- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas ERP Software Market Forecast 2034 | CAGR 7.2%

Global Oil and Gas ERP Software Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, On-Premise), By Operation (Upstream, Midstream, Downstream), By Function (Financial Management & Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production & Operations), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 3.28 Billion | USD 6.15 Billion | 7.2% | North America, 42.1% |

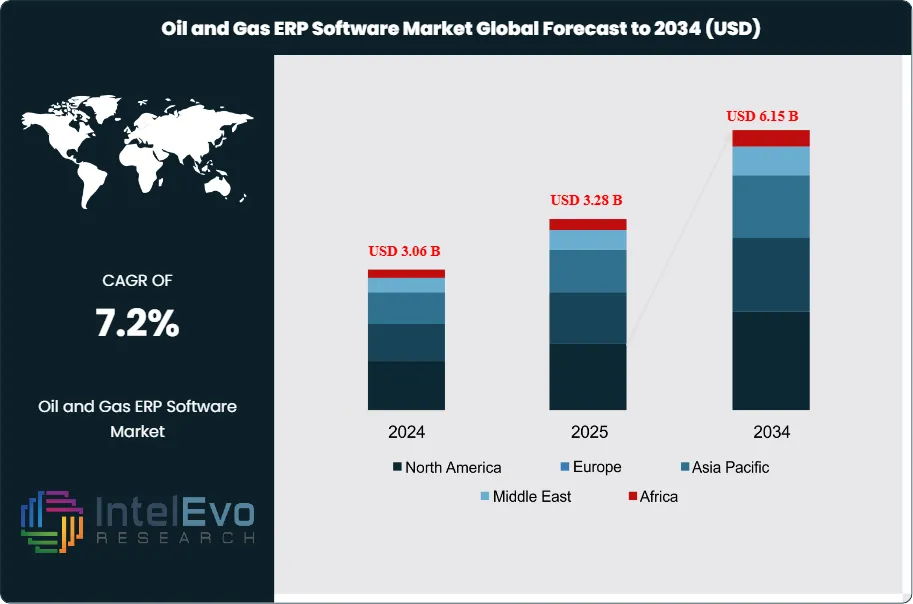

The Oil and Gas ERP Software Market was valued at approximately USD 3.06 Billion in 2024 and reached USD 3.28 Billion in 2025. The market is projected to grow to USD 6.15 Billion by 2034, expanding at a CAGR of 7.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 2.87 billion over the analysis period. The oil and gas ERP software market encompasses enterprise resource planning solutions designed specifically for upstream, midstream, and downstream operations, integrating financial management, supply chain, human capital, asset management, and production accounting functions into unified platforms.

Get More Information about this report -

Request Free Sample ReportDemand for specialized ERP solutions in the energy sector accelerates as operators seek to consolidate fragmented legacy systems that impede operational efficiency. The average integrated oil company maintains 15-25 discrete software applications for production accounting, joint venture billing, land management, and regulatory reporting. This complexity drives total cost of ownership upward and creates data silos that prevent real-time decision-making. Oil and gas ERP software addresses these challenges through industry-specific functionality that generic enterprise systems cannot match. SAP S/4HANA for Oil and Gas, Oracle Cloud for Energy, and Microsoft Dynamics 365 for Energy incorporate production revenue accounting, division order processing, and regulatory compliance modules purpose-built for energy sector requirements.

Cloud deployment models are transforming the oil and gas ERP software market. Cloud-based solutions now represent 52.4% of new deployments in 2025, up from 28% in 2020. The shift reflects operator preferences for reduced capital expenditure, faster implementation timelines, and automatic updates that maintain regulatory compliance. Quorum Software, P2 Energy Solutions, and other specialized vendors have transitioned their portfolios to cloud-native architectures that support remote operations and mobile workforce access. On-premise deployments retain importance among national oil companies and operators with strict data sovereignty requirements.

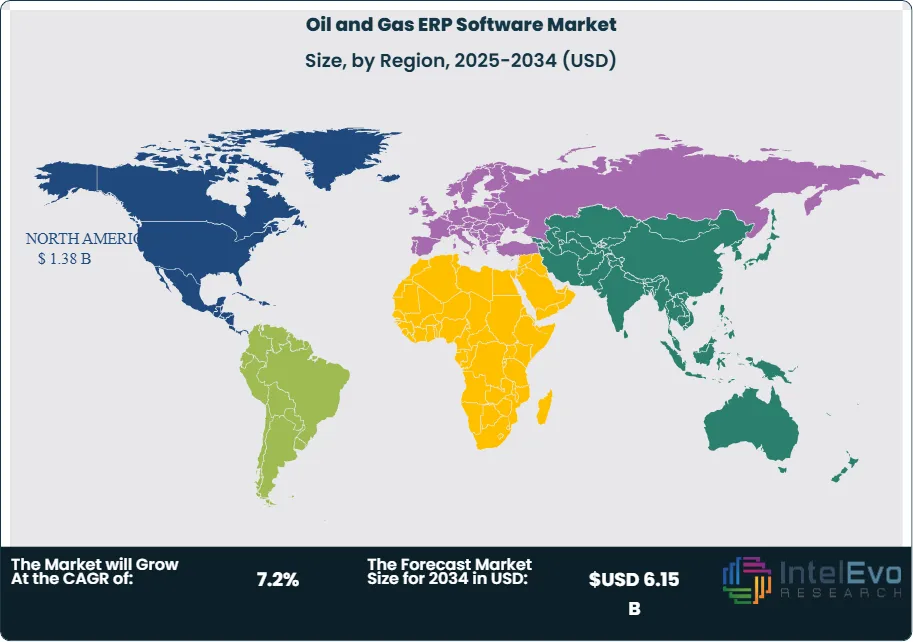

North America dominates the oil and gas ERP software market with 42.1% share in 2025, generating USD 1.38 billion in revenue. The concentration of independent producers in the Permian Basin, Eagle Ford, and Bakken formations drives demand for production accounting and land management solutions. Europe follows at 24.8% share, with North Sea operators and integrated refiners investing in digital transformation programs. The Middle East and Africa accounts for 18.6% share as national oil companies modernize enterprise systems under Vision 2030 and similar initiatives. Asia Pacific represents 10.2% with growth driven by refinery investments in India and China. Integration with operational technology systems including SCADA, DCS, and production optimization platforms represents a growing requirement as operators pursue unified digital operations strategies.

, By Operation (Upstream, Midstream, Downstream), By Function (Financial Management & Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production & Operations), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas ERP software market is projected to expand from USD 3.28 billion in 2025 to USD 6.15 billion by 2034, achieving a CAGR of 7.2% during the 2025-2034 forecast period.

- Segment Dominance (By Deployment): Cloud-based ERP solutions lead with 52.4% market share in 2025, valued at USD 1.72 billion, driven by reduced implementation costs and faster time-to-value compared to on-premise alternatives.

- Segment Dominance (By Operation): Upstream operations account for 46.8% of market revenue in 2025, generating USD 1.54 billion, as exploration and production companies invest in production accounting, joint venture billing, and land management modules.

- Driver: Digital transformation initiatives have accelerated ERP modernization, with 68% of oil and gas companies prioritizing enterprise system upgrades in 2025 capital budgets.

- Restraint: Implementation complexity and change management challenges delay deployments, with average project timelines extending 40% beyond initial estimates for large-scale ERP transformations.

- Opportunity: AI and machine learning integration within ERP platforms presents a USD 890 million incremental opportunity by 2034, enabling predictive analytics for supply chain and financial planning.

- Trend: Industry cloud adoption has reached 52.4% of new deployments in 2025, up from 28% in 2020, reflecting operator preferences for SaaS models with lower total cost of ownership.

- Regional Analysis: North America maintains market leadership with 42.1% share and USD 1.38 billion revenue in 2025, driven by independent operator concentration in major shale basins and continued M&A activity requiring system integration.

Competitive Landscape Overview

The oil and gas ERP software market exhibits moderate consolidation, with the top four vendors capturing approximately 58% of global revenue in 2025. Competition centers on industry-specific functionality, cloud platform capabilities, and integration with operational technology systems. SAP and Oracle maintain leadership positions through extensive partner networks and installed bases at major integrated oil companies. Microsoft has gained share through Dynamics 365 adoption among mid-market operators. Quorum Software dominates the North American upstream segment following strategic acquisitions that consolidated multiple point solutions. Recent M&A activity has intensified as large enterprise vendors acquire specialized oil and gas software companies to strengthen vertical capabilities.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SAP | Germany | Leader | SAP S/4HANA for Oil & Gas | Global | Launched RISE with SAP for Energy (Mar 2025) |

| Oracle | US | Leader | Oracle Cloud for Energy | North America | Acquired Hydric Industries for USD 420M (Jan 2025) |

| Microsoft | US | Leader | Dynamics 365 for Energy | Global | Expanded Copilot for Oil & Gas (Feb 2026) |

| Quorum Software | US | Leader | myQuorum Platform | North America | Merged with Aucerna operations (Dec 2024) |

| P2 Energy Solutions | US | Challenger | P2 BOLO Platform | North America | Released cloud-native upstream suite (Jun 2025) |

| Infor | US | Challenger | Infor CloudSuite O&G | North America | Partnered with AVEVA for integration (Apr 2025) |

| ABB | Switzerland | Challenger | ABB Ability Energy Suite | Europe | Launched AI-powered optimization (Sep 2025) |

| Emerson | US | Challenger | Paradigm Geolog Suite | North America | Integrated with Aspen HYSYS (Aug 2025) |

| IFS | Sweden | Niche Player | IFS Cloud for Energy | Europe | Acquired Poka for USD 95M (Nov 2024) |

| AVEVA | UK | Niche Player | AVEVA Unified Operations | Europe | Enhanced digital twin capabilities (May 2025) |

By Deployment Mode

The oil and gas ERP software market segments by deployment into cloud-based and on-premise solutions. Cloud-based ERP commands 52.4% market share in 2025, generating USD 1.72 billion in revenue. This segment has grown rapidly as vendors transition portfolios to SaaS delivery models that reduce upfront capital requirements and accelerate implementation timelines. Average cloud ERP implementations complete in 8-14 months compared to 18-30 months for on-premise projects. Subscription pricing models align costs with production levels, benefiting operators during commodity price volatility. SAP RISE for Energy, Oracle Cloud for Energy, and Quorum myQuorum represent leading cloud platforms purpose-built for oil and gas operations. On-premise ERP retains 47.6% share at USD 1.56 billion in 2025. National oil companies including Saudi Aramco, ADNOC, and Petrobras maintain on-premise installations due to data sovereignty requirements and existing infrastructure investments. Large integrated oil companies with substantial IT organizations often prefer on-premise control for mission-critical financial systems.

By Operation

Upstream operations represent the largest operational segment with 46.8% share in 2025, valued at USD 1.54 billion. Exploration and production companies require specialized functionality for production revenue accounting, joint venture billing, division order processing, and land management. The complexity of royalty calculations, working interest allocations, and regulatory reporting creates demand for purpose-built upstream ERP modules. Quorum Software and P2 Energy Solutions dominate this segment with solutions designed specifically for North American independent producers. Major integrated companies typically deploy SAP IS-Oil or Oracle Financials with industry add-ons.

Midstream operations hold 24.6% share at USD 807 million in 2025. Pipeline operators, gas processors, and storage terminal owners require ERP functionality for custody transfer accounting, transportation tariff management, and capacity scheduling. Integration with SCADA and measurement systems enables real-time revenue recognition and allocation. Enterprise Companies, Williams, and Kinder Morgan represent major midstream ERP customers investing in system modernization. Downstream operations capture 28.6% share, generating USD 938 million. Refiners and petrochemical companies deploy ERP for supply chain management, crude procurement, product sales, and margin optimization. Integration with advanced process control systems and blend optimization software represents a growing requirement.

By Function

Financial management and accounting functions lead with 32.4% market share in 2025, generating USD 1.06 billion. This includes general ledger, accounts payable, accounts receivable, fixed assets, and consolidation capabilities. Production revenue accounting and joint venture billing represent specialized financial functions critical for upstream operators. Supply chain management holds 24.8% share at USD 813 million, encompassing procurement, inventory management, logistics, and supplier relationship management. Oil and gas supply chains involve complex trading operations, crude and product movements, and just-in-time inventory strategies that require industry-specific ERP functionality. Asset management captures 18.6% share, valued at USD 610 million, supporting maintenance planning, work order management, and equipment lifecycle tracking for refineries, platforms, and processing facilities. Human capital management accounts for 14.2% share at USD 466 million, providing workforce planning, payroll, and training management for distributed operations. Production and operations modules comprise 10.0% share, generating USD 328 million for production reporting, well data management, and operational analytics integration.

By Enterprise Size

Large enterprises dominate oil and gas ERP adoption with 68.4% market share in 2025, generating USD 2.24 billion in revenue. Supermajors, national oil companies, and large independents maintain complex enterprise architectures requiring extensive customization and integration. ExxonMobil, Shell, Chevron, and BP each operate multi-million dollar ERP environments spanning upstream, downstream, and corporate functions. Implementation projects at this scale typically exceed USD 100 million over multi-year timelines. Small and medium enterprises hold 31.6% share at USD 1.04 billion. Independent producers, regional refiners, and oilfield service companies increasingly adopt cloud ERP solutions that provide enterprise functionality without substantial IT infrastructure investment. Quorum Software and P2 Energy Solutions have built strong positions serving mid-market operators with pre-configured solutions that accelerate deployment.

Regional Analysis

North America

North America commands 42.1% of the global oil and gas ERP software market in 2025, generating USD 1.38 billion in revenue. The United States accounts for 86% of regional revenue, driven by the large population of independent producers operating in shale basins requiring specialized production accounting and land management solutions. Over 6,000 active operators in the Permian Basin, Eagle Ford, Bakken, and Marcellus formations create substantial addressable demand for upstream ERP platforms. Quorum Software and P2 Energy Solutions have built dominant positions serving this segment. Major integrated companies including ExxonMobil and Chevron maintain substantial SAP and Oracle installations across global operations headquartered in Houston and San Ramon. Canada contributes 11% of North American revenue with oil sands operators and natural gas producers investing in ERP modernization. Suncor, CNRL, and Cenovus represent major Canadian accounts. Mexico accounts for 3% following energy reform initiatives that attracted international operators requiring standardized enterprise systems.

Europe

Europe holds 24.8% market share in 2025, valued at USD 813 million. The United Kingdom leads with 32% of regional revenue as North Sea operators including Shell UK, BP, and Harbour Energy invest in digital transformation programs. SAP maintains strong positions among integrated operators with European headquarters. Norway contributes 28% with Equinor, Aker BP, and Vaar Energi modernizing enterprise systems to support continental shelf operations. Germany accounts for 16% driven by refinery and petrochemical operations at BASF, Covestro, and integrated energy companies. The Netherlands and France together contribute 18% as TotalEnergies, Shell headquarters, and regional refiners upgrade aging ERP installations. EU regulatory requirements for emissions reporting and sustainability disclosure are driving ERP enhancement projects that integrate environmental data with financial reporting.

Middle East and Africa

The Middle East and Africa region represents 18.6% of the global market in 2025, generating USD 610 million in revenue. Saudi Arabia dominates with 42% of regional revenue as Saudi Aramco executes one of the world's largest SAP S/4HANA implementations as part of its digital transformation strategy. The company's ERP environment supports over 65,000 users across upstream, downstream, and corporate functions. The UAE contributes 26% with ADNOC's enterprise modernization program including SAP S/4HANA deployment and integration with operational technology platforms. Qatar accounts for 12% driven by QatarEnergy LNG expansion projects requiring integrated financial and supply chain systems. African markets including Nigeria, Angola, and Egypt comprise 15% of regional revenue, with international operators standardizing on global ERP templates across African subsidiaries. The remaining GCC markets including Kuwait, Oman, and Bahrain contribute 5% with growing ERP investments as production operations expand.

Asia Pacific

Asia Pacific captures 10.2% of the global oil and gas ERP software market in 2025, valued at USD 335 million, while achieving strong regional growth at 9.4% CAGR through 2034. China leads with 38% of regional revenue as CNPC, Sinopec, and CNOOC modernize enterprise systems to support refining expansion and petrochemical integration. Indian refiners including Indian Oil Corporation, Reliance Industries, and Bharat Petroleum account for 28% of regional revenue, investing in SAP and Oracle implementations to support refinery optimization and retail network management. Australia contributes 18% as LNG operators including Woodside, Santos, and Chevron Australia deploy enterprise systems for integrated upstream and export operations. Japan accounts for 10% with refiners consolidating operations and upgrading aging ERP platforms. Southeast Asian markets including Indonesia, Malaysia, and Thailand comprise 6% with national oil companies investing in digital transformation.

Latin America

Latin America accounts for 4.3% of the global market in 2025, valued at USD 141 million. Brazil dominates with 62% of regional revenue as Petrobras maintains one of the world's largest SAP installations supporting integrated upstream, downstream, and distribution operations. Pre-salt development partners including Shell, TotalEnergies, and Equinor deploy regional instances of global ERP templates. Argentina contributes 18% with YPF and international operators investing in enterprise systems for Vaca Muerta shale development. Mexico accounts for 14% as Pemex modernization programs include ERP upgrades despite budget constraints. Colombia and other Andean markets comprise 6% with Ecopetrol and regional operators adopting cloud ERP solutions that reduce implementation complexity compared to on-premise alternatives.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Mode

- Cloud-Based

- On-Premise

By Operation

- Upstream

- Midstream

- Downstream

By Function

- Financial Management and Accounting

- Supply Chain Management

- Asset Management

- Human Capital Management

- Production and Operations

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.28 B |

| Forecast Revenue (2034) | USD 6.15 B |

| CAGR (2025-2034) | 7.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode, (Cloud-Based, On-Premise), By Operation, (Upstream, Midstream, Downstream), By Function, (Financial Management and Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production and Operations), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAP, ORACLE, MICROSOFT, QUORUM SOFTWARE, P2 ENERGY SOLUTIONS, INFOR, ABB, EMERSON, IFS, AVEVA, ASPEN TECHNOLOGY, EPICOR, ENERTIA SOFTWARE, OGSYS, PETROWARE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Operation (Upstream, Midstream, Downstream), By Function (Financial Management & Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production & Operations), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Function (Financial Management & Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production & Operations), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Function (Financial Management & Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production & Operations), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas ERP Software Market?

Global Oil & gas ERP software market valued at USD 3.06B in 2024, reaching USD 6.15B by 2034, growing at a CAGR of 7.2% from 2026–2034.

Who are the major players in the Oil and Gas ERP Software Market?

SAP, ORACLE, MICROSOFT, QUORUM SOFTWARE, P2 ENERGY SOLUTIONS, INFOR, ABB, EMERSON, IFS, AVEVA, ASPEN TECHNOLOGY, EPICOR, ENERTIA SOFTWARE, OGSYS, PETROWARE, Others

Which segments covered the Oil and Gas ERP Software Market?

By Deployment Mode, (Cloud-Based, On-Premise), By Operation, (Upstream, Midstream, Downstream), By Function, (Financial Management and Accounting, Supply Chain Management, Asset Management, Human Capital Management, Production and Operations), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas ERP Software Market

Published Date : 03 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date