- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil & Gas Workforce Software Market Forecast 2034 | CAGR 9.9%

Global Oil and Gas Workforce Management Software Market Size, Share, Growth & Industry Analysis By Deployment (Cloud-Based, On-Premise, Hybrid), By End-User (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application (Crew Scheduling & Dispatch, Time & Attendance, Compliance & Safety, Training & Competency, Workforce Analytics), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 4.2 Billion | USD 9.8 Billion | 9.9% | North America, 38.5% |

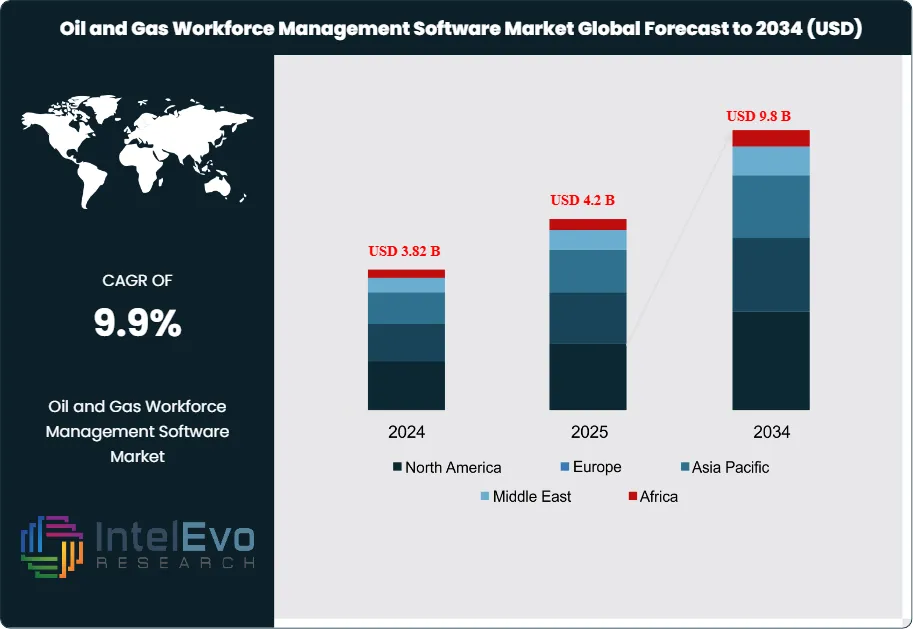

The Oil and Gas Workforce Management Software Market was valued at approximately USD 3.82 Billion in 2024 and reached USD 4.2 Billion in 2025. The market is projected to grow to USD 9.8 Billion by 2034, expanding at a CAGR of 9.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.6 billion over the analysis period. Oil and gas workforce management software encompasses scheduling, competency tracking, fatigue risk management, time and attendance, payroll integration, and field crew optimization platforms tailored to upstream, midstream, and downstream operations.

Get More Information about this report -

Request Free Sample ReportDemand for oil and gas workforce management software is accelerating as operators face simultaneous pressure from an aging field workforce and tightening safety regulations. The American Petroleum Institute (API) and OSHA have intensified compliance reporting requirements since 2023, pushing operators to adopt digital crew management tools. Upstream operators deploying AI-enabled scheduling modules reported a 22% reduction in unplanned overtime costs during 2025 field trials. Cloud-based deployment accounted for 61.3% of new license revenue in 2025, reflecting a broad shift away from legacy on-premise installations across both national oil companies and independent producers.

Technology effects are reshaping adoption patterns. AI and machine learning modules now handle crew competency matching, fatigue risk scoring, and predictive attrition modeling. Automation of manual timesheets has cut administrative overhead by an estimated 30% for midstream pipeline operators in the Permian Basin. Digital twin integration allows real-time headcount simulation on offshore platforms, reducing mobilization lead times by up to four days. These capabilities are converting workforce management from a back-office cost center into a strategic planning function.

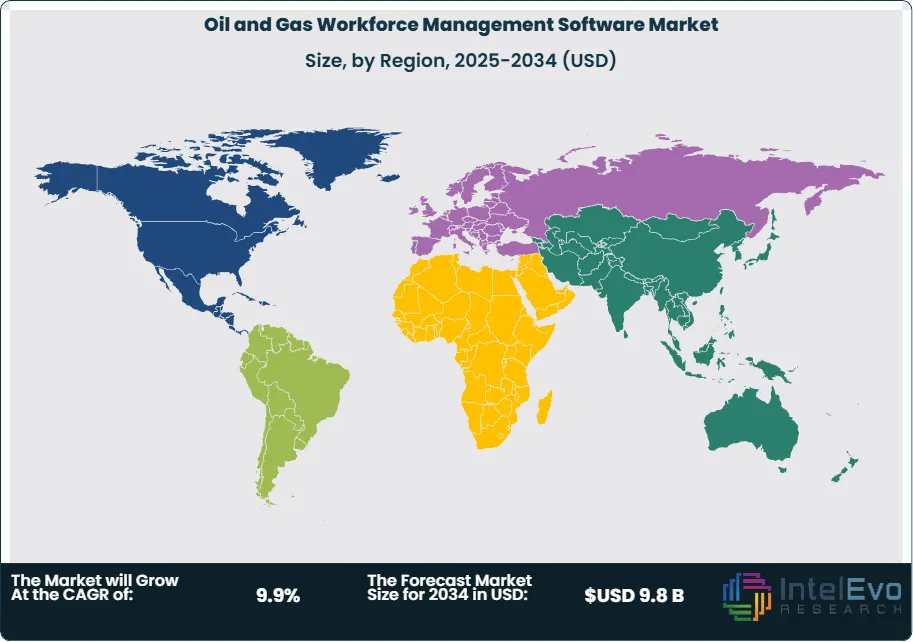

Regional investment patterns show North America leading with 38.5% market share in 2025, driven by shale basin activity and stringent OSHA reporting mandates. The Middle East and Africa region is the fastest-growing area, with Saudi Aramco and ADNOC both mandating enterprise workforce platforms across all operated assets by 2026. Europe accounted for 21.2% of the market in 2025, supported by North Sea decommissioning projects that demand specialized crew tracking. Asia Pacific held 17.8% share, with India and China investing in refinery workforce digitization. Latin America contributed 5.0%, concentrated in Brazil pre-salt operations. Risk factors include data sovereignty concerns, integration complexity with legacy ERP systems, and cybersecurity threats targeting cloud-hosted labor data. The oil and gas workforce management software market outlook remains strong as digital transformation budgets across the global energy sector continue to expand through 2034.

, By End-User (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application (Crew Scheduling & Dispatch, Time & Attendance, Compliance & Safety, Training & Competency, Workforce Analytics), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oil and gas workforce management software market was valued at USD 4.2 billion in 2025 and is projected to reach USD 9.8 billion by 2034, registering a CAGR of 9.9% over the forecast period 2025–2034.

- Segment Dominance (By Deployment): Cloud-based deployment captured 61.3% of the market in 2025, valued at USD 2.57 billion, as operators shifted to subscription-model platforms with lower upfront capital requirements.

- Segment Dominance (By End-User): Upstream operations accounted for 42.0% of market revenue in 2025, reflecting intensive field crew scheduling needs across drilling, completions, and production optimization activities.

- Driver: Tightening safety and compliance regulations from OSHA, API, and BSEE are compelling operators to digitize workforce tracking; 68% of large E&P companies had initiated workforce software procurement by 2025.

- Restraint: Integration complexity with legacy ERP and SCADA systems remains a barrier; average implementation timelines exceed 14 months for enterprise-wide deployments, increasing total cost of ownership by 18–25%.

- Opportunity: AI-powered predictive workforce analytics represent a USD 1.9 billion incremental opportunity through 2034, enabling operators to forecast attrition, optimize crew rotations, and reduce non-productive time by up to 15%.

- Trend: Mobile-first workforce applications surged to 54% adoption among field crews in 2025, up from 31% in 2022, driven by ruggedized tablet deployments and offline-capable scheduling apps for remote well sites.

- Regional Analysis: North America led with 38.5% market share, generating USD 1.62 billion in 2025; strong shale activity in the Permian Basin and Gulf of Mexico deepwater operations anchored demand.

Competitive Landscape Overview

The oil and gas workforce management software market is moderately consolidated, with the top four vendors collectively holding approximately 44% of global revenue in 2025. Competition is primarily technology-driven, centering on AI scheduling algorithms, regulatory compliance modules, and cloud platform reliability. Merger and acquisition activity accelerated through 2024–2025 as enterprise software firms sought to acquire domain-specific workforce solutions. New entrants from the broader HR-tech sector have intensified price competition in the mid-market tier, though established players retain loyalty through deep integration with oilfield ERP and SCADA platforms.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SAP SE | Germany | Leader | SAP S/4HANA Workforce for Energy | Europe | Launched AI crew scheduler for upstream operations (Mar 2025) |

| Oracle Corporation | US | Leader | Oracle Energy WFM Cloud | North America | Acquired PetroPlan Analytics for USD 420M (Jan 2025) |

| Halliburton (Landmark) | US | Leader | Landmark iEnergy Workforce | North America | Expanded MENA workforce module partnership with ADNOC (Jun 2025) |

| IBM Corporation | US | Leader | IBM Maximo Worker Insights | North America | Released generative AI fatigue risk model (Sep 2025) |

| Workday Inc. | US | Challenger | Workday Adaptive Workforce | North America | Added offshore rotation management module (Feb 2026) |

| Honeywell International | US | Challenger | Honeywell Forge WFM | Middle East | Signed five-year platform deal with Aramco (Dec 2024) |

| AVEVA Group | UK | Challenger | AVEVA Operations Crew Manager | Europe | Integrated digital twin workforce simulation (Apr 2025) |

| Accenture plc | Ireland | Challenger | Accenture Energy Workforce Platform | Global | Launched managed WFM service for NOCs (Nov 2025) |

| Petro.ai | US | Niche Player | Petro.ai Crew Optimizer | North America | Closed USD 85M Series C funding round (Aug 2025) |

| ARCOS LLC | US | Niche Player | ARCOS Resource Management | North America | Expanded into midstream pipeline crew scheduling (May 2025) |

By Deployment:

Cloud-based deployment dominated the market with a 61.3% share valued at USD 2.57 billion in 2025. Operators across the Permian Basin, North Sea, and Middle East are migrating from on-premise installations to cloud-hosted platforms that offer automatic regulatory updates, elastic scalability during drilling campaigns, and lower initial CAPEX. Subscription pricing models have reduced procurement cycle times by approximately 40%. Multi-tenant SaaS architectures allow vendors to push quarterly compliance patches aligned with OSHA and API reporting changes. On-premise deployment held 28.2% of the market in 2025, valued at USD 1.18 billion. National oil companies with strict data sovereignty mandates, including Saudi Aramco and Gazprom, still favor on-premise installations. On-premise systems offer tighter integration with proprietary SCADA and production databases but carry higher maintenance overhead. Hybrid deployment captured the remaining 10.5%, or USD 0.44 billion. Hybrid models appeal to operators managing both onshore and offshore assets who need local data processing at well sites combined with centralized analytics in cloud environments.

By End-User:

Upstream operations accounted for 42.0% of market revenue in 2025, generating USD 1.76 billion. Drilling contractors, E&P companies, and completions firms require complex crew rotation scheduling across remote locations, competency verification for high-risk tasks, and fatigue risk management under BSEE and API standards. The high variability of field operations, combined with skilled labor shortages, makes upstream the most software-intensive segment. Midstream operations held 26.5% share, valued at USD 1.11 billion. Pipeline operators, gas processing plants, and storage terminal managers use workforce software to coordinate maintenance turnarounds, track PHMSA-mandated operator qualifications, and manage geographically dispersed field technicians. Downstream operations captured 22.0% of revenue, or USD 0.92 billion, driven by refinery turnaround scheduling and petrochemical plant shift optimization. Oilfield services companies accounted for the remaining 9.5%, valued at USD 0.40 billion, using workforce platforms to manage multi-client crew deployments across multiple basins.

By Application:

Crew scheduling and dispatch led with 33.0% market share in 2025, valued at USD 1.39 billion. Scheduling is the entry point for most workforce management deployments, addressing the core challenge of matching certified personnel to field assignments across multiple rigs, platforms, and facilities. AI-driven scheduling engines now factor in certifications, fatigue limits, travel logistics, and contractual labor rules. Time and attendance management held 21.5%, generating USD 0.90 billion. Digital timesheet capture via mobile devices and biometric clock-in systems has replaced paper-based processes at most large operators. Compliance and safety management captured 19.0% share, worth USD 0.80 billion, driven by mandatory incident reporting, training record verification, and audit-ready documentation under OSHA and API standards. Competency and training management accounted for 15.5%, or USD 0.65 billion. This segment tracks certifications, well control training, H2S awareness, and equipment-specific qualifications. Workforce analytics and reporting held the remaining 11.0%, valued at USD 0.46 billion, encompassing dashboards for labor cost analysis, productivity benchmarking, and predictive attrition modeling.

By Enterprise Size:

Large enterprises commanded 66.0% of market revenue in 2025, valued at USD 2.77 billion. Supermajors, national oil companies, and large independents with workforces exceeding 5,000 field employees require enterprise-grade platforms capable of managing multi-basin, multi-country operations with role-based access controls, union labor rule engines, and integration with SAP or Oracle ERP systems. These organizations also drive the majority of custom implementation revenue. Small and medium enterprises (SMEs) held 34.0% share, generating USD 1.43 billion. Independent E&P operators, regional drilling contractors, and midstream service firms increasingly adopt modular, subscription-based workforce tools that can be deployed in weeks rather than months. Vendor-hosted cloud solutions with preconfigured oil and gas workflows have lowered the entry barrier for SMEs, fueling a 14.2% year-over-year growth rate in this segment during 2025.

Regional Analysis

North America:

North America led the oil and gas workforce management software market with 38.5% share, generating USD 1.62 billion in 2025. The United States accounted for the bulk of regional demand, driven by Permian Basin shale operations, Gulf of Mexico deepwater drilling, and stringent OSHA workforce safety requirements. Canada contributed through oil sands operations in Alberta and Montney basin activity, where crew scheduling complexity is amplified by remote locations and harsh climate rotations. Mexico's state-owned Pemex accelerated workforce digitization as part of its 2024–2028 modernization plan. The region benefits from a mature IT infrastructure, high cloud adoption rates exceeding 70%, and established vendor ecosystems. Over 85% of the top 50 US E&P companies had deployed at least one workforce management module by 2025. BSEE offshore safety mandates and PHMSA pipeline operator qualification rules continue to compel investment in compliance-grade tracking platforms.

Europe:

Europe held 21.2% of the global market, valued at USD 0.89 billion in 2025. The United Kingdom anchored regional demand through North Sea operations, where offshore platform decommissioning projects require specialized crew competency tracking and regulatory documentation under the UK Health and Safety Executive framework. Norway's Equinor and Aker BP deployed enterprise workforce platforms across their continental shelf assets. Germany contributed through downstream refinery workforce optimization, while France's TotalEnergies expanded digital crew management across its global operated portfolio from its European technology center. The European Union's evolving digital labor regulations and Working Time Directive compliance requirements push operators toward automated time tracking and fatigue management modules. Regional spending on workforce analytics grew at 11.3% during 2025, outpacing the global average.

Asia Pacific:

Asia Pacific captured 17.8% market share, generating USD 0.75 billion in 2025. China led regional demand as PetroChina and CNOOC digitized field workforce operations across onshore and offshore assets. India's Reliance Industries and ONGC invested in crew scheduling platforms for refinery complexes and deepwater exploration blocks. Australia's LNG export terminals, including facilities at Gladstone and Darwin, adopted workforce management software to coordinate multi-employer rotational crews. South Korea's refinery operators, led by SK Innovation, implemented shift optimization tools. The region's growth trajectory is supported by rapid cloud infrastructure expansion, government-backed digitization programs in India and China, and rising offshore drilling activity in Southeast Asia.

Latin America:

Latin America accounted for 5.0% of the global market, generating USD 0.21 billion in 2025. Brazil dominated regional demand through Petrobras pre-salt deepwater operations, where complex FPSO crew rotations and helicopter logistics require advanced scheduling platforms. Petrobras mandated digital competency tracking across all operated FPSOs by mid-2025. Argentina's Vaca Muerta shale development attracted workforce management investment from YPF and international operators. Colombia and Trinidad and Tobago contributed smaller but growing shares as upstream activity expanded. Limited cloud infrastructure in remote operating areas remains a challenge; vendors offering offline-capable mobile applications hold a competitive advantage in this region.

Middle East and Africa:

The Middle East and Africa region held 17.5% market share, valued at USD 0.74 billion in 2025, and registered the fastest growth rate globally. Saudi Arabia's Saudi Aramco and UAE's ADNOC both issued enterprise-wide mandates for workforce management software adoption during 2024–2025, covering all upstream, midstream, and downstream operations. Qatar's North Field expansion project, the largest LNG development in history, generated significant workforce coordination demand. Kuwait and Oman invested in refinery turnaround crew management. In Africa, Nigeria's upstream operators and Angola's deepwater projects adopted workforce platforms to manage expatriate and local crew rotations. South Africa's downstream sector also contributed to regional growth. Governments across the Gulf Cooperation Council are linking workforce digitization targets to national economic diversification strategies, creating sustained long-term demand.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment

- Cloud-Based

- On-Premise

- Hybrid

By End-User

- Upstream Operations

- Midstream Operations

- Downstream Operations

- Oilfield Services Companies

By Application

- Crew Scheduling and Dispatch

- Time and Attendance Management

- Compliance and Safety Management

- Competency and Training Management

- Workforce Analytics and Reporting

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.2 B |

| Forecast Revenue (2034) | USD 9.8 B |

| CAGR (2025-2034) | 9.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment, (Cloud-Based, On-Premise, Hybrid), By End-User, (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application, (Crew Scheduling and Dispatch, Time and Attendance Management, Compliance and Safety Management, Competency and Training Management, Workforce Analytics and Reporting), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAP SE, ORACLE CORPORATION, HALLIBURTON (LANDMARK), IBM CORPORATION, WORKDAY INC., HONEYWELL INTERNATIONAL, AVEVA GROUP, ACCENTURE PLC, PETRO.AI, ARCOS LLC, KRONOS (UKG), CERIDIAN HCM, DASSAULT SYSTEMES, EMERSON ELECTRIC, SIEMENS AG, INFOR INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application (Crew Scheduling & Dispatch, Time & Attendance, Compliance & Safety, Training & Competency, Workforce Analytics), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

, By End-User (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application (Crew Scheduling & Dispatch, Time & Attendance, Compliance & Safety, Training & Competency, Workforce Analytics), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

, By End-User (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application (Crew Scheduling & Dispatch, Time & Attendance, Compliance & Safety, Training & Competency, Workforce Analytics), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil and Gas Workforce Management Software Market?

Global Oil & gas workforce management software market valued at USD 3.82B in 2024, reaching USD 9.8B by 2034, growing at a CAGR of 9.9% from 2026–2034.

Who are the major players in the Oil and Gas Workforce Management Software Market?

SAP SE, ORACLE CORPORATION, HALLIBURTON (LANDMARK), IBM CORPORATION, WORKDAY INC., HONEYWELL INTERNATIONAL, AVEVA GROUP, ACCENTURE PLC, PETRO.AI, ARCOS LLC, KRONOS (UKG), CERIDIAN HCM, DASSAULT SYSTEMES, EMERSON ELECTRIC, SIEMENS AG, INFOR INC., Others

Which segments covered the Oil and Gas Workforce Management Software Market?

By Deployment, (Cloud-Based, On-Premise, Hybrid), By End-User, (Upstream Operations, Midstream Operations, Downstream Operations, Oilfield Services Companies), By Application, (Crew Scheduling and Dispatch, Time and Attendance Management, Compliance and Safety Management, Competency and Training Management, Workforce Analytics and Reporting), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil and Gas Workforce Management Software Market

Published Date : 03 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date