- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas IoT Platform Market Size & Forecast 2034 | CAGR 11.7%

Global Oil & Gas IoT Platform Market Size, Share, Growth & Industry Analysis By Deployment Model (Cloud-Based, On-Premise, Hybrid), By Operation (Upstream, Midstream, Downstream), By Application (Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking & Worker Safety), By End-User (NOCs, IOCs, Independent Operators, Oilfield Services) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 8.45 Billion | USD 22.80 Billion | 11.7% | North America, 38.2% |

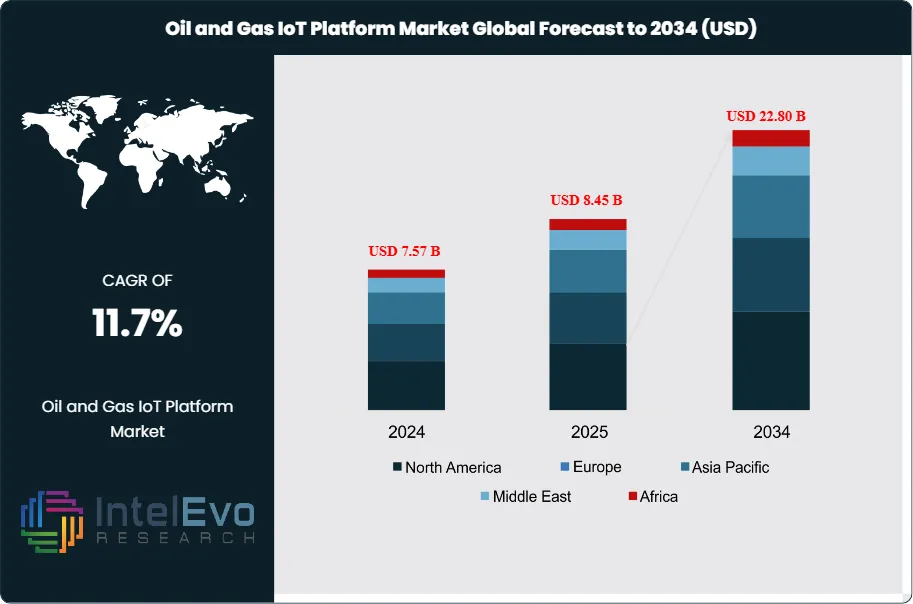

The Oil and Gas IoT Platform Market was valued at approximately USD 7.57 Billion in 2024 and reached USD 8.45 Billion in 2025. The market is projected to grow to USD 22.80 Billion by 2034, expanding at a CAGR of 11.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 14.35 Billion over the analysis period, reflecting mounting pressure across operators to digitalize production assets, reduce unplanned downtime, and comply with increasingly stringent emissions monitoring requirements set by the EPA, BSEE, and PHMSA.

Get More Information about this report -

Request Free Sample ReportThe Oil and Gas IoT Platform market encompasses integrated software and hardware solutions that connect sensors, actuators, SCADA systems, and edge devices across upstream, midstream, and downstream operations. These platforms collect real-time telemetry from wellheads, pipelines, compressor stations, refineries, and FPSOs, then apply machine learning and analytics to drive production optimization, predictive maintenance, and flow assurance. As exploration and production companies face persistent pressure to lower lifting costs per barrel, IoT-driven asset performance management has shifted from a discretionary investment to a core operational requirement. The International Energy Agency estimates that digital investments in O&G operations could reduce lifting costs by 10–20% per barrel across mature fields, providing a concrete economic justification for platform adoption.

Demand is strongest in North America, where Permian Basin operators are deploying IoT platforms to manage high-density well pads at scale. The Middle East follows closely, with National Oil Companies including Saudi Aramco and ADNOC committing multi-year digital transformation budgets exceeding USD 5 Billion through 2030. Within the Oil and Gas IoT Platform market, upstream applications hold the dominant share at 44.3% of 2025 revenues, driven by the need for real-time reservoir surveillance and wellhead monitoring. Midstream pipeline integrity monitoring is emerging as the fastest-growing sub-segment, compelled by PHMSA's Mega Rule mandating sensor-based leak detection across gas transmission lines.

Technology tailwinds are reshaping the Oil and Gas IoT Platform market at an accelerating pace. The convergence of 5G private networks, edge AI chips, and open-architecture frameworks such as ExxonMobil's Open Process Automation standard is dismantling legacy vendor lock-in. Cloud-native deployments are gaining traction, with AWS, Microsoft Azure, and Google Cloud all launching O&G-specific data connectors between 2024 and 2026. Cybersecurity risk remains a material constraint; a 2025 survey by the ISA99 Committee found that 61% of O&G operators reported at least one OT network intrusion attempt in the prior 12 months, prompting increased spending on zero-trust security layers embedded within IoT platform architectures. Despite near-term capital expenditure volatility tied to crude oil price cycles, the long-run structural case for the Oil and Gas IoT Platform market remains intact through 2034.

, By Operation (Upstream, Midstream, Downstream), By Application (Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking & Worker Safety), By End-User (NOCs, IOCs, Independent Operators, Oilfield Services) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global Oil and Gas IoT Platform market was valued at USD 8.45 Billion in 2025 and is forecast to reach USD 22.80 Billion by 2034, registering a CAGR of 11.7% during 2025–2034.

- Segment Dominance: By deployment model, cloud-based platforms held the largest share at 52.4% of total Oil and Gas IoT Platform market revenues in 2025, driven by lower upfront CAPEX and faster time-to-insight for multi-asset operators.

- Segment Dominance: By operation, upstream applications accounted for 44.3% of 2025 revenues, with wellhead monitoring, artificial lift optimization, and reservoir surveillance leading deployment use cases.

- Driver: Mandatory PHMSA pipeline sensor requirements and EPA methane detection rules are compelling capital reallocation toward IoT-enabled compliance infrastructure, adding an estimated USD 1.8 Billion in incremental platform spend across North America between 2025 and 2028.

- Restraint: OT cybersecurity vulnerabilities and high integration costs with legacy SCADA systems present the primary headwind; operators report average integration project overruns of 34% above initial budgets, dampening adoption rates among mid-tier independents.

- Opportunity: Methane emissions monitoring across the Permian Basin, Marcellus, and MENA offshore blocks represents an addressable IoT platform opportunity of USD 3.2 Billion through 2030, supported by IRA methane waste fees and UAE Net Zero 2050 commitments.

- Trend: Edge AI inference deployed directly at the wellhead or compressor station is the dominant architectural trend; shipments of ruggedized edge computing nodes into O&G environments grew 28.3% year-over-year in 2025, enabling sub-second anomaly detection without cloud round-trips.

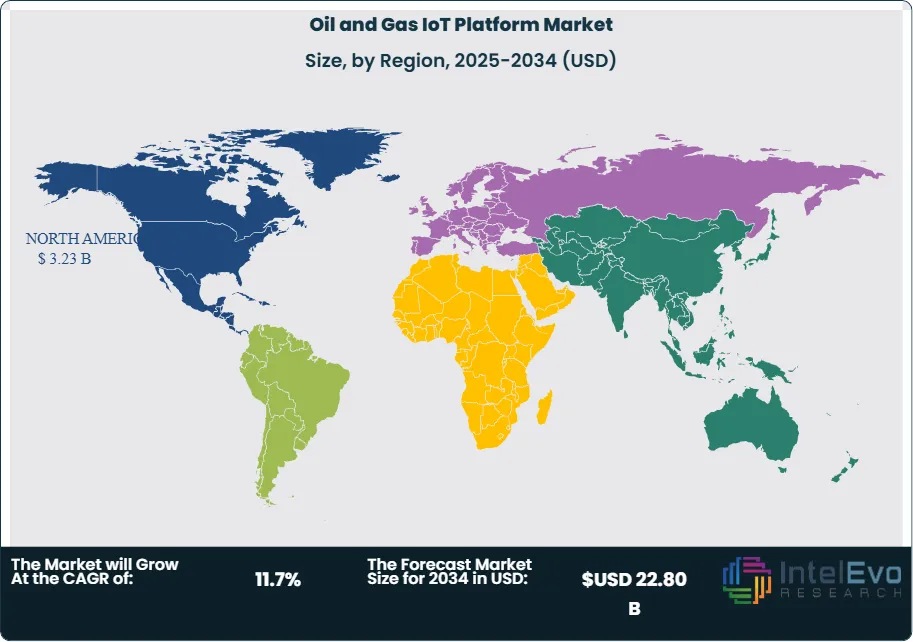

- Regional Analysis: North America led the Oil and Gas IoT Platform market with a 38.2% share, equivalent to USD 3.23 Billion in 2025 revenues, underpinned by dense Permian Basin activity and aggressive PHMSA compliance timelines.

Competitive Landscape Overview

The Oil and Gas IoT Platform market is moderately consolidated, with the top four players — Siemens AG, Honeywell International, ABB Ltd, and Emerson Electric — collectively holding approximately 41.5% of global revenues in 2025. Competition is primarily technology- and integration-driven, with vendors differentiating on open-architecture compatibility, cybersecurity depth, and analytics model accuracy. M&A activity accelerated between 2024 and 2026 as industrial automation majors absorbed specialist IoT software firms to close capability gaps in edge AI and subsea monitoring. New entrants from the cloud hyperscaler ecosystem — particularly AWS and Microsoft — are intensifying pressure on incumbent platform vendors by offering consumption-based pricing models that appeal to cost-conscious independent operators.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Siemens AG | Germany | Leader | MindSphere IoT Platform | Europe / Global | Launched AI-driven predictive maintenance module for upstream O&G (Feb 2025) |

| Honeywell International | USA | Leader | Forge Connected Plant | North America | Acquired Compressor Controls Corp assets to expand IoT SCADA portfolio (Apr 2025) |

| ABB Ltd | Switzerland | Leader | ABB Ability™ Platform | Europe / MEA | Partnered with Saudi Aramco to deploy edge IoT across 12 onshore fields (Aug 2025) |

| Emerson Electric | USA | Leader | Plantweb Digital Ecosystem | North America | Launched Plantweb Insight v4.0 with real-time wellhead analytics (Nov 2025) |

| Schneider Electric | France | Challenger | EcoStruxure Oil & Gas | Europe / LatAm | Expanded EcoStruxure deployment across Petrobras midstream assets (Jan 2026) |

| Yokogawa Electric | Japan | Challenger | OpreX Industrial IoT Suite | Asia Pacific | Signed 5-year IoT managed services agreement with INPEX (Mar 2025) |

| General Electric (GE Vernova) | USA | Challenger | OpShield / APM Connect | North America | Divested legacy SCADA units; refocused on cloud-native O&G IoT (Dec 2024) |

| PTC Inc. | USA | Niche Player | ThingWorx Industrial IoT | North America | Integrated ThingWorx with ExxonMobil's Open Process Automation framework (Jun 2025) |

| Rockwell Automation | USA | Niche Player | FactoryTalk Edge IoT | North America / Asia | Launched FactoryTalk Edge Gateway for offshore FPSO environments (Sep 2025) |

| Baker Hughes (Cordant) | USA | Niche Player | Cordant Operations Suite | Global Upstream | Deployed Cordant across 8 deepwater GoM platforms; 18% OPEX reduction reported (Jan 2026) |

By Deployment Model

The Oil and Gas IoT Platform market by Deployment Model is split across cloud, on-premise, and hybrid architectures. Cloud-based platforms commanded 52.4% of 2025 revenues, equivalent to USD 4.43 Billion. Adoption is concentrated among super-major and large independent operators with multi-basin portfolios, who require centralized data aggregation from geographically dispersed assets. AWS Energy and Microsoft Azure IoT Hub lead cloud infrastructure provision, offering pre-built connectors for OSIsoft PI, SCADA-Link, and OPC-UA protocols widely used across O&G operations. Deployment cycles for cloud-native platforms have compressed from 18 months to under 9 months on average since 2023, accelerating return-on-investment timelines. On-premise deployments retained 29.8% share in 2025, at USD 2.52 Billion, remaining essential for offshore platforms with limited satellite bandwidth and for operators in sovereign jurisdictions — such as Saudi Arabia and Russia — that mandate local data residency. Hybrid architectures captured the remaining 17.8% share at USD 1.50 Billion in 2025 and are projected to grow fastest across the forecast period as operators seek to balance data sovereignty requirements with cloud analytics capability.

By Operation

By Operation, the Oil and Gas IoT Platform market segments into upstream, midstream, and downstream verticals. Upstream held the largest share at 44.3%, or USD 3.74 Billion in 2025, reflecting demand for wellhead telemetry, artificial lift optimization, ESP performance monitoring, and fracture stimulation analytics across the Permian Basin, Montney, and pre-salt Brazil. OPEX reduction through IoT-enabled production optimization delivered measurable results: operators using real-time flow assurance platforms reported an average 8–12% production uplift per well-pad versus manual monitoring practices. Midstream captured 33.6% of 2025 revenues, at USD 2.84 Billion, propelled by PHMSA's Mega Rule imposing automated leak detection and real-time pressure monitoring across natural gas transmission infrastructure. The midstream segment is growing rapidly as compressor station IoT deployment across the Haynesville and Marcellus shales accelerates. Downstream IoT platforms accounted for 22.1%, or USD 1.87 Billion in 2025, used primarily for refinery turnaround management, distillation column optimization, and emissions compliance monitoring under EPA MACT standards.

By Application

By Application within the Oil and Gas IoT Platform market, production optimization holds the top position at 31.5% share, generating USD 2.66 Billion in 2025. Predictive maintenance follows at 27.2% (USD 2.30 Billion), driven by the proven ability of vibration, temperature, and acoustic sensors to predict rotating equipment failures 30–60 days in advance. Pipeline integrity monitoring stands at 21.8% (USD 1.84 Billion) and is the fastest-growing application sub-segment, fueled by regulatory mandates and the high cost of pipeline failure incidents. Asset tracking and field worker safety applications together represent the remaining 19.5% (USD 1.65 Billion), encompassing GPS-enabled valve tracking, ATEX-rated wearables, and confined space monitoring systems. Each application vertical is experiencing increased demand for real-time analytics delivery rather than batch-mode reporting, a shift that favors platform vendors with low-latency edge processing capabilities.

By End-User

By End-User, the Oil and Gas IoT Platform market divides between National Oil Companies (NOCs), integrated oil companies (IOCs), independent operators, and oilfield services firms. NOCs represented the largest end-user segment at 38.9% in 2025 (USD 3.29 Billion), led by Saudi Aramco, ADNOC, QatarEnergy, and Petrobras, all of which have active multi-year IoT platform procurement programs. IOCs accounted for 31.4% (USD 2.65 Billion), with TotalEnergies, Shell, and Chevron deploying standardized platforms across global portfolios to achieve operational consistency. Independent operators held 20.7% (USD 1.75 Billion) and predominantly favor SaaS-based consumption models to minimize capital commitment. Oilfield services companies including SLB, Halliburton, and Baker Hughes represented 9.0% (USD 0.76 Billion) and are increasingly embedding IoT platform licensing within service contracts, creating bundled recurring revenue streams.

Regional Analysis

North America

North America dominated the Oil and Gas IoT Platform market in 2025 with a 38.2% share, generating USD 3.23 Billion in revenues. The United States accounts for the vast majority of this figure, driven by Permian Basin well density exceeding 55,000 active producing wells and aggressive PHMSA compliance timelines for gas transmission operators. Canada contributes meaningfully through Montney and SAGD oil sands IoT deployments, where remote location and harsh climate conditions make wireless sensor networks essential for asset surveillance. Mexico's Pemex has initiated a USD 400 Million digital transformation program targeting offshore IoT deployment in the Bay of Campeche. Regulatory drivers are particularly potent: the IRA methane waste fee, effective from 2025, creates direct financial incentive for upstream operators to deploy continuous methane monitoring platforms to avoid penalties of up to USD 1,500 per metric ton of excess emissions. North America is home to the highest concentration of IoT platform vendors, fostering competitive pricing and rapid product iteration.

Europe

Europe held 24.1% of the Oil and Gas IoT Platform market in 2025, equivalent to USD 2.04 Billion. The North Sea remains the primary deployment theater, with UK and Norwegian operators investing in digital twin and IoT platforms to extend asset life on aging infrastructure. The UK's Oil and Gas Authority requires operators to file digital integrity plans demonstrating sensor-based well monitoring, driving steady procurement. Germany's energy transition places additional impetus on midstream gas network IoT, as network operators must comply with EU regulations on gas transmission system efficiency. The Netherlands, a major gas trading and distribution hub, is deploying pipeline IoT platforms to manage flow volatility during the ongoing transition away from Russian gas supplies. European competition is shaped by Siemens, ABB, and Schneider Electric, who benefit from established relationships with NOCs and national grid operators.

Asia Pacific

Asia Pacific accounted for 22.4% of the Oil and Gas IoT Platform market in 2025, generating USD 1.89 Billion. China represents the largest single country market within the region, with CNOOC and Sinopec deploying IoT platforms across offshore South China Sea fields and refinery complexes. India's ONGC and Reliance Industries have initiated multi-field IoT rollouts, supported by the Indian government's Digital India energy infrastructure initiative. Australia's LNG sector, centered on Gorgon, Ichthys, and Prelude FLNG assets, requires sophisticated process monitoring IoT platforms to manage complex liquefaction trains. Japan's Inpex Corporation and JERA are deploying IoT-enabled asset management platforms aligned with Japan's GX Green Transformation strategy. The Asia Pacific Oil and Gas IoT Platform market is growing at the fastest regional rate, supported by expanding national E&P programs and government-mandated emissions reporting frameworks.

Latin America

Latin America held 9.4% market share in 2025, generating USD 0.79 Billion. Brazil is the dominant market, with Petrobras operating the world's largest deepwater FPSO fleet and requiring robust subsea IoT systems for flow assurance and riser monitoring. Colombia's Ecopetrol has committed to a USD 150 Million digital operations program through 2027, encompassing IoT platform deployment across its midstream pipeline network. Argentina's Vaca Muerta shale development is creating new upstream IoT platform demand, particularly for wellhead automation and water handling optimization. Infrastructure limitations and currency volatility constrain growth in smaller markets. Multinational platform vendors typically partner with regional system integrators to navigate local procurement and workforce requirements.

Middle East and Africa

Middle East and Africa contributed 5.9% of the Oil and Gas IoT Platform market in 2025, at USD 0.50 Billion. Saudi Arabia is the anchor market, with Saudi Aramco operating a USD 2.5 Billion multi-year digital transformation initiative that includes IoT platform standardization across its Master Gas System and crude oil gathering networks. The UAE's ADNOC has completed IoT deployments at its onshore Liwa Plastics complex and is extending the program to offshore Umm Shaif and Zakum fields. Qatar's LNG infrastructure presents a significant IoT platform opportunity as QatarEnergy expands North Field LNG capacity by 64 MTPA. Africa lags in deployment maturity but Nigeria, Angola, and Egypt represent near-term growth markets as international operators expand subsea and onshore IoT capability to meet host government local content and emissions reporting requirements.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Model

- Cloud-Based

- On-Premise

- Hybrid

By Operation

- Upstream

- Midstream

- Downstream

By Application

- Production Optimization

- Predictive Maintenance

- Pipeline Integrity Monitoring

- Asset Tracking and Worker Safety

By End-User

- National Oil Companies (NOCs)

- Integrated Oil Companies (IOCs)

- Independent Operators

- Oilfield Services Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.45 B |

| Forecast Revenue (2034) | USD 22.80 B |

| CAGR (2025-2034) | 11.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Model, Cloud-Based, On-Premise, Hybrid, By Operation, Upstream, Midstream, Downstream, By Application, Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking and Worker Safety, By End-User, National Oil Companies (NOCs), Integrated Oil Companies (IOCs), Independent Operators, Oilfield Services Companies |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SIEMENS AG, HONEYWELL INTERNATIONAL INC., ABB LTD, EMERSON ELECTRIC CO., SCHNEIDER ELECTRIC SE, YOKOGAWA ELECTRIC CORPORATION, GE VERNOVA (GENERAL ELECTRIC), PTC INC., ROCKWELL AUTOMATION INC., BAKER HUGHES COMPANY (CORDANT), SLB (SCHLUMBERGER), HALLIBURTON (LANDMARK SOFTWARE), MICROSOFT CORPORATION (AZURE IOT), AMAZON WEB SERVICES (AWS IOT SITEWISE), CISCO SYSTEMS INC., AVEVA GROUP PLC, OSIsoft (NOW PART OF AVEVA), ASPENTECH (ASPENONE IOT), WEATHERFORD INTERNATIONAL, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Operation (Upstream, Midstream, Downstream), By Application (Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking & Worker Safety), By End-User (NOCs, IOCs, Independent Operators, Oilfield Services) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Application (Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking & Worker Safety), By End-User (NOCs, IOCs, Independent Operators, Oilfield Services) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Operation (Upstream, Midstream, Downstream), By Application (Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking & Worker Safety), By End-User (NOCs, IOCs, Independent Operators, Oilfield Services) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas IoT Platform Market?

Global Oil & gas IoT platform market valued at USD 7.57B in 2024, reaching USD 22.80B by 2034, growing at a CAGR of 11.7% from 2026–2034.

Who are the major players in the Oil and Gas IoT Platform Market?

SIEMENS AG, HONEYWELL INTERNATIONAL INC., ABB LTD, EMERSON ELECTRIC CO., SCHNEIDER ELECTRIC SE, YOKOGAWA ELECTRIC CORPORATION, GE VERNOVA (GENERAL ELECTRIC), PTC INC., ROCKWELL AUTOMATION INC., BAKER HUGHES COMPANY (CORDANT), SLB (SCHLUMBERGER), HALLIBURTON (LANDMARK SOFTWARE), MICROSOFT CORPORATION (AZURE IOT), AMAZON WEB SERVICES (AWS IOT SITEWISE), CISCO SYSTEMS INC., AVEVA GROUP PLC, OSIsoft (NOW PART OF AVEVA), ASPENTECH (ASPENONE IOT), WEATHERFORD INTERNATIONAL, Others

Which segments covered the Oil and Gas IoT Platform Market?

By Deployment Model, Cloud-Based, On-Premise, Hybrid, By Operation, Upstream, Midstream, Downstream, By Application, Production Optimization, Predictive Maintenance, Pipeline Integrity Monitoring, Asset Tracking and Worker Safety, By End-User, National Oil Companies (NOCs), Integrated Oil Companies (IOCs), Independent Operators, Oilfield Services Companies

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas IoT Platform Market

Published Date : 01 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date