- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

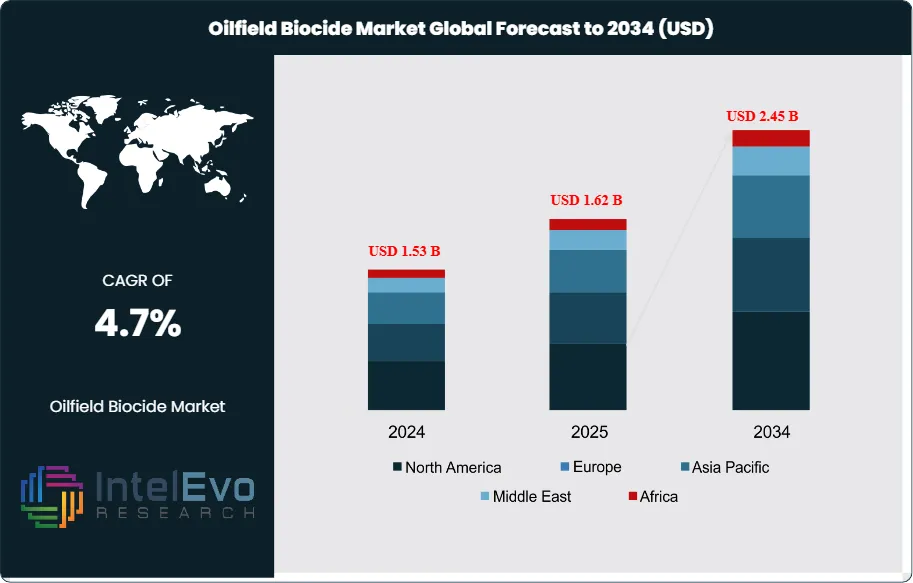

Global Oilfield Biocide Market Size, Share & Forecast 2034 | CAGR 4.7%

Global Oilfield Biocide Market Size, Share, Growth Analysis By Type (THPS, Glutaraldehyde, DBNPA, Other Biocides), By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline & Facility Preservation, Injection Water & Seawater Treatment), By Location (Onshore, Offshore), By Function, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

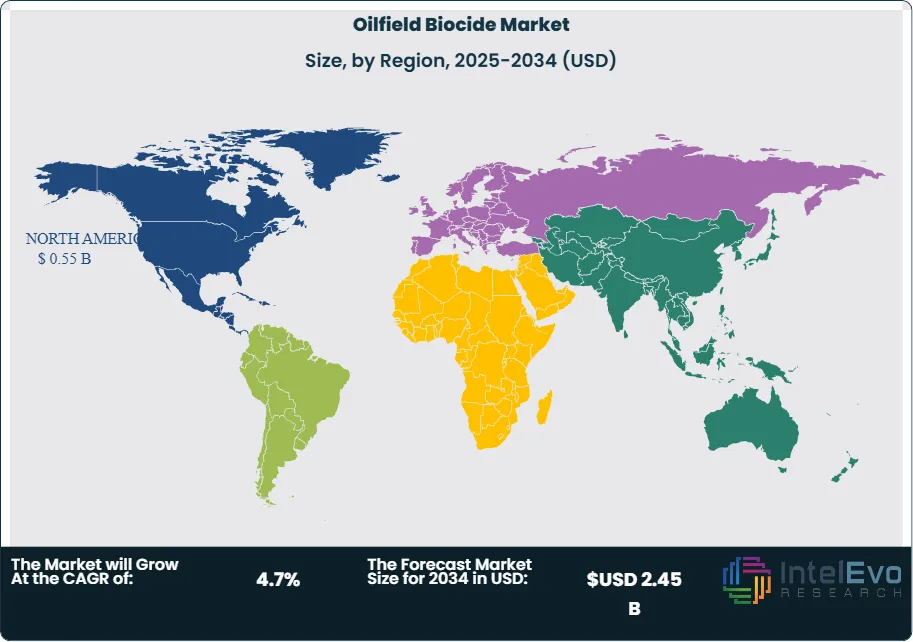

| USD 1.62 Billion | USD 2.45 Billion | 4.7% | North America, 34.0% |

The Oilfield Biocide Market was valued at approximately USD 1.53 Billion in 2024 and increased to USD 1.62 Billion in 2025. The market is projected to reach nearly USD 2.45 Billion by 2034, expanding at a compound annual growth rate (CAGR) of around 4.7% during the forecast period from 2026 to 2034. Market growth is primarily driven by the increasing need to control microbial contamination in oilfield operations, particularly in water injection systems, pipelines, and enhanced oil recovery processes. Additionally, rising offshore drilling activities and stricter environmental and safety regulations are further supporting the demand for advanced and environmentally compliant biocide solutions.

Get More Information about this report -

Request Free Sample ReportThe oilfield biocide market sits inside the broader oilfield chemicals chain and remains tied to microbial control in drilling fluids, completion fluids, injection water, and produced water treatment. This report models the 2025 market from active drilling intensity, water-handling volumes, offshore reinjection demand, and supplier positioning across production chemicals. The growth path is moderate rather than explosive because upstream oil investment is under pressure in 2025, yet field chemistry demand remains resilient in mature assets, high-water-cut wells, and sour service systems where microbial-induced corrosion and biofouling raise failure risk.

The oilfield biocide market is shaped by two opposing forces. Demand rises with water reuse, deeper offshore developments, and tighter asset-integrity targets. Demand softens when rig counts weaken or producers cut discretionary chemical dosages during low-price cycles. At the same time, the Middle East continues to support strong oil and gas capital flows, which underpins steady biocide demand in produced-water treatment, seawater injection systems, and flow assurance programs across the Gulf.

Supply remains moderately consolidated. ChampionX positions itself as a global leader in oilfield water treatment chemicals. SLB offers bacteria management and digital chemical-injection tools. Baker Hughes and Halliburton both pair production chemistry with wider completion and production service contracts. Nalco Water maintains a full line of hydrocarbon- and water-based biocides and broad water-treatment coverage. This vendor mix keeps price competition active, but competition is not purely price-led. Performance, local service, supply assurance, and digital dosage control now decide a larger share of contract awards.

Regulation also matters. Product authorization and antimicrobial oversight raise registration, testing, and documentation costs, especially for glutaraldehyde and phosphonium chemistries. These rules push suppliers toward lower-toxicity formulations, better dosing control, and digital monitoring. By 2025, North America leads with 34.0% of global oilfield biocide market revenue, while the Middle East & Africa posts the strongest long-horizon expansion profile because of offshore sour service, water injection, and high regional upstream spending.

, By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline & Facility Preservation, Injection Water & Seawater Treatment), By Location (Onshore, Offshore), By Function, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oilfield biocide market stands at USD 1.62 Billion in 2025 and is projected to reach USD 2.45 Billion by 2034. That implies a 4.7% CAGR across 2026–2034.

- Segment Dominance: By type, THPS-based biocides lead with 38.0% share in 2025, equal to about USD 0.62 Billion, supported by broad use in injection water and produced-water systems.

- Segment Dominance: By application, produced water treatment leads with 41.0% share in 2025, equal to about USD 0.66 Billion, because water recycling and reinjection keep microbial control in daily operating budgets.

- Driver: The main growth driver is asset-integrity protection. Continuous biocide application can reduce average corrosion rates by 35.0% to 77.0% in facility service, which directly lowers failure risk and supports chemical spend.

- Restraint: Regulatory compliance and toxicity management hold back faster growth. A 6.0% decline in upstream oil investment in 2025 limits chemical spending on lower-priority wells even when microbial risk persists.

- Opportunity: Digital injection control and water-system analytics create the biggest upside. The digital-linked service opportunity in the oilfield biocide market is projected to expand from about USD 0.18 Billion in 2025 to USD 0.39 Billion by 2034.

- Trend: The strongest trend is integration of biocides with remote monitoring and water-treatment programs. In 2025, an estimated 28.0% of global demand is tied to digitally monitored programs, and the share is set to exceed 45.0% by 2034.

- Regional Analysis: North America is the largest region with 34.0% share in 2025, equal to about USD 0.55 Billion, supported by shale water management, mature infrastructure, and high chemical intensity.

Competitive Landscape

The oilfield biocide market is moderately consolidated. The top four suppliers hold an estimated 48.0% of global revenue in 2025. Competition is technology-driven and service-led, not purely price-led, because dosage accuracy, local field support, water-treatment know-how, and chemical logistics all shape customer retention. Competitive intensity increased through 2025 as SLB completed its ChampionX acquisition, Baker Hughes secured a large multi-year chemicals award in Guyana, and Clariant expanded its European oil-services footprint with a new Norway supply base.

| Company | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| ChampionX | US | Leader | Water Solutions portfolio | North America, Middle East | Introduced ESP Production Optimization Services with remote chemical-injection visibility in Feb 2025 |

| Baker Hughes | US | Leader | Production Chemicals for topsides and water injection | Latin America, Middle East | Secured multi-year ExxonMobil Guyana chemicals award in Feb 2025 |

| SLB | US | Leader | Microbially Induced Corrosion Management and Delfi production chemistry tools | Global offshore, Middle East | Completed ChampionX acquisition in Jul 2025 |

| Halliburton | US | Leader | Production Chemicals and associated services | Middle East, North America | Sustained chemicals scale in key regions during 2025 international activity rebound |

| Ecolab Nalco Water | US | Challenger | Hydrocarbon- and water-based Biocides | North America, Europe | Expanded digital water-treatment positioning across 2025 |

| Clariant | Switzerland | Challenger | PRESERVAN hydrotest technologies and oil services chemistry | Europe, Middle East | Opened new Norway supply base with Swire Energy Services in Sep 2025 |

| BASF | Germany | Niche Player | OASE gas-treatment platform and specialty actives | Europe, Middle East | Continued gas-purification and sulfur-removal expansion across energy applications in 2025 |

| Solenis | US | Niche Player | Generox chlorine dioxide systems | Latin America, North America | Expanded water-treatment deployments and chemical-input reduction programs in 2025 |

| Solvay | Belgium | Niche Player | Specialty phosphonium chemistry inputs | Europe | Maintained specialty position in industrial and energy-related biocide intermediates |

| Dorf Ketal | India | Niche Player | Production and water-treatment chemicals | Middle East, India | Expanded regional manufacturing and application support in 2025 |

By Type

By type, the oilfield biocide market splits into THPS, glutaraldehyde, DBNPA, and other biocides. THPS leads with 38.0% share in 2025, or USD 0.62 Billion, because operators use it widely in produced water, injection water, and sulfide-control programs where phosphonium chemistry offers strong performance in high-throughput systems. Glutaraldehyde follows at 31.0%, or USD 0.50 Billion, and remains a core non-oxidizing biocide for broad-spectrum microbial control in drilling, completion, and production environments. DBNPA holds 17.0%, or USD 0.28 Billion, with strength in rapid kill applications and shorter residence-time systems. Other biocides, including chlorine dioxide, bronopol, quaternary blends, and oxidizing packages, account for 12.0%, or USD 0.19 Billion, while niche formulations make up the remaining 2.0%. Through 2034, the mix shifts modestly toward THPS and engineered blends as suppliers push lower-dosage and better-monitored programs.

By Application

By application, produced water treatment leads the oilfield biocide market with 41.0% share in 2025, equal to USD 0.66 Billion. That dominance reflects the steady need to control sulfate-reducing bacteria, slime formation, souring, and biofilm in recycled water, disposal lines, and reinjection networks. Drilling fluids account for 24.0%, or USD 0.39 Billion, because water-based muds and polymer systems remain vulnerable to bacterial degradation, especially in hot climates and long circulation cycles. Hydraulic fracturing fluids represent 18.0%, or USD 0.29 Billion, supported by shale water reuse and bacterial control in storage and blending systems. Pipeline and facility preservation, hydrotest, and midstream uses hold 11.0%, or USD 0.18 Billion, while injection water and seawater treatment represent the final 6.0%, or USD 0.10 Billion. The best near-term revenue pool remains produced water treatment because it is linked to operating continuity, not only new well counts.

By Location of Use

By location of use, onshore oilfields hold 63.0% share in 2025, or USD 1.02 Billion, because shale basins, mature land wells, tank batteries, and gathering systems consume high volumes of water-treatment and preservation chemicals. Offshore oilfields account for 37.0%, or USD 0.60 Billion, but offshore systems show higher chemical intensity per site because seawater injection, subsea tiebacks, long residence times, and platform utility systems need continuous monitoring and treatment. Recent offshore project awards in Brazil, Guyana, Norway, and the Gulf point to stable offshore demand even when land rig activity softens. Offshore projects also favor suppliers with integrated logistics, remote monitoring, and production chemistry expertise.

By Function

By function, microbial corrosion control is the largest use case with 36.0% share in 2025, or USD 0.58 Billion. This segment sits at the center of integrity programs because microbes drive pitting, under-deposit attack, and sulfide formation in pipelines and production equipment. Souring control and SRB management follow at 27.0%, or USD 0.44 Billion, reflecting high demand in produced-water systems and offshore injection loops. Biofilm and slime control hold 21.0%, or USD 0.34 Billion, especially in tanks, separators, and utility-water circuits. Fluid preservation and storage stability represent 10.0%, or USD 0.16 Billion, while other microbial-control functions account for 6.0%, or USD 0.10 Billion. Suppliers now market these functions through integrated chemistry-plus-monitoring packages rather than separate chemicals.

Regional Analysis

North America Oilfield Biocide Market Regional Analysis

North America held 34.0% of the oilfield biocide market in 2025, equal to USD 0.55 Billion. The United States drives about USD 0.44 Billion of the regional total, Canada contributes roughly USD 0.07 Billion, and Mexico adds about USD 0.04 Billion. The region leads because shale operations generate repeat demand for fracturing-fluid preservation, produced-water treatment, and microbial corrosion control in tanks, gathering lines, and disposal networks. The US market remains the anchor because unconventional basins consume large fluid volumes and increasingly recycle water. Canada benefits from thermal heavy-oil and oil sands infrastructure, where water handling and biofouling control support steady demand. Mexico is smaller, but offshore and onshore rehabilitation programs keep service demand active. Even with capital discipline, mature asset protection, water recycling, and integrity programs keep this region the largest revenue pool through the medium term.

Europe Oilfield Biocide Market Regional Analysis

Europe held 20.0% of the oilfield biocide market in 2025, equal to USD 0.32 Billion. Norway leads with about USD 0.09 Billion, the UK contributes USD 0.07 Billion, Germany accounts for USD 0.05 Billion, and France contributes USD 0.03 Billion, with the balance spread across other markets. Europe’s position rests on North Sea offshore production, mature infrastructure, strict chemical governance, and continued demand for preservation, hydrotest, and produced-water chemistry in aging assets. Europe is the most regulation-heavy regional market. That raises compliance costs and favors larger suppliers with stronger product documentation. Norway and the UK remain the high-value countries because offshore production systems need seawater treatment, bacterial control, and preservation programs. Europe grows below Asia Pacific and MEA on volume, but margins remain attractive because compliance and offshore service quality matter more than lowest price.

Asia Pacific Oilfield Biocide Market Regional Analysis

Asia Pacific held 21.0% of the oilfield biocide market in 2025, equal to USD 0.34 Billion. China leads with about USD 0.12 Billion, Australia contributes USD 0.07 Billion, India adds USD 0.06 Billion, and Indonesia contributes USD 0.04 Billion. Asia Pacific demand comes from offshore gas processing, mature onshore waterfloods, LNG-linked midstream assets, and increasing water-treatment complexity across older fields. China remains the largest country market because of broad upstream and gas-processing scale. Australia matters through offshore gas and high-spec integrity requirements. India is growing from a lower base as upstream redevelopment and water management improve. The region also shows strong adoption potential for digitally monitored chemical programs because remote sites and offshore platforms benefit from lower manual sampling frequency and tighter dosage control. Asia Pacific should post one of the fastest regional growth rates through 2034.

Latin America Oilfield Biocide Market Regional Analysis

Latin America held 11.0% of the oilfield biocide market in 2025, equal to USD 0.18 Billion. Brazil contributes around USD 0.08 Billion, Mexico USD 0.04 Billion, Argentina USD 0.03 Billion, and Colombia USD 0.01 Billion. Brazil dominates because deepwater projects need injection-water treatment, subsea preservation, and produced-water microbial control. Mexico remains important through offshore rehabilitation and onshore infrastructure. Argentina adds demand through shale developments, especially where water reuse expands. The region offers attractive long-cycle demand but remains exposed to political swings, local-content rules, and project timing delays. Regional suppliers that combine local stock points with production chemistry expertise tend to outperform because import delays can disrupt treatment continuity.

Middle East & Africa Oilfield Biocide Market Regional Analysis

Middle East & Africa held 14.0% of the oilfield biocide market in 2025, equal to USD 0.23 Billion. Saudi Arabia leads with about USD 0.08 Billion, the UAE contributes USD 0.04 Billion, South Africa about USD 0.01 Billion, and the rest comes from Oman, Qatar, Kuwait, Angola, and Nigeria. The region is smaller than North America today, but it holds the strongest strategic growth profile. Saudi Arabia and the UAE anchor regional demand because water injection, sour service, and large integrated production systems need constant microbial control. Oman remains important for field chemical service contracts. In Africa, Angola and Nigeria drive offshore demand, while Namibia can become more relevant as developments move ahead. The region favors suppliers with local manufacturing, blending, and field-service capabilities and should record the fastest CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- THPS

- Glutaraldehyde

- DBNPA

- Other Biocides

By Application

- Produced Water Treatment

- Drilling Fluids

- Hydraulic Fracturing Fluids

- Pipeline and Facility Preservation

- Injection Water and Seawater Treatment

By Location of Use

- Onshore

- Offshore

By Function

- Microbial Corrosion Control

- Souring Control and SRB Management

- Biofilm and Slime Control

- Fluid Preservation and Storage Stability

- Other Microbial Control Functions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.62 B |

| Forecast Revenue (2034) | USD 2.45 B |

| CAGR (2025-2034) | 4.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (THPS, Glutaraldehyde, DBNPA, Other Biocides), By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline and Facility Preservation, Injection Water and Seawater Treatment), By Location of Use (Onshore, Offshore), By Function (Microbial Corrosion Control, Souring Control and SRB Management, Biofilm and Slime Control, Fluid Preservation and Storage Stability, Other Microbial Control Functions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CHAMPIONX, BAKER HUGHES, SLB, HALLIBURTON, ECOLAB NALCO WATER, CLARIANT, BASF, SOLENIS, SOLVAY, DORF KETAL, KEMIRA, NOURYON, LUBRIZOL, SNF, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline & Facility Preservation, Injection Water & Seawater Treatment), By Location (Onshore, Offshore), By Function, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline & Facility Preservation, Injection Water & Seawater Treatment), By Location (Onshore, Offshore), By Function, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline & Facility Preservation, Injection Water & Seawater Treatment), By Location (Onshore, Offshore), By Function, Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oilfield Biocide Market?

The Global Oilfield Biocide Market was valued at USD 1.53 Billion in 2024 and USD 1.62 Billion in 2025, projected to reach USD 2.45 Billion by 2034, growing at a CAGR of 4.7% from 2026–2034, driven by rising demand for microbial control, EOR applications, and expanding offshore drilling activities.

Who are the major players in the Oilfield Biocide Market?

CHAMPIONX, BAKER HUGHES, SLB, HALLIBURTON, ECOLAB NALCO WATER, CLARIANT, BASF, SOLENIS, SOLVAY, DORF KETAL, KEMIRA, NOURYON, LUBRIZOL, SNF, Others

Which segments covered the Oilfield Biocide Market?

By Type (THPS, Glutaraldehyde, DBNPA, Other Biocides), By Application (Produced Water Treatment, Drilling Fluids, Hydraulic Fracturing Fluids, Pipeline and Facility Preservation, Injection Water and Seawater Treatment), By Location of Use (Onshore, Offshore), By Function (Microbial Corrosion Control, Souring Control and SRB Management, Biofilm and Slime Control, Fluid Preservation and Storage Stability, Other Microbial Control Functions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date