- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas RPA Market Size & Forecast 2034 | CAGR 12.5%

Global Oil & Gas Robotic Process Automation (RPA) Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, On-Premise), By Application (Invoice & Payment Processing, Data Migration & Management, Compliance & Regulatory Reporting, HR & Payroll, Supply Chain & Procurement, Others), By Operation (Upstream, Midstream, Downstream), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

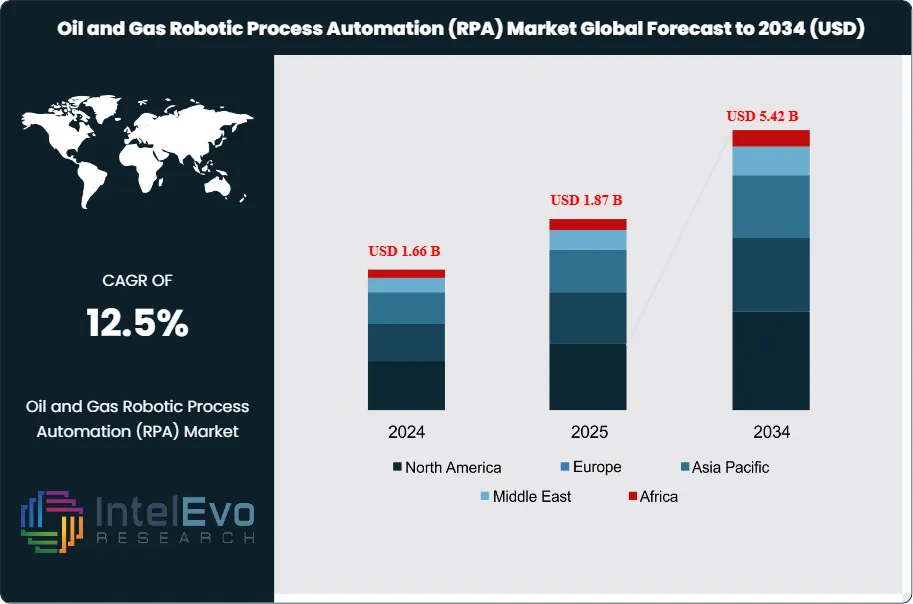

| USD 1.87 Billion | USD 5.42 Billion | 12.5% | North America, 38.4% |

The Oil and Gas Robotic Process Automation (RPA) Market was valued at approximately USD 1.66 Billion in 2024 and reached USD 1.87 Billion in 2025. The market is projected to grow to USD 5.42 Billion by 2034, expanding at a CAGR of 12.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.55 billion over the analysis period. The oil and gas robotic process automation market is experiencing strong growth as upstream, midstream, and downstream operators seek to streamline back-office functions, reduce manual data entry errors, and accelerate invoice processing cycles.

Get More Information about this report -

Request Free Sample ReportDemand for RPA solutions in the energy sector has intensified due to volatile commodity prices, which compel operators to cut operational expenditures without sacrificing production output. The oil and gas RPA market benefits from its ability to automate repetitive tasks such as well data aggregation, joint venture billing reconciliation, royalty calculations, and regulatory compliance filings. According to the American Petroleum Institute, administrative overhead in upstream operations accounts for approximately 8% of total lifting costs, a figure that RPA deployments have reduced by 35% to 50% in early adopter organizations. SLB, ExxonMobil, and Shell have each piloted RPA programs that process over 400,000 transactions monthly with error rates below 0.3%.

Regulatory drivers continue to shape RPA adoption. The U.S. Environmental Protection Agency and PHMSA mandate detailed emissions and pipeline safety reporting, creating high-volume documentation workflows ideal for automation. In Europe, the EU Methane Regulation requires real-time data submission, accelerating deployment of RPA bots integrated with SCADA systems. The market also gains traction from digital transformation initiatives funded by national oil companies such as Saudi Aramco and ADNOC, which have allocated over USD 2.1 billion to enterprise automation programs between 2024 and 2027.

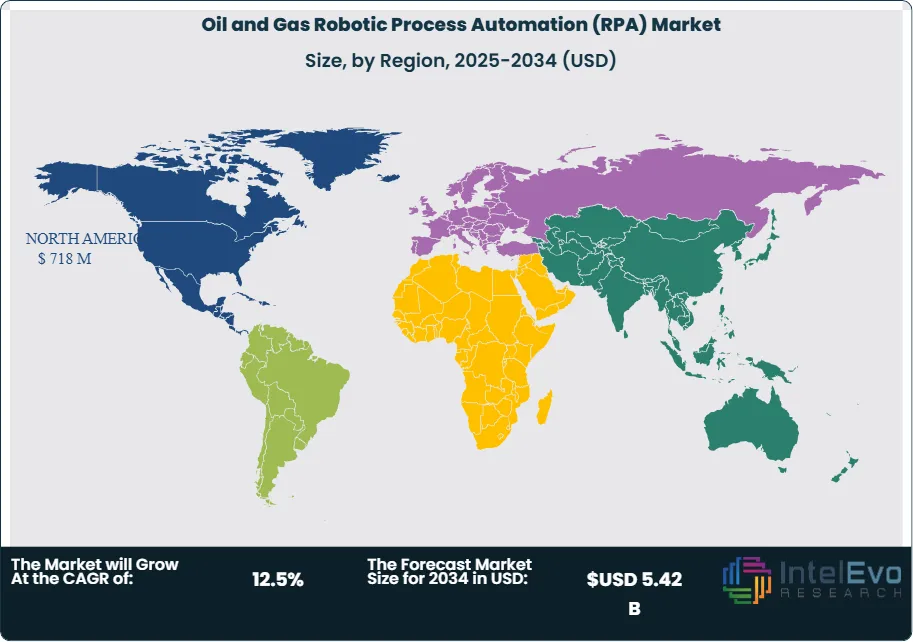

North America leads the oil and gas RPA market with a 38.4% revenue share in 2025, generating USD 718 million. The Permian Basin and Gulf of Mexico operations drive adoption, where operators integrate RPA with SAP S/4HANA and Oracle ERP systems. Europe follows with 24.6% share, propelled by North Sea operators facing workforce shortages and strict environmental reporting mandates. Asia Pacific is the fastest-growing region at 14.8% CAGR, fueled by refinery modernization projects in India, China, and Southeast Asia. The Middle East contributes 18.2% market share, anchored by mega-projects in Saudi Arabia, UAE, and Qatar that embed RPA into greenfield digital oilfield architectures.

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, On-Premise), By Application (Invoice & Payment Processing, Data Migration & Management, Compliance & Regulatory Reporting, HR & Payroll, Supply Chain & Procurement, Others), By Operation (Upstream, Midstream, Downstream), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas robotic process automation market is projected to expand from USD 1.87 billion in 2025 to USD 5.42 billion by 2034, achieving a CAGR of 12.5% during the 2026-2034 forecast period.

- Segment Dominance (By Deployment): Cloud-based RPA solutions command 58.3% market share in 2025, valued at USD 1.09 billion, driven by lower upfront costs and rapid scalability across distributed oilfield operations.

- Segment Dominance (By Application): Invoice and payment processing holds the largest application share at 26.4%, generating USD 494 million in 2025, as operators automate high-volume accounts payable workflows.

- Driver: Operational cost reduction mandates have accelerated RPA adoption; early adopters report 42% reduction in process cycle times and 55% decrease in manual data entry labor hours.

- Restraint: Legacy system integration complexity hampers deployment, with 34% of operators citing incompatibility between RPA platforms and aging SCADA or production accounting software.

- Opportunity: Intelligent automation combining RPA with AI and ML presents a USD 1.2 billion incremental opportunity by 2034, enabling predictive maintenance scheduling and anomaly detection.

- Trend: Hyperautomation strategies are gaining traction, with 47% of major operators planning enterprise-wide RPA rollouts by 2027, up from 18% in 2023.

- Regional Analysis: North America maintains market leadership with 38.4% share and USD 718 million revenue in 2025, driven by Permian Basin digitalization and Gulf of Mexico offshore automation initiatives.

Competitive Landscape Overview

The oil and gas robotic process automation market exhibits moderate consolidation, with the top four vendors capturing approximately 52% of global revenue in 2025. Competition is technology-driven, with platform capabilities, AI integration, and vertical-specific pre-built bots serving as primary differentiators. UiPath and Automation Anywhere lead the market, followed by Blue Prism and Microsoft Power Automate. Recent M&A activity has intensified as pure-play RPA vendors acquire NLP and process mining capabilities to expand intelligent automation offerings. New entrants from the enterprise software sector, including SAP and ServiceNow, have launched competing solutions, increasing competitive pressure on established players.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| UiPath | US | Leader | UiPath Platform for Oil & Gas | North America | Acquired Re:infer NLP for USD 115M (Feb 2025) |

| Automation Anywhere | US | Leader | Automation 360 for Energy | North America | Launched Gen AI process mining (Jan 2026) |

| Blue Prism (SS&C) | UK | Leader | Blue Prism Cloud for Energy | Europe | Integrated Chorus AI capabilities (Mar 2025) |

| Microsoft | US | Leader | Power Automate for O&G | Global | Released Copilot RPA connectors (Nov 2024) |

| SAP | Germany | Challenger | SAP Build Process Automation | Europe | Partnered with Schlumberger (Apr 2025) |

| IBM | US | Challenger | IBM Cloud Pak for BA | North America | Expanded watsonx RPA integration (Jun 2025) |

| NICE | Israel | Challenger | NEVA for Energy Sector | Middle East | Launched attended automation suite (Dec 2024) |

| Pega | US | Niche Player | Pega Platform for Energy | North America | Released low-code RPA modules (Aug 2025) |

| Kofax | US | Niche Player | Kofax RPA for Oil & Gas | North America | Acquired Ephesoft for USD 230M (May 2025) |

| WorkFusion | US | Niche Player | WorkFusion for Upstream | North America | Launched pre-built O&G bots (Sep 2025) |

By Deployment Mode

The oil and gas RPA market segments by deployment into cloud-based and on-premise solutions. Cloud-based RPA dominates with 58.3% market share in 2025, generating USD 1.09 billion in revenue. This segment benefits from the distributed nature of oil and gas operations, where field sites, refineries, and headquarters require unified automation platforms accessible via secure web interfaces. Major cloud providers including AWS, Microsoft Azure, and Google Cloud have established energy-sector partnerships that enable operators to deploy RPA bots alongside existing cloud ERP installations. Average implementation timelines for cloud RPA are 6 to 8 weeks, compared to 14 to 20 weeks for on-premise deployments. On-premise RPA holds 41.7% share, valued at USD 780 million in 2025. National oil companies and operators in regions with strict data sovereignty requirements prefer on-premise architectures. Saudi Aramco, ADNOC, and Petronas maintain on-premise RPA environments integrated with proprietary production management systems.

By Application

Invoice and payment processing leads the application landscape with 26.4% share, generating USD 494 million in 2025. The upstream oil and gas sector processes millions of invoices annually from service companies, equipment suppliers, and logistics providers. RPA bots extract data from PDF invoices, validate against purchase orders, and post to ERP systems, reducing processing time from 4 days to under 4 hours. Data migration and management holds 21.8% share, capturing USD 408 million. Operators employ RPA to consolidate well performance data from disparate sources, migrate legacy records to modern data lakes, and maintain master data consistency across business units. Compliance and regulatory reporting accounts for 19.2% share, valued at USD 359 million. EPA emissions reporting, PHMSA pipeline safety filings, and BSEE offshore operations documentation require extensive data compilation that RPA automates. Human resources and payroll processing contributes 14.7% share at USD 275 million, automating crew scheduling, timekeeping, and benefits administration for field personnel. Supply chain and procurement automation captures 11.3% share, generating USD 211 million. Other applications including well log digitization, joint interest billing, and production allocation comprise the remaining 6.6% share.

By Operation

Upstream operations represent the largest operational segment with 42.5% share, valued at USD 795 million in 2025. Exploration and production activities generate vast documentation requirements including drilling reports, well completion records, and production accounting that RPA streamlines. Midstream operations hold 28.3% share at USD 529 million, driven by pipeline scheduling, custody transfer documentation, and storage inventory reconciliation automation. Downstream operations capture 29.2% share, generating USD 546 million. Refinery operations, fuel distribution logistics, and retail network management present high-volume transaction processing opportunities suited for RPA deployment.

By Enterprise Size

Large enterprises dominate RPA adoption with 71.4% market share in 2025, generating USD 1.34 billion in revenue. Supermajors and national oil companies possess the IT infrastructure, change management capabilities, and transaction volumes that justify enterprise-wide RPA programs. ExxonMobil, Shell, Chevron, and BP have each deployed over 500 production bots handling more than 200 distinct processes. Small and medium enterprises hold 28.6% share at USD 535 million. Independent operators and regional service companies increasingly adopt cloud-based RPA-as-a-service models that eliminate upfront infrastructure investment. Vendors have developed SME-specific pricing tiers and pre-built bot libraries targeting common oilfield accounting and compliance tasks.

Regional Analysis

North America

North America commands 38.4% of the oil and gas RPA market in 2025, generating USD 718 million in revenue. The United States accounts for 82% of regional revenue, driven by Permian Basin operators seeking cost efficiencies amid commodity price volatility. Major independents including Pioneer Natural Resources, Diamondback Energy, and EOG Resources have implemented RPA programs that process well production data, automate land administration workflows, and streamline joint venture accounting. Gulf of Mexico offshore operators deploy RPA for regulatory compliance documentation required by BSEE and the U.S. Coast Guard. Canada contributes 14% of North American revenue, with oil sands operators in Alberta automating environmental monitoring reports and Indigenous engagement documentation. Mexico accounts for 4% following energy reform initiatives that increased private sector participation and introduced more complex commercial arrangements requiring automated contract management.

Europe

Europe holds 24.6% market share in 2025, valued at USD 460 million. The United Kingdom leads with 34% of regional revenue as North Sea operators address workforce aging and skills shortages through automation. BP and Shell UK operations have deployed RPA bots for production reporting, contractor invoice processing, and decommissioning project documentation. Norway contributes 28% of European revenue, with Equinor implementing enterprise-wide RPA for subsea operations data management and offshore logistics coordination. Germany accounts for 15% driven by refinery automation at facilities operated by BASF and OMV. The Netherlands and France together contribute 18% as integrated energy companies modernize downstream operations. EU Methane Regulation compliance requirements are accelerating RPA adoption across the region, with operators automating emissions data collection and submission workflows.

Asia Pacific

Asia Pacific represents 12.8% of the global market in 2025, generating USD 239 million in revenue, while achieving the fastest regional growth at 14.8% CAGR through 2034. China leads with 38% of regional revenue as CNPC, Sinopec, and CNOOC digitalize operations under national energy security directives. Indian refiners including Indian Oil Corporation and Reliance Industries account for 26% of regional revenue, deploying RPA for crude procurement documentation and product distribution logistics. Australia contributes 18% as LNG operators including Woodside, Santos, and Chevron Australia automate export documentation and regulatory compliance for expanding gas projects. Southeast Asian markets including Indonesia, Malaysia, and Thailand comprise 12% of regional revenue. Japan accounts for 6% with refiners implementing RPA for inventory management and regulatory reporting.

Middle East and Africa

The Middle East and Africa holds 18.2% market share in 2025, generating USD 340 million in revenue. Saudi Arabia leads with 42% of regional revenue as Saudi Aramco executes its digital transformation roadmap that includes enterprise RPA deployment across upstream and downstream operations. The UAE contributes 28% with ADNOC implementing RPA for production optimization reporting and contractor management. Qatar accounts for 15% driven by QatarEnergy LNG expansion projects requiring automated documentation workflows. Other GCC markets including Kuwait and Oman comprise 10% of regional revenue. African markets including Nigeria, Angola, and Egypt account for the remaining 5%, with adoption accelerating as international operators standardize digital processes across global portfolios.

Latin America

Latin America captures 6.0% of the global oil and gas RPA market in 2025, valued at USD 112 million. Brazil dominates with 58% of regional revenue as Petrobras and international partners operating pre-salt fields deploy RPA for production accounting and regulatory submissions to ANP. Argentina contributes 22% with Vaca Muerta shale development driving demand for automated land management and royalty calculation systems. Mexico accounts for 14% as Pemex modernization initiatives include RPA pilot programs. Colombia and other Andean markets comprise 6% of regional revenue with growing adoption among national oil companies and independent operators.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Mode

- Cloud-Based

- On-Premise

By Application

- Invoice and Payment Processing

- Data Migration and Management

- Compliance and Regulatory Reporting

- Human Resources and Payroll

- Supply Chain and Procurement

- Others

By Operation

- Upstream

- Midstream

- Downstream

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.87 B |

| Forecast Revenue (2034) | USD 5.42 B |

| CAGR (2025-2034) | 12.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode, Cloud-Based, On-Premise, By Application, Invoice and Payment Processing, Data Migration and Management, Compliance and Regulatory Reporting, Human Resources and Payroll, Supply Chain and Procurement, Others, By Operation, Upstream, Midstream, Downstream, By Enterprise Size, Large Enterprises, Small and Medium Enterprises |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | UIPATH, AUTOMATION ANYWHERE, BLUE PRISM (SS&C TECHNOLOGIES), MICROSOFT, SAP, IBM, NICE, PEGA, KOFAX, WORKFUSION, APPIAN, SERVICENOW, NINTEX, CELONIS, DATAMATICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, On-Premise), By Application (Invoice & Payment Processing, Data Migration & Management, Compliance & Regulatory Reporting, HR & Payroll, Supply Chain & Procurement, Others), By Operation (Upstream, Midstream, Downstream), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, On-Premise), By Application (Invoice & Payment Processing, Data Migration & Management, Compliance & Regulatory Reporting, HR & Payroll, Supply Chain & Procurement, Others), By Operation (Upstream, Midstream, Downstream), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, On-Premise), By Application (Invoice & Payment Processing, Data Migration & Management, Compliance & Regulatory Reporting, HR & Payroll, Supply Chain & Procurement, Others), By Operation (Upstream, Midstream, Downstream), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Robotic Process Automation (RPA) Market?

Global Oil & gas RPA market valued at USD 1.66B in 2024, reaching USD 5.42B by 2034, growing at a CAGR of 12.5% from 2026–2034.

Who are the major players in the Oil and Gas Robotic Process Automation (RPA) Market?

UIPATH, AUTOMATION ANYWHERE, BLUE PRISM (SS&C TECHNOLOGIES), MICROSOFT, SAP, IBM, NICE, PEGA, KOFAX, WORKFUSION, APPIAN, SERVICENOW, NINTEX, CELONIS, DATAMATICS, Others

Which segments covered the Oil and Gas Robotic Process Automation (RPA) Market?

By Deployment Mode, Cloud-Based, On-Premise, By Application, Invoice and Payment Processing, Data Migration and Management, Compliance and Regulatory Reporting, Human Resources and Payroll, Supply Chain and Procurement, Others, By Operation, Upstream, Midstream, Downstream, By Enterprise Size, Large Enterprises, Small and Medium Enterprises

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Robotic Process Automation (RPA) Market

Published Date : 01 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date