- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Digital Twin Market Size & Forecast 2034 | CAGR 16.3%

Global Oil & Gas Digital Twin Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Application (Production Optimization, Predictive Maintenance, Asset Integrity & Safety, Reservoir Management, Supply Chain & Logistics), By Deployment (Cloud, On-Premise, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2024–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

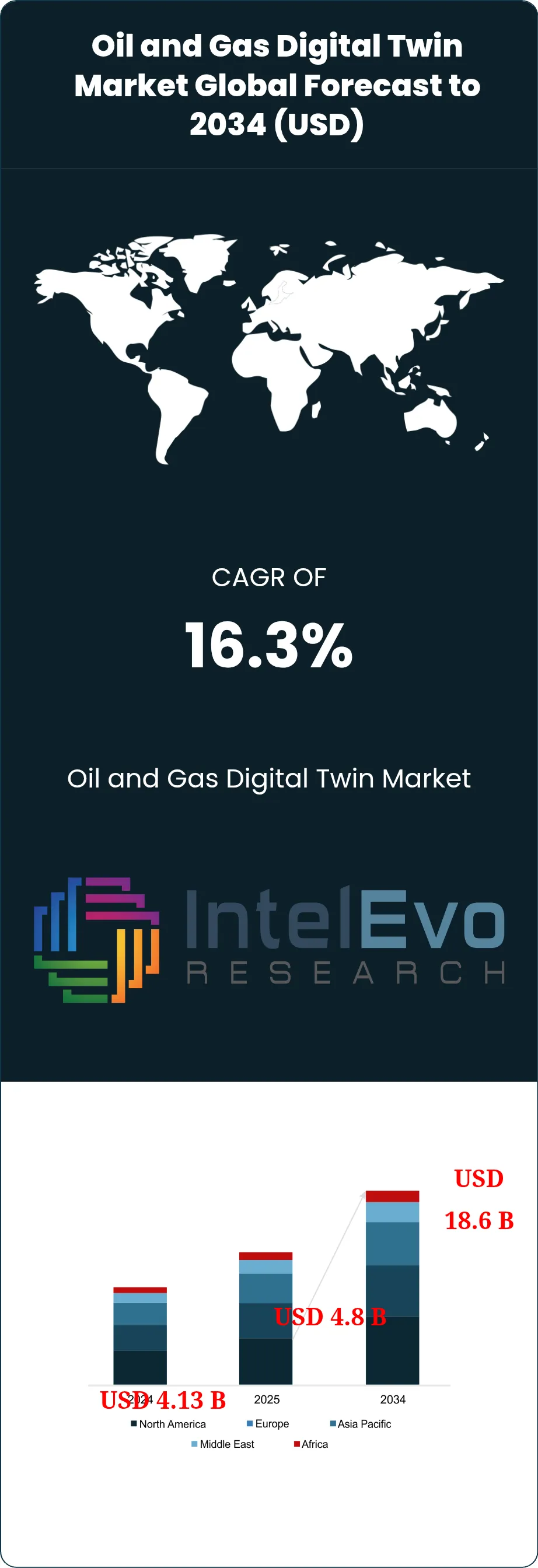

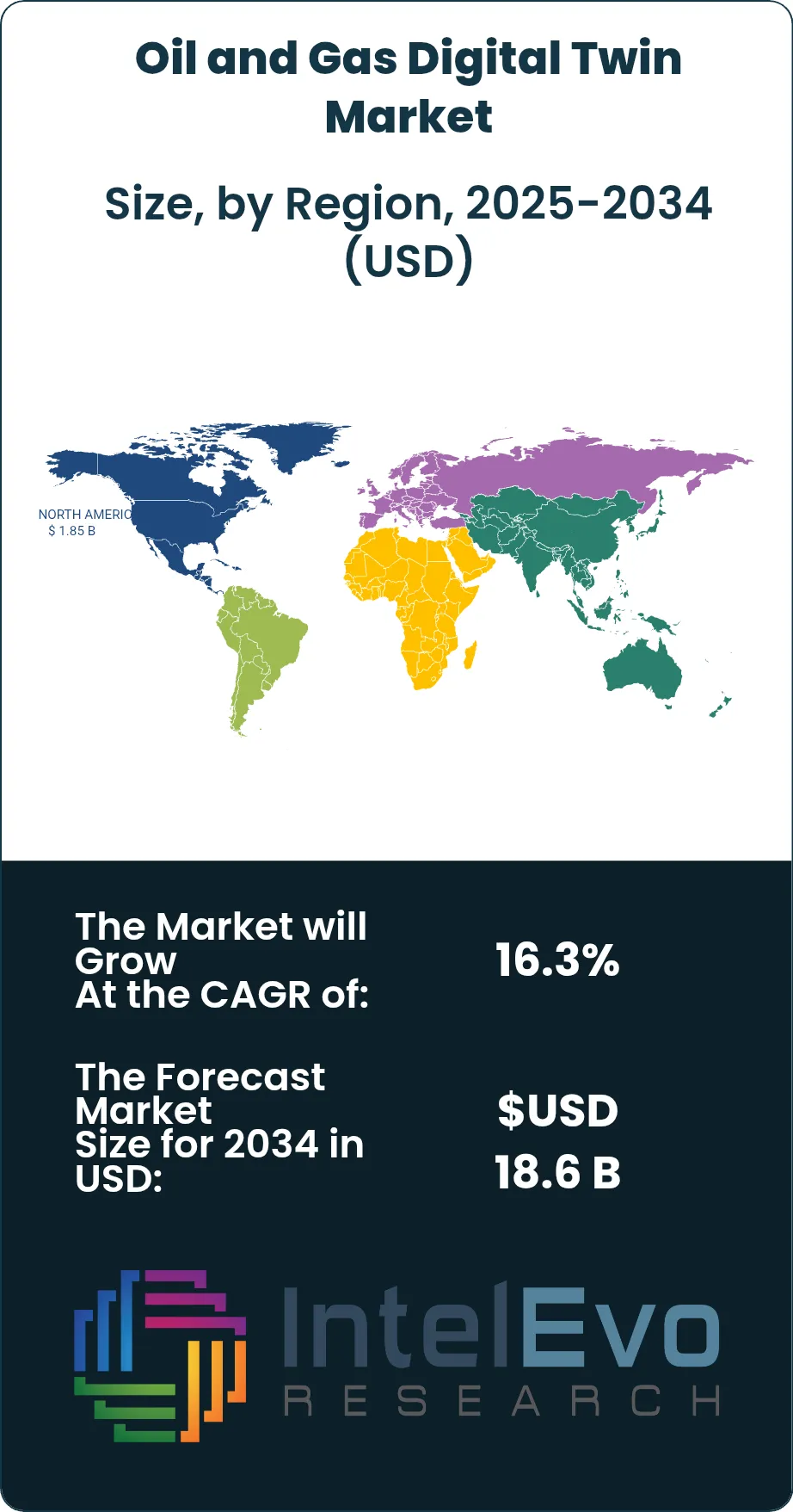

| USD 4.8 Billion | USD 18.6 Billion | 16.3% | North America, 38.5% |

The Oil and Gas Digital Twin Market was valued at approximately USD 4.13 Billion in 2024 and reached USD 4.8 Billion in 2025. The market is projected to grow to USD 18.6 Billion by 2034, expanding at a CAGR of 16.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.8 Billion over the analysis period. Digital twin technology replicates physical oil and gas assets, processes, and systems as virtual models that update in real time through IoT sensor feeds, enabling operators to predict equipment failures, optimize production, and reduce downtime. Rising capital intensity across upstream, midstream, and downstream operations has accelerated adoption as operators seek to lower lifting costs per barrel and improve asset utilization rates.

Get More Information about this report -

Request Free Sample ReportThe oil and gas digital twin market draws momentum from three structural forces. First, regulatory pressure from the EPA, IEA, and national emission mandates requires operators to model and minimize flaring, methane leaks, and carbon intensity per barrel of oil equivalent. Second, the API and BSEE safety standards demand continuous well integrity monitoring, a function that digital twins automate by correlating pressure, temperature, and vibration data streams from subsea and onshore completions. Third, the global rig count recovery to approximately 1,780 active rigs in 2025 has increased demand for real-time drilling optimization, where digital twins reduce non-productive time by 15–20% on average.

North America accounted for 38.5% of global revenue in 2025, driven by intensive adoption in the Permian Basin and Gulf of Mexico deepwater operations. Europe held 24.2% market share, supported by North Sea asset life extension programs and the European Commission’s mandate for refinery energy efficiency. Asia Pacific captured 21.8%, led by digitalization programs at CNOOC, ONGC, and Petronas. Investment in cloud-native digital twin platforms grew 28% year over year in 2025, reflecting the shift from on-premise SCADA-linked twins to AI-augmented, multi-physics simulation environments. The oil and gas digital twin market is expected to see the fastest growth in the Middle East, where national oil companies are committing USD 3.5 Billion to smart oilfield programs through 2030.

, By Application (Production Optimization, Predictive Maintenance, Asset Integrity & Safety, Reservoir Management, Supply Chain & Logistics), By Deployment (Cloud, On-Premise, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2024–2034")

Key Takeaways

- Market Growth: The oil and gas digital twin market was valued at USD 4.8 Billion in 2025 and is projected to reach USD 18.6 Billion by 2034, expanding at a CAGR of 16.3% over the 2025–2034 forecast period.

- Segment Dominance (By Offering): The solutions segment led the market with a 62.4% share in 2025, generating USD 3.0 Billion in revenue as operators prioritized platform deployment over consulting engagements.

- Segment Dominance (By Application): Production optimization held the largest application share at 28.7% in 2025, valued at USD 1.38 Billion, driven by the need to maximize output from mature reservoirs.

- Driver: The expansion of IoT sensor networks across oilfield infrastructure increased connected device density by 34% between 2023 and 2025, creating the data foundation for digital twin deployment.

- Restraint: High implementation costs averaging USD 8–15 Million per integrated upstream digital twin limit adoption among independent E&P operators with annual CAPEX below USD 500 Million.

- Opportunity: Subsea digital twins for deepwater fields represent a USD 2.6 Billion addressable opportunity by 2034, as FPSO operators seek to reduce intervention costs by 25–35%.

- Trend: AI-augmented predictive maintenance modules embedded within digital twin platforms reached 41% penetration among large-cap operators in 2025, up from 18% in 2022.

- Regional Analysis: North America dominated the oil and gas digital twin market with a 38.5% share and USD 1.85 Billion in revenue in 2025, anchored by Permian Basin and Gulf of Mexico deployments.

Competitive Landscape Overview

The oil and gas digital twin market is moderately consolidated, with the top four players; Siemens Energy, GE Vernova, ABB, and Emerson; commanding a combined 47.3% market share in 2025. Competition is technology-driven, centered on AI model accuracy, multi-physics simulation fidelity, and cloud platform scalability. M&A activity intensified through 2025, with six acquisitions exceeding USD 200 Million each as incumbents absorbed niche analytics providers. New entrants from the industrial IoT and reservoir simulation sectors have increased competitive intensity, particularly in the upstream subsurface twin segment.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Siemens Energy | Germany | Leader | Siemens Xcelerator Digital Twin Suite | Europe | Launched AI-integrated digital twin for LNG terminals (Feb 2026) |

| General Electric Vernova | US | Leader | GE Digital APM & Digital Twin Platform | North America | Acquired OspreyData for real-time well monitoring (Jun 2025) |

| ABB Ltd | Switzerland | Leader | ABB Ability Digital Twin | Europe | Expanded partnership with ADNOC for refinery digital twins (Sep 2025) |

| Emerson Electric | US | Leader | Emerson DeltaV Digital Twin | North America | Integrated predictive analytics module into DeltaV (Jan 2026) |

| AVEVA Group | UK | Challenger | AVEVA Unified Operations Center | Europe | Released cloud-native digital twin for offshore platforms (Mar 2025) |

| Honeywell International | US | Challenger | Honeywell Forge Digital Twin | North America | Partnered with Saudi Aramco for upstream twin deployment (Dec 2024) |

| Schlumberger (SLB) | US | Challenger | SLB Delfi Digital Platform | Middle East | Deployed subsurface digital twin across 12 fields in Permian Basin (Aug 2025) |

| Baker Hughes | US | Challenger | Cordant Digital Twin Platform | North America | Launched Cordant 2.0 with real-time reservoir modeling (Apr 2025) |

| Yokogawa Electric | Japan | Niche Player | Yokogawa Digital Twin Platform | Asia Pacific | Signed digital twin contract with INPEX for offshore Australia (Nov 2025) |

| Kongsberg Digital | Norway | Niche Player | Kongsberg K-Sim Digital Twin | Europe | Deployed FPSO digital twin for Equinor (Jul 2025) |

By Offering:

The solutions segment captured 62.4% of the oil and gas digital twin market in 2025, generating USD 3.0 Billion. This category includes platform software licenses, cloud subscriptions, and pre-built twin models for asset classes such as compressors, heat exchangers, distillation columns, and wellheads. Siemens Xcelerator, GE Digital APM, and AVEVA Unified Operations Center dominate the platform tier, each offering physics-based and data-driven hybrid models that integrate with SCADA, DCS, and ERP systems. The shift toward SaaS delivery models increased recurring revenue to 38% of total solution sales in 2025. Platform vendors are embedding large language model interfaces to allow operations engineers to query twin models using natural language, reducing the time required for root cause analysis from hours to minutes.

The services segment held 37.6% share, valued at USD 1.8 Billion in 2025. Services include implementation consulting, systems integration, model calibration, training, and managed twin-as-a-service offerings. Accenture, Capgemini, and Infosys have built dedicated oil and gas digital twin practices, deploying cross-functional teams of reservoir engineers, data scientists, and cloud architects. Average implementation timelines for an integrated refinery digital twin range from 14 to 22 months, creating sustained revenue streams. Managed services grew 31% year over year in 2025 as mid-size operators outsourced twin operations rather than building internal teams.

By Application:

Production optimization accounted for 28.7% of the oil and gas digital twin market in 2025. Digital twins model reservoir flow dynamics, artificial lift performance, and surface facility constraints to maximize barrel-per-day output. Operators using production twins in the Permian Basin reported 8–12% increases in well productivity. The segment is anchored by enhanced oil recovery modeling, gas-lift optimization, and water-cut prediction capabilities.

Predictive maintenance held 24.3% share. Digital twins track vibration signatures, thermal profiles, and corrosion rates on rotating equipment, pipelines, and subsea manifolds. Average unplanned downtime reduction among adopters reached 22% in 2025. The asset integrity and safety segment captured 18.6% share, driven by BSEE and API compliance requirements for well integrity, pressure vessel monitoring, and leak detection on offshore platforms. Reservoir management represented 16.2%, where subsurface digital twins integrate seismic, well log, and production data to guide infill drilling and waterflood optimization. Supply chain and logistics held 12.2%, as pipeline operators use flow simulation twins to optimize throughput scheduling and batch planning.

By Deployment:

Cloud deployment captured 53.8% of the oil and gas digital twin market in 2025, reflecting the shift toward scalable computing for multi-physics simulation workloads. AWS, Microsoft Azure, and Google Cloud each launched oil and gas digital twin accelerators between 2024 and 2025, providing pre-configured environments with GPU-optimized compute for reservoir and process simulation. Cloud twins reduce total cost of ownership by 30–40% compared with on-premise installations for operators managing more than 500 connected assets. On-premise deployment held 28.5% share, preferred by national oil companies and large supermajors with classified subsurface data and sovereign data residency requirements. Saudi Aramco, ADNOC, and CNOOC maintain on-premise twin infrastructure within secure data centers. Hybrid deployment accounted for 17.7%, serving operators that run latency-sensitive edge twins on platforms and rigs while synchronizing data to cloud environments for enterprise-level analytics.

By Operation:

Upstream operations dominated with 44.1% of market revenue in 2025, valued at USD 2.12 Billion. Drilling optimization, well completions monitoring, reservoir simulation, and surface facility management drive the upstream twin market. Midstream operations held 26.3%, where digital twins model pipeline flow assurance, compressor station performance, and LNG terminal operations. The midstream segment benefits from PHMSA pipeline safety mandates that encourage continuous monitoring. Downstream operations captured 29.6%, driven by refinery process optimization, crude distillation unit modeling, and turnaround planning. Digital twins in downstream reduce turnaround duration by 10–15%, saving refiners USD 5–10 Million per event.

Regional Analysis

North America Oil and Gas Digital Twin Market:

North America commanded a 38.5% share of the global oil and gas digital twin market in 2025, generating USD 1.85 Billion in revenue. The United States contributed 82% of regional revenue, driven by intensive digital twin deployment across the Permian Basin, Eagle Ford, and Gulf of Mexico deepwater assets. ExxonMobil, Chevron, and ConocoPhillips each disclosed digital twin budgets exceeding USD 200 Million annually. The Permian Basin alone hosts over 4,500 digitally connected wells, with twin-enabled production optimization contributing to an average 9% uplift in barrel-per-day output. Canada’s oil sands operators, including Suncor and Canadian Natural Resources, adopted process digital twins to optimize SAGD steam-to-oil ratios. Mexico’s Pemex initiated digital twin pilots at Dos Bocas refinery in 2025. EPA methane emission regulations under NSPS OOOOb/c accelerated leak detection twin adoption across midstream operators.

Europe Oil and Gas Digital Twin Market:

Europe held 24.2% of the oil and gas digital twin market in 2025, valued at USD 1.16 Billion. The United Kingdom and Norway led the region, together accounting for 61% of European spending. North Sea operators including Equinor, BP, and Shell deployed asset life extension twins to manage aging platforms originally installed in the 1980s and 1990s. The UK’s North Sea Transition Authority mandated emissions monitoring plans that incentivize digital twin-based flaring reduction. Germany’s downstream sector adopted refinery digital twins for energy efficiency, with BASF and Covestro piloting process twins at Ludwigshafen and Leverkusen complexes. France’s TotalEnergies expanded its digital twin program to 15 operated assets globally from its Paris technology center. The European Commission’s Fit for 55 regulatory package is projected to increase refinery twin adoption by 22% through 2028.

Asia Pacific Oil and Gas Digital Twin Market:

Asia Pacific captured 21.8% of market share in 2025, generating USD 1.05 Billion. China led the region with 42% of Asia Pacific revenue as CNOOC, PetroChina, and Sinopec deployed digital twins across offshore production platforms in the South China Sea and onshore fields in the Tarim Basin. Japan’s INPEX committed USD 180 Million to digital twin deployment for its Ichthys LNG facility in Australia. India’s ONGC and Reliance Industries initiated upstream twin pilots in the Krishna-Godavari Basin. South Korea’s HD Hyundai and Samsung Heavy Industries integrated digital twins into FPSO construction and commissioning workflows. Australia’s Woodside Energy operates one of the most advanced digital twin deployments globally, covering its Pluto LNG and Scarborough gas assets with full-facility twins.

Latin America Oil and Gas Digital Twin Market:

Latin America accounted for 8.8% of the global oil and gas digital twin market in 2025, valued at USD 0.42 Billion. Brazil dominated the region with 64% of Latin American revenue, driven by Petrobras’s digital twin program for pre-salt FPSO operations in the Santos and Campos basins. Petrobras deployed digital twins across 12 FPSO units, reducing unplanned shutdowns by 18% in 2025. Mexico contributed through Pemex’s refinery modernization program. Argentina’s Vaca Muerta shale operators, including YPF and Vista Energy, began digital twin deployments for hydraulic fracture optimization. Colombia’s Ecopetrol piloted predictive maintenance twins at the Barrancabermeja refinery complex.

Middle East and Africa Oil and Gas Digital Twin Market:

The Middle East and Africa held 6.7% of market share in 2025, generating USD 0.32 Billion, but represented the fastest-growing region with a projected CAGR of 19.8% through 2034. Saudi Aramco committed USD 1.5 Billion to its smart oilfield digital twin initiative covering the Ghawar, Shaybah, and Khurais mega-fields. ADNOC’s Panorama digital command center integrates digital twins across upstream, midstream, and downstream operations. Qatar Energy deployed digital twins for the North Field East LNG expansion, the largest LNG project globally. The UAE’s AI and digital economy strategy positions Abu Dhabi as a hub for oil and gas technology development. South Africa’s Sasol piloted process twins at its Secunda coal-to-liquids complex, and Nigeria’s Dangote Refinery, the largest single-train refinery in Africa, initiated digital twin implementation for commissioning optimization.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions

- Services

By Application

- Production Optimization

- Predictive Maintenance

- Asset Integrity and Safety

- Reservoir Management

- Supply Chain and Logistics

By Deployment

- Cloud

- On-Premise

- Hybrid

By Operation

- Upstream

- Midstream

- Downstream

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.8 B |

| Forecast Revenue (2034) | USD 18.6 B |

| CAGR (2025-2034) | 16.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Solutions, Services), By Application (Production Optimization, Predictive Maintenance, Asset Integrity and Safety, Reservoir Management, Supply Chain and Logistics), By Deployment , (Cloud, On-Premise, Hybrid), By Operation , Upstream, Midstream, Downstream) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SIEMENS ENERGY, GENERAL ELECTRIC VERNOVA, ABB LTD, EMERSON ELECTRIC, AVEVA GROUP (SCHNEIDER ELECTRIC), HONEYWELL INTERNATIONAL, SCHLUMBERGER (SLB), BAKER HUGHES, YOKOGAWA ELECTRIC, KONGSBERG DIGITAL, ASPEN TECHNOLOGY, DASSAULT SYSTEMES, ANSYS INC., BENTLEY SYSTEMS, C3.AI, HALLIBURTON, ROCKWELL AUTOMATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Production Optimization, Predictive Maintenance, Asset Integrity & Safety, Reservoir Management, Supply Chain & Logistics), By Deployment (Cloud, On-Premise, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2024–2034")

, By Application (Production Optimization, Predictive Maintenance, Asset Integrity & Safety, Reservoir Management, Supply Chain & Logistics), By Deployment (Cloud, On-Premise, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2024–2034")

, By Application (Production Optimization, Predictive Maintenance, Asset Integrity & Safety, Reservoir Management, Supply Chain & Logistics), By Deployment (Cloud, On-Premise, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2024–2034")

Frequently Asked Questions

How big is the Oil and Gas Digital Twin Market?

Global Oil & gas digital twin market valued at USD 4.13B in 2024, reaching USD 18.6B by 2034, growing at a CAGR of 16.3% from 2026–2034.

Who are the major players in the Oil and Gas Digital Twin Market?

SIEMENS ENERGY, GENERAL ELECTRIC VERNOVA, ABB LTD, EMERSON ELECTRIC, AVEVA GROUP (SCHNEIDER ELECTRIC), HONEYWELL INTERNATIONAL, SCHLUMBERGER (SLB), BAKER HUGHES, YOKOGAWA ELECTRIC, KONGSBERG DIGITAL, ASPEN TECHNOLOGY, DASSAULT SYSTEMES, ANSYS INC., BENTLEY SYSTEMS, C3.AI, HALLIBURTON, ROCKWELL AUTOMATION, Others

Which segments covered the Oil and Gas Digital Twin Market?

By Offering (Solutions, Services), By Application (Production Optimization, Predictive Maintenance, Asset Integrity and Safety, Reservoir Management, Supply Chain and Logistics), By Deployment , (Cloud, On-Premise, Hybrid), By Operation , Upstream, Midstream, Downstream)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Digital Twin Market

Published Date : 31 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date