- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas SCADA System Market Size & Forecast 2034 | CAGR 8.5%

Global Oil & Gas SCADA System Market Size, Share, Growth & Industry Analysis By Component (Hardware Including RTU, PLC, HMI Panels & Communication Equipment, Software Including SCADA Platforms, Historian, Alarm Management & Analytics, Services Including Integration & Cybersecurity), By Application (Pipeline Monitoring, Upstream Production, Refinery Automation, LNG Terminals), By Deployment (On-Premise, Cloud, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

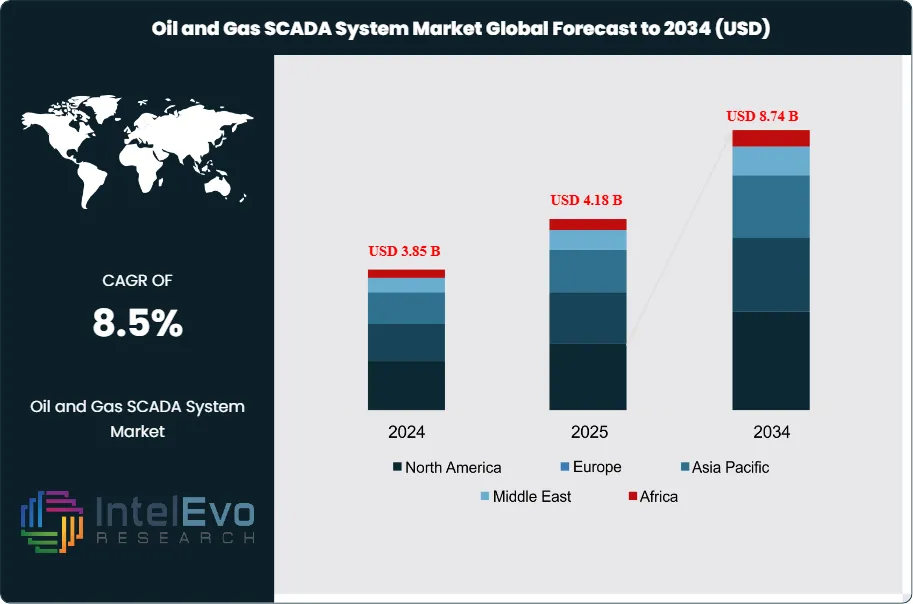

| USD 4.18 Billion | USD 8.74 Billion | 8.5% | North America, 36.8% |

The Oil and Gas SCADA System Market was valued at approximately USD 3.85 Billion in 2024 and reached USD 4.18 Billion in 2025. The market is projected to grow to USD 8.74 Billion by 2034, expanding at a CAGR of 8.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.56 Billion over the analysis period, reflecting sustained capital commitment from upstream operators, midstream pipeline companies, and downstream refiners seeking integrated supervisory control, real-time telemetry, and remote asset management across geographically dispersed production infrastructure.

Get More Information about this report -

Request Free Sample ReportOil and Gas SCADA systems function as the operational nervous system of the global energy sector, connecting wellhead sensors, pipeline pressure transmitters, compressor stations, and terminal automation systems into centralized control rooms capable of monitoring millions of process data points per second. Demand for these systems accelerates in direct proportion to upstream CAPEX cycles and the geographic expansion of pipeline infrastructure. Global upstream CAPEX reached an estimated USD 580 Billion in 2025 per IEA data, with midstream pipeline CAPEX adding a further USD 90 Billion, both figures representing multi-year highs and directly supporting SCADA procurement budgets across operator categories.

Technology forces are reshaping the Oil and Gas SCADA System market at an accelerating rate. The integration of Industrial Internet of Things (IIoT) sensors, cloud-based historian platforms, AI-driven anomaly detection, and edge computing at remote field sites is transitioning SCADA from passive data collection to active production optimization infrastructure. Operators adopting next-generation SCADA report production uptime improvements of 8-14% and unplanned shutdown reductions of 20-30%, translating directly into revenue protection on high-CAPEX offshore and shale assets.

Cybersecurity has become the defining procurement criterion in the Oil and Gas SCADA System market following a series of high-profile industrial control system incidents, including the 2021 Colonial Pipeline ransomware attack, which demonstrated the real-world consequence of inadequate OT network segmentation. TSA pipeline cybersecurity directives issued in 2021 and updated in 2023 mandate architecture controls including network segmentation, access management, and incident reporting that directly drive SCADA upgrade investment across U.S. pipeline operators. The EU NIS2 Directive, which expanded OT security obligations for critical infrastructure operators effective October 2024, is generating comparable procurement activity across European oil and gas companies.

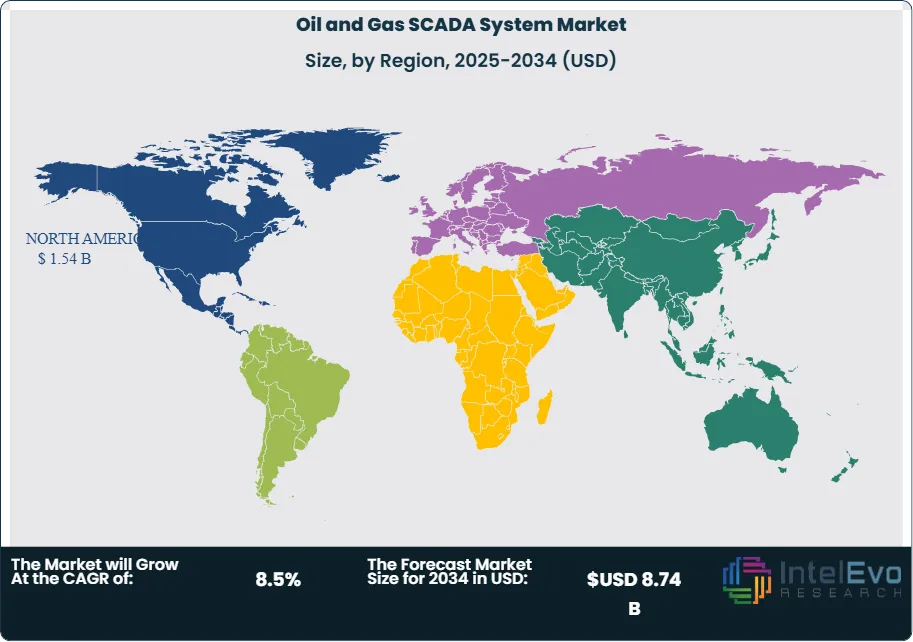

North America leads the Oil and Gas SCADA System market with 36.8% share in 2025, anchored by the Permian Basin's dense well network and an extensive interstate pipeline grid. The Middle East and Africa hold the highest regional growth rate at 10.2% CAGR through 2034, driven by Saudi Aramco, ADNOC, and Qatar Energy SCADA modernization programs. The market features moderate consolidation, with the top four vendors — Honeywell, ABB, Siemens, and Emerson — collectively controlling approximately 52% of global revenue in 2025.

, By Application (Pipeline Monitoring, Upstream Production, Refinery Automation, LNG Terminals), By Deployment (On-Premise, Cloud, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global Oil and Gas SCADA System market was valued at USD 4.18 Billion in 2025 and is forecast to reach USD 8.74 Billion by 2034, at a CAGR of 8.5% during 2025–2034.

- Segment Dominance (By Component): Hardware components — including RTUs, PLCs, and HMI panels — account for 41.6% of global SCADA system revenue in 2025 (USD 1.74 Billion), driven by field device replacement cycles across aging onshore production infrastructure.

- Segment Dominance (By Application): Pipeline monitoring and management is the leading application segment at 38.4% share (2025, USD 1.60 Billion), reflecting the global expansion of natural gas transmission infrastructure and regulatory-driven pipeline integrity management programs.

- Driver: Accelerating digital transformation investment by oil and gas operators — with global OT digitalization CAPEX estimated at USD 22 Billion in 2025 — is the primary market driver, supporting an average SCADA system refresh cycle now compressing from 12 years to 7-8 years.

- Restraint: OT cybersecurity vulnerabilities and the high cost of legacy system integration constrain adoption, with an estimated 68% of operating SCADA installations in the oil and gas sector running software versions more than 5 years behind current releases as of 2025.

- Opportunity: Cloud-native and hybrid SCADA architectures represent the largest untapped opportunity, with cloud SCADA adoption in oil and gas projected to grow from 18.2% of deployments in 2025 to over 41% by 2034, generating an incremental addressable market of USD 2.1 Billion.

- Trend: AI and machine learning integration into SCADA platforms is the dominant 2025 trend, with 34.6% of new SCADA procurement contracts in oil and gas now including AI-driven anomaly detection or predictive maintenance modules as standard requirements.

- Regional Analysis: North America leads with 36.8% market share and USD 1.54 Billion in revenue in 2025, driven by Permian Basin well count expansion and TSA cybersecurity mandates generating mandatory SCADA upgrade programs across U.S. pipeline operators.

Competitive Landscape

The Oil and Gas SCADA System market is moderately consolidated, with the top four vendors — Honeywell, ABB, Siemens, and Emerson — collectively holding approximately 52% of global revenue in 2025. Competition is technology-driven in the enterprise SCADA and cloud integration segments, and project-bid-driven in regional brownfield upgrade contracts. M&A activity intensified in 2024-2025, with ABB acquiring Aver Systems for USD 310 Million and multiple software vendors absorbing IIoT analytics startups. New entrants from the cloud-native industrial software space are challenging incumbent automation vendors on total cost of ownership in cloud SCADA deployments.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Honeywell International | USA | Leader | Experion PKS SCADA | North America / MEA | Launched Experion PKS R520 with AI anomaly detection (Feb 2025) |

| ABB Ltd | Switzerland | Leader | ABB Ability SCADA / Symphony Plus | Europe / Asia Pacific | Acquired Aver Systems OT cybersecurity unit for USD 310M (Apr 2025) |

| Siemens AG | Germany | Leader | SIMATIC WinCC OA SCADA | Europe / Middle East | Released WinCC OA v3.20 with cloud-native OT gateway (Jan 2026) |

| Emerson Electric | USA | Challenger | Ovation SCADA / DeltaV Suite | North America / Latin America | Signed 5-year SCADA managed services contract with Petrobras (Sep 2025) |

| Rockwell Automation | USA | Challenger | FactoryTalk Historian / View SE | North America | Integrated Plex Systems cloud SCADA into FactoryTalk Hub (Mar 2026) |

| Schneider Electric | France | Challenger | EcoStruxure for O&G SCADA | Europe / MEA | Deployed EcoStruxure SCADA at ADNOC Onshore for 8,000+ I/O points (Nov 2025) |

| General Electric (Vernova) | USA | Niche Player | GE Vernova SCADA for Pipelines | North America / Asia Pacific | Launched AI-driven leak detection module for midstream SCADA (Jun 2025) |

| AVEVA Group | UK | Niche Player | AVEVA System Platform / PI Server | Europe / Asia Pacific | Expanded PI Server integration with Microsoft Azure IoT Hub (Dec 2024) |

| Yokogawa Electric | Japan | Niche Player | CENTUM VP Integrated SCADA | Asia Pacific / MEA | Secured 3-year SCADA O&M contract with Saudi Aramco (Aug 2025) |

By Component

| Component | Market Share (2025) | Revenue (2025) |

| Hardware (RTU, PLC, HMI) | 41.6% | USD 1.74 Billion |

| Software | 36.8% | USD 1.54 Billion |

| Services (Integration & Managed) | 21.6% | USD 0.90 Billion |

Hardware components — comprising remote terminal units (RTUs), programmable logic controllers (PLCs), human-machine interface (HMI) panels, and communication equipment — account for 41.6% of Oil and Gas SCADA System market revenue at USD 1.74 Billion in 2025. RTUs are the foundational field data acquisition device, installed at wellheads, compressor stations, and metering points to poll sensor data and execute local control logic. The ongoing replacement of first-generation electronic RTUs with modern IEC 61131-3 compliant devices equipped with native 4G/LTE and satellite communication modules is a key hardware volume driver, particularly across remote onshore production areas in the Middle East, West Africa, and North America. HMI panels are transitioning from dedicated workstation formats to thin-client and tablet-based architectures, reducing hardware costs by 30-40% per operator station. PLCs in oil and gas SCADA applications are increasingly specified with cybersecurity-hardened firmware and hardware-enforced network segmentation to comply with ICS-CERT advisories and TSA pipeline directives.

Software holds 36.8% share at USD 1.54 Billion in 2025 and is the fastest-growing component segment at a CAGR of 10.2% through 2034. SCADA software encompasses real-time data acquisition engines, historian databases, alarm management systems, and increasingly, AI-driven analytics and digital twin platforms. The PI System by AVEVA (formerly OSIsoft) remains the most widely deployed historian in the oil and gas sector, with over 1,000 upstream and downstream installations globally. Cloud-native SCADA software platforms — where the data acquisition and visualization layers run on AWS, Azure, or Google Cloud infrastructure — are gaining share rapidly, reaching 18.2% of new deployments in 2025. Software margins are structurally higher than hardware, with leading vendors achieving gross margins of 70-80% on SaaS-based SCADA subscriptions versus 35-45% on hardware product lines.

Services — spanning system integration, managed SCADA operations, cybersecurity consulting, and training — account for 21.6% of revenue at USD 0.90 Billion in 2025. The managed SCADA services sub-segment is the fastest-growing within services, as operators outsource remote monitoring and SCADA operations to reduce internal OT staffing requirements. Emerson's multi-facility SCADA managed services contract with Petrobras, signed in September 2025 and covering 12 facilities, exemplifies the commercial model gaining traction among NOCs seeking operational cost reduction without capital investment in in-house SCADA teams.

By Application

| Application | Market Share (2025) | Revenue (2025) |

| Pipeline Monitoring & Management | 38.4% | USD 1.60 Billion |

| Upstream Production Monitoring | 31.2% | USD 1.30 Billion |

| Refinery & Processing Automation | 18.6% | USD 0.78 Billion |

| LNG Terminal & Storage | 11.8% | USD 0.49 Billion |

Pipeline monitoring and management is the largest application segment, accounting for 38.4% of the Oil and Gas SCADA System market at USD 1.60 Billion in 2025. Natural gas transmission pipelines represent the highest-density SCADA instrumentation environment, with PHMSA regulations under 49 CFR Part 192 and Part 195 mandating continuous pressure monitoring, valve position feedback, and leak detection data acquisition across all class location segments. The U.S. interstate pipeline network spans over 300,000 miles, with an estimated 40% of SCADA infrastructure more than 15 years old and subject to mandatory integrity management program upgrades. Internationally, new gas pipeline corridors in the Middle East, East Africa, and Southeast Asia are driving greenfield SCADA procurement, where integrated supervisory control from compressor station to terminal is specified as a baseline design requirement.

Upstream production monitoring accounts for 31.2% at USD 1.30 Billion in 2025. This application covers wellhead telemetry, artificial lift control, production allocation, and field data management for onshore and offshore producing assets. In unconventional shale plays, the density of well pads — with 8-16 wells per pad in the Permian Basin — creates high SCADA I/O counts per geographic footprint and drives demand for multi-well pad controllers with local edge processing capability. Offshore SCADA for FPSO vessels and subsea production systems requires ruggedized hardware certified for hazardous area installation per IECEx/ATEX standards, commanding 25-40% hardware price premiums over equivalent onshore-rated equipment.

Refinery and processing automation holds 18.6% share at USD 0.78 Billion in 2025. This segment overlaps with distributed control system (DCS) markets, but SCADA components — particularly historians, alarm management systems, and advanced process control interfaces — are distinct procurement categories at refineries. LNG terminal and storage SCADA, at 11.8% share (USD 0.49 Billion), is the highest-growth application sub-segment at 11.4% CAGR through 2034, driven by new LNG export terminal construction in the United States, Qatar, and Mozambique requiring large-scale SCADA integration from loading arm to regasification plant.

By Deployment Mode

| Deployment Mode | Market Share (2025) | Revenue (2025) |

| On-Premise | 62.4% | USD 2.61 Billion |

| Cloud / Hosted | 18.2% | USD 0.76 Billion |

| Hybrid | 19.4% | USD 0.81 Billion |

On-premise SCADA deployments retain 62.4% share at USD 2.61 Billion in 2025, reflecting the operational reality that mission-critical oil and gas control systems require deterministic response times, air-gap security architectures, and functional safety compliance that most cloud platforms cannot yet guarantee for real-time control applications. Brownfield refinery and pipeline operators with existing on-premise SCADA infrastructure face substantial integration complexity and cost barriers to migration, sustaining the installed base. However, new greenfield projects are increasingly specifying hybrid architectures from the outset. Cloud and hybrid combined represent 37.6% of the 2025 market and are forecast to exceed 50% of deployments by 2030, driven by the economics of centralizing historian data, dashboarding, and analytics on cloud infrastructure while retaining local on-premise control logic at field sites.

Regional Analysis

| Region | Share (2025) | Revenue (2025) | CAGR (2025–2034) |

| North America | 36.8% | USD 1.54 Billion | 7.8% |

| Europe | 24.2% | USD 1.01 Billion | 7.4% |

| Middle East & Africa | 19.6% | USD 0.82 Billion | 10.2% |

| Asia Pacific | 14.8% | USD 0.62 Billion | 9.6% |

| Latin America | 4.6% | USD 0.19 Billion | 8.1% |

North America

North America dominates the Oil and Gas SCADA System market with 36.8% share and USD 1.54 Billion in revenue in 2025, expanding at a 7.8% CAGR through 2034. The United States accounts for approximately 80% of the regional total, with SCADA demand concentrated in four primary sectors: Permian Basin upstream production monitoring, U.S. Gulf Coast LNG export terminal automation, interstate natural gas pipeline integrity management, and Gulf of Mexico deepwater facility remote monitoring. TSA cybersecurity directives issued under 49 U.S.C. § 60105 mandate that hazardous liquid and natural gas pipeline operators implement OT network segmentation, access control, and incident reporting — requirements that are directly translating into SCADA hardware and software upgrade contracts. The U.S. EIA reports that domestic natural gas production reached 103 Bcf/d in 2025, requiring extensive SCADA infrastructure across gathering, processing, and transmission networks. Canada's oil sands operations in the Athabasca region and Montney shale gas plays represent secondary demand centers, with operators including Canadian Natural Resources and Cenovus Energy executing multi-site SCADA modernization programs. Mexico's Pemex, constrained by budget cycles, is selectively upgrading SCADA at its Cantarell and Ku-Maloob-Zaap offshore platforms.

Europe

Europe accounts for 24.2% of the Oil and Gas SCADA System market at USD 1.01 Billion in 2025, growing at a 7.4% CAGR through 2034. The EU NIS2 Directive, effective October 2024, substantially expanded cybersecurity obligations for operators of essential services — including oil and gas transmission and distribution — mandating risk assessments, incident reporting within 24 hours, and supply chain security measures that directly drive SCADA security upgrade procurement. Norway is the region's largest single-country SCADA market, with Equinor operating one of the world's most SCADA-intensive offshore production footprints across the Johan Sverdrup, Snøhvit, and Troll fields. The Netherlands, as the hub of European natural gas distribution through the Gasunie grid, maintains extensive SCADA infrastructure across 14,000 km of transmission pipelines. The UK's North Sea decommissioning wave, while reducing production asset count, simultaneously drives SCADA upgrade investment as operators require real-time well integrity and subsea system monitoring during abandonment phases. Germany's SCADA market is primarily concentrated in natural gas distribution networks and refinery automation, where BASF's Ludwigshafen complex and Rheinland Raffinerie operate among Europe's most advanced process SCADA installations.

Middle East & Africa

The Middle East and Africa hold 19.6% of global Oil and Gas SCADA System revenue at USD 0.82 Billion in 2025, with the highest regional CAGR at 10.2% through 2034. Saudi Arabia is the region's dominant SCADA market, anchored by Saudi Aramco's ongoing Master Gas System expansion and upstream SCADA modernization across the Ghawar, Khurais, and Haradh super-giant fields. Saudi Aramco's Intelligent Oil Field program has deployed SCADA and real-time production monitoring across more than 300 well pads, with ongoing investment in AI-integrated SCADA visualization platforms. The UAE's ADNOC has committed to full digitalization of its onshore and offshore production infrastructure by 2028, with Schneider Electric's EcoStruxure SCADA deployment at ADNOC Onshore — covering 8,000+ I/O points — serving as the reference architecture for subsequent phases. Qatar Energy's North Field expansion program, the world's largest LNG megaproject, requires integrated SCADA across wellhead, pipeline, and LNG terminal segments. In Africa, Nigeria's NNPC and Angola's Sonangol are executing SCADA modernization under national digital transformation frameworks, while Mozambique's new LNG projects are procuring greenfield SCADA systems.

Asia Pacific

Asia Pacific accounts for 14.8% of global Oil and Gas SCADA System revenue at USD 0.62 Billion in 2025, expanding at a 9.6% CAGR through 2034 — the second-highest regional growth rate. China's CNPC and CNOOC are the region's largest SCADA buyers, with CNPC's West-East Pipeline system spanning over 70,000 km requiring continuous SCADA monitoring and integrity management. China's domestic SCADA vendors — including SUPCON and Hollysys Automation — hold significant share in the domestic market, limiting penetration by international vendors to premium technology segments. India's ONGC and GAIL are executing SCADA upgrade programs across their producing fields and gas distribution networks, with the Petroleum and Natural Gas Regulatory Board (PNGRB) mandating real-time pipeline monitoring for city gas distribution companies. Australia's LNG sector — including the Ichthys, Prelude FLNG, and North West Shelf projects — represents a high-value SCADA procurement segment, with offshore SCADA systems requiring IECEx-rated hardware and integrated cybersecurity architectures.

Latin America

Latin America holds 4.6% of Oil and Gas SCADA System revenue at USD 0.19 Billion in 2025, growing at an 8.1% CAGR through 2034. Brazil dominates the region, with Petrobras operating one of the world's largest offshore SCADA-dependent production footprints across 73 production platforms in the Santos and Campos basins. Emerson's 5-year managed SCADA services agreement with Petrobras, signed in September 2025, covers 12 facilities and exemplifies the trend toward outsourced SCADA operations in the region. Colombia's Ecopetrol and Ecuador's Petroecuador are secondary markets, with SCADA investment concentrated in upstream production monitoring and pipeline integrity management across their producing basins. Argentina's YPF is executing SCADA modernization across the Vaca Muerta shale play as pad drilling density increases.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Hardware (RTU, PLC, HMI Panels, Communication Equipment)

- Software (SCADA Platform, Historian, Alarm Management, Analytics)

- Services (System Integration, Managed SCADA Operations, Cybersecurity Consulting)

By Application

- Pipeline Monitoring and Management

- Upstream Production Monitoring

- Refinery and Processing Automation

- LNG Terminal and Storage

By Deployment Mode

- On-Premise

- Cloud / Hosted

- Hybrid

By Operation

- Upstream

- Midstream

- Downstream

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.18 B |

| Forecast Revenue (2034) | USD 8.74 B |

| CAGR (2025-2034) | 8.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware (RTU, PLC, HMI Panels, Communication Equipment), Software (SCADA Platform, Historian, Alarm Management, Analytics), Services (System Integration, Managed SCADA Operations, Cybersecurity Consulting)), By Application, (Pipeline Monitoring and Management, Upstream Production Monitoring, Refinery and Processing Automation, LNG Terminal and Storage), By Deployment Mode, (On-Premise, Cloud / Hosted, Hybrid), By Operation, (Upstream, Midstream, Downstream) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HONEYWELL INTERNATIONAL, ABB LTD, SIEMENS AG, EMERSON ELECTRIC, ROCKWELL AUTOMATION, SCHNEIDER ELECTRIC, GENERAL ELECTRIC (GE VERNOVA), AVEVA GROUP (SCHNEIDER ELECTRIC), YOKOGAWA ELECTRIC CORPORATION, BAKER HUGHES (PANAMETRICS / BENTLY NEVADA), SLB (SCHLUMBERGER), INDUCTIVE AUTOMATION, FAST/TOOLS (YOKOGAWA OT SCADA), SUPCON TECHNOLOGY (CHINA), HOLLYSYS AUTOMATION TECHNOLOGIES, CIRCULAR SOLUTIONS / MOXA INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Pipeline Monitoring, Upstream Production, Refinery Automation, LNG Terminals), By Deployment (On-Premise, Cloud, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends & Forecast 2026–2034")

, By Application (Pipeline Monitoring, Upstream Production, Refinery Automation, LNG Terminals), By Deployment (On-Premise, Cloud, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends & Forecast 2026–2034")

, By Application (Pipeline Monitoring, Upstream Production, Refinery Automation, LNG Terminals), By Deployment (On-Premise, Cloud, Hybrid), By Operation (Upstream, Midstream, Downstream) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas SCADA System Market?

Global oil & gas SCADA system market valued at USD 3.85B in 2024, reaching USD 8.74B by 2034, growing at a CAGR of 8.5% from 2026–2034.

Who are the major players in the Oil and Gas SCADA System Market?

HONEYWELL INTERNATIONAL, ABB LTD, SIEMENS AG, EMERSON ELECTRIC, ROCKWELL AUTOMATION, SCHNEIDER ELECTRIC, GENERAL ELECTRIC (GE VERNOVA), AVEVA GROUP (SCHNEIDER ELECTRIC), YOKOGAWA ELECTRIC CORPORATION, BAKER HUGHES (PANAMETRICS / BENTLY NEVADA), SLB (SCHLUMBERGER), INDUCTIVE AUTOMATION, FAST/TOOLS (YOKOGAWA OT SCADA), SUPCON TECHNOLOGY (CHINA), HOLLYSYS AUTOMATION TECHNOLOGIES, CIRCULAR SOLUTIONS / MOXA INC., Others

Which segments covered the Oil and Gas SCADA System Market?

By Component, (Hardware (RTU, PLC, HMI Panels, Communication Equipment), Software (SCADA Platform, Historian, Alarm Management, Analytics), Services (System Integration, Managed SCADA Operations, Cybersecurity Consulting)), By Application, (Pipeline Monitoring and Management, Upstream Production Monitoring, Refinery and Processing Automation, LNG Terminal and Storage), By Deployment Mode, (On-Premise, Cloud / Hosted, Hybrid), By Operation, (Upstream, Midstream, Downstream)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas SCADA System Market

Published Date : 30 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date