meters account for 68% of offshore decommissioning activity, while deepwater operations in 200–1,500 meter depths represent the fastest-growing segment at 12% annual growth.

Onshore decommissioning holds a 27.2% market share at USD 2.3 Billion in 2025. Land-based operations address well abandonment, facility demolition, and site restoration across producing regions. North America leads onshore decommissioning activity with approximately 150,000 orphaned and abandoned wells requiring plugging across state and federal lands. California alone has identified 35,000 idle wells requiring P&A within regulatory timelines. Onshore decommissioning benefits from easier access and lower mobilization costs compared to offshore operations.

By Water Depth

Shallow water operations in depths under 200 meters represent 58.3% of offshore decommissioning revenue. The Gulf of Mexico shelf contains the highest concentration of shallow water platforms globally, with over 1,400 structures in federal waters. Fixed platform removal using crane barges and lift boats dominates shallow water operations, with established methodologies reducing project timelines to 30–45 days for typical four-leg jackets. North Sea shallow water decommissioning commands premium pricing due to stringent OSPAR environmental requirements.

Deepwater and ultra-deepwater decommissioning in depths exceeding 200 meters accounts for 14.5% of offshore activity. First-generation deepwater developments in the Gulf of Mexico, Brazil, and West Africa are reaching 25–30 year design limits, creating emerging decommissioning requirements. Floating production system decommissioning presents unique challenges including turret disconnection, mooring system recovery, and riser removal. Costs for deepwater facility decommissioning range from USD 100–500 Million depending on system complexity.

Regional Analysis

Europe

Europe leads the oil and gas decommissioning market with a 42.5% share, generating USD 3.6 Billion in 2025. The United Kingdom dominates European activity with USD 2.1 Billion in annual decommissioning expenditure, supported by the North Sea Transition Authority oversight and Cessation of Production regulatory framework. Over 250 UK platforms require decommissioning through 2035, with total liability estimated at USD 52 Billion across the UK Continental Shelf. The Oil and Gas Authority tax relief provisions allow operators to recover 40–75% of decommissioning costs against prior production income.

Norway contributes USD 1.1 Billion to European decommissioning revenue, with Equinor, Aker BP, and ConocoPhillips executing major Cessation of Production programs. Norwegian regulations under the Petroleum Activities Act require complete facility removal unless specific derogations apply. Denmark, the Netherlands, and Germany add incremental demand from mature North Sea and onshore gas field decommissioning. OSPAR Decision 98/3 establishes the regional regulatory framework requiring complete platform removal with limited exceptions for concrete gravity base structures.

North America

North America holds a 28.6% market share at USD 2.4 Billion in 2025. The United States dominates regional activity with USD 2.1 Billion in decommissioning expenditure concentrated in the Gulf of Mexico federal waters. BSEE regulations require removal of idle iron within specified timeframes, with enhanced bonding requirements for financially stressed operators. Over 1,800 platforms operate in federal waters, with approximately 650 structures classified as end-of-life or idle. The Rigs-to-Reefs program provides an alternative disposition pathway, with 12 Gulf states permitting artificial reef conversion.

Onshore decommissioning in the United States addresses a backlog of 150,000 orphaned and abandoned wells across producing states. The Infrastructure Investment and Jobs Act allocated USD 4.7 Billion for orphaned well plugging through 2030, creating substantial federal funding for state programs. California, Texas, Pennsylvania, and Oklahoma hold the largest inventories of wells requiring P&A. Canada contributes USD 0.3 Billion to North American decommissioning, with Alberta's Orphan Well Association managing approximately 8,000 inactive wells requiring abandonment.

Asia Pacific

Asia Pacific accounts for 15.8% of the oil and gas decommissioning market, generating USD 1.3 Billion in 2025. Australia leads regional demand at USD 0.5 Billion, with NOPSEMA regulations requiring comprehensive decommissioning plans for all offshore petroleum titles. The Timor Sea and Northwest Shelf contain aging infrastructure from 1980s and 1990s developments approaching end-of-life status. Woodside and Santos have announced major decommissioning programs commencing 2026 for mature Bass Strait and Carnarvon Basin facilities.

Malaysia contributes USD 0.4 Billion to regional decommissioning activity, with Petronas managing over 400 offshore platforms across the Malay Basin and Sabah/Sarawak waters. Approximately 30% of Malaysian platforms have exceeded 30-year design life, creating near-term decommissioning requirements. Indonesia, Thailand, and Brunei add incremental demand from mature Gulf of Thailand and South China Sea developments. Regional regulatory frameworks remain less prescriptive than North Sea standards, with case-by-case decommissioning approvals typical.

Middle East and Africa

The Middle East and Africa region holds an 8.3% market share, equivalent to USD 0.7 Billion in 2025. The Middle East contribution remains modest despite substantial installed infrastructure, as relatively young fields continue production and regulatory frameworks for mandatory decommissioning remain underdeveloped. UAE and Qatar have initiated regulatory development for eventual decommissioning requirements. African decommissioning activity concentrates in Nigeria and Angola, where first-generation deepwater FPSOs approach 20–25 year operating limits.

West African decommissioning represents an emerging growth segment, with Shell, TotalEnergies, and ExxonMobil evaluating end-of-life strategies for Niger Delta and offshore Angola infrastructure. Egypt contributes incremental demand from aging Gulf of Suez concessions. The absence of mandatory decommissioning timelines in most regional jurisdictions slows market development compared to OSPAR and BSEE regulatory environments.

Latin America

Latin America accounts for 4.8% of the oil and gas decommissioning market at USD 0.4 Billion in 2025. Brazil leads regional activity as first-generation Pre-Salt FPSOs approach design life limits and legacy Campos Basin infrastructure requires removal. Petrobras has identified 25 fixed platforms and 8 FPSOs for decommissioning through 2030. ANP regulations require environmental impact assessment and financial provisions for decommissioning prior to field development approval.

Mexico contributes modest decommissioning demand from mature Cantarell and Ku-Maloob-Zaap field infrastructure. Argentina and Trinidad and Tobago add incremental activity from aging offshore and onshore developments. Regional decommissioning markets remain early-stage compared to mature North Sea and Gulf of Mexico activity, with significant growth potential as installed base ages through the forecast period.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Well Plugging and Abandonment

- Platform Removal

- Pipeline Decommissioning

- Conductor and Casing Removal

- Site Remediation

By Location

- Offshore

- Onshore

By Water Depth

- Shallow Water (Under 200m)

- Deepwater (200m–1500m)

- Ultra-Deepwater (Over 1500m)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.4 B |

| Forecast Revenue (2034) | USD 15.8 B |

| CAGR (2025-2034) | 7.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Well Plugging and Abandonment, Platform Removal, Pipeline Decommissioning, Conductor and Casing Removal, Site Remediation), By Location, Offshore, Onshore), By Water Depth, (Shallow Water (Under 200m), Deepwater (200m–1500m), Ultra-Deepwater (Over 1500m)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TECHNIPFMC, PETROFAC, AKER SOLUTIONS, WOOD PLC, SLB, HELIX ENERGY SOLUTIONS, AF GRUPPEN, ALLSEAS GROUP, HEEREMA MARINE CONTRACTORS, ACTEON GROUP, VEOLIA ENVIRONMENT, REVER OFFSHORE, SAIPEM, MCDERMOTT INTERNATIONAL, WELL-SAFE SOLUTIONS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Location (Offshore, Onshore), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater) Industry Trends, Competitive Landscape, Market Dynamics, Investment Analysis & Forecast 2026–2034")

, By Location (Offshore, Onshore), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater) Industry Trends, Competitive Landscape, Market Dynamics, Investment Analysis & Forecast 2026–2034")

, By Location (Offshore, Onshore), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater) Industry Trends, Competitive Landscape, Market Dynamics, Investment Analysis & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Decommissioning Market?

Global Oil & gas decommissioning market valued at USD 7.83B in 2024, reaching USD 15.8B by 2034, growing at a CAGR of 7.3% from 2026–2034.

Who are the major players in the Oil and Gas Decommissioning Market?

TECHNIPFMC, PETROFAC, AKER SOLUTIONS, WOOD PLC, SLB, HELIX ENERGY SOLUTIONS, AF GRUPPEN, ALLSEAS GROUP, HEEREMA MARINE CONTRACTORS, ACTEON GROUP, VEOLIA ENVIRONMENT, REVER OFFSHORE, SAIPEM, MCDERMOTT INTERNATIONAL, WELL-SAFE SOLUTIONS, Others

Which segments covered the Oil and Gas Decommissioning Market?

By Service Type, (Well Plugging and Abandonment, Platform Removal, Pipeline Decommissioning, Conductor and Casing Removal, Site Remediation), By Location, Offshore, Onshore), By Water Depth, (Shallow Water (Under 200m), Deepwater (200m–1500m), Ultra-Deepwater (Over 1500m))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Decommissioning Market

Published Date : 07 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date