- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oilfield Equipment Rental Market Forecast 2034 | CAGR 6.3%

Global Oilfield Equipment Rental Market Size, Share, Growth & Industry Analysis By Equipment Type (Drilling Equipment, Pressure Control Equipment, Well Intervention Equipment, Production Equipment, Fishing & Abandonment Tools), By Application (Onshore, Offshore), By End-User (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 11.8 Billion | USD 20.5 Billion | 6.3% | North America, 34.2% |

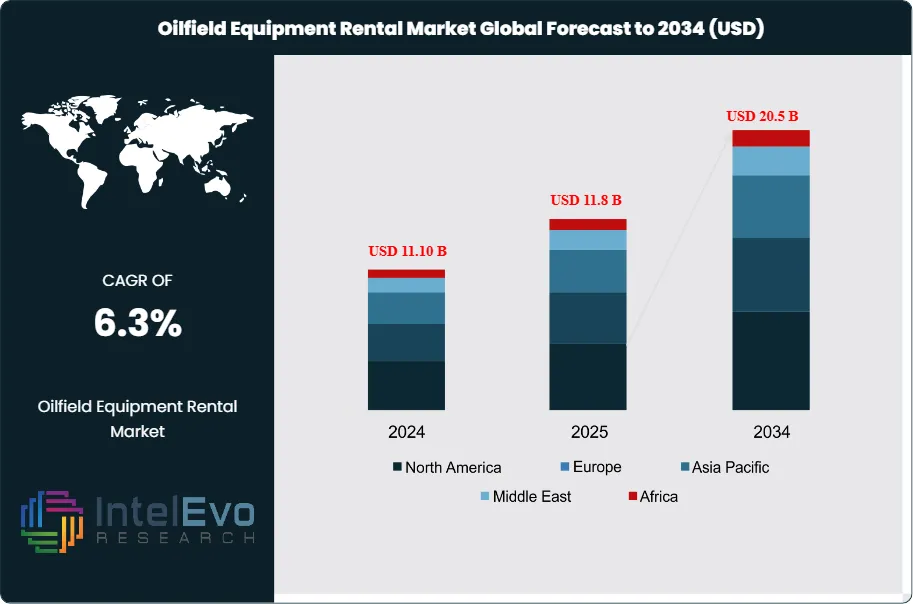

The Oilfield Equipment Rental Market was valued at approximately USD 11.10 Billion in 2024 and reached USD 11.8 Billion in 2025. The market is projected to grow to USD 20.5 Billion by 2034, expanding at a CAGR of 6.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.7 Billion over the analysis period. The oilfield equipment rental sector provides exploration and production companies with access to drilling rigs, pressure control equipment, well intervention tools, and production hardware without the capital burden of outright purchase. Operators increasingly prefer rental models to preserve balance sheet flexibility amid volatile crude prices and tightening capital discipline mandates from investors.

Get More Information about this report -

Request Free Sample ReportUpstream activity recovery following the 2020 downturn has reignited demand for rental fleets across all major basins. North America remains the largest revenue contributor at USD 4.0 Billion (2025), driven by the Permian Basin, Eagle Ford, and Montney unconventional plays where rig mobilization speed and equipment availability dictate project economics. The Middle East holds the second largest share at 22.8%, with national oil companies in Saudi Arabia, the UAE, and Iraq accelerating capacity expansion programs under long-term field development contracts. Asia Pacific accounts for 19.3% of the market, supported by offshore drilling campaigns in Malaysia, Indonesia, and deepwater exploration blocks in India.

Technological advancements in pressure control and well intervention equipment are reshaping rental portfolios. Blowout preventer stacks with real-time condition monitoring sensors command premium day rates as operators seek to minimize non-productive time. Coiled tubing units, hydraulic workover rigs, and wireline equipment remain core rental categories, collectively representing 42% of total rental revenue in 2025. Environmental regulations, particularly methane emission controls under EPA and BSEE guidelines, are compelling operators to deploy emission-compliant rental equipment rather than retrofit legacy assets.

Capital discipline remains a structural driver. Exploration and production companies subject to shareholder pressure are targeting a 15–20% reduction in owned equipment fleets by 2028, accelerating migration to rental and lease models. Integrated rental contracts bundling equipment, maintenance, and logistics support now account for 28% of market value, reflecting operator preference for turnkey solutions that transfer operational risk to service providers. The oilfield equipment rental market will continue expanding as drilling activity normalizes and operators prioritize flexibility over ownership.

, By Application (Onshore, Offshore), By End-User (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The oilfield equipment rental market is projected to grow from USD 11.8 Billion in 2025 to USD 20.5 Billion by 2034, registering a CAGR of 6.3% during the forecast period.

- Segment Dominance (Equipment Type): Drilling equipment rentals lead the market with a 38.5% share in 2025, driven by high rig utilization rates and operator preference for rental rigs in unconventional basins.

- Segment Dominance (Application): Onshore applications dominate with a 68.2% market share in 2025, reflecting the concentration of rental activity in shale plays and mature onshore fields.

- Driver: Capital discipline mandates from investors have increased rental adoption by 22% since 2022, as operators redirect CAPEX from equipment ownership to production activities.

- Restraint: Equipment supply chain constraints and lead times exceeding 18 months for critical components such as BOPs limit fleet expansion for rental companies.

- Opportunity: Digital rental platforms enabling real-time equipment tracking and utilization analytics represent a USD 1.2 Billion addressable market by 2030.

- Trend: Integrated rental contracts combining equipment, maintenance, and logistics grew from 18% of market value in 2020 to 28% in 2025, signaling operator preference for turnkey solutions.

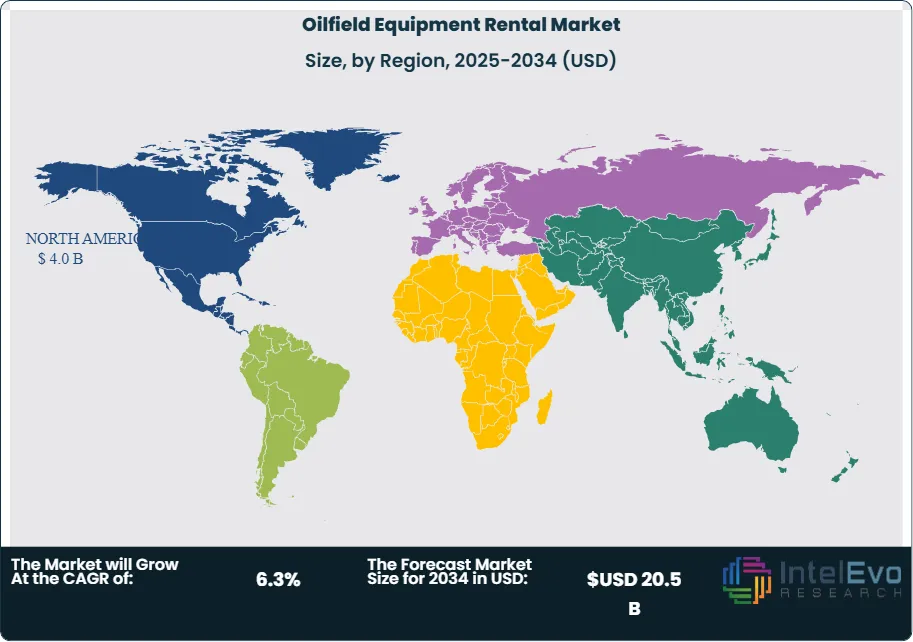

- Regional Analysis: North America leads the market with a 34.2% share, equivalent to USD 4.0 Billion in 2025, supported by sustained unconventional drilling activity in the Permian Basin.

Competitive Landscape Overview

The oilfield equipment rental market exhibits moderate consolidation, with the top four players commanding approximately 38% of global revenue in 2025. Competition is technology-driven in premium segments such as pressure control and well intervention, while price competition dominates standardized drilling tool rentals. Recent consolidation activity includes multiple strategic acquisitions aimed at expanding geographic coverage and fleet capacity. New market entrants from adjacent sectors, including industrial equipment rental companies, have increased competitive intensity in North American onshore markets.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | OneSubsea Rental Services | Global | Acquired Aker subsea rental portfolio for USD 1.4B (Feb 2025) |

| Baker Hughes | US | Leader | Oilfield Services Equipment | North America | Launched AI-driven equipment monitoring (Jan 2025) |

| Halliburton | US | Leader | Completion Tools Rental | Americas | Expanded Permian fleet by 800 units (Mar 2025) |

| NOV Inc. | US | Leader | Rig Components Rental | Global | Opened Middle East rental hub in Abu Dhabi (Dec 2024) |

| Weatherford | US | Challenger | Tubular Running Services | Middle East | Signed USD 320M Saudi Aramco rental contract (Apr 2025) |

| Superior Energy | US | Challenger | Well Services Rental | North America | Merged with Complete Production (Jun 2025) |

| Tesco Corporation | Canada | Niche | Top Drive Systems | North America | Introduced next-gen casing drive rental (Sep 2025) |

| Hunting PLC | UK | Niche | OCTG and Connections | Europe | Acquired North Sea rental specialist (Nov 2025) |

| NESR | UAE | Challenger | Production Services | MENA | Secured USD 180M ADNOC framework agreement (Jan 2026) |

| Odfjell Drilling | Norway | Niche | Offshore Rig Rental | North Sea | Deployed two ultra-deepwater rigs to Brazil (Feb 2026) |

Segmentation Analysis

The oilfield equipment rental market segments by equipment type into drilling equipment, pressure control equipment, well intervention equipment, production equipment, and fishing and abandonment tools. Each category addresses distinct operational requirements across the exploration and production lifecycle. Drilling equipment encompasses rental rigs, top drives, mud pumps, and rotary equipment. Pressure control covers blowout preventers, wellheads, and choke manifolds. Well intervention includes coiled tubing, wireline units, and hydraulic workover systems. Production equipment spans separators, heaters, and artificial lift components. Fishing tools address downhole recovery operations.

By Equipment Type

Drilling equipment rentals command the largest market share at 38.5%, generating USD 4.5 Billion in 2025. Rental rigs remain the highest-revenue category, with day rates for land rigs in North America averaging USD 22,000–28,000 depending on depth capacity and automation level. Top drive rental demand has surged as operators retrofit older rigs with modern power systems, avoiding USD 2–3 million capital outlays for outright purchase. Mud pumps and rotary tables round out the drilling rental portfolio, with utilization rates exceeding 78% across major shale basins.

Pressure control equipment holds a 24.2% market share, equivalent to USD 2.9 Billion in 2025. Blowout preventer stacks represent the most critical rental category, with operators increasingly specifying units equipped with real-time monitoring and predictive maintenance sensors. Following the Macondo incident, regulatory scrutiny from BSEE has intensified BOP inspection and certification requirements, favoring rental models that transfer compliance burden to equipment providers. Wellheads and choke manifolds account for the balance of pressure control rentals, with standardized API configurations dominating onshore applications.

Well intervention equipment captures 20.8% of market value at USD 2.5 Billion in 2025. Coiled tubing units remain essential for wellbore cleanout, nitrogen lifting, and stimulation operations across mature fields. Hydraulic workover rigs, capable of servicing wells under live pressure, command premium rental rates as operators prioritize safety and minimize well control risks. Wireline equipment, including slickline and electric line units, supports logging, perforation, and mechanical intervention activities throughout the well lifecycle.

Production equipment rentals account for 11.3% of the market, generating USD 1.3 Billion in 2025. Operators deploying early production facilities increasingly rely on rental separators, heaters, and flare systems to monetize discoveries before permanent infrastructure construction. Artificial lift equipment, including rod pumps, progressive cavity pumps, and gas lift mandrels, supports production optimization in declining fields where capital investment returns are marginal. Rental models allow operators to match equipment capacity to evolving reservoir performance.

Fishing and abandonment tools represent 5.2% of market value at USD 0.6 Billion in 2025. Downhole recovery operations require specialized rental equipment including overshots, milling tools, and fishing jars. Plug and abandonment activity is accelerating across mature basins as regulatory deadlines approach in the North Sea and Gulf of Mexico, driving demand for rental cement retainers, bridge plugs, and section milling assemblies.

By Application

Onshore applications dominate the oilfield equipment rental market with a 68.2% share, reflecting concentrated activity in unconventional basins where well counts and equipment turnover rates exceed offshore operations. The Permian Basin alone accounts for approximately 18% of global onshore rental demand, with operators drilling 400–500 wells per month at peak activity. Equipment logistics, including rapid rig-up and rig-down cycles, favor rental models that provide immediate availability without long-term capital commitment. Midstream rental equipment supporting gathering systems and early production adds incremental demand in prolific shale plays.

Offshore applications hold a 31.8% market share, equivalent to USD 3.8 Billion in 2025. Deepwater and ultra-deepwater operations in Brazil, West Africa, and the Gulf of Mexico require specialized rental equipment rated for high-pressure, high-temperature environments. Subsea intervention equipment, including riserless well intervention vessels and ROV-deployed tooling, commands premium rental rates given limited global availability. Floating production storage and offloading (FPSO) projects increasingly incorporate rental production equipment during ramp-up phases before permanent systems commission.

By End User

Independent exploration and production companies represent the largest end-user segment at 45.3% of market value. Capital-constrained independents rely heavily on rental models to preserve liquidity and maintain operational flexibility. Private equity-backed operators, facing defined investment horizons, favor rental over ownership to facilitate exit strategies and portfolio divestitures. Integrated majors account for 32.1% of rental demand, increasingly outsourcing non-core equipment categories to rental providers while concentrating capital on strategic assets.

National oil companies contribute 18.4% of rental market value, with Saudi Aramco, ADNOC, and Petrobras operating large-scale rental programs to support capacity expansion and field development initiatives. NOC rental demand correlates with production target mandates and government infrastructure spending. Drilling contractors hold the remaining 4.2% share, renting supplementary equipment to augment rig fleets during peak demand periods or to meet specific contract specifications.

Regional Analysis

North America

North America leads the oilfield equipment rental market with a 34.2% share, generating USD 4.0 Billion in 2025. The United States accounts for 88% of regional revenue, with the Permian Basin, Eagle Ford, and Bakken formations driving sustained rental demand. Active rig counts averaging 580–620 land rigs throughout 2025 translate directly into drilling equipment utilization. Canada contributes USD 0.4 Billion, concentrated in the Montney and Duvernay unconventional plays where seasonal drilling windows compress equipment deployment cycles.

Pressure control equipment rentals in North America benefit from stringent PHMSA and BSEE compliance requirements that favor certified rental fleets over aging owned equipment. Well intervention activity across the region's 500,000+ producing wells supports coiled tubing and wireline rental demand. Mexico's upstream liberalization has expanded rental market access, with international operators seeking rental solutions to navigate Pemex operational complexities. Digital fleet management platforms enabling real-time equipment tracking have achieved 45% adoption among North American rental providers.

Europe

Europe holds a 14.5% market share at USD 1.7 Billion in 2025, anchored by North Sea operations and emerging activity in the Mediterranean. The United Kingdom contributes USD 0.7 Billion, supported by platform drilling campaigns on mature fields and decommissioning programs requiring specialized abandonment equipment. Norway accounts for USD 0.5 Billion, with Johan Sverdrup and Troll field developments sustaining drilling equipment demand through 2030.

Regulatory emphasis on emissions reduction has accelerated adoption of low-emission rental equipment across European operations. Operators facing Scope 1 and Scope 2 reporting requirements under EU taxonomy regulations increasingly specify rental equipment meeting Euro Stage V emission standards. Decommissioning activity in the North Sea, with over 200 platforms scheduled for removal by 2035, creates substantial demand for well abandonment tools and subsea intervention equipment. Germany and the Netherlands contribute incremental rental revenue from onshore gas production and storage operations.

Asia Pacific

Asia Pacific accounts for 19.3% of the oilfield equipment rental market, generating USD 2.3 Billion in 2025. China leads regional demand at USD 0.8 Billion, with CNPC, Sinopec, and CNOOC operating extensive rental programs to support both onshore tight gas development and offshore South China Sea exploration. India contributes USD 0.4 Billion, driven by ONGC deepwater campaigns in the Krishna-Godavari Basin and Reliance Industries' production optimization initiatives.

Southeast Asian offshore activity in Malaysia, Indonesia, and Vietnam sustains drilling and well intervention rental demand, with Petronas and Pertamina executing multi-year field development programs. Australia's Bass Strait and Browse Basin operations require specialized subsea rental equipment for high-temperature reservoirs. The region's fragmented regulatory environment complicates cross-border equipment deployment, favoring local rental operators with established customs and certification processes. Japan and South Korea contribute modest demand from refinery turnaround projects and limited upstream activity.

Middle East and Africa

The Middle East and Africa region holds a 22.8% market share, equivalent to USD 2.7 Billion in 2025. Saudi Arabia dominates at USD 1.1 Billion, with Saudi Aramco's capacity expansion from 12 to 13 million barrels per day requiring substantial drilling and completion equipment rental. The UAE contributes USD 0.6 Billion, concentrated on ADNOC's offshore and unconventional development programs. Iraq's rehabilitation of southern oil fields drives rental demand at USD 0.3 Billion.

African rental markets, while smaller, exhibit strong growth trajectories. Nigeria generates USD 0.3 Billion from deepwater and marginal field developments. Angola's pre-salt blocks and Mozambique's LNG-linked drilling programs contribute incremental demand. The region's reliance on long-term framework agreements with major service companies shapes competitive dynamics, with local content requirements in several countries compelling international rental providers to establish in-country fleets and service capabilities.

Latin America

Latin America accounts for 9.2% of the oilfield equipment rental market at USD 1.1 Billion in 2025. Brazil leads the region at USD 0.6 Billion, driven by Petrobras and international operators drilling ultra-deepwater pre-salt wells in the Santos and Campos Basins. Floating rig demand in Brazil requires specialized rental equipment for HPHT applications, with BOP and subsea intervention equipment commanding premium rates.

Argentina contributes USD 0.2 Billion, with Vaca Muerta shale development accelerating following investment reforms. The basin's geological complexity, including overpressured zones, necessitates rental pressure control equipment meeting stringent safety standards. Colombia and Ecuador add incremental demand from conventional field developments and mature basin rehabilitation. Regional currency volatility and local content mandates influence equipment sourcing decisions, with operators balancing rental cost optimization against regulatory compliance.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Equipment Type

- Drilling Equipment

- Pressure Control Equipment

- Well Intervention Equipment

- Production Equipment

- Fishing and Abandonment Tools

By Application

- Onshore

- Offshore

By End User

- Independent E&P Companies

- Integrated Oil Companies

- National Oil Companies

- Drilling Contractors

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 11.8 B |

| Forecast Revenue (2034) | USD 20.5 B |

| CAGR (2025-2034) | 6.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment Type, (Drilling Equipment, Pressure Control Equipment, Well Intervention Equipment, Production Equipment, Fishing and Abandonment Tools), By Application, (Onshore, Offshore), By End User, (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, BAKER HUGHES, HALLIBURTON, NOV INC., WEATHERFORD INTERNATIONAL, SUPERIOR ENERGY SERVICES, TESCO CORPORATION, HUNTING PLC, NATIONAL ENERGY SERVICES REUNITED (NESR), ODFJELL DRILLING, EXPRO GROUP, WELLBORE INTEGRITY SOLUTIONS, WELLHUNT GROUP, KEY ENERGY SERVICES, BASIC ENERGY SERVICES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Onshore, Offshore), By End-User (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Application (Onshore, Offshore), By End-User (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

, By Application (Onshore, Offshore), By End-User (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors) Industry Trends, Competitive Landscape, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oilfield Equipment Rental Market?

Global Oilfield equipment rental market valued at USD 11.10B in 2024, reaching USD 20.5B by 2034, growing at a CAGR of 6.3% from 2026–2034.

Who are the major players in the Oilfield Equipment Rental Market?

SLB, BAKER HUGHES, HALLIBURTON, NOV INC., WEATHERFORD INTERNATIONAL, SUPERIOR ENERGY SERVICES, TESCO CORPORATION, HUNTING PLC, NATIONAL ENERGY SERVICES REUNITED (NESR), ODFJELL DRILLING, EXPRO GROUP, WELLBORE INTEGRITY SOLUTIONS, WELLHUNT GROUP, KEY ENERGY SERVICES, BASIC ENERGY SERVICES, Others

Which segments covered the Oilfield Equipment Rental Market?

By Equipment Type, (Drilling Equipment, Pressure Control Equipment, Well Intervention Equipment, Production Equipment, Fishing and Abandonment Tools), By Application, (Onshore, Offshore), By End User, (Independent E&P Companies, Integrated Oil Companies, National Oil Companies, Drilling Contractors)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oilfield Equipment Rental Market

Published Date : 07 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date