- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Oilfield Surfactant Market Size, Share, Growth & Forecast | CAGR 4.6%

Global Oilfield Surfactant Market Size, Share, Industry Analysis By Product Type (Non-ionic Surfactants, Anionic Surfactants, Cationic Surfactants, Amphoteric Surfactants, Bio-based Surfactants), By Application (Enhanced Oil Recovery, Production Chemicals & Flow Assurance, Drilling Fluids, Stimulation & Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Key Players, Strategic Developments, Technology Innovations, Growth Drivers & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

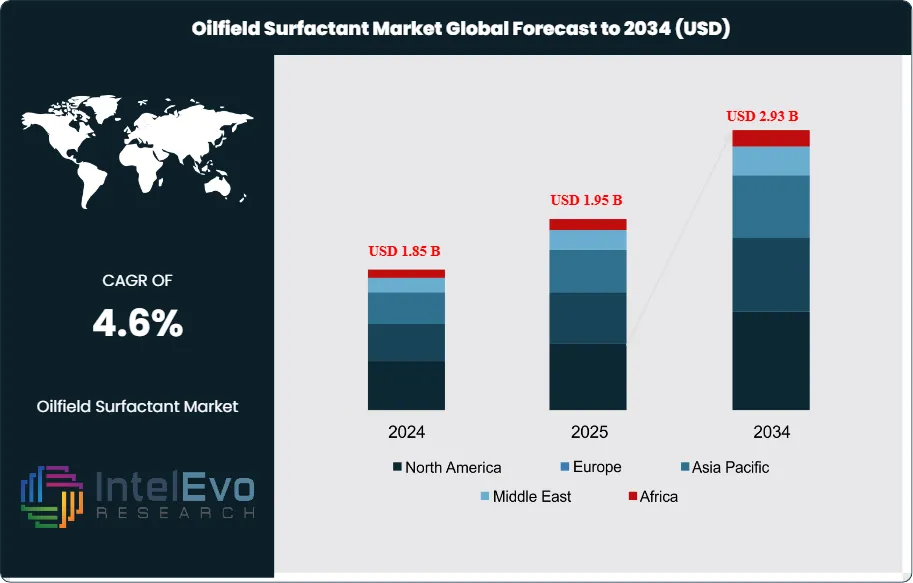

| USD 1.95 Billion | USD 2.93 Billion | 4.6% | North America, 31.0% |

The Oilfield Surfactant Market was valued at approximately USD 1.85 Billion in 2024 and increased to USD 1.95 Billion in 2025. The market is projected to reach nearly USD 2.93 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 4.6% during the forecast period from 2026 to 2034. The market growth is primarily driven by increasing demand for enhanced oil recovery (EOR) techniques, rising offshore exploration activities, and the growing use of surfactants in drilling fluids and production chemicals. Additionally, advancements in bio-based and environmentally friendly surfactant formulations are expected to create new opportunities for market expansion over the coming years.

Get More Information about this report -

Request Free Sample ReportThe oilfield surfactant market sits inside the broader specialty oilfield chemicals chain and remains tied to production chemistry, enhanced oil recovery, drilling fluid performance, and stimulation efficiency. Demand stays strongest where operators need higher recovery from mature reservoirs, better phase behavior in complex fluids, and stronger flow assurance in offshore and high-salinity environments. The oilfield surfactant market also benefits from a structural shift toward reservoir management over pure volume drilling. IEA expects upstream oil investment to fall 6% to about USD 420 Billion in 2025, while conventional projects remain more resilient than US light tight oil. That mix favors chemistry-led production improvement over purely rig-led expansion. Upstream oil and gas costs are also set to rise about 3% in 2025, which increases pressure on operators to use chemicals that raise recovery and reduce non-productive time.

In 2025, enhanced oil recovery accounts for 34.0% of oilfield surfactant market revenue, equal to USD 0.66 Billion, because surfactants directly reduce interfacial tension and alter wettability in chemical flooding and production enhancement programs. ChampionX states that its surfactant formulations are designed to improve oil recovery across conventional and unconventional reservoirs over a broad range of salinities and temperatures. SLB's technical material also links alkaline-surfactant-polymer flooding to improved oil production. These technology pathways support steady demand in China, the Middle East, Latin America, and mature North American assets.

Supply remains moderately concentrated. The top four suppliers hold an estimated 42.0% of 2025 revenue. Halliburton Multi-Chem, SLB, Baker Hughes, ChampionX, and Clariant shape the high-value end through integrated chemistry, field service coverage, and digital dosing or production management tools. Halliburton says Multi-Chem supports global upstream, midstream, and downstream markets through regional laboratories and digitally enabled workflows. Clariant describes Oil Services as a world leader in specialty chemicals for enhanced oil recovery, offshore and deepwater, and intelligent chemical management. SLB completed its ChampionX acquisition in July 2025 and expects about USD 400 Million in annual pretax synergies within three years, which increases scale in production and recovery chemistry.

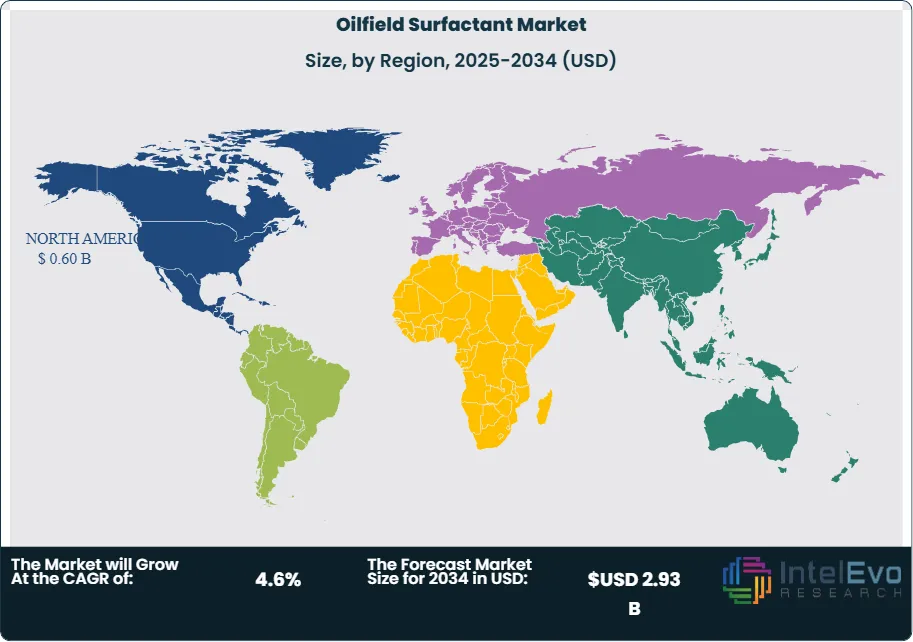

Regionally, North America leads with 31.0% of 2025 revenue, or USD 0.60 Billion, driven by US unconventional production chemistry and Gulf of Mexico flow assurance needs. The Middle East & Africa follows with 24.0%, supported by higher Middle East upstream spending and large brownfield recovery programs. IEA expects the Middle East share of global upstream investment to reach 20% in 2025, the highest level on record. Asia Pacific stands out as the fastest-growing oilfield surfactant market through 2034 because China and India are expanding mature-field recovery, while Southeast Asia and Australia are adding offshore demand. Environmental rules remain a selective risk. EPA's PFAS actions and tighter screening of persistent chemistries are pushing suppliers toward lower-toxicity, more biodegradable formulations in some product lines.

, By Application (Enhanced Oil Recovery, Production Chemicals & Flow Assurance, Drilling Fluids, Stimulation & Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Key Players, Strategic Developments, Technology Innovations, Growth Drivers & Forecast 2026–2034")

Key Takeaways

| Category | Insight |

|---|---|

| Market Growth | The oilfield surfactant market stands at USD 1.95 Billion in 2025 and is projected to reach USD 2.93 Billion by 2034. That implies a 4.6% CAGR across 2026-2034. |

| Segment Dominance | Non-ionic surfactants lead the oilfield surfactant market by product type with 37.0% share in 2025, equal to USD 0.72 Billion. They hold the top position because they perform well across wide salinity and temperature windows. |

| Segment Dominance | Enhanced oil recovery leads by application with 34.0% share in 2025, equal to USD 0.66 Billion. Mature-field redevelopment and chemical flooding keep this segment ahead of drilling and stimulation uses. |

| Driver | Mature-field recovery is the primary growth driver. Around 58.0% of 2025 oilfield surfactant demand comes from production and recovery uses, and EOR-linked chemistries are expanding faster than the total market. |

| Restraint | Raw material volatility and compliance costs remain the main brake. Feedstock and formulation cost pressure is reducing EBITDA in some chemical lines and holds back about 0.7 percentage points of annual market growth in price-sensitive regions. |

| Opportunity | Bio-based and low-toxicity surfactants represent the largest untapped opening. This niche accounts for USD 0.21 Billion in 2025 and can exceed USD 0.43 Billion by 2034 at about 8.4% CAGR. |

| Trend | Digital chemical management is the strongest operating trend. Roughly 29.0% of 2025 market revenue is linked to programs that include remote dosing, lab analytics, or predictive field monitoring. |

| Regional Analysis | North America leads the oilfield surfactant market with 31.0% share in 2025, equivalent to USD 0.60 Billion. US land production chemistry and Gulf of Mexico offshore assets anchor that lead. |

Competitive Landscape

The oilfield surfactant market is moderately consolidated. The top four players account for an estimated 42.0% of global 2025 revenue. Competition is technology-driven in EOR and production chemistry, but price and service density still matter in drilling and flow assurance. Competitive intensity increased in 2025 after SLB closed the ChampionX acquisition and targeted about USD 400 Million in annual pretax synergies within three years. Baker Hughes also added chemicals momentum through ExxonMobil Guyana, while Halliburton continued to win multi-year stimulation work tied to reservoir productivity.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| SLB | US | Leader | Production Chemicals and EOR portfolio | North America, Middle East | Completed ChampionX acquisition with expected annual pretax synergies of about USD 400 Million within three years (Jul 2025) |

| HALLIBURTON | US | Leader | Multi-Chem specialty chemicals | North America, Middle East | Won a five-year ConocoPhillips well stimulation contract in the North Sea (Aug 2025) |

| BAKER HUGHES | US | Leader | Specialty chemicals for FPSO and production systems | Latin America, Middle East | Secured a major ExxonMobil Guyana chemicals award for FPSOs (Feb 2025) |

| CHAMPIONX | US | Leader | PROE surfactant technology portfolio | North America, Latin America | Expanded Chemical Technologies leadership and digital optimization focus ahead of SLB integration (Feb 2025) |

| CLARIANT | Switzerland | Challenger | Oil Services EOR and VERITRAX | Middle East, Latin America | Reported mid-single-digit Oil Services sales growth recovery in 2025 and continued regional capacity focus in Asia (Oct 2025) |

| BASF | Germany | Challenger | Lutensol and specialty surfactant systems for oilfield formulations | Europe, Middle East | Continued focus on lower-footprint surfactant chemistry and regional supply localization in 2025 |

| SOLVAY | Belgium | Challenger | Specialty surfactants and formulation intermediates | Europe, Latin America | Advanced fluorine-free and lower-impact surfactant positioning across industrial chemistries in 2025 |

| NOURYON | Netherlands | Niche Player | Ethoxylates and specialty surfactant intermediates | Europe, Middle East | Expanded specialty chemistry supply support for energy and industrial customers in 2025 |

| STEPAN COMPANY | US | Niche Player | Alpha olefin sulfonates and custom surfactants | North America | Increased focus on bio-based and application-specific surfactant development in 2025 |

| INNOSPEC | US | Niche Player | Specialty performance surfactants | North America, Europe | Continued specialty chemicals push in high-value industrial applications through 2025 |

By Product Type

Non-ionic surfactants hold the largest share of the oilfield surfactant market at 37.0% in 2025, or USD 0.72 Billion. They lead because operators use them across drilling, stimulation, and production systems where tolerance to salinity, compatibility with other additives, and stable emulsification matter more than peak activity in narrow conditions. In offshore production chemicals and mature-field remediation, non-ionic systems often sit at the center of blended formulations because they balance wetting, detergency, and demulsification. Anionic surfactants rank second with 28.0% share, or USD 0.55 Billion, and remain critical in chemical EOR where interfacial tension reduction drives displacement efficiency. Cationic surfactants account for 14.0%, or USD 0.27 Billion, and serve niche roles in clay stabilization, corrosion control, and selected stimulation chemistries. Amphoteric surfactants represent 9.0%, or USD 0.18 Billion, supported by high-compatibility systems in complex brines and mixed packages. Bio-based surfactants still hold only 11.0%, or USD 0.21 Billion, but they are the fastest-growing product class because procurement teams in Europe and North America are screening toxicity, biodegradability, and PFAS-adjacent exposure more closely. That growth path aligns with broader pressure to move away from persistent chemistries and with supplier investment in renewable-carbon surfactant lines.

By Application

Enhanced oil recovery is the largest application in the oilfield surfactant market with 34.0% share in 2025, equal to USD 0.66 Billion. This segment benefits from mature-field redevelopment, especially where operators seek incremental barrels without major new drilling campaigns. ChampionX states that its EOR surfactant formulations are designed to improve recovery across conventional and unconventional reservoirs over broad salinity and temperature ranges. Production chemicals and flow assurance follow with 24.0% share, or USD 0.47 Billion, supported by paraffin control, emulsion treatment, water handling, and well clean-up. Halliburton's Multi-Chem case history shows how a surfactant-linked program restored saltwater disposal performance and produced monthly ROI above USD 204,000, which explains why operators protect these budgets even in softer drilling cycles. Drilling fluids represent 18.0%, or USD 0.35 Billion, where surfactants help lubricity, shale inhibition packages, and emulsification. Stimulation and hydraulic fracturing account for 16.0%, or USD 0.31 Billion, tied to wetting, cleanup, and water-trap mitigation. The remaining 8.0%, or USD 0.16 Billion, covers cementing, pipeline cleaning, and specialty well intervention. Across the forecast period, EOR and production chemistry will keep gaining mix share because IEA expects conventional project spending to prove more resilient than light tight oil investment in 2025.

By Source

Synthetic surfactants dominate the oilfield surfactant market by source with 89.0% share in 2025, equivalent to USD 1.74 Billion. They remain the default choice because oilfield applications demand repeatable performance under high temperature, high salinity, high shear, and multi-additive conditions. Synthetic chemistries also benefit from established qualification protocols, large installed customer bases, and lower unit cost in mainstream drilling and production packages. That strength is most visible in North America, the Middle East, and offshore Latin America, where field economics still favor proven formulations at scale. Bio-based surfactants account for 11.0%, or USD 0.21 Billion, but their role is expanding faster than the overall market. Clariant's 2025 product communication on 100% bio-based surfactants and PEGs with renewable carbon index above 95% shows how specialty suppliers are pushing lower-carbon chemistry into commercial pipelines. Growth remains strongest in Europe, selective offshore projects, and multinational procurement programs that embed sustainability criteria in chemical sourcing. The commercial hurdle is not demand interest. It is qualification speed, cost, and performance under harsh reservoir conditions. Even so, bio-based share should rise steadily through 2034 as suppliers improve formulation stability and regulators continue to tighten scrutiny on persistent, poorly degradable ingredients.

By Field Type

Onshore fields account for 68.0% of the oilfield surfactant market in 2025, or USD 1.33 Billion. Their lead comes from the scale of US land production chemistry, Chinese mature fields, Middle East brownfields, and onshore Latin American recovery programs. Onshore assets consume high volumes of drilling, stimulation, and production chemicals, but buyers remain cost-sensitive and expect clear field economics. That keeps non-ionic and anionic blends in wide use, especially in water handling, paraffin control, and EOR pilots. Offshore fields hold 32.0%, or USD 0.62 Billion, but generate a richer revenue mix because formulations face stricter performance thresholds, logistics constraints, and discharge rules. Offshore demand is strongest in Brazil, Guyana, the North Sea, West Africa, and the Gulf of Mexico. Baker Hughes' 2025 ExxonMobil Guyana award for specialty chemicals tied to FPSOs underscores the value density of offshore production chemistry. Halliburton's North Sea stimulation contract points in the same direction. Offshore surfactant demand will outgrow onshore on a value basis through 2034 because deepwater operators spend more per treated barrel and need stronger flow assurance, emulsion control, and asset integrity support.

Regional Analysis

North America Oilfield Surfactant Market

North America holds 31.0% of the oilfield surfactant market in 2025, equal to USD 0.60 Billion. The United States accounts for about USD 0.47 Billion of that total, Canada for USD 0.08 Billion, and Mexico for USD 0.05 Billion. The region leads because it combines large unconventional production chemistry demand with mature-field remediation and offshore applications in the Gulf of Mexico. Halliburton reported North America revenue of USD 2.2 Billion in the first quarter of 2025, although lower stimulation activity in US land softened the service backdrop. Even with that pressure, chemical programs remain sticky because operators still need flow assurance, water treatment, paraffin management, and stimulation cleanup. The US remains the anchor market. Permian, Eagle Ford, Bakken, and Gulf Coast assets rely on surfactant packages across drilling fluids, hydraulic fracturing, produced water treatment, and well clean-up. Canada adds heavy-oil and thermal chemistry needs, especially in Western Canada, while Mexico remains linked to mature onshore and offshore optimization. Regulatory pressure is higher here than in most regions. EPA's PFAS program and broader water-quality oversight are pushing suppliers toward lower-persistence ingredients and clearer disclosure. That does not reduce surfactant demand. It changes the formulation mix and raises qualification costs. North America also remains the most mature digital chemistry market. Halliburton's APX platform and ChampionX remote chemical injection monitoring show why service intensity, not only chemistry, drives market share. The region should keep its lead through 2034, but growth will stay moderate because drilling is cyclical and operators remain disciplined on spend.

Europe Oilfield Surfactant Market

Europe represents 17.0% of the oilfield surfactant market in 2025, or USD 0.33 Billion. Norway leads the region with about USD 0.10 Billion, followed by the UK at USD 0.08 Billion, Germany at USD 0.05 Billion, and France at USD 0.04 Billion, with the balance spread across the Netherlands, Italy, and the rest of Europe. The North Sea is the core value pool because offshore mature assets require high-performance production chemistry, emulsion treatment, and stimulation support. Halliburton's 2025 five-year ConocoPhillips North Sea stimulation award shows that operators are still extending reservoir productivity in the basin. Europe differs from North America because environmental and product stewardship standards play a larger role in buying decisions. That pushes more demand toward lower-toxicity, lower-discharge surfactants and higher documentation requirements. The region also benefits from the presence of large specialty chemical suppliers such as BASF, Clariant, Solvay, and Nouryon, which helps local formulation support and technical service. Germany and France matter more as formulation and supply-chain centers than as upstream demand centers, while Norway and the UK drive offshore consumption. Europe's oilfield surfactant market will grow below the global average through 2034 because upstream expansion is limited, but revenue per treated well stays high. The region remains attractive for suppliers that can combine offshore chemistry, digital dosing control, and strong environmental compliance.

Asia Pacific Oilfield Surfactant Market

Asia Pacific accounts for 22.0% of the oilfield surfactant market in 2025, or USD 0.43 Billion. China leads with roughly USD 0.18 Billion, followed by India at USD 0.08 Billion, Australia at USD 0.06 Billion, and Japan at USD 0.04 Billion. The rest comes from Indonesia, Malaysia, and Southeast Asia offshore projects. Asia Pacific is the fastest-growing regional market because it combines mature-field EOR demand with offshore project activity and expanding domestic chemical supply chains. China is the central driver. Mature conventional fields and state-backed recovery programs create a large market for chemical flooding and production enhancement. India adds growth through maturing onshore assets and rising domestic service capability. Australia contributes offshore high-value chemistry demand, while Southeast Asia adds deepwater and brownfield support work. Clariant's regional manufacturing and technical presence in India and China supports this shift, and its 2025 communication around bio-based surfactants also fits Asia's growing mix of supply security and sustainability goals. Asia Pacific will likely post the highest regional CAGR through 2034 because chemistry intensity per barrel is still rising and because the region continues to add offshore and mature-field recovery programs at the same time.

Latin America Oilfield Surfactant Market

Latin America holds 14.0% of the oilfield surfactant market in 2025, equal to USD 0.27 Billion. Brazil leads with about USD 0.12 Billion, Mexico contributes USD 0.06 Billion, and Argentina adds USD 0.04 Billion, with the remainder spread across Colombia and the rest of the region. Brazil is the main value center because offshore pre-salt assets require high-performance production and flow assurance chemistry. Guyana is not counted in Latin America for this report's country list, but its rapid offshore build-out is also pulling supplier resources into the wider basin. Baker Hughes' 2025 ExxonMobil Guyana award for specialty chemicals tied to FPSOs confirms how fast offshore chemical demand is scaling in the region. Brazil and Guyana support premium offshore formulations. Mexico remains more exposed to mature-field and service-cycle risks, while Argentina adds onshore unconventional and water-management chemistry demand. Latin America also offers strong upside for EOR and production enhancement because many assets require incremental recovery and flow assurance rather than large new drilling programs. Halliburton's reported weaker Latin America revenue in early 2025 shows the region can swing with national budgets and project timing, but chemistry remains one of the more resilient spend lines when operators need production continuity. Through 2034, Latin America should outpace Europe on growth because offshore expansion and brownfield optimization continue together.

Middle East & Africa Oilfield Surfactant Market

Middle East & Africa represents 24.0% of the oilfield surfactant market in 2025, or USD 0.47 Billion. Saudi Arabia leads with about USD 0.14 Billion, the UAE contributes USD 0.08 Billion, South Africa adds USD 0.02 Billion, and the remainder comes from Kuwait, Oman, West Africa, and the rest of the region. The market is split between Middle East brownfield recovery and African offshore production chemistry. IEA expects the Middle East share of global upstream investment to reach 20% in 2025, the highest level on record. That underpins long-cycle chemistry demand tied to reservoir management and conventional production optimization. Saudi Arabia, the UAE, Kuwait, and Oman drive volume through stimulation, flow assurance, and mature-field production enhancement. Halliburton's first-quarter 2025 results showed stronger activity in Kuwait, Saudi Arabia, and the UAE, including higher stimulation activity and increased fluid services. Africa contributes more selectively through deepwater projects in Angola, Nigeria, and Namibia. Nigeria's policy push to raise crude output and ExxonMobil's planned USD 1.5 Billion investment in revitalizing deepwater operations support future chemistry demand in West Africa. This region will remain one of the most attractive oilfield surfactant markets through 2034 because reservoirs are large, conventional spending is resilient, and recovery improvement matters more than pure rig count. Suppliers with strong field service networks and high-temperature, high-salinity surfactant systems hold the best position here.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Non-ionic Surfactants

- Anionic Surfactants

- Cationic Surfactants

- Amphoteric Surfactants

- Bio-based Surfactants

By Application

- Enhanced Oil Recovery

- Production Chemicals and Flow Assurance

- Drilling Fluids

- Stimulation and Hydraulic Fracturing

- Others

By Source

- Synthetic

- Bio-based

By Field Type

- Onshore

- Offshore

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.95 B |

| Forecast Revenue (2034) | USD 2.93 B |

| CAGR (2025-2034) | 4.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Non-ionic Surfactants, Anionic Surfactants, Cationic Surfactants, Amphoteric Surfactants, Bio-based Surfactants), By Application (Enhanced Oil Recovery, Production Chemicals and Flow Assurance, Drilling Fluids, Stimulation and Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, CHAMPIONX, CLARIANT, BASF, SOLVAY, NOURYON, STEPAN COMPANY, INNOSPEC, DOW, CRODA INTERNATIONAL, HUNTSMAN, SNF, CHEVRON PHILLIPS CHEMICAL, LUBRIZOL, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Enhanced Oil Recovery, Production Chemicals & Flow Assurance, Drilling Fluids, Stimulation & Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Key Players, Strategic Developments, Technology Innovations, Growth Drivers & Forecast 2026–2034")

, By Application (Enhanced Oil Recovery, Production Chemicals & Flow Assurance, Drilling Fluids, Stimulation & Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Key Players, Strategic Developments, Technology Innovations, Growth Drivers & Forecast 2026–2034")

, By Application (Enhanced Oil Recovery, Production Chemicals & Flow Assurance, Drilling Fluids, Stimulation & Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Key Players, Strategic Developments, Technology Innovations, Growth Drivers & Forecast 2026–2034")

Frequently Asked Questions

How big is the Oilfield Surfactant Market?

The Global Oilfield Surfactant Market was valued at USD 1.85 Billion in 2024 and reached USD 1.95 Billion in 2025, projected to grow to USD 2.93 Billion by 2034 at a CAGR of 4.6% from 2026–2034. Growth is driven by rising enhanced oil recovery (EOR) activities, expanding offshore exploration, and increasing demand for advanced drilling and production chemicals.

Who are the major players in the Oilfield Surfactant Market?

SLB, HALLIBURTON, BAKER HUGHES, CHAMPIONX, CLARIANT, BASF, SOLVAY, NOURYON, STEPAN COMPANY, INNOSPEC, DOW, CRODA INTERNATIONAL, HUNTSMAN, SNF, CHEVRON PHILLIPS CHEMICAL, LUBRIZOL, Others

Which segments covered the Oilfield Surfactant Market?

By Product Type (Non-ionic Surfactants, Anionic Surfactants, Cationic Surfactants, Amphoteric Surfactants, Bio-based Surfactants), By Application (Enhanced Oil Recovery, Production Chemicals and Flow Assurance, Drilling Fluids, Stimulation and Hydraulic Fracturing, Others), By Source (Synthetic, Bio-based), By Field Type (Onshore, Offshore)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date