- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Inspection Services Market Forecast 2034 | CAGR 6.8%

Global Oil & Gas Inspection Services Market Size, Share, Growth & Industry Analysis By Service Type (Non-Destructive Testing (NDT), Asset Integrity Management (AIM), QA/QC & Destructive Testing, Visual Inspection & Drone Surveys, Pipeline Integrity Services), By Sector (Upstream, Midstream, Downstream), By Application (Onshore, Offshore Subsea & Surface) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 18.50 Billion | USD 33.35 Billion | 6.8% | North America, 32.4% |

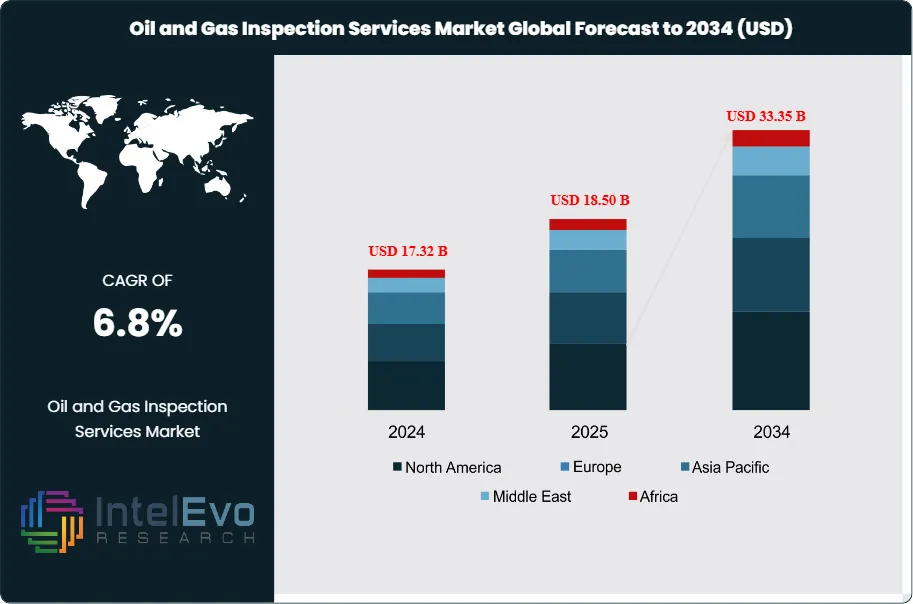

The Oil and Gas Inspection Services Market was valued at approximately USD 17.32 Billion in 2024 and reached USD 18.50 Billion in 2025. The market is projected to grow to USD 33.35 Billion by 2034, expanding at a CAGR of 6.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 14.85 Billion over the analysis period. The requirement for stringent asset integrity and safety protocols across the energy value chain has anchored the necessity for specialized inspection services. Current industry analysis indicates that aging infrastructure in mature basins, particularly in the North Sea and the Permian Basin, is a primary driver for recurring inspection demand. As operators focus on life extension projects for legacy assets, the reliance on advanced non-destructive testing and structural health monitoring has intensified.

Get More Information about this report -

Request Free Sample ReportThe supply side of the oil and gas inspection services market is undergoing a rapid transition toward digital integration and remote operations. Field technicians now utilize autonomous drones and robotic crawlers to inspect hazardous or inaccessible areas, such as flare stacks and subsea pipelines, reducing human exposure to risk. Demand and supply forces are currently balanced by the high volume of turnaround maintenance in the downstream sector and the resurgence of offshore exploration in the Atlantic Margin. Regulatory influences, specifically from the Bureau of Safety and Environmental Enforcement (BSEE) and the American Petroleum Institute (API), have mandated more rigorous inspection cycles for blowout preventers and subsea manifolds, ensuring a stable baseline of activity.

Technological effects are fundamentally altering the competitive environment, with artificial intelligence and machine learning now used to analyze radiographic and ultrasonic data in real time. The introduction of digital twin technology allows operators to visualize structural degradation and predict failure points before they occur. Digitalization has enabled a shift from reactive to predictive maintenance strategies, which significantly lowers operational costs for supermajors and national oil companies. Regional highlights show that emerging investment hotspots are concentrated in the Asia Pacific petrochemical corridor and the Brazilian pre-salt fields, where extreme pressures and corrosive environments demand high-tier inspection expertise.

Risk factors for the oil and gas inspection services market include the inherent volatility of commodity prices, which often dictates the timing of large-scale maintenance shutdowns. However, the mission-critical nature of safety inspections often shields this sector from immediate budget cuts during minor price corrections. The integration of carbon capture and storage (CCS) infrastructure is a rising trend, creating new demand for specialized CO2 pipeline and storage tank inspection. Based on supply-chain and demand-side evaluation, the industry is moving toward a highly technical service model where data analytics and software integration are as valuable as physical testing.

, Asset Integrity Management (AIM), QA/QC & Destructive Testing, Visual Inspection & Drone Surveys, Pipeline Integrity Services), By Sector (Upstream, Midstream, Downstream), By Application (Onshore, Offshore Subsea & Surface) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The industry was valued at USD 18.50 Billion in 2025 and is projected to reach USD 33.35 Billion by 2034, maintaining a steady CAGR of 6.8%.

- Segment Dominance: The Non-Destructive Testing (NDT) segment holds the leading share of 45.2% in 2025 due to its ability to inspect assets without causing damage or operational downtime.

- Segment Dominance: The Midstream sector accounts for the largest application share of 38.6% in 2025, driven by extensive pipeline integrity requirements and safety regulations.

- Driver: Stricter regulatory mandates regarding pipeline safety and methane leak detection are expected to contribute a USD 2.4 Billion increase in annual service demand by 2034.

- Restraint: The shortage of Level III certified NDT technicians is limiting the operational capacity of service providers, potentially raising project costs by 12.0% annually.

- Opportunity: The adoption of drone-based aerial inspections presents a USD 4.8 Billion addressable market for service providers offering high-resolution thermal and visual data.

- Trend: The shift toward AI-driven predictive maintenance is growing at an annual rate of 15.4%, replacing traditional interval-based inspection schedules in offshore assets.

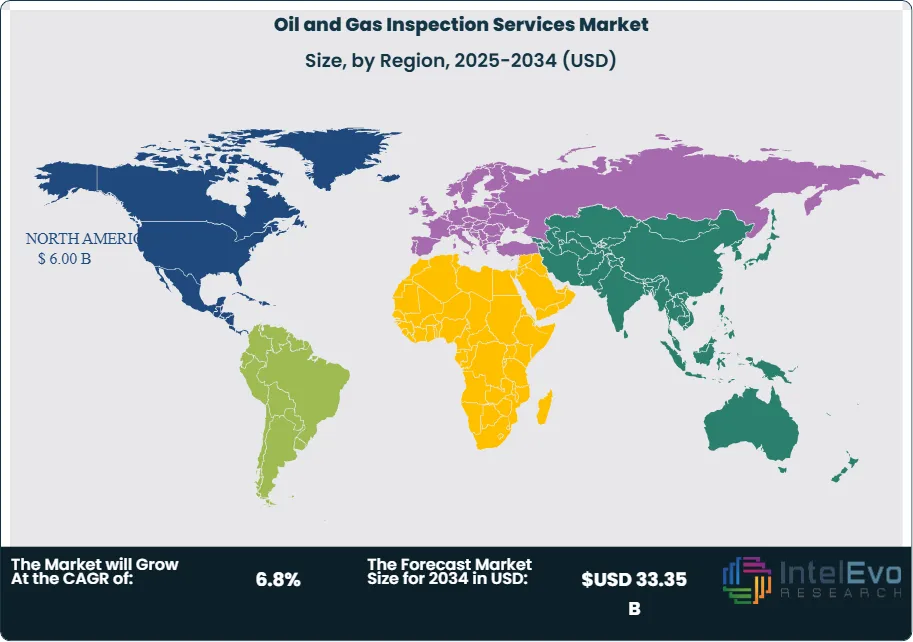

- Regional Analysis: North America is the leading region with a 32.4% market share, valued at USD 6.00 Billion in 2025, supported by massive shale infrastructure.

Competitive Landscape Overview

The oil and gas inspection services market is moderately consolidated, with the top four players commanding a combined market share of approximately 38.5% in 2025. Competition is primarily technology-driven, as companies differentiate themselves through proprietary data analytics platforms and specialized subsea robotics. Competitive intensity has shifted toward strategic acquisitions of digital firms to enhance remote inspection capabilities. Industry analysis shows that integrated service providers who can offer both physical inspection and digital integrity management are securing longer-term master service agreements with supermajors.

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| SGS SA | Switzerland | Leader | Asset Integrity Management | Global | Launched AI-powered corrosion monitoring, 2025 |

| INTERTEK GROUP | United Kingdom | Leader | Technical Inspection Services | Europe / North America | Acquired regional NDT specialist in SE Asia, 2025 |

| BUREAU VERITAS | France | Leader | Veristar Integrity | Global | Expanded offshore services in Brazil Pre-salt, 2025 |

| APPLUS+ | Spain | Leader | RTD Rayscan | Europe / MEA | Partnership for drone-based flare inspection, 2025 |

| MISTRAS GROUP | United States | Challenger | PCMS Software | North America | Integrated digital twin platform for refineries, 2024 |

| TEAM INC | United States | Challenger | Quest Integrity | Global | Strategic restructuring of inspection assets, 2025 |

| OCEANEERING | United States | Niche Player | Subsea NDT Robotics | North Sea / Gulf of Mexico | Released new autonomous subsea crawler, 2026 |

| BAKER HUGHES | United States | Leader | Waygate Technologies | North America / MEA | Expanded radiographic inspection centers, 2025 |

| DNV | Norway | Challenger | Synergi Plant | Europe | Digital certification for hydrogen pipelines, 2025 |

| TUV SUD | Germany | Niche Player | Pipeline Integrity | Europe / Asia | Commissioned new NDT testing lab in China, 2025 |

Segmentation Analysis

The Global Oil and Gas Inspection Services Market is analyzed through several critical dimensions, including service type, sector, and application environment, reflecting the diverse technical requirements of the energy industry.

By Service Type

Non-Destructive Testing (NDT) stands as the dominant service type, representing a market share of 45.2% and a value of USD 8.36 Billion in 2025. This dominance is attributed to the critical requirement for inspecting active pipelines, pressure vessels, and storage tanks without halting production. Methods such as ultrasonic testing, radiographic testing, and magnetic particle inspection are essential for detecting corrosion, weld defects, and fatigue cracks. The transition toward advanced NDT, including Phased Array Ultrasonic Testing (PAUT) and Computed Radiography, has increased the accuracy of defect sizing, thereby reducing the risk of catastrophic asset failure.

Asset Integrity Management (AIM) accounts for 28.5% of the market share, valued at USD 5.27 Billion in 2025. This segment involves the holistic management of assets to ensure they perform their required functions effectively and safely throughout their lifecycle. AIM services are increasingly being integrated with Risk-Based Inspection (RBI) methodologies, which allow operators to prioritize inspection activities based on the probability and consequence of failure. This data-centric approach is particularly valuable in mature offshore basins where maintenance costs are high and personnel safety is paramount.

Destructive Testing and QA/QC services make up 15.4% of the market share, valued at USD 2.85 Billion in 2025. While destructive testing is primarily performed during the construction and commissioning phases, QA/QC remains a recurring requirement for new projects and major overhauls. This segment is driven by the expansion of LNG liquefaction plants and new pipeline projects in the Middle East and Africa. Other specialized services, such as visual inspection and drone-led surveys, account for the remaining 10.9% of the market.

By Sector

The Midstream sector is the primary end-user, capturing 38.6% of the market with a valuation of USD 7.14 Billion in 2025. The global network of pipelines, which exceeds 3.5 million kilometers, requires continuous monitoring to prevent leaks and structural failures. Regulatory bodies like the Pipeline and Hazardous Materials Safety Administration (PHMSA) in the United States have implemented stringent "Mega Rule" requirements, mandating more frequent and accurate inspections of natural gas transmission lines. The rise in cross-border pipeline projects further accelerates demand in this sector.

The Downstream sector accounts for 34.2% of the market share, valued at USD 6.33 Billion in 2025. Refineries and petrochemical plants are characterized by high-temperature and high-pressure environments that accelerate corrosion and thermal fatigue. Periodic turnaround maintenance is a massive revenue generator for inspection firms, as thousands of heat exchangers, reactors, and storage tanks must be certified for continued operation. The focus on reducing methane slip and fugitive emissions in refineries has created a specialized niche for advanced leak detection and repair (LDAR) services.

The Upstream sector represents 27.2% of the market share, valued at USD 5.03 Billion in 2025. This segment focuses on drilling rigs, wellheads, and production platforms. Offshore upstream inspections are the most technically demanding, involving subsea ROV inspections of risers and mooring lines. As operators move into ultra-deepwater environments, the technical specifications for inspection equipment have become more rigorous, requiring tools that can withstand extreme hydrostatic pressures and low temperatures.

By Application

Onshore applications represent the majority share of 68.5%, valued at USD 12.67 Billion in 2025. The sheer volume of land-based infrastructure, including shale wells, storage terminals, and domestic pipelines, provides a steady baseline of work for regional inspection firms. Onshore services are generally more accessible and utilize a wide range of mobile NDT units and technician teams. The expansion of natural gas infrastructure in India and China is currently the strongest growth driver for onshore inspection activities.

Offshore applications account for 31.5% of the market share, worth USD 5.83 Billion in 2025. Although smaller in volume, offshore projects command significantly higher margins due to the logistical complexity and the specialized technology required for subsea and deepwater assets. Working on Floating Production Storage and Offloading (FPSO) vessels and subsea manifolds requires technicians with offshore survival certifications and expertise in specialized subsea NDT tools. The resurgence of deepwater drilling in Brazil and Guyana is expected to significantly expand this segment through 2034.

Regional Analysis

The regional distribution of the oil and gas inspection services market highlights the differences between established energy hubs and high-growth emerging markets.

North America

North America is the leading region, holding a 32.4% market share with a value of USD 6.00 Billion in 2025. This dominance is supported by the extensive pipeline network in the United States and the continuous development of the Permian Basin. The region is characterized by a very high level of regulatory compliance, where agencies such as the EPA and PHMSA drive the adoption of advanced inspection technologies. The presence of major service providers and a robust ecosystem of technology startups focusing on drone and AI-based inspections also contributes to the high market valuation.

Europe

Europe maintains a 23.5% market share, valued at USD 4.35 Billion in 2025. The European market is defined by the aging infrastructure in the North Sea and the stringent environmental standards of the European Union. Norway and the United Kingdom are hubs for subsea inspection innovation. The focus on the energy transition has also led to the repurposing of existing gas infrastructure for hydrogen transport, requiring specialized inspection services to manage hydrogen embrittlement risks. The region is a leader in implementing digital twin and predictive maintenance models.

Asia Pacific

Asia Pacific is the fastest-growing region, capturing a 22.8% market share with a value of USD 4.22 Billion in 2025. China and India are investing heavily in downstream capacity and strategic petroleum reserves. The construction of massive new refinery complexes and the expansion of the natural gas grid in China are creating high demand for onshore QA/QC and NDT services. In Australia, the large LNG export sector requires sophisticated inspection of cryogenic storage tanks and offshore production platforms.

Middle East & Africa

The Middle East & Africa (MEA) region accounts for 16.2% of the market share, worth USD 3.00 Billion in 2025. The market is dominated by national oil companies such as Saudi Aramco and ADNOC, who maintain rigorous asset integrity programs for their vast onshore and offshore fields. Large-scale capital projects in Qatar and Saudi Arabia are driving demand for construction-phase inspection. In Africa, Nigeria and Angola provide significant opportunities in the offshore sector, although geopolitical factors can influence the pace of service deployment.

Latin America

Latin America represents 5.1% of the market, valued at USD 0.94 Billion in 2025. Brazil is the primary driver in this region, with Petrobras leading massive subsea inspection programs for its pre-salt developments. Guyana has emerged as a major new hotspot for offshore inspection services as it rapidly scales up its production capacity. While smaller in share, the region offers some of the highest growth rates in the offshore subsea segment due to the nature of the deepwater assets being developed.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Non-Destructive Testing (NDT)

- Asset Integrity Management (AIM)

- QA/QC and Destructive Testing

- Visual Inspection and Drone Surveys

- Pipeline Integrity Services

By Sector

- Upstream (Offshore Platforms, Wellheads)

- Midstream (Pipelines, Terminals, Storage)

- Downstream (Refineries, Petrochemical Plants, LNG)

By Application

- Onshore

- Offshore (Subsea, Surface)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 18.50 B |

| Forecast Revenue (2034) | USD 33.35 B |

| CAGR (2025-2034) | 6.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Non-Destructive Testing (NDT), Asset Integrity Management (AIM), QA/QC and Destructive Testing, Visual Inspection and Drone Surveys, Pipeline Integrity Services), By Sector, (Upstream (Offshore Platforms, Wellheads), Midstream (Pipelines, Terminals, Storage), Downstream (Refineries, Petrochemical Plants, LNG)), By Application, (Onshore, Offshore (Subsea, Surface)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SGS SA, INTERTEK GROUP, BUREAU VERITAS, APPLUS+, MISTRAS GROUP, TEAM INC, OCEANEERING, BAKER HUGHES, DNV, TUV SUD, ELEMENT MATERIALS TECHNOLOGY, STATS GROUP, IKM GRUPPEN, DEKRA SE, RINA S.P.A., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Asset Integrity Management (AIM), QA/QC & Destructive Testing, Visual Inspection & Drone Surveys, Pipeline Integrity Services), By Sector (Upstream, Midstream, Downstream), By Application (Onshore, Offshore Subsea & Surface) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, Asset Integrity Management (AIM), QA/QC & Destructive Testing, Visual Inspection & Drone Surveys, Pipeline Integrity Services), By Sector (Upstream, Midstream, Downstream), By Application (Onshore, Offshore Subsea & Surface) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, Asset Integrity Management (AIM), QA/QC & Destructive Testing, Visual Inspection & Drone Surveys, Pipeline Integrity Services), By Sector (Upstream, Midstream, Downstream), By Application (Onshore, Offshore Subsea & Surface) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Inspection Services Market?

Global Oil & gas inspection services market valued at USD 17.32B in 2024, reaching USD 33.35B by 2034, growing at a CAGR of 6.8% from 2026–2034.

Who are the major players in the Oil and Gas Inspection Services Market?

SGS SA, INTERTEK GROUP, BUREAU VERITAS, APPLUS+, MISTRAS GROUP, TEAM INC, OCEANEERING, BAKER HUGHES, DNV, TUV SUD, ELEMENT MATERIALS TECHNOLOGY, STATS GROUP, IKM GRUPPEN, DEKRA SE, RINA S.P.A., Others

Which segments covered the Oil and Gas Inspection Services Market?

By Service Type, (Non-Destructive Testing (NDT), Asset Integrity Management (AIM), QA/QC and Destructive Testing, Visual Inspection and Drone Surveys, Pipeline Integrity Services), By Sector, (Upstream (Offshore Platforms, Wellheads), Midstream (Pipelines, Terminals, Storage), Downstream (Refineries, Petrochemical Plants, LNG)), By Application, (Onshore, Offshore (Subsea, Surface))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Inspection Services Market

Published Date : 08 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date