- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Online Alternative Finance Market Size 2025–2034 | CAGR 20.1%

Global Online Alternative Finance Market Size, Share, Growth & Analysis By Type (Peer-to-Peer Lending, Crowdfunding, Invoice Trading, Supply Chain Finance, Others), By End-Use (Individuals, SMEs, Large Enterprises), By Platform Model (Marketplace Lending, Direct Lending, Hybrid Models), By Region & Key Players – Industry Overview, Market Dynamics, Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2025–2034

Report Overview

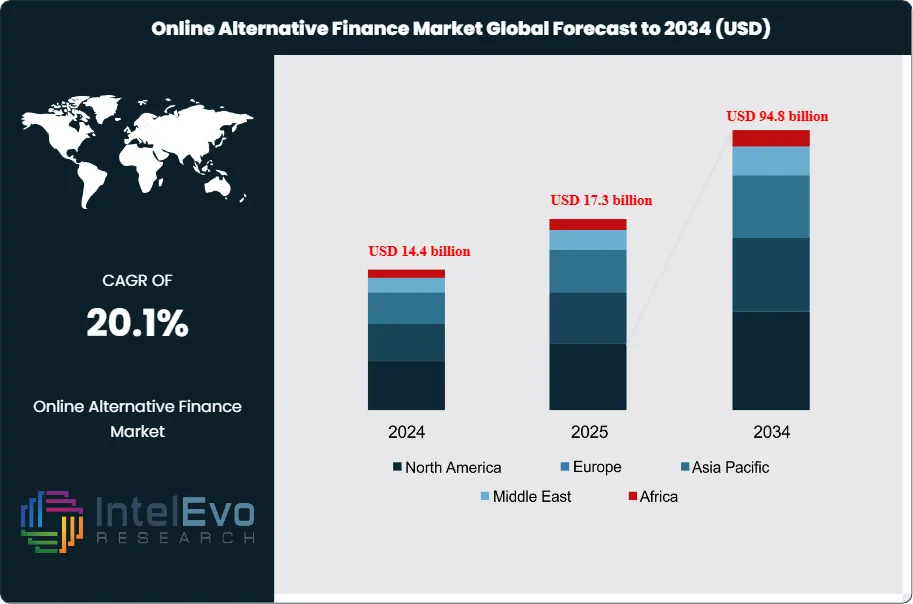

The Online Alternative Finance Market will likely reach about USD 17.3 billion by 2025. It is expected to grow to around USD 94.8 billion by 2034, with a strong CAGR of about 20.1% from 2026 to 2034. This growth is fuelled by the increasing use of digital lending platforms. More retail and institutional investors are getting involved. Traditional banks are tightening credit, which also influences this market. The rising use of AI for credit assessment, quicker loan approval processes, and better access in underbanked areas enhance platform growth. As regulations become clearer and data-based risk management improves, online alternative finance should become more integrated within global financial systems.

Get More Information about this report -

Request Free Sample ReportOnline alternative finance comprises digital platforms that provide lending, crowdfunding, invoice trading, and crypto-enabled services outside traditional banking channels. These models connect funders directly with borrowers and enterprises, compress intermediation layers, and lower transaction costs, which supports rapid scale-up across both mature and emerging economies.

Growth momentum reflects strong demand from small businesses, start-ups, and individual borrowers that face tighter underwriting standards in conventional credit markets. Platforms use streamlined onboarding, automated credit decisioning, and flexible repayment structures to expand access to capital for users with thin or uneven credit files. On the supply side, retail and institutional investors seek yield premia versus traditional deposits and fixed income, which sustains liquidity and product innovation across peer-to-peer lending, revenue-based finance, and specialized working-capital solutions.

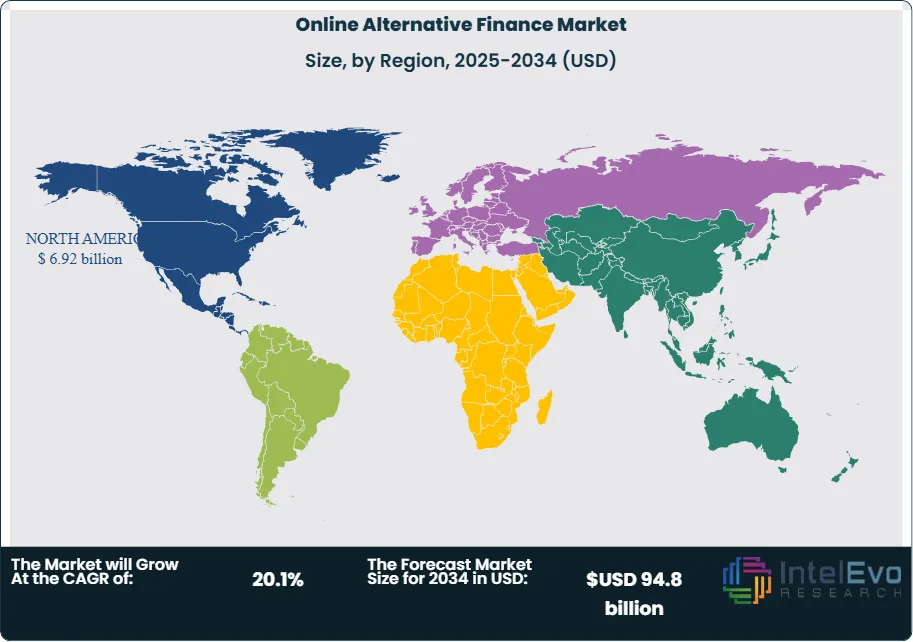

North America accounted for over 45% of global revenues in 2023, or around USD 5.5 Billion, anchored by a deep fintech ecosystem and supportive capital markets. Europe continues to expand under open-banking and data-sharing regimes, while Asia Pacific is emerging as the fastest-growing region, supported by high smartphone penetration, large underbanked populations, and increasingly pro-fintech regulatory sandboxes. Developing markets in Latin America, the Middle East, and Africa offer new growth runways where traditional banking infrastructure remains fragmented.

Technology acts as a primary differentiator. Platforms deploy artificial intelligence, machine learning, and advanced analytics to refine risk models, detect fraud in real time, and personalize pricing. Automation and digital identity tools compress processing times from weeks to minutes, improve user experience, and reduce operating cost per loan. At the same time, rising cyber threats, data-privacy obligations, and evolving licensing rules introduce regulatory and compliance risk.

Sustained expansion of the market will depend on regulators balancing innovation with consumer protection and financial stability. Clear prudential standards, consistent disclosure requirements, and harmonized cross-border frameworks can reduce uncertainty for operators and investors. Participants that combine robust risk governance with scalable technology and diversified funding bases are positioned to capture disproportionate value as online alternative finance becomes embedded in mainstream financial systems.

, By End-Use (Individuals, SMEs, Large Enterprises), By Platform Model (Marketplace Lending, Direct Lending, Hybrid Models), By Region & Key Players – Industry Overview, Market Dynamics, Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Global Online Alternative Finance Market grows from USD 17.3 billion by 2025 to USD 94.8 billion by 2034, implying a CAGR of 20.1% from 2026 to 2034.

- Segment Dominance: Peer-to-peer lending holds over 55.0% of total market share, 2023, as borrowers and lenders increasingly transact directly without conventional intermediaries.

- Segment Dominance: The business customer segment contributes 62.0% of overall online alternative finance volume, 2023, underscoring strong corporate demand for non-bank financing channels.

- Driver: Digital platforms that bypass traditional financial intermediaries and accelerate approval processes support rapid adoption, with estimated: 20.0% annual transaction growth, 2024.

- Restraint: Regulatory uncertainty, credit-risk concerns, and evolving compliance requirements limit scale in some jurisdictions, with estimated: 15.0% of potential borrowers constrained by policy or risk controls, 2024.

- Opportunity: Expanding access in underpenetrated small-business and emerging-market segments creates headroom for new platforms and products, with estimated: 10.0 billion USD incremental addressable volume, 2030.

- Trend: Platforms increasingly apply automation, data analytics, and AI-driven scoring to streamline onboarding and risk assessment, with estimated: 70.0% of leading providers using algorithmic underwriting, 2024.

- Regional Analysis: North America leads the market with more than 45.0% share and about 5.5 billion USD in revenue, 2023, while high-growth regions in Asia Pacific and other developing markets collectively contribute estimated: 30.0% of global volumes, 2024.

Type Analysis

Peer-to-peer lending continues to hold the largest share of the online alternative finance market in 2025. It accounts for more than half of global transactions, supported by strong demand from individuals and businesses seeking direct funding channels that do not use traditional intermediaries. Users value faster decision cycles and transparent pricing. Platforms that focus on small personal loans and SME credit have gained steady traction as borrowing needs rise across major economies.

The segment grows as platforms apply AI-driven scoring models that improve borrower assessment and reduce default risk. Providers use real-time data, behavioral indicators, and automated verification to create more accurate profiles, which increases lender confidence. Market analysts estimate that default rates on leading P2P platforms have dropped by 6 to 10 percent since 2022, improving platform credibility and widening participation among new lenders.

Crowdfunding, invoice trading, and other categories also expand in 2025. Crowdfunding supports early-stage businesses and creative projects, achieving double-digit annual growth as more users adopt digital fundraising. Invoice trading appeals to SMEs that require working capital and faster liquidity cycles. Several providers report transaction volume increases of more than 20 percent per year, driven by tighter bank lending conditions and steady digital adoption among small firms.

Application Analysis

Pavers, retaining walls, and related applications see growing use of online funding channels as project owners shift towards platforms that provide faster access to capital. Demand rises in regions where construction cycles accelerate and traditional lenders apply stricter approval filters. Project developers use online platforms to secure short-term funding for material procurement and contractor payments, which improves workflow continuity.

Retaining wall projects, often tied to infrastructure and land development, show increased interest in P2P and invoice-based financing as these projects require staged disbursements. Platforms that specialize in construction-related financing report higher application activity from small contractors who prefer predictable approval times and flexible repayment structures. Other applications, including landscaping and urban development projects, also integrate online finance for equipment purchases and service contracts.

Growth in this category reflects broader sector needs rather than large-ticket lending. Most transactions fall within small to mid-sized project budgets, making online finance suitable for rapid approval and moderate risk levels. Industry data from 2024 and 2025 indicates steady adoption as project owners favor digital models over conventional loans.

End-Use Analysis

Businesses remain the primary users of online alternative finance in 2025, accounting for close to two-thirds of total market activity. SMEs rely on these platforms to address cash flow gaps and project-based financing as banks continue to apply conservative credit policies. These firms value short processing cycles, minimal documentation, and a wider mix of funding models including P2P, crowdfunding, and invoice trading.

Early-stage businesses use online channels to support asset purchases, payroll coverage, and expansion projects. Many of them face high rejection rates from conventional lenders, which increases reliance on digital platforms. Large enterprises also participate, although at a smaller scale, mainly using invoice trading to improve working capital positions or support supplier financing.

Individual borrowers form the second major segment. They use P2P platforms for personal loans, medical expenses, education-related financing, and debt consolidation. Adoption climbs in markets with widening credit card debt, stricter bank lending, or limited access to traditional credit products. Average ticket sizes remain low compared with business loans, but overall transaction volume continues to rise.

Regional Analysis

North America maintains the largest regional share of the online alternative finance market in 2025. The region accounts for more than 40 percent of global revenue, supported by high digital adoption, a mature fintech environment, and users who are comfortable with non-bank financial tools. The United States leads regional activity, driven by strong participation from SMEs and a well-established technology base. Canada sees steady growth as regulatory bodies refine guidelines for online lending and crowdfunding.

Europe follows with stable expansion across major markets, including the United Kingdom, Germany, and the Nordic countries. Open banking frameworks and standardized digital identity systems support market activity. European SMEs use invoice trading and P2P lending to manage cross-border operations and diversified supply chains. Southern Europe records faster growth rates as smaller businesses transition to online funding options.

Asia Pacific is the fastest-growing region. Rapid digitization, rising smartphone penetration, and large unbanked populations support strong platform adoption in China, India, Indonesia, and the Philippines. Local providers scale quickly due to high loan demand and supportive regulatory sandboxes. Latin America and the Middle East & Africa show steady momentum, driven by financial inclusion programs and increasing interest from global fintech investors.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Peer-to-Peer Lending

- Crowdfunding

- Invoice Trade

- Others

By End-Use

- Individual

- Businesses

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 17.3 billion |

| Forecast Revenue (2034) | USD 94.8 billion |

| CAGR (2025-2034) | 20.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Peer-to-Peer Lending, Crowdfunding, Invoice Trade, Others), By End-Use (Individual, Businesses) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Prosper Marketplace, Upstart, Funding Circle, Kiva, SoFi, StreetShares, Peerform, ZOPA, Lending Club, Kickstarter, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use (Individuals, SMEs, Large Enterprises), By Platform Model (Marketplace Lending, Direct Lending, Hybrid Models), By Region & Key Players – Industry Overview, Market Dynamics, Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By End-Use (Individuals, SMEs, Large Enterprises), By Platform Model (Marketplace Lending, Direct Lending, Hybrid Models), By Region & Key Players – Industry Overview, Market Dynamics, Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By End-Use (Individuals, SMEs, Large Enterprises), By Platform Model (Marketplace Lending, Direct Lending, Hybrid Models), By Region & Key Players – Industry Overview, Market Dynamics, Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Online Alternative Finance Market?

The Online Alternative Finance Market is projected to grow from USD 17.3 billion in 2025 to USD 94.8 billion by 2034, expanding at a CAGR of 20.1% during 2026–2034, driven by digital lending, AI-based credit assessment, and rising demand from underbanked regions.

Who are the major players in the Online Alternative Finance Market?

Prosper Marketplace, Upstart, Funding Circle, Kiva, SoFi, StreetShares, Peerform, ZOPA, Lending Club, Kickstarter, Other Key Players

Which segments covered the Online Alternative Finance Market?

By Type (Peer-to-Peer Lending, Crowdfunding, Invoice Trade, Others), By End-Use (Individual, Businesses)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Online Alternative Finance Market

Published Date : 31 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date