- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oncolytic Virus Therapy Market Size, Share & Forecast | CAGR of 15.2%

Global Oncolytic Virus Therapy Market Size, Share, Analysis By Virus Type (Herpes Simplex Virus - HSV, Adenovirus, Reovirus), By Application (Melanoma, Lung Cancer, Breast Cancer), By Delivery Route (Intratumoral, Intravenous), By End-User (Hospitals, Research Institutes) Region, Key Players – Dynamics, Immuno-Oncology & Cancer Immunotherapy Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

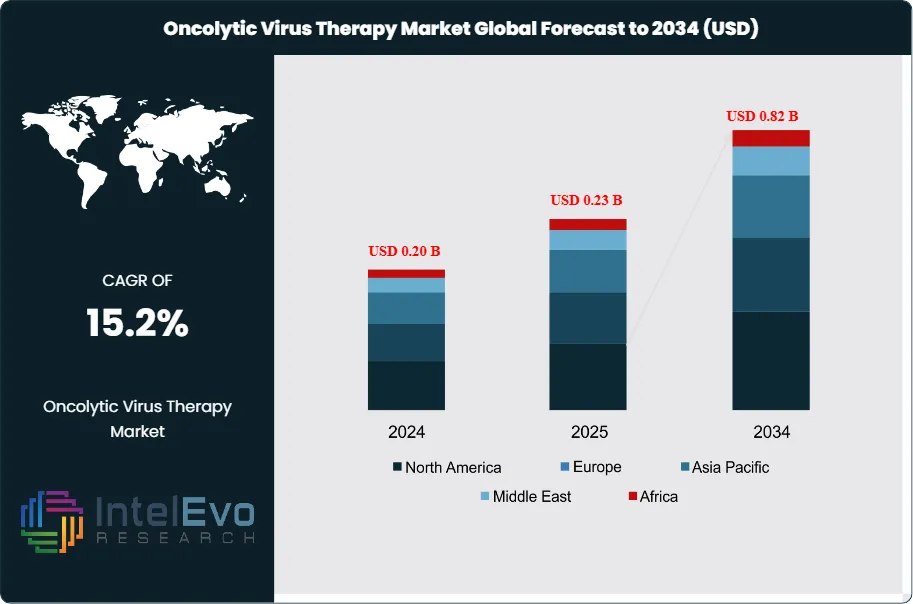

| USD 0.23 Billion | USD 0.82 Billion | 15.2% | North America, 42.9% |

The Oncolytic Virus Therapy Market was valued at approximately USD 0.20 billion in 2024 and reached USD 0.23 billion in 2025. The market is projected to grow to USD 0.82 billion by 2034, expanding at a CAGR of 15.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 0.59 Billion over the analysis period. The oncolytic virus therapy market remains a narrow commercial market because only a small number of approved products, including Amgen's Imlygic, Daiichi Sankyo's Delytact, and Shanghai Sunway Biotech's H101, generate routine treatment revenue.

Get More Information about this report -

Request Free Sample ReportThe demand case for the oncolytic virus therapy market is built on cancer immunotherapy gaps rather than broad oncology replacement. WHO and IARC estimated close to 20 million new cancer cases and 9.7 million deaths in 2022, and projected more than 35 million new cases by 2050. Viral immunotherapy addresses tumors where checkpoint inhibitors, chemotherapy, and radiation leave residual local disease, because engineered HSV-1, adenovirus, vaccinia, and reovirus platforms can lyse tumor cells and release tumor antigens inside the tumor microenvironment.

Regulatory risk is the central constraint in the oncolytic virus therapy market. The U.S. FDA approved talimogene laherparepvec for unresectable cutaneous, subcutaneous, and nodal melanoma lesions after surgery, but the same agency issued a second complete response letter to Replimune's RP1 BLA on April 10, 2026. That decision showed that single-arm response data may not support accelerated approval when FDA reviewers want randomized evidence linking clinical response to the viral product rather than to a checkpoint inhibitor backbone.

Commercial momentum is shifting toward bladder cancer, prostate cancer, and ovarian cancer programs with controlled late-stage designs. CG Oncology reported more than 600 patients studied across its cretostimogene program by February 2026, including BOND-003 and PIVOT-006 in non-muscle invasive bladder cancer. Candel Therapeutics disclosed a 745-patient randomized Phase 3 prostate cancer trial for CAN-2409, while Genelux expects second-half 2026 top-line data from the Phase 3 OnPrime/GOG-3076 trial of Olvi-Vec in platinum-resistant ovarian cancer.

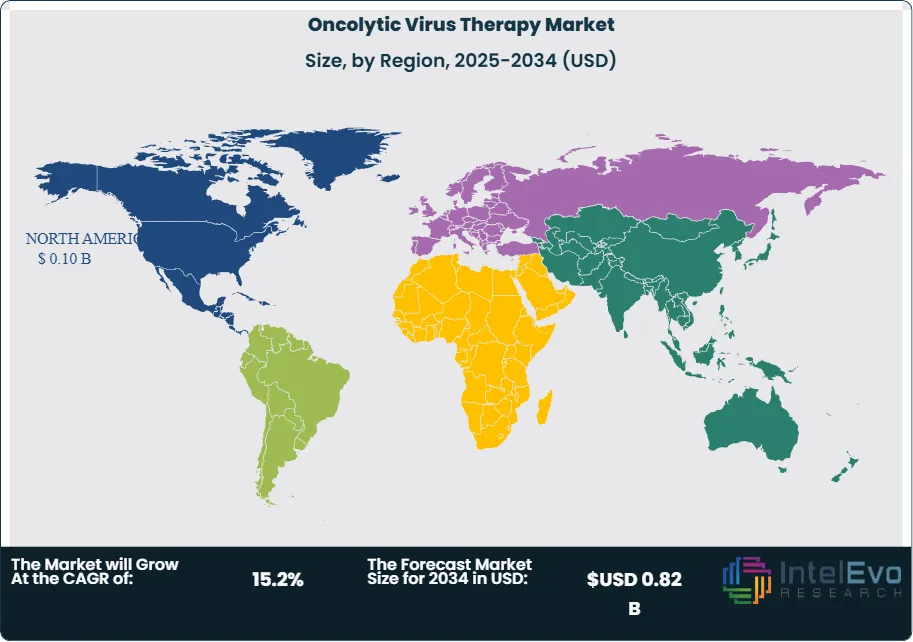

North America held 42.9% of oncolytic virus therapy market revenue in 2025, equivalent to USD 0.10 Billion, because U.S. cancer centers, FDA CBER pathways, venture financing, and immuno-oncology trial density concentrate commercial access. Asia Pacific is the fastest-growing region through 2034 because China already commercialized H101, Japan conditionally approved Delytact, and regional companies are testing intratumoral, intravesical, and peritoneal delivery approaches across solid tumors. By 2034, the market should remain smaller than antibody immunotherapy, but a single bladder or prostate approval could more than double addressable treated-patient volume.

Market Definition & Scope

The oncolytic virus therapy market is defined as the commercial and clinical-development market for live or replication-competent viruses engineered or selected to infect tumor cells, induce tumor lysis, and stimulate anti-tumor immunity. The market encompasses approved viral medicines, late-stage viral immunotherapy candidates, combination regimens with PD-1 or PD-L1 inhibitors, and supporting treatment protocols used in melanoma, glioma, bladder cancer, prostate cancer, ovarian cancer, pancreatic cancer, and other solid tumors.

This analysis includes drug revenue from approved oncolytic products, pipeline-attributed opportunity for late-stage candidates, hospital administration economics, and specialty oncology procurement tied to viral therapy use. It excludes pure viral-vector CDMO services, gene therapy for inherited disease, cancer vaccines without replicating viral lysis, CAR-T therapy, monoclonal antibody immunotherapy, and diagnostic viral-vector assays. Within the broader cancer immunotherapy parent market, oncolytic virus therapy represented less than 0.5% of 2025 revenue, which explains its high growth base and high regulatory sensitivity.

, By Application (Melanoma, Lung Cancer, Breast Cancer), By Delivery Route (Intratumoral, Intravenous), By End-User (Hospitals, Research Institutes) Region, Key Players – Dynamics, Immuno-Oncology & Cancer Immunotherapy Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The oncolytic virus therapy market was valued at USD 0.23 Billion in 2025 and is forecast to reach USD 0.82 Billion by 2034 at a 15.2% CAGR.

- Segment Dominance: Herpes simplex virus platforms held 38.0% share in 2025, equal to USD 0.09 Billion, because Imlygic, Delytact, RP1, and multiple oHSV candidates anchor late-stage use.

- Segment Dominance: Melanoma represented 36.0% of 2025 revenue, or USD 0.08 Billion, due to Amgen's approved Imlygic and multiple HSV-based skin-cancer trials.

- Driver: Global cancer incidence is projected to rise from about 20 million cases in 2022 to more than 35 million cases by 2050, expanding demand for tumor-local immunotherapies.

- Restraint: FDA's April 2026 RP1 complete response letter raised the evidentiary bar for single-arm oncolytic studies, delaying U.S. commercialization timelines for checkpoint-combination programs.

- Opportunity: Non-muscle invasive bladder cancer offers an estimated USD 0.18 Billion opportunity by 2034 because intravesical delivery can fit established urology workflows.

- Trend: Controlled Phase 3 trials are replacing single-arm accelerated-approval packages, with CG Oncology, Candel Therapeutics, and Genelux running late-stage programs through 2026.

- Regional: North America led with 42.9% share and USD 0.10 Billion in 2025 revenue, while Asia Pacific is forecast to record the fastest regional CAGR at 17.1%.

Key Insights Summary

- The oncolytic virus therapy market includes three commercial reference products: Imlygic in the United States and Europe, Delytact in Japan, and H101 in China.

- CG Oncology's cretostimogene program covered more than 600 patients by February 2026, with two Phase 3 trials in non-muscle invasive bladder cancer.

- Candel Therapeutics' CAN-2409 Phase 3 localized prostate cancer trial enrolled 745 patients and used a randomized, double-blind, placebo-controlled design.

- On April 10, 2026, FDA rejected Replimune's RP1 BLA again because available studies did not provide adequate evidence of effectiveness.

- Genelux's OnPrime/GOG-3076 Phase 3 ovarian cancer trial is designed as a randomized study of Olvi-Vec followed by platinum-doublet chemotherapy and bevacizumab.

- Imlygic's FDA label uses an initial 10^6 PFU per mL dose and subsequent 10^8 PFU per mL doses, showing how viral potency and administration schedule shape hospital handling.

- Global cancer burden projections imply a 77.0% increase in new cases between 2022 and 2050, supporting long-run demand for local and systemic immuno-oncolytic approaches.

Competitive Landscape Overview

The oncolytic virus therapy market is moderately concentrated by commercial revenue but fragmented by pipeline count. Amgen, Daiichi Sankyo, Shanghai Sunway Biotech, and CG Oncology represent the most consequential current and near-term revenue positions, while Replimune, Candel Therapeutics, Genelux, Oncolytics Biotech, Imugene, and Calidi Biotherapeutics compete through clinical catalysts. The top four players accounted for approximately 58.0% of 2025 therapy revenue and risk-adjusted late-stage value.

Competition is driven by virus backbone, delivery route, randomized evidence quality, manufacturing control, and ability to combine with checkpoint inhibitors. The April 2026 RP1 decision weakened single-arm melanoma strategies, while bladder and prostate programs gained relative value because their trial designs, treatment settings, and endpoint structures better match regulator expectations.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| Amgen Inc. | United States | Leader | Imlygic (talimogene laherparepvec) | United States, Europe | Maintained Imlygic as the U.S. commercial reference product while oncology revenue reached USD 36.8 Billion group-wide in 2025 |

| Daiichi Sankyo Co., Ltd. | Japan | Leader | Delytact (teserpaturev/G47 Delta) | Japan | Continued Japanese use of Delytact under regenerative medical product rules while focusing group oncology investment on global specialty products |

| Shanghai Sunway Biotech Co., Ltd. | China | Leader | H101 / Oncorine adenovirus | China | Sustained China's approved adenovirus therapy position as regional intratumoral programs expanded in 2025 and 2026 |

| CG Oncology, Inc. | United States | Leader | Cretostimogene grenadenorepvec | United States | Reported more than 600 studied NMIBC patients and two Phase 3 trials in February 2026 |

| Replimune Group, Inc. | United States | Challenger | RP1, RP2, RP3 | United States, Europe | Received a second FDA complete response letter for RP1 on April 10, 2026 |

| Candel Therapeutics, Inc. | United States | Challenger | CAN-2409, CAN-3110 | United States | Raised USD 100 Million in February 2026 to fund late-stage viral immunotherapy development |

| Genelux Corporation | United States | Challenger | Olvi-Vec | United States | Guided to Phase 3 ovarian cancer top-line data in the second half of 2026 |

| Oncolytics Biotech Inc. | Canada | Challenger | Pelareorep | North America | Prepared for FDA Type C interaction in Q1 2026 for pancreatic cancer development planning |

| Imugene Limited | Australia | Niche Player | VAXINIA / CF33-hNIS | Australia, United States | Updated Phase 1 VAXINIA trial records in early 2026 as the program narrowed development focus |

| Calidi Biotherapeutics, Inc. | United States | Niche Player | CLD-101, RTNova platform | United States | Continued glioma and systemic virotherapy platform development through 2025 |

Segmentation Analysis

The oncolytic virus therapy market segments by virus type, application, delivery route, and end-user, with segment economics shaped by approved-product precedent, route-of-administration feasibility, and the quality of disease-specific clinical evidence.

By Virus Type

The oncolytic virus therapy market by virus type was led by herpes simplex virus platforms at 38.0% share and USD 0.09 Billion in 2025. HSV platforms dominate because Imlygic, Delytact, Replimune RP1, and Candel's CAN-3110 use herpes-family biology or HSV-derived payload logic in settings where local injection is feasible. HSV backbones provide large genome capacity for immune genes such as GM-CSF, which supports product differentiation in melanoma, glioma, and other solid tumors. Compared with adenovirus platforms at 24.0% share, HSV products carry more commercial proof but face handling constraints linked to live-virus shedding and immunocompromised patients.

Adenovirus platforms accounted for 24.0% of 2025 revenue, or USD 0.06 Billion, with CG Oncology's cretostimogene and Shanghai Sunway Biotech's H101 anchoring the category. Adenovirus therapy benefits from intravesical and intratumoral administration, because urologists and interventional oncologists can expose localized lesions without systemic viral delivery. Vaccinia virus represented 18.0% share, driven by Genelux Olvi-Vec and Imugene CF33 work across ovarian and solid tumor settings. Reovirus, Newcastle disease virus, vesicular stomatitis virus, and other platforms formed the remaining 20.0% share, with Oncolytics Biotech and academic groups pursuing systemic immune priming rather than direct tumor injection only.

By Application

The oncolytic virus therapy market by application was led by melanoma at 36.0% share and USD 0.08 Billion in 2025, because Amgen's Imlygic remains the main approved U.S. therapy and RP1 targeted advanced melanoma before FDA's 2026 rejection. Melanoma retains clinical relevance because injectable skin and nodal lesions allow direct viral delivery, biopsy monitoring, and combination with nivolumab or other checkpoint inhibitors. Bladder cancer ranked second at 18.0% share and USD 0.04 Billion, with CG Oncology's cretostimogene creating the largest risk-adjusted near-term expansion pathway. Bladder cancer's advantage is operational, because intravesical therapy already fits urology clinics that use BCG, mitomycin, and device-assisted drug delivery.

Glioma accounted for 14.0% share in 2025, led by Daiichi Sankyo's Delytact in Japan and glioblastoma programs from Calidi Biotherapeutics and academic centers. Ovarian cancer represented 12.0% share, supported by Genelux Olvi-Vec in platinum-resistant disease and intraperitoneal delivery logic. Other solid tumors, including prostate, pancreatic, lung, and head and neck cancers, held 20.0% share and should expand faster than melanoma through 2034. Candel's prostate and NSCLC programs show why the market is moving toward randomized disease-specific evidence rather than broad pan-tumor claims.

By Delivery Route

The oncolytic virus therapy market by delivery route was dominated by local administration at 66.0% share in 2025, covering intratumoral, intralesional, and intravesical use. Local delivery leads because viral biodistribution, shedding, immune neutralization, and dose escalation can be controlled more easily than with intravenous therapy. Imlygic requires direct injection into melanoma lesions, while cretostimogene uses bladder instillation and Delytact uses a neurosurgical oncology setting. Compared with systemic administration, local delivery lowers early development risk and improves payer understanding of procedure-linked costs.

Intraperitoneal delivery held 13.0% share, mainly because ovarian cancer allows compartmental exposure to peritoneal disease with Olvi-Vec and similar vaccinia programs. Intravenous delivery represented 9.0% share, led by Oncolytics Biotech pelareorep and next-wave systemic platforms that seek immune priming across metastatic disease. Other delivery modes, including carrier-cell delivery and image-guided injection, represented 12.0% share. These routes should grow through 2034 as manufacturers use cell carriers, polymer shielding, and dosing algorithms to reduce neutralizing antibody effects.

By End-User

The oncolytic virus therapy market by end-user was led by hospitals and specialty oncology clinics at 51.0% share in 2025, equal to USD 0.12 Billion. This segment leads because approved viral therapies require clinician-administered dosing, biosafety processes, lesion measurement, and post-treatment monitoring. Academic cancer centers and research institutes held 29.0% share, because trial enrollment remains the primary access route for RP1, cretostimogene, CAN-2409, Olvi-Vec, pelareorep, and VAXINIA. Procurement teams in these centers evaluate storage temperature, viral shedding protocols, pharmacy preparation time, and procedure-room fit before adding a therapy.

Biotechnology and pharmaceutical companies represented 20.0% of 2025 market economics through sponsored trials, companion manufacturing, and clinical material consumption. This category has the fastest 2034 growth because Phase 2 and Phase 3 viral programs consume GMP batches before any commercial revenue appears. For vendor selection, the procurement checklist increasingly includes randomized trial readiness, CMC comparability after scale-up, vector identity testing, and potency assay reproducibility. The oncolytic virus therapy implementation timeline therefore depends as much on pharmacy and biosafety staffing as on oncologist demand.

Regional Analysis

The oncolytic virus therapy market remains concentrated in North America, Europe, and Asia Pacific, while Latin America and Middle East & Africa depend on tertiary cancer centers and imported specialty oncology access.

North America: North America led the oncolytic virus therapy market with 42.9% share and USD 0.10 Billion in 2025 revenue. The United States accounted for most regional demand because Amgen commercializes Imlygic, FDA CBER regulates biologics licenses, and CG Oncology, Replimune, Candel Therapeutics, Genelux, Calidi Biotherapeutics, and Oncolytics Biotech run U.S.-centered trials. FDA's April 2026 RP1 decision slowed melanoma expansion, but CG Oncology's rolling BLA work and Candel's Phase 3 planning preserved late-stage investor attention. Canada contributed through Oncolytics Biotech and cancer-center trial participation, while Mexico remains mainly a clinical-access market.

Europe: Europe held 24.0% of the oncolytic virus therapy market in 2025, equivalent to USD 0.06 Billion. Germany, France, the United Kingdom, Italy, and Spain are the main countries because EMA advanced therapy medicinal product rules, national cancer plans, and melanoma treatment centers support hospital-administered viral immunotherapy. Europe has lower commercial penetration than the United States because reimbursement pathways are country-specific and injectable viral products require biosafety training. Replimune and Candel trial activity across European centers has kept investigator interest active despite the U.S. regulatory setback for RP1.

Asia Pacific: Asia Pacific captured 25.6% of the oncolytic virus therapy market in 2025, or USD 0.06 Billion, and is forecast to post the fastest 17.1% CAGR through 2034. China and Japan lead regional revenue because H101 is approved in China and Delytact is approved in Japan for malignant glioma under conditional and time-limited rules. South Korea, Australia, and India contribute trial enrollment and manufacturing capability rather than large commercial revenue. Asia Pacific's structural advantage is regulatory precedent, because China and Japan already operate approved viral therapy channels.

Latin America: Latin America represented 4.5% of the oncolytic virus therapy market in 2025, equal to USD 0.01 Billion. Brazil, Mexico, Argentina, and Chile provide the main hospital demand, but most access occurs through trials, named-patient pathways, or imported oncology products. Brazil's cancer-center networks and private oncology hospitals are likely first adopters when additional viral products receive U.S., EU, or Japanese approvals. Regional growth trails Asia Pacific because live-virus storage, clinician training, and reimbursement budgets limit near-term adoption.

Middle East & Africa: Middle East and Africa held 3.0% of the oncolytic virus therapy market in 2025, equal to USD 0.01 Billion. Saudi Arabia, the United Arab Emirates, Israel, South Africa, and Turkey form the practical demand base because tertiary cancer centers can manage biologic handling and interventional oncology procedures. Israel contributes scientific depth in immuno-oncology and viral-vector research, while Gulf markets provide high-value private oncology procurement. Adoption remains limited because procurement teams must justify live-virus pharmacy infrastructure for a therapy class with few approved indications.

Country Analysis

The oncolytic virus therapy market at country level is led by the United States, China, Japan, and Germany, because these markets combine approved-product access, clinical-trial density, and advanced therapy regulation.

United States: The United States oncolytic virus therapy market reached USD 0.085 Billion in 2025 and is forecast to grow at a 14.8% CAGR through 2034. Demand is anchored by FDA-approved Imlygic, active CBER biologics review pathways, and U.S. oncology centers enrolling patients in RP1, cretostimogene, CAN-2409, Olvi-Vec, pelareorep, and Calidi programs. FDA's second RP1 complete response letter in April 2026 made randomized evidence a procurement and investor requirement. CG Oncology's cretostimogene BLA path and Candel's USD 100 Million February 2026 financing create the highest near-term domestic upside.

China: China's oncolytic virus therapy market reached approximately USD 0.030 Billion in 2025 and is projected to advance at an 18.4% CAGR through 2034. Shanghai Sunway Biotech's H101 gives China the longest commercial precedent for adenovirus-based oncolytic treatment. Domestic hospitals, provincial oncology networks, and university-affiliated cancer centers support intratumoral H101 use and new studies in hepatocellular carcinoma, head and neck cancers, and bladder cancer. China's advantage is practical viral-manufacturing capacity, but international revenue depends on trial data that meet FDA, EMA, and PMDA expectations.

Japan: Japan's oncolytic virus therapy market reached approximately USD 0.024 Billion in 2025 and is forecast to grow at a 13.5% CAGR through 2034. Daiichi Sankyo's Delytact established the country's first approved oncolytic virus therapy for malignant glioma under conditional and time-limited approval. Japanese adoption is concentrated in neuro-oncology centers capable of managing surgical delivery, viral handling, and post-administration monitoring. PMDA's regenerative medical product framework provides a route for highly specialized viral therapies, but the small glioma patient pool caps near-term revenue.

Germany: Germany's oncolytic virus therapy market reached approximately USD 0.018 Billion in 2025 and is forecast to expand at a 12.9% CAGR through 2034. Demand is concentrated in university hospitals, melanoma centers, and advanced therapy units familiar with EMA biologics and ATMP requirements. German centers participate in multinational immuno-oncology trials, while statutory reimbursement assessment slows fast uptake after approval. The country's opportunity is high-value controlled use, because procedure-based oncology delivery can be integrated into certified cancer centers with pharmacy and biosafety capability.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Virus Type

- Herpes Simplex Virus (HSV)

- Adenovirus

- Reovirus

- Others

By Application

- Melanoma

- Lung Cancer

- Breast Cancer

- Others

By Delivery Route

- Intratumoral

- Intravenous

- Others

By End-User

- Hospitals

- Cancer Research Institutes

- Specialty Clinics

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.23 B |

| Forecast Revenue (2034) | USD 0.82 B |

| CAGR (2025-2034) | 15.2% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Virus Type, (Herpes Simplex Virus (HSV), Adenovirus, Reovirus, Others), By Application, (Melanoma, Lung Cancer, Breast Cancer, Others), By Delivery Route, (Intratumoral, Intravenous, Others), By End-User, (Hospitals, Cancer Research Institutes, Specialty Clinics, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AMGEN INC., DAIICHI SANKYO CO., LTD., SHANGHAI SUNWAY BIOTECH CO., LTD., CG ONCOLOGY, INC., REPLIMUNE GROUP, INC., CANDEL THERAPEUTICS, INC., GENELUX CORPORATION, ONCOLYTICS BIOTECH INC., IMUGENE LIMITED, CALIDI BIOTHERAPEUTICS, INC., THERIVA BIOLOGICS, INC., VYRIAD, INC., TILT BIOTHERAPEUTICS LTD., ASCEND BIOPHARMACEUTICALS LTD., BINHUI BIOPHARMACEUTICAL CO., LTD., HANGZHOU CONVERD CO., LTD., EPICENTRX, INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Melanoma, Lung Cancer, Breast Cancer), By Delivery Route (Intratumoral, Intravenous), By End-User (Hospitals, Research Institutes) Region, Key Players – Dynamics, Immuno-Oncology & Cancer Immunotherapy Trends & Forecast 2026-2034")

, By Application (Melanoma, Lung Cancer, Breast Cancer), By Delivery Route (Intratumoral, Intravenous), By End-User (Hospitals, Research Institutes) Region, Key Players – Dynamics, Immuno-Oncology & Cancer Immunotherapy Trends & Forecast 2026-2034")

, By Application (Melanoma, Lung Cancer, Breast Cancer), By Delivery Route (Intratumoral, Intravenous), By End-User (Hospitals, Research Institutes) Region, Key Players – Dynamics, Immuno-Oncology & Cancer Immunotherapy Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Oncolytic Virus Therapy Market?

Global Oncolytic Virus Therapy Market was valued at USD 0.20 billion in 2024 and is projected to reach USD 0.82 billion by 2034, at a CAGR of 15.2% during 2026–2034.

Who are the major players in the Oncolytic Virus Therapy Market?

AMGEN INC., DAIICHI SANKYO CO., LTD., SHANGHAI SUNWAY BIOTECH CO., LTD., CG ONCOLOGY, INC., REPLIMUNE GROUP, INC., CANDEL THERAPEUTICS, INC., GENELUX CORPORATION, ONCOLYTICS BIOTECH INC., IMUGENE LIMITED, CALIDI BIOTHERAPEUTICS, INC., THERIVA BIOLOGICS, INC., VYRIAD, INC., TILT BIOTHERAPEUTICS LTD., ASCEND BIOPHARMACEUTICALS LTD., BINHUI BIOPHARMACEUTICAL CO., LTD., HANGZHOU CONVERD CO., LTD., EPICENTRX, INC., OTHERS

Which segments covered the Oncolytic Virus Therapy Market?

By Virus Type, (Herpes Simplex Virus (HSV), Adenovirus, Reovirus, Others), By Application, (Melanoma, Lung Cancer, Breast Cancer, Others), By Delivery Route, (Intratumoral, Intravenous, Others), By End-User, (Hospitals, Cancer Research Institutes, Specialty Clinics, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oncolytic Virus Therapy Market

Published Date : 18 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date