- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oil Country Tubular Goods Market Size, Forecast 2034 | CAGR of 5.6%

Global Oil Country Tubular Goods (OCTG) Market Size, Share, Growth & Industry Analysis By Product Type (Casing, Tubing, Drill Pipe, Line Pipe OCTG Grade, Accessories & Couplings), By Grade (API Grades J55, N80, L80, P110, Premium & Semi-Premium Connections, Corrosion-Resistant Alloys), By Application (Unconventional, Onshore, Offshore Deepwater & Shallow Water, Geothermal), By Well Type (Horizontal, Vertical, Directional) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

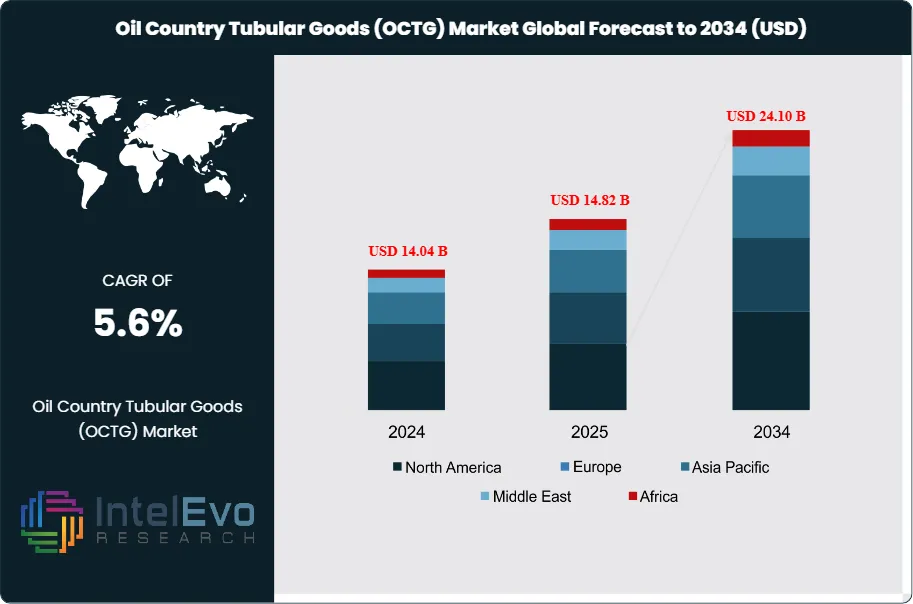

| USD 14.82 Billion | USD 24.10 Billion | 5.6% | North America, 38.4% |

The Oil Country Tubular Goods (OCTG) Market was valued at approximately USD 14.04 Billion in 2024 and reached USD 14.82 Billion in 2025. The market is projected to grow to USD 24.10 Billion by 2034, expanding at a CAGR of 5.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 9.28 Billion over the analysis period, driven by accelerating upstream capital expenditures, rising global rig counts, and structural demand from unconventional resource development across North America and the Middle East.

Get More Information about this report -

Request Free Sample ReportOil Country Tubular Goods — which encompass casing, tubing, drill pipe, and line pipe used in well construction and completion — are foundational consumables for every phase of upstream oil and gas operations. Demand for OCTG tracks closely with active drilling programs, making the market acutely responsive to crude oil price cycles, OPEC+ production quota adjustments, and the capital allocation strategies of national oil companies and independent operators alike. In 2025, global upstream CAPEX is estimated at USD 580 Billion, according to IEA data, with a growing proportion directed toward complex well architectures in shale basins and deepwater fields that consume significantly more OCTG per well than conventional vertical wells.

From a product perspective, casing accounts for the largest share of OCTG consumption, reflecting its use across surface, intermediate, and production strings in every well drilled. Premium connection variants are capturing a disproportionate share of growth as operators push into high-pressure, high-temperature reservoirs, sour-gas fields, and ultra-deepwater environments where API-grade connections are inadequate. Premium and semi-premium connections now represent approximately 31.4% of total OCTG revenue in 2025, up from 22% five years earlier, per API standards tracking data.

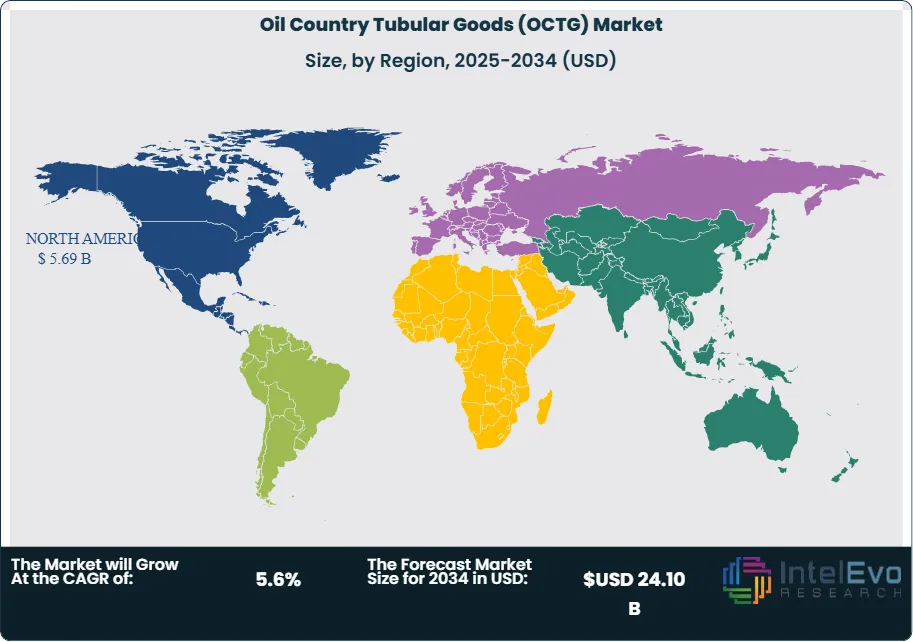

Geographically, North America commands 38.4% of global Oil Country Tubular Goods demand in 2025, with the Permian Basin alone accounting for over 200,000 active lateral feet per quarter. Middle East and Africa collectively hold 26.1% share, with Saudi Aramco, ADNOC, and Qatar Energy executing multi-year upstream expansion programs that require sustained OCTG volumes. Asia Pacific is the third-largest region at 19.3%, led by China National Petroleum Corporation's deepwater and unconventional push in the Sichuan Basin and the South China Sea.

On the supply side, the Oil Country Tubular Goods market features a moderately consolidated structure, with Tenaris, Vallourec, TMK Group, and Nippon Steel collectively accounting for approximately 54% of global capacity. Trade policy remains a significant variable: the United States maintains anti-dumping and countervailing duties on OCTG imports from South Korea, China, Turkey, India, and other jurisdictions under Commerce Department Section 201 and 232 frameworks, which have structurally supported domestic producers such as U.S. Steel and ArcelorMittal Tubular Products.

Digitalization is reshaping procurement and supply chain management in the OCTG sector. Real-time inventory tracking, AI-driven demand forecasting, and automated threading quality inspection are reducing lead times and rejection rates. Environmental considerations, including API 5CT-compliant low-emission manufacturing and recyclable steel grades, are gaining prominence as supermajors embed supply chain sustainability requirements into vendor qualification frameworks. These dynamics collectively position the Oil Country Tubular Goods market for steady, supply-constrained growth through 2034.

Market Size, Share, Growth & Industry Analysis By Product Type (Casing, Tubing, Drill Pipe, Line Pipe OCTG Grade, Accessories & Couplings), By Grade (API Grades J55, N80, L80, P110, Premium & Semi-Premium Connections, Corrosion-Resistant Alloys), By Application (Unconventional, Onshore, Offshore Deepwater & Shallow Water, Geothermal), By Well Type (Horizontal, Vertical, Directional) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global Oil Country Tubular Goods market was valued at USD 14.82 Billion in 2025 and is forecast to reach USD 24.10 Billion by 2034, at a CAGR of 5.6% during 2025–2034.

- Segment Dominance (By Product): Casing is the largest product segment, accounting for 48.2% of global OCTG revenue in 2025 (USD 7.14 Billion), driven by multi-string well architectures in shale and deepwater programs.

- Segment Dominance (By Application): Unconventional oil and gas drilling applications represent the leading end-use category at 42.6% share (2025), reflecting the sustained Permian Basin and Marcellus Shale drilling activity.

- Driver: Rising global upstream CAPEX, estimated at USD 580 Billion in 2025 by the IEA, is the primary growth driver, with a 9.4% year-on-year increase in active rig count across the Permian, GCC, and offshore Brazil corridors.

- Restraint: Trade policy volatility — including U.S. anti-dumping duties exceeding 100% on Chinese OCTG and 25% Section 232 tariffs on steel imports — raises input costs for domestic operators and compresses distributor margins by an estimated 4-6%.

- Opportunity: Middle East and Africa NOC-driven upstream expansion programs, collectively targeting USD 130 Billion in upstream CAPEX through 2030, represent the largest addressable growth opportunity for premium OCTG suppliers.

- Trend: Premium connection adoption is accelerating, reaching 31.4% of OCTG revenue in 2025, as operators target ultra-HP/HT wells exceeding 15,000 psi where API-grade connections are structurally inadequate.

- Regional Analysis: North America leads with 38.4% market share and USD 5.69 Billion in revenue in 2025, anchored by Permian Basin drilling density and robust U.S. domestic production programs.

Competitive Landscape

The Global Oil Country Tubular Goods market is moderately consolidated, with the top four producers — Tenaris, Vallourec, TMK Group, and Nippon Steel — collectively holding approximately 54% of global production capacity in 2025. Competition is technology-driven in the premium connection segment and price-driven in the commodity API-grade casing and tubing segment. U.S. trade protection measures have reinforced domestic producer positions, while NOC-aligned supply agreements in the Middle East favor suppliers with established in-country threading and inspection infrastructure. M&A activity has intensified since 2024, with Tenaris completing the IPSCO acquisition and ArcelorMittal committing USD 180 Million in facility upgrades.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Tenaris | Luxembourg | Leader | TenarisHydril Premium Connections | North America / Latin America | Acquired IPSCO Tubulars assets for USD 1.07B (Jan 2025) |

| Vallourec | France | Leader | VAM Premium OCTG Connections | Middle East / Europe | Launched VAM 21 ultra-HP connection for deepwater wells (Mar 2025) |

| TMK Group | Russia | Leader | TMK UP Series Premium Threads | Russia / CIS / MEA | Expanded Oman distribution hub capacity by 35% (Jun 2025) |

| U.S. Steel (USS/United States Steel) | USA | Challenger | Tubular Products Division — API Grade J55/N80 | North America | Signed 3-year supply agreement with ExxonMobil Permian Basin ops (Sep 2025) |

| Nippon Steel Corporation | Japan | Challenger | NS-CC Premium OCTG Casing | Asia Pacific / Middle East | Entered JV with ADNOC Drilling for UAE OCTG supply (Nov 2025) |

| ISMT Limited | India | Niche Player | Seamless OCTG — Chrome Grade | Asia Pacific / MEA | Commenced 120 KTPA seamless tube expansion at Baramati plant (Feb 2026) |

| Techint Group (TenarisSiderca) | Argentina | Challenger | SideRCa Sour-Service OCTG | Latin America / MEA | Received API 5CT certification for ultra-low temperature grade (Apr 2026) |

| ArcelorMittal Tubular Products | Luxembourg | Niche Player | AM Tubular API-grade ERW/seamless | Europe / North America | Invested USD 180M in ERW upgrades at Houston facility (Jan 2026) |

By Product Type

| Product Type | Market Share (2025) | Revenue (2025) |

| Casing | 48.2% | USD 7.14 Billion |

| Tubing | 27.6% | USD 4.09 Billion |

| Drill Pipe | 15.8% | USD 2.34 Billion |

| Line Pipe (OCTG Grade) | 5.4% | USD 0.80 Billion |

| Accessories & Couplings | 3.0% | USD 0.44 Billion |

Casing dominates the Oil Country Tubular Goods product mix, accounting for 48.2% of total revenue at USD 7.14 Billion in 2025. Its primacy reflects the multi-string architecture of modern wells, where surface casing, intermediate casing, production casing, and liner strings each require distinct grades and connection types. In unconventional plays such as the Permian Basin and Marcellus Shale, lateral lengths exceeding 15,000 feet demand large-diameter intermediate casing strings that consume substantial tonnage per well. High-chromium casing grades — including 13Cr and Super 13Cr — are capturing growing share in CO2-rich and sour-gas fields across the Middle East and Southeast Asia, supporting premium pricing. The casing segment is forecast to grow at 5.4% CAGR through 2034 as deepwater and HP/HT programs proliferate.

Tubing holds 27.6% share at USD 4.09 Billion in 2025. Production tubing carries reservoir fluids from the pay zone to surface and must withstand sustained well pressure, fluid corrosion, and mechanical wear from artificial lift equipment. As more wells employ electric submersible pumps and gas lift in mature fields, corrosion-resistant alloy (CRA) tubing demand is rising. CRA variants command 40-60% price premiums over carbon steel alternatives and are standard in sour-service applications compliant with NACE MR0175. The tubing sub-segment is particularly sensitive to workover and recompletion activity, which remains elevated as operators manage declining production curves in long-producing basins.

Drill pipe accounts for 15.8% of OCTG revenue at USD 2.34 Billion in 2025. Unlike casing and tubing, drill pipe is reusable across multiple well campaigns, which moderates per-well consumption. However, escalating well depths and horizontal drilling complexity — with directional wellbores exceeding 30,000 measured feet in some Permian operations — are accelerating drill string fatigue and replacement cycles. Premium drill pipe grades such as S-135 and Z-140 are gaining adoption as operators push into ultra-deep and extended-reach drilling programs. Demand for heavy-weight drill pipe (HWDP) is also rising in geologically complex formations.

Line pipe in OCTG grades and accessories collectively represent 8.4% of market revenue in 2025. API 5L PSL2 line pipe used in field gathering networks is included in the OCTG category by major operators tracking full well-to-pipeline OCTG spend. Couplings, thread protectors, and centralizers are high-margin accessory items that follow casing and tubing volumes closely.

By Grade

| Grade | Market Share (2025) | Revenue (2025) |

| API Grade (J55, N80, L80, P110) | 61.8% | USD 9.16 Billion |

| Premium / Semi-Premium Connection | 31.4% | USD 4.65 Billion |

| Corrosion-Resistant Alloy (CRA) | 6.8% | USD 1.01 Billion |

API-grade OCTG — covering the J55, N80, L80, and P110 yield-strength tiers defined under API Specification 5CT — represents the foundational product layer, holding 61.8% market share at USD 9.16 Billion in 2025. These grades are cost-effective workhorses for conventional and moderately demanding unconventional wells. API-grade product pricing is highly competitive and margin-thin, making volume and logistics efficiency the primary competitive levers for suppliers in this segment.

Premium and semi-premium connection OCTG captures 31.4% share at USD 4.65 Billion in 2025, up from approximately 22% in 2019. This structural shift reflects the proliferation of HP/HT wells, complex multi-lateral well architectures, and deepwater programs where metal-to-metal seal premium connections are specified by engineering design. Tenaris HydrilSeal, Vallourec VAM 21, and TMK UP series connections command 25-50% price premiums over API couplings and are increasingly standard on production and intermediate casing strings in the Middle East, North Sea, and Gulf of Mexico.

CRA-grade OCTG holds 6.8% share at USD 1.01 Billion in 2025. Duplex stainless steel, 13Cr, Super 13Cr, and Inconel-based alloys are standard in sour-service fields containing hydrogen sulfide concentrations that exceed SSC threshold limits per NACE MR0175. While CRA volumes are modest, per-tonne revenue is two to three times higher than carbon-steel alternatives, making this sub-segment disproportionately important for specialty manufacturers.

By Application

| Application | Market Share (2025) | Revenue (2025) |

| Unconventional (Shale/Tight Oil/Gas) | 42.6% | USD 6.31 Billion |

| Conventional Onshore | 27.4% | USD 4.06 Billion |

| Offshore Deepwater / Ultra-Deepwater | 18.8% | USD 2.79 Billion |

| Offshore Shallow Water | 8.2% | USD 1.21 Billion |

| Geothermal & Other | 3.0% | USD 0.44 Billion |

Unconventional applications — shale oil, tight gas, and coalbed methane — account for 42.6% of Oil Country Tubular Goods demand at USD 6.31 Billion in 2025. The Permian Basin, Marcellus/Utica, Eagle Ford, and Montney plays in North America are the core consumption centers. Each horizontal well in the Permian consumes an average of 450 tonnes of OCTG, compared to 120 tonnes for a conventional vertical well, making well count the primary volume driver. With the U.S. EIA projecting Permian crude output reaching 7.3 million bpd by 2026, unconventional OCTG demand retains structural upside through the forecast period.

Conventional onshore drilling holds 27.4% share at USD 4.06 Billion in 2025. This segment spans OPEC member fields in Saudi Arabia, Iraq, Kuwait, and UAE, as well as onshore programs in Kazakhstan, Algeria, and Libya. Saudi Aramco's Master Gas System expansion and ADNOC's Hail and Ghasha sour-gas megaprojects are driving sustained conventional OCTG procurement volumes in the GCC corridor.

Offshore deepwater and ultra-deepwater operations account for 18.8% of OCTG revenue at USD 2.79 Billion in 2025. Brazil's pre-salt Santos Basin, the Gulf of Mexico, and West Africa's deepwater blocks drive this segment. Ultra-deepwater wells in water depths exceeding 2,000 meters require premium connection casing strings with metal-to-metal seals and tight dimensional tolerances, commanding premium pricing. TotalEnergies, Petrobras, and Shell are among the largest deepwater OCTG buyers globally.

Regional Analysis

| Region | Share (2025) | Revenue (2025) | CAGR (2025–2034) |

| North America | 38.4% | USD 5.69 Billion | 5.2% |

| Middle East & Africa | 26.1% | USD 3.87 Billion | 6.4% |

| Asia Pacific | 19.3% | USD 2.86 Billion | 6.1% |

| Europe | 10.2% | USD 1.51 Billion | 3.9% |

| Latin America | 6.0% | USD 0.89 Billion | 5.8% |

North America

North America dominates the Oil Country Tubular Goods market with a 38.4% share and USD 5.69 Billion in revenue in 2025, growing at a 5.2% CAGR through 2034. The United States is the region's anchor, with the Permian Basin accounting for roughly 43% of all U.S. OCTG consumption. The Gulf of Mexico deepwater complex adds a premium-connection-heavy demand layer, with operators including BP, Shell, and Chevron executing multi-well development campaigns in the Wilcox and Norphlet formations. Canada's Montney and Duvernay tight-oil plays are sustaining OCTG demand in Western Canada, particularly for large-diameter casing used in extended-reach horizontal wells. Mexico's Pemex, though constrained by budget cycles, is gradually increasing onshore and shallow-water OCTG procurement under its 2025-2030 upstream recovery plan. U.S. anti-dumping and Section 232 tariff frameworks continue to support domestic OCTG producers, with import duties on Chinese OCTG exceeding 100% and South Korean material subject to quota-rate agreements. Domestic mill capacity utilization reached 76% in 2025, up from 68% in 2023, per AISC data.

Middle East & Africa

The Middle East and Africa hold 26.1% of global Oil Country Tubular Goods market share, contributing USD 3.87 Billion in revenue in 2025, with the highest regional CAGR at 6.4% through 2034. Saudi Arabia is the region's largest OCTG consumer, with Saudi Aramco procuring an estimated 600,000 tonnes annually to support Haradh, Khurais, and Marjan field expansions, as well as the Master Gas System Phase III. The UAE's ADNOC has committed USD 150 Billion in upstream CAPEX through 2030, with significant volumes directed to offshore and sour-gas programs requiring CRA and premium-grade OCTG. Qatar Energy's North Field expansion, the world's largest LNG project, demands high-chromium tubing and premium connections throughout its well construction program. In Africa, Nigeria's deepwater pre-salt discoveries and Mozambique's LNG megaprojects are driving offshore OCTG demand growth. The region benefits from established in-country threading facilities operated by Tenaris and TMK in the UAE and Oman, which reduce lead times for NOC procurement programs.

Asia Pacific

Asia Pacific accounts for 19.3% of global Oil Country Tubular Goods market share at USD 2.86 Billion in 2025, expanding at a 6.1% CAGR through 2034. China is the region's largest producer and consumer of OCTG, with CNPC and CNOOC executing aggressive offshore and unconventional campaigns in the Tarim Basin, South China Sea, and Sichuan shale formations. China's domestic OCTG manufacturers — including Tianjin Pipe Group and Baoshan Iron & Steel — are primary suppliers to Chinese NOC programs, with export flows constrained by U.S. and EU trade barriers. India represents the region's fastest-growing OCTG import market as ONGC and Oil India Limited scale up Krishna-Godavari deepwater exploration and Rajasthan tight-oil production. Japan's Nippon Steel is a globally significant premium OCTG supplier, exporting into the Middle East and Southeast Asian markets. Australia's Barossa and Scarborough offshore LNG projects sustain premium-connection demand in the South Pacific.

Europe

Europe holds 10.2% of global Oil Country Tubular Goods revenue at USD 1.51 Billion in 2025, growing at the slowest regional CAGR of 3.9% through 2034, reflecting declining North Sea production volumes and constrained new exploration licensing under EU energy transition policy. Norway remains the region's primary OCTG consumer, with Equinor's Johan Sverdrup Phase II and Wisting Arctic program driving premium casing and tubing demand. The UK continental shelf sees sustained workover and recompletion OCTG volumes as operators maintain aging fields. Romania's Neptun Deep Black Sea project, developed by OMV Petrom and Romgaz, is the region's most significant new deepwater OCTG demand source. Vallourec's French manufacturing base and its premium connection technology position it as the preferred European NOC supplier. EU decarbonization targets and offshore licensing pauses in several member states are structural headwinds limiting volume growth beyond the medium term.

Latin America

Latin America accounts for 6.0% of global Oil Country Tubular Goods revenue at USD 0.89 Billion in 2025, growing at a 5.8% CAGR through 2034. Brazil's pre-salt Santos Basin, operated by Petrobras and partners including Shell and TotalEnergies, is the region's dominant OCTG demand center. Ultra-deepwater FPSOs deployed at water depths exceeding 2,000 meters require metal-to-metal premium connection casing strings with fatigue-rated connections, commanding premium pricing. Argentina's Vaca Muerta shale play — one of the world's largest tight-oil formations outside North America — is driving unconventional OCTG demand, with YPF, Chevron, and Vista Oil executing multi-well pad drilling campaigns. Colombia's Llanos Basin and Ecuador's deepening Oriente production are additional regional demand contributors. Techint Group's TenarisSiderca facility in Campana, Argentina supplies Vaca Muerta operators with locally manufactured OCTG, reducing import dependency and lead times.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Casing

- Tubing

- Drill Pipe

- Line Pipe (OCTG Grade)

- Accessories and Couplings

By Grade

- API Grade (J55, N80, L80, P110)

- Premium / Semi-Premium Connection

- Corrosion-Resistant Alloy (CRA)

By Application

- Unconventional (Shale / Tight Oil / Gas)

- Conventional Onshore

- Offshore Deepwater / Ultra-Deepwater

- Offshore Shallow Water

- Geothermal and Other

By Well Type

- Horizontal

- Vertical

- Directional

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.82 B |

| Forecast Revenue (2034) | USD 24.10 B |

| CAGR (2025-2034) | 5.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Casing, Tubing, Drill Pipe, Line Pipe (OCTG Grade), Accessories and Couplings), By Grade, (API Grade (J55, N80, L80, P110), Premium / Semi-Premium Connection, Corrosion-Resistant Alloy (CRA)), By Application, (Unconventional (Shale / Tight Oil / Gas), Conventional Onshore, Offshore Deepwater / Ultra-Deepwater, Offshore Shallow Water, Geothermal and Other), By Well Type, (Horizontal, Vertical, Directional) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TENARIS, VALLOUREC, TMK GROUP, NIPPON STEEL CORPORATION, UNITED STATES STEEL CORPORATION (U.S. STEEL), ARCELORMITTAL TUBULAR PRODUCTS, ISMT LIMITED, TECHINT GROUP (TENARISIDERCA), TIANJIN PIPE GROUP (TPCO), BAOSHAN IRON & STEEL CO. (BAOSTEEL), JINDAL SAW LIMITED, HUNTING PLC, BENTELER INTERNATIONAL, FORUM ENERGY TECHNOLOGIES, TEXAS STEEL TECHNOLOGIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share, Growth & Industry Analysis By Product Type (Casing, Tubing, Drill Pipe, Line Pipe OCTG Grade, Accessories & Couplings), By Grade (API Grades J55, N80, L80, P110, Premium & Semi-Premium Connections, Corrosion-Resistant Alloys), By Application (Unconventional, Onshore, Offshore Deepwater & Shallow Water, Geothermal), By Well Type (Horizontal, Vertical, Directional) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Product Type (Casing, Tubing, Drill Pipe, Line Pipe OCTG Grade, Accessories & Couplings), By Grade (API Grades J55, N80, L80, P110, Premium & Semi-Premium Connections, Corrosion-Resistant Alloys), By Application (Unconventional, Onshore, Offshore Deepwater & Shallow Water, Geothermal), By Well Type (Horizontal, Vertical, Directional) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Product Type (Casing, Tubing, Drill Pipe, Line Pipe OCTG Grade, Accessories & Couplings), By Grade (API Grades J55, N80, L80, P110, Premium & Semi-Premium Connections, Corrosion-Resistant Alloys), By Application (Unconventional, Onshore, Offshore Deepwater & Shallow Water, Geothermal), By Well Type (Horizontal, Vertical, Directional) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oil Country Tubular Goods (OCTG) Market?

Global OCTG market valued at USD 14.04B in 2024, reaching USD 24.10B by 2034, growing at a CAGR of 5.6% from 2026–2034.

Who are the major players in the Oil Country Tubular Goods (OCTG) Market?

TENARIS, VALLOUREC, TMK GROUP, NIPPON STEEL CORPORATION, UNITED STATES STEEL CORPORATION (U.S. STEEL), ARCELORMITTAL TUBULAR PRODUCTS, ISMT LIMITED, TECHINT GROUP (TENARISIDERCA), TIANJIN PIPE GROUP (TPCO), BAOSHAN IRON & STEEL CO. (BAOSTEEL), JINDAL SAW LIMITED, HUNTING PLC, BENTELER INTERNATIONAL, FORUM ENERGY TECHNOLOGIES, TEXAS STEEL TECHNOLOGIES, Others

Which segments covered the Oil Country Tubular Goods (OCTG) Market?

By Product Type, (Casing, Tubing, Drill Pipe, Line Pipe (OCTG Grade), Accessories and Couplings), By Grade, (API Grade (J55, N80, L80, P110), Premium / Semi-Premium Connection, Corrosion-Resistant Alloy (CRA)), By Application, (Unconventional (Shale / Tight Oil / Gas), Conventional Onshore, Offshore Deepwater / Ultra-Deepwater, Offshore Shallow Water, Geothermal and Other), By Well Type, (Horizontal, Vertical, Directional)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oil Country Tubular Goods (OCTG) Market

Published Date : 30 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date