- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oilfield Data Analytics Market Size & Forecast 2034 | CAGR 11.3%

Global Oilfield Data Analytics Market Size, Share, Growth & Industry Analysis By Offering (Software, Services, Data & Analytics as a Service), By Application (Upstream Exploration & Production, Midstream Operations, Downstream Refining & Petrochemical), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End-User (Onshore Operations, Offshore Operations) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 4.8 Billion | USD 12.6 Billion | 11.3% | North America, 38.5% |

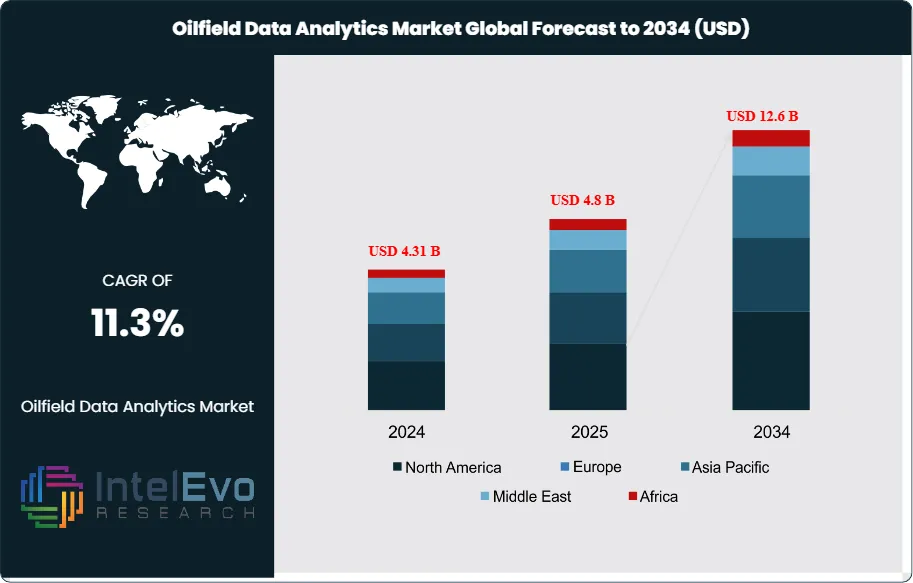

The Oilfield Data Analytics Market was valued at approximately USD 4.31 Billion in 2024 and reached USD 4.8 Billion in 2025. The market is projected to grow to USD 12.6 Billion by 2034, expanding at a CAGR of 11.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.8 billion over the analysis period. Oilfield data analytics encompasses software platforms, cloud-based solutions, and integrated services that transform raw drilling, production, and reservoir data into actionable operational intelligence. Upstream operators, midstream pipeline companies, and downstream refineries deploy these solutions to reduce lifting costs, predict equipment failures, and maximize hydrocarbon recovery rates across mature and frontier basins.

Get More Information about this report -

Request Free Sample ReportMarket demand is propelled by the oil and gas industry's accelerating digital transformation. Exploration and production companies face sustained pressure to lower breakeven costs per barrel while maintaining safe, compliant operations. Real-time analytics platforms ingest seismic, well log, and sensor telemetry data to enable predictive maintenance schedules that cut unplanned downtime by 15-20%. Artificial intelligence and machine learning models applied to reservoir simulation have shortened field development planning cycles from months to weeks. Major national oil companies and international operators alike have increased capital allocation toward digital oilfield initiatives. Saudi Aramco, ADNOC, and ExxonMobil each disclosed multi-year technology partnerships exceeding USD 500 million cumulatively by late 2025 to embed analytics across their asset portfolios.

Regulatory mandates further accelerate adoption. The U.S. Environmental Protection Agency finalized methane emissions reporting requirements in early 2025, compelling operators to deploy analytics-driven leak detection systems. The European Union's revised Emissions Trading System expanded coverage to include upstream oil and gas installations, incentivizing predictive flaring reduction. These compliance drivers dovetail with commercial imperatives: operators report 8-12% production uplifts from analytics-optimized artificial lift and well spacing decisions. Offshore deepwater projects in Brazil's pre-salt basins and the Gulf of Mexico depend on real-time flow assurance analytics to manage multiphase flow challenges and prevent hydrate formation.

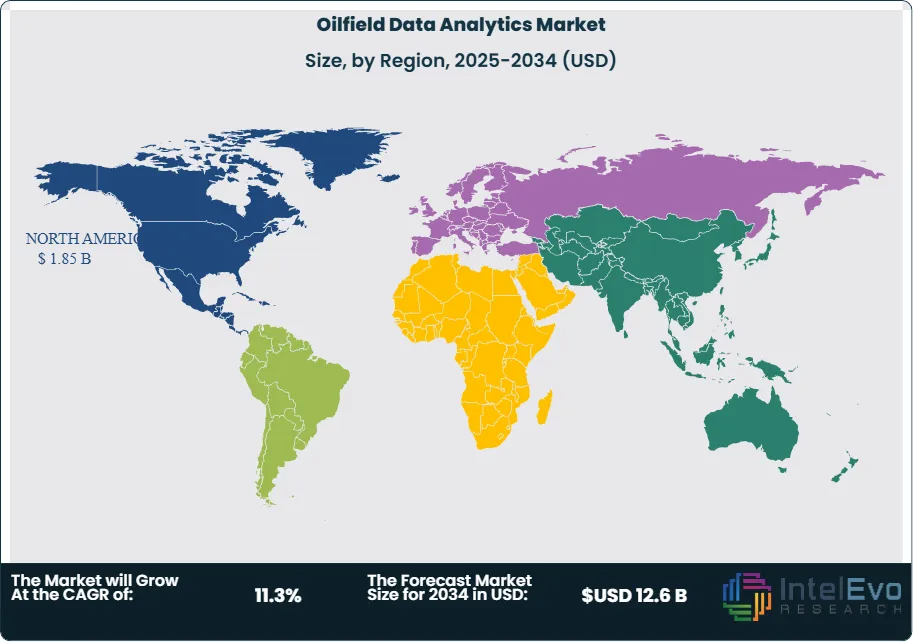

Regional adoption patterns vary by basin maturity and digital infrastructure. North America commands 38.5% of global revenue (USD 1.85 billion, 2025), led by Permian Basin operators integrating edge computing with cloud analytics. The Middle East and Africa region exhibits the fastest growth trajectory; ADNOC's AI-enabled reservoir management program and Saudi Arabia's Vision 2030 digitalization targets anchor investment pipelines. Europe's North Sea operators prioritize asset integrity analytics to extend field life amid decommissioning pressures. Asia Pacific operators in offshore Southeast Asia and onshore China deploy analytics to offset declining brownfield productivity. Latin America's Petrobras-led ecosystem invests in subsea sensor networks linked to predictive analytics dashboards.

Competitive intensity has increased through strategic acquisitions and technology alliances. SLB's 2025 acquisition of a leading AI analytics startup expanded its Delfi platform capabilities. Halliburton and Baker Hughes each launched upgraded cloud-native suites with enhanced visualization modules. Independent software vendors such as Emerson, Honeywell, and Kongsberg Digital compete on vertical integration and interoperability with legacy SCADA systems. Private equity funding into oilfield analytics startups exceeded USD 1.2 billion in 2024-2025, signaling continued market entry by specialized disruptors. The competitive landscape favors vendors offering flexible deployment models, from edge-deployed algorithms on drilling rigs to fully managed SaaS platforms accessible via standard web interfaces.

, By Application (Upstream Exploration & Production, Midstream Operations, Downstream Refining & Petrochemical), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End-User (Onshore Operations, Offshore Operations) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oilfield data analytics market will expand from USD 4.8 billion in 2025 to USD 12.6 billion by 2034, reflecting a CAGR of 11.3% across the nine-year forecast period.

- Segment Dominance: Software solutions held 52.3% market share in 2025, generating USD 2.51 billion in revenue as operators prioritized platform investments over one-time consulting engagements.

- Segment Dominance: Upstream exploration and production applications accounted for 61.8% of market revenue (USD 2.97 billion, 2025), driven by reservoir optimization and drilling performance analytics.

- Driver: Digital oilfield initiatives across major NOCs and IOCs accelerated spending by 18% year-over-year in 2025, with AI-enabled predictive maintenance reducing unplanned downtime by up to 20%.

- Restraint: Data integration complexity limits adoption; 43% of mid-sized operators cited siloed legacy systems as the primary barrier to enterprise-wide analytics deployment.

- Opportunity: Edge computing integration for remote offshore assets represents a USD 1.4 billion addressable opportunity through 2034 as latency-sensitive drilling automation expands.

- Trend: Cloud-native analytics adoption accelerated; 58% of new platform deployments in 2025 utilized public or hybrid cloud architectures versus 39% in 2023.

- Regional Analysis: North America led with 38.5% share and USD 1.85 billion revenue in 2025, supported by Permian Basin digital investments and Gulf of Mexico deepwater analytics programs.

Competitive Landscape Overview

The oilfield data analytics market exhibits moderate consolidation, with the top four players commanding approximately 47% combined market share in 2025. Competition centers on technology differentiation, particularly AI and machine learning algorithm sophistication, cloud deployment flexibility, and seamless integration with existing drilling and production control systems. Strategic M&A activity intensified; three acquisitions exceeding USD 300 million each closed between December 2024 and March 2026. Emerging analytics specialists continue to attract venture capital, pressuring incumbents to accelerate product roadmaps and expand partnership ecosystems with oilfield service contractors.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | Delfi Platform | North America | Acquired Gyrodata AI division for USD 420M (Feb 2025) |

| Halliburton | US | Leader | Landmark DecisionSpace 365 | North America | Launched real-time drilling optimizer module (Jan 2026) |

| Baker Hughes | US | Leader | Leucipa Platform | Middle East | Expanded ADNOC partnership to USD 850M (Dec 2024) |

| Emerson Electric | US | Leader | Plantweb Optics | Europe | Integrated AI engine into Plantweb suite (Mar 2025) |

| Honeywell | US | Challenger | Forge Enterprise | Asia Pacific | Won USD 180M Petronas analytics contract (Sep 2025) |

| Kongsberg Digital | Norway | Challenger | Kognitwin Energy | Europe | Deployed digital twin for Equinor Johan Sverdrup (Jun 2025) |

| Siemens Energy | Germany | Challenger | Opcenter APS | Europe | Signed five-year Wintershall Dea contract (Nov 2025) |

| C3.ai | US | Niche Player | C3 AI Reliability | North America | Expanded Shell partnership scope (Aug 2025) |

| Rockwell Automation | US | Niche Player | Plex Smart Manufacturing | North America | Launched oilfield-specific analytics package (Apr 2025) |

| Petrosys (Vela) | Australia | Niche Player | Petrosys PRO | Asia Pacific | Acquired by Vela Software for USD 95M (Oct 2025) |

Segmentation Analysis

Oilfield data analytics market segmentation reveals distinct adoption patterns across offering types, applications, deployment models, and end-user categories. Each segment exhibits unique growth drivers, competitive dynamics, and regional concentration that shape vendor strategies and investment priorities.

By Offering

Software solutions dominated the oilfield data analytics market with a 52.3% share generating USD 2.51 billion in 2025. Enterprise analytics platforms integrating reservoir modeling, drilling optimization, and production forecasting modules captured the largest software revenue segment. Operators prefer unified platforms that consolidate data streams from SCADA systems, IoT sensors, and legacy historians into single visualization dashboards. SLB's Delfi, Halliburton's DecisionSpace 365, and Baker Hughes' Leucipa compete directly for enterprise licenses, typically structured as multi-year subscriptions with annual recurring revenue models. Services contributed 31.4% (USD 1.51 billion, 2025) encompassing implementation consulting, data engineering, and managed analytics operations. Professional services demand spikes during digital transformation programs when operators lack in-house data science expertise. Managed services appeal to smaller independents seeking turnkey analytics without capital-intensive infrastructure investments. Data and analytics as a service accounted for 16.3% (USD 0.78 billion, 2025), reflecting growing preference for consumption-based pricing models that align costs with production output.

By Application

Upstream exploration and production applications commanded 61.8% market share (USD 2.97 billion, 2025) as operators prioritized reservoir characterization, drilling performance, and production optimization analytics. Reservoir simulation enhanced by machine learning algorithms shortens field development planning from eighteen months to under six months in mature basins. Drilling analytics reduce non-productive time by identifying bit wear patterns and optimizing weight-on-bit parameters in real time. Production optimization platforms apply artificial lift algorithms and well spacing models to maximize barrel output per CAPEX dollar invested. Midstream applications represented 23.7% (USD 1.14 billion, 2025), driven by pipeline integrity analytics, leak detection systems, and custody transfer measurement accuracy improvements. U.S. pipeline operators accelerated analytics investments following PHMSA's updated integrity management mandates. Downstream refinery and petrochemical applications accounted for 14.5% (USD 0.70 billion, 2025), leveraging process optimization analytics to improve yield, reduce energy consumption, and ensure regulatory compliance with emissions limits.

By Deployment Mode

Cloud-based deployment captured 49.2% market share (USD 2.36 billion, 2025) as operators embraced hybrid and public cloud architectures for scalability and reduced capital expenditure on data center infrastructure. Microsoft Azure and Amazon Web Services host the majority of oilfield analytics workloads, with Google Cloud gaining traction among data-intensive seismic processing users. On-premises deployment retained 32.6% share (USD 1.57 billion, 2025), favored by national oil companies with data sovereignty mandates and operators in jurisdictions with limited cloud infrastructure availability. Saudi Aramco, ADNOC, and Petrobras maintain significant on-premises analytics capacity despite parallel cloud pilot programs. Hybrid deployment accounted for 18.2% (USD 0.87 billion, 2025), enabling operators to process sensitive reservoir data locally while offloading compute-intensive training workloads to cloud environments.

By End-User

Onshore operations represented 58.4% of market revenue (USD 2.80 billion, 2025), driven by Permian Basin, Eagle Ford, and Bakken shale operators deploying analytics across thousands of producing wells. Pad drilling economics incentivize real-time analytics to coordinate simultaneous operations and minimize rig move time. Artificial lift optimization analytics yield 5-10% production gains on mature onshore wells through pump-off controller tuning and rod string fatigue prediction. Offshore operations accounted for 41.6% (USD 2.00 billion, 2025), with deepwater analytics investments concentrated in Brazil's pre-salt basins, the Gulf of Mexico, and offshore West Africa. Flow assurance analytics prevent hydrate blockages in subsea flowlines, while digital twin deployments monitor floating production storage and offloading vessel performance. Edge computing adoption accelerates offshore as latency requirements for drilling automation exceed satellite bandwidth constraints.

Regional Analysis

North America

North America commanded 38.5% of the oilfield data analytics market with USD 1.85 billion revenue in 2025. The United States dominates regional demand, contributing 89% of North American analytics spending driven by Permian Basin operators pursuing sub-USD 40 per barrel breakeven targets through data-driven drilling and completions optimization. Gulf of Mexico deepwater projects increasingly deploy digital twin analytics for floating production units, with Shell, Chevron, and BP leading adoption. Canada's Montney and Duvernay formations support analytics growth for multi-well pad operations and emissions monitoring compliance with federal methane regulations. Mexico's nascent private upstream sector represents an emerging opportunity following energy reform, though adoption remains limited by infrastructure gaps and regulatory uncertainty. U.S.-based vendors including SLB, Halliburton, Baker Hughes, and Emerson maintain headquarters advantages and dominate regional sales.

Europe

Europe accounted for 21.3% of global market share (USD 1.02 billion, 2025), anchored by North Sea operators prioritizing asset integrity analytics to extend field life beyond original decommissioning schedules. Norway's Equinor, the United Kingdom's BP and Shell, and the Netherlands' Shell operate mature offshore platforms where predictive maintenance analytics defer costly equipment replacements. Germany's Wintershall Dea and Austria's OMV deploy analytics for onshore operations in Argentina (through joint ventures) and North African concessions. European regulatory emphasis on emissions reduction accelerated adoption of flare gas recovery analytics and methane leak detection platforms. Kongsberg Digital and Siemens Energy compete effectively against U.S. incumbents through localized support and compliance expertise tailored to EU regulatory frameworks.

Asia Pacific

Asia Pacific held 19.8% market share (USD 0.95 billion, 2025), led by China National Petroleum Corporation (CNPC) and China National Offshore Oil Corporation (CNOOC) analytics investments across mature onshore basins and South China Sea developments. India's Oil and Natural Gas Corporation deploys analytics for aging Mumbai High and Krishna-Godavari basin assets, targeting 3-5% production decline mitigation. Southeast Asian operators including Malaysia's Petronas, Indonesia's Pertamina, and Thailand's PTTEP accelerate offshore analytics to counter natural decline rates in legacy fields. Australia's Santos and Woodside apply LNG plant analytics to optimize train efficiency and spot cargo scheduling. Japanese trading houses invest in analytics platforms for overseas equity oil and gas positions. Regional growth outpaces global averages as national oil companies embrace digitalization to offset declining brownfield productivity.

Latin America

Latin America represented 11.2% of global revenue (USD 0.54 billion, 2025), dominated by Brazil's Petrobras pre-salt analytics programs. Subsea sensor networks transmit real-time flow assurance data from ultra-deepwater wells to onshore analytics centers in Rio de Janeiro. Petrobras' 2025 strategic plan allocated USD 1.8 billion for digital technologies including predictive maintenance and reservoir simulation. Argentina's Vaca Muerta shale formation attracts analytics investment from YPF and international partners including Shell and Chevron, deploying completion optimization algorithms adapted from Permian Basin experience. Colombia's Ecopetrol and Ecuador's state operators represent smaller but growing analytics markets targeting mature field revitalization. Mexico's PEMEX faces budget constraints limiting analytics adoption despite significant reservoir optimization potential across legacy fields.

Middle East and Africa

The Middle East and Africa region captured 9.2% market share (USD 0.44 billion, 2025) but exhibits the fastest growth trajectory driven by ambitious national digitalization programs. Saudi Aramco's AI and advanced analytics center of excellence targets 2-3% production efficiency gains across its 12 million barrel-per-day capacity. ADNOC's partnership with Baker Hughes and IBM deployed AI-powered reservoir management across Abu Dhabi's major fields. Qatar Energy invests in LNG plant analytics for North Field expansion capacity additions. Kuwait Oil Company and Iraq's national operators represent emerging analytics opportunities, though security and infrastructure challenges temper near-term adoption rates. Sub-Saharan Africa's analytics market concentrates on offshore Nigeria and Angola, where TotalEnergies, Shell, and Eni deploy predictive maintenance platforms for floating production units.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software

- Services

- Data and Analytics as a Service

By Application

- Upstream Exploration and Production

- Midstream Operations

- Downstream Refining and Petrochemical

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By End-User

- Onshore Operations

- Offshore Operations

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.8 B |

| Forecast Revenue (2034) | USD 12.6 B |

| CAGR (2025-2034) | 11.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software; Services; Data and Analytics as a Service), By Application, (Upstream Exploration and Production; Midstream Operations; Downstream Refining and Petrochemical), By Deployment Mode, (Cloud-Based; On-Premises; Hybrid), By End-User, (Onshore Operations; Offshore Operations) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, EMERSON ELECTRIC, HONEYWELL INTERNATIONAL, KONGSBERG DIGITAL, SIEMENS ENERGY, C3.AI, ROCKWELL AUTOMATION, PETROSYS (VELA SOFTWARE), ASPENTECH, AVEVA, QUORUM SOFTWARE, INFORMATICA, TIBCO SOFTWARE, DATAWATCH (ALTAIR), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Upstream Exploration & Production, Midstream Operations, Downstream Refining & Petrochemical), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End-User (Onshore Operations, Offshore Operations) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

, By Application (Upstream Exploration & Production, Midstream Operations, Downstream Refining & Petrochemical), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End-User (Onshore Operations, Offshore Operations) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

, By Application (Upstream Exploration & Production, Midstream Operations, Downstream Refining & Petrochemical), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End-User (Onshore Operations, Offshore Operations) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oilfield Data Analytics Market?

Global Oilfield data analytics market valued at USD 4.31B in 2024, reaching USD 12.6B by 2034, growing at a CAGR of 11.3% from 2026–2034.

Who are the major players in the Oilfield Data Analytics Market?

SLB, HALLIBURTON, BAKER HUGHES, EMERSON ELECTRIC, HONEYWELL INTERNATIONAL, KONGSBERG DIGITAL, SIEMENS ENERGY, C3.AI, ROCKWELL AUTOMATION, PETROSYS (VELA SOFTWARE), ASPENTECH, AVEVA, QUORUM SOFTWARE, INFORMATICA, TIBCO SOFTWARE, DATAWATCH (ALTAIR), Others

Which segments covered the Oilfield Data Analytics Market?

By Offering, (Software; Services; Data and Analytics as a Service), By Application, (Upstream Exploration and Production; Midstream Operations; Downstream Refining and Petrochemical), By Deployment Mode, (Cloud-Based; On-Premises; Hybrid), By End-User, (Onshore Operations; Offshore Operations)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oilfield Data Analytics Market

Published Date : 01 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date