- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Open Banking API Platform Market Size, Share | CAGR 26.1%

Global Open Banking API Platform Market Size, Share, Growth Analysis By Component (API Management & Gateway, Developer Portal & Sandbox, Consent & Identity Management, Analytics & Monetization), By Service Type (AIS, PIS, Open Finance Data Services), By Deployment (Cloud-Native SaaS, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 5.36 Billion | USD 43.18 Billion | 26.1% | Europe, 36.2% |

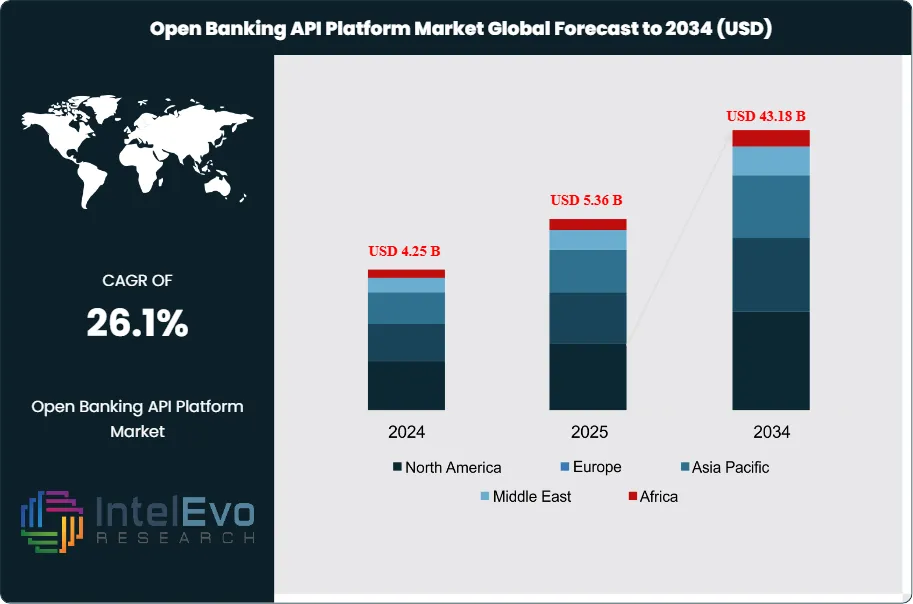

The Open Banking API Platform Market was valued at approximately USD 4.25 Billion in 2024 and reached USD 5.36 Billion in 2025. The market is projected to grow to USD 43.18 Billion by 2034, expanding at a CAGR of 26.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 37.82 Billion over the analysis period, establishing Open Banking API Platforms as one of the most consequential infrastructure investments in the global financial services technology sector.

Get More Information about this report -

Request Free Sample ReportOpen Banking API Platforms are the technology middleware and management infrastructure that enable banks, credit unions, and licensed third-party providers (TPPs) to securely share consumer and business financial data and initiate payment transactions through standardized application programming interfaces, subject to explicit customer consent. The platform layer encompasses API gateway management, developer portal operations, consent and identity management, security and encryption, analytics and monetization tooling, and sandbox testing environments. These platforms sit at the intersection of regulatory mandate, competitive strategy, and customer experience, as banks that deploy robust open banking infrastructure unlock revenue from API monetization, reduce the cost of digital product development, and retain customer relationships that would otherwise migrate to fintech challengers offering superior data-driven financial services.

Open Banking API Platform market growth is propelled by four structural forces. Regulatory mandates are the foundational driver: the EU's revised Payment Services Directive (PSD2), fully enforced from 2020 and now supplemented by PSD3 consultations that will expand open finance scope, requires all EU payment service providers to expose account information and payment initiation APIs to licensed TPPs. The UK's Open Banking Implementation Entity framework, mandated by the Competition and Markets Authority, has produced the world's most technically standardized open banking ecosystem, with over 11 million active open banking users as of 2025. Brazil's Open Finance framework, administered by Banco Central do Brasil, has expanded beyond open banking into open insurance and open investment data, creating one of the world's broadest open finance regulatory perimeters. India's Account Aggregator framework, backed by the Reserve Bank of India, has enrolled over 80 million financial information users, making it the world's largest open finance consent network by user count. Beyond regulatory mandates, competitive pressure from neobanks, embedded finance platforms, and big technology companies entering financial services is compelling incumbent banks to modernize their API infrastructure to match the developer experience and data accessibility of technology-native competitors.

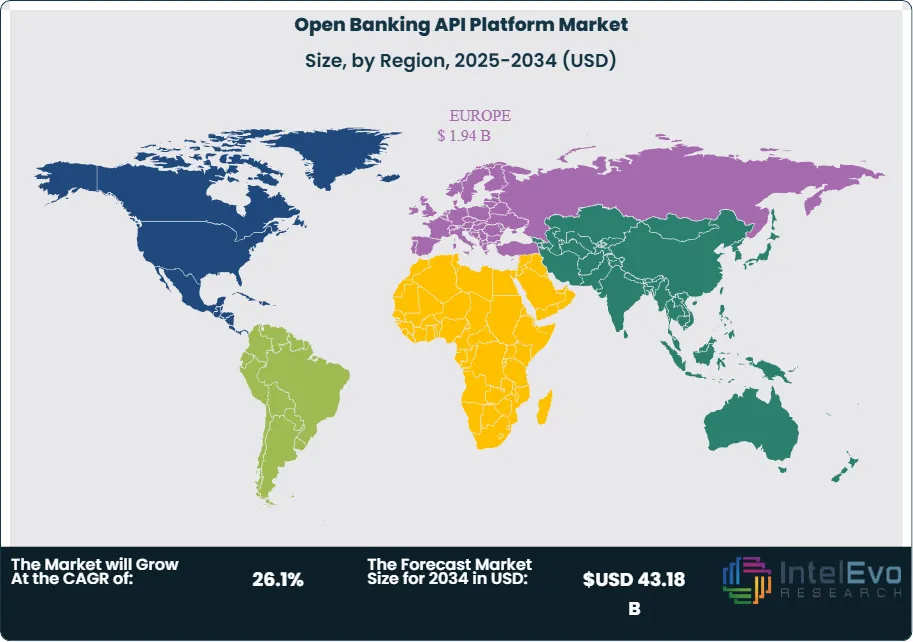

Europe leads global market revenue at 36.2% in 2025, approximately USD 1.94 Billion, reflecting PSD2's seven-year head start in creating regulatory demand for API platform investment and the commercial sophistication of the European TPP ecosystem. North America holds a 28.7% share, driven by market-led open banking adoption in the United States following the Consumer Financial Protection Bureau's Section 1033 open banking rule finalized in October 2024, and by Canada's advancing open banking framework implementation. Asia Pacific accounted for 24.6% of global Open Banking API Platform revenue in 2025, with India's Account Aggregator network, Australia's Consumer Data Right, and Singapore's SGFinDex framework as the leading institutional platforms. The competitive environment is intensifying as API management platform vendors, cloud hyperscalers, and banking software providers converge on the open banking infrastructure market from adjacent positions, competing with specialist open banking platform vendors for bank enterprise contracts.

The Open Banking API Platform is at an inflection point where the initial regulatory compliance deployment phase is giving way to commercial API monetization and open finance expansion. Banks that implemented minimum viable PSD2 and PSD3 compliance APIs are now investing in premium developer portals, API product management capabilities, and consent analytics that convert regulatory obligations into commercial API revenue streams. The emergence of open finance, which extends open banking data sharing to investments, insurance, pensions, and mortgage products, is substantially expanding the API surface area requiring platform management and creating new platform capability requirements for consent granularity, data schema standardization, and liability management across a broader range of financial products.

, By Service Type (AIS, PIS, Open Finance Data Services), By Deployment (Cloud-Native SaaS, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global Open Banking API Platform market reached USD 5.36 Billion in 2025 and is forecast to reach USD 43.18 Billion by 2034, expanding at a CAGR of 26.1% over the 2026–2034 forecast period.

- Segment Dominance: By component, API management and gateway solutions held the largest share at 38.4% of global Open Banking API Platform revenue in 2025, reflecting the foundational role of API lifecycle management, traffic routing, rate limiting, and security enforcement infrastructure in any open banking deployment, regardless of bank size or regulatory jurisdiction.

- Segment Dominance: By end-user, retail and commercial banks represented the dominant demand segment at 62.3% of global market revenue in 2025, as the regulated entities bearing the primary API exposure obligation under PSD2, Section 1033, and analogous frameworks worldwide are the primary platform buyers, supplemented by growing demand from credit unions and building societies subject to the same mandates.

- Driver: Regulatory mandates across 60-plus jurisdictions, anchored by PSD2 in Europe, the CFPB Section 1033 rule in the United States, Banco Central do Brasil's open finance framework, and RBI's Account Aggregator system, are compelling financial institutions to invest in production-grade open banking API infrastructure as a compliance requirement with enforceable timelines and significant non-compliance penalty exposure.

- Restraint: Bank legacy core banking system architecture, with an estimated 43% of global bank assets held on mainframe or COBOL-based core systems, creates API integration complexity and latency challenges that extend Open Banking API Platform deployment timelines by 12–24 months and increase total implementation costs by 30–60% versus greenfield deployments on modern cloud-native banking stacks.

- Opportunity: The expansion from open banking to open finance, encompassing investment account data, insurance policy data, pension information, and mortgage product comparison APIs, is creating a platform capability expansion opportunity estimated at USD 12.4 Billion in incremental platform revenue by 2034 as financial institutions extend their API infrastructure beyond payment accounts to the full breadth of consumer and business financial product data.

- Trend: AI-augmented API intelligence, embedding machine learning models in API gateway and analytics layers to detect anomalous consent usage patterns, predict API performance degradation before customer impact, generate dynamic API documentation, and personalize developer onboarding, is the dominant 2025 platform development trend, with vendors reporting 25–40% improvement in developer time-to-first-call metrics versus non-AI-assisted portal experiences.

- Regional Analysis: Europe leads the global Open Banking API Platform market with a 36.2% share in 2025, representing approximately USD 1.94 Billion, driven by PSD2 regulatory mandates, the UK Open Banking Implementation Entity framework with 11 million active users, and the commercial sophistication of the European TPP ecosystem spanning account aggregation, payment initiation, and credit decisioning.

Competitive Landscape Overview

The global Open Banking API Platform market is moderately fragmented, with the top four vendors, Tink (Visa), TrueLayer, Plaid, and Yapily, collectively accounting for approximately 29.6% of global platform revenue in 2025. Competition operates across two distinct market layers: API platform infrastructure providers serving banks and financial institutions as deploying organizations, and open banking connectivity aggregators serving fintech developers and financial service providers as data and payment API consumers. Several vendors operate across both layers. Competitive differentiation at the bank platform layer centers on regulatory coverage breadth, core banking system integration capability, developer portal quality, and API monetization tooling. At the connectivity aggregator layer, differentiation is driven by bank coverage breadth, data quality and normalization accuracy, payment initiation success rates, and the richness of value-added enrichment services applied to raw bank API data. M&A activity has been substantial: Visa's acquisition of Tink for EUR 1.8 Billion in 2021 and Mastercard's acquisition of Aiia (formerly Openbank) signal payments network interest in controlling open banking infrastructure. Cloud hyperscalers including AWS, Microsoft Azure, and Google Cloud are entering the market through financial services API management tools, increasing competitive pressure on specialist platforms.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Tink (Visa) | Sweden | Leader | Tink Open Banking Platform | Europe | Launched Tink Pay Direct A2A payment product across 12 EU markets; expanded bank coverage to 6,000 European financial institutions (Jan 2025). |

| TrueLayer | UK | Leader | TrueLayer Payment Network | Europe / Australia | Launched Variable Recurring Payments (VRP) commercial product in UK; signed open banking payment integration with Revolut and Klarna (Mar 2025). |

| Plaid | USA | Leader | Plaid Data Network | North America / Europe | Reached 8,000 financial institution connections in U.S.; launched Plaid Layer identity verification product reducing app onboarding friction by 60% (Sep 2025). |

| Yapily | UK | Challenger | Yapily Open Banking API | Europe | Signed 5-year API infrastructure contract with HSBC UK for PSD3 compliance platform; expanded to 18 EU member state markets (Dec 2024). |

| Axway | USA | Challenger | Amplify Open Banking Suite | North America / Europe | Launched Amplify AI API Analytics module with predictive consent usage modeling; signed open banking platform contracts with 3 Tier-1 North American banks (Apr 2025). |

| Salt Edge | Moldova | Challenger | Salt Edge Open Banking Platform | Europe / Asia Pacific | Received FCA TPP license; launched Salt Edge Open Finance module covering investment and insurance APIs for EU banks (Jun 2025). |

| Mulesoft (Salesforce) | USA | Challenger | MuleSoft Anypoint for Financial Services | North America / Europe | Launched pre-built open banking accelerator templates for PSD2, Section 1033, and CDR; signed implementation partnership with 12 global systems integrators (Oct 2025). |

| Konsentus | UK | Niche Player | Konsentus TPP Identity Verification | Europe | Extended TPP real-time identity and regulatory status verification to 30 EU markets; processed 2.4B TPP verification checks in 2025 (Jan 2026). |

| Finclude | Singapore | Niche Player | Finclude Open Finance API Gateway | Asia Pacific | Deployed open finance API gateway at two Southeast Asian national banks; certified under MAS API Exchange standards (Feb 2026). |

By Component:

API management and gateway solutions represent the largest component segment of the global Open Banking API Platform at 38.4% of revenue in 2025, approximately USD 2.06 Billion. API gateways perform the core functions of request routing, authentication and authorization enforcement, rate limiting, traffic management, and protocol translation between legacy bank core systems and REST or GraphQL API consumers. For a major bank exposing 200-plus API endpoints to thousands of registered TPP developers, an enterprise API gateway handles millions of API calls daily, applying security policy enforcement at microsecond latency while maintaining the 99.9%-plus availability SLAs required by PSD2 and analogous regulatory standards. Leading API management platforms including Axway's Amplify, MuleSoft's Anypoint, Kong Enterprise, and AWS API Gateway are deployed by banks as the foundational infrastructure layer on which open banking functionality is built. The growing adoption of event-driven API architectures, including webhook notifications for account balance changes and payment status updates, is expanding gateway capability requirements beyond synchronous REST management to include event streaming infrastructure.

Developer portals and sandbox environments accounted for 22.7% of market revenue in 2025, approximately USD 1.22 Billion, reflecting the critical role of developer experience in determining the commercial success of open banking programs. A bank's developer portal is the primary interface through which TPP developers discover, test, and onboard to the bank's API products, and the quality of portal documentation, sandbox data realism, and onboarding support directly determines how many high-quality TPP applications are built on the bank's API infrastructure. The UK's Open Banking Implementation Entity has published developer portal best practice standards that have been adopted as reference benchmarks globally, and commercial portal platforms from vendors including Stoplight, Readme, and Apigee are used by banks to deliver developer experiences competitive with leading technology API programs. Consent and identity management platforms held a 21.4% share, encompassing the technical infrastructure for customer consent journeys, consent storage and audit trails, TPP regulatory status verification, and strong customer authentication (SCA) flows required by PSD2. Analytics and monetization tooling accounted for the remaining 17.5%, covering API usage analytics, revenue attribution, API product packaging, and billing infrastructure for premium API tier monetization.

By Deployment:

Cloud-native SaaS deployment dominates new Open Banking API Platform implementations at 58.6% of new contract value in 2025, approximately USD 3.14 Billion. Cloud-native open banking platforms deliver continuous regulatory update libraries as new API standards from the Berlin Group, UK Open Banking Standards, BIAN, and national regulatory bodies are published, removing the implementation burden of keeping on-premise platform deployments aligned with evolving specification versions. Elastic scaling for API traffic spikes, occurring during high-usage periods including salary payment dates, end-of-month account reconciliation, and peak retail lending application seasons, is substantially simpler in cloud-native architectures than in capacity-constrained on-premise deployments. Regulatory cloud adoption has accelerated significantly since 2023 as bank regulators including the ECB, FCA, and FDIC have published cloud outsourcing guidance frameworks that define acceptable cloud operational resilience standards, removing a previously significant barrier to cloud open banking platform adoption among conservative bank technology committees. On-premise deployment retained a 28.4% share in 2025, concentrated among large incumbent banks with established API infrastructure investments and data residency requirements in markets including China, India, and South Korea. Hybrid architectures, where core banking API integration layers operate on-premise while developer portal, analytics, and monetization capabilities are cloud-hosted, accounted for the remaining 13.0%.

By Service Type:

Account information services (AIS), enabling licensed third parties to access consumer and business bank account data including transactions, balances, and account metadata, represent the most established service category in the Open Banking API Platform at 44.8% of revenue in 2025, approximately USD 2.40 Billion. AIS APIs power the majority of consumer personal finance management applications, credit decisioning platforms, and business accounting software integrations that constitute the open banking use case ecosystem. Plaid's 8,000 U.S. financial institution connections and Tink's 6,000 European institution coverage demonstrate the commercial scale achieved by leading AIS aggregators. Payment initiation services (PIS), enabling TPPs to initiate account-to-account payments directly from consumer and business bank accounts without card network intermediation, accounted for 33.6% of market revenue in 2025 and is the fastest-growing service category at approximately 34% annual growth, driven by merchant adoption of A2A payments as a lower-cost alternative to card payment acceptance. TrueLayer's Variable Recurring Payments product and Tink's Pay Direct demonstrate commercial PIS scale in the UK and European markets. Open finance data services, extending beyond payment account data to investment portfolios, insurance policies, pension statements, and mortgage product information, represented 21.6% of market revenue in 2025 and will be the primary growth driver from 2028 onward as open finance regulatory frameworks supersede open banking mandates globally.

By End-User:

Retail and commercial banks represent the dominant end-user category for Open Banking API Platform platforms at 62.3% of global revenue in 2025, approximately USD 3.34 Billion. As the regulated entities bearing the legal obligation to expose account data and payment initiation APIs under PSD2, Section 1033, CDR, and analogous frameworks, incumbent banks are the primary API platform deployers, investing in platform infrastructure to meet compliance obligations, reduce regulatory risk, and progressively monetize their API products commercially. Tier-1 global banks with large multi-jurisdiction API programs including HSBC, BNP Paribas, ING, and Lloyds Banking Group represent the highest individual platform contract values, while the large population of mid-tier and regional banks in the EU, UK, and North America is expanding the addressable market significantly as minimum viable compliance deployments upgrade to full commercial API programs. Credit unions and building societies accounted for 14.8% of market revenue, fintech and neobanks 13.2%, and non-banking financial institutions including insurance companies and investment platforms held the remaining 9.7% as open finance mandates progressively pull non-bank financial entities into the open data ecosystem.

Regional Analysis

Europe

Europe leads the global Open Banking API Platform market with a 36.2% share in 2025, representing approximately USD 1.94 Billion, driven by the world's longest-established and most comprehensively enforced open banking regulatory framework. PSD2's account information and payment initiation provisions, fully enforced across all EU member states and EEA countries since 2020, created mandatory API exposure obligations for approximately 6,000 payment service providers, generating a sustained wave of compliance and commercial API platform investment. The UK's Open Banking Implementation Entity, mandated by the Competition and Markets Authority as part of the CMA9 remedies applied to the nine largest UK banks, has produced the world's most technically consistent open banking ecosystem, with a single standardized API specification, mandatory developer portal quality standards, and centralized TPP directory and registration infrastructure. The UK reached 11 million active open banking users by mid-2025, with Variable Recurring Payments launched commercially by the UK's largest banks and building societies creating a new payment initiation revenue stream for platform operators. Germany's banking sector, operating through the Berlin Group's NextGenPSD2 standard, France's STET API standard, and the Netherlands' Open Banking implementation, each represent major national API platform markets within the EU. The European Commission's PSD3 legislative proposal and the Financial Data Access (FIDA) regulation, expected to enter force in 2026–2027, will extend open finance obligations to investment accounts, insurance, and pensions, substantially expanding the open banking platform addressable market. The Berlin Group's OpenFinance API Framework is positioning the EU for a technically harmonized open finance transition that will drive another generation of platform investment across European financial institutions.

North America

North America accounted for 28.7% of the global Open Banking API Platform market in 2025, approximately USD 1.54 Billion, with the United States undergoing a fundamental shift from market-led open banking to regulatory mandate following the Consumer Financial Protection Bureau's Section 1033 final rule published in October 2024. The Section 1033 rule, implementing the open banking provision of the Dodd-Frank Act, requires depository institutions above USD 850 Million in assets to provide consumers with electronic access to their financial data through standardized APIs by defined compliance deadlines, with larger institutions subject to earlier compliance dates beginning in 2026. This regulatory mandate converts the U.S. open banking market from a voluntary ecosystem driven by Plaid, Yodlee, and MX Technologies' screen-scraping and API connectivity aggregators into a compliance-driven market requiring banks to invest in production-grade API infrastructure equivalent to PSD2 standards. Financial Data Exchange (FDX), the industry-led standard body with over 200 member institutions managing USD 100 Trillion in financial assets, has developed the FDX API standard that is expected to serve as the technical implementation reference for Section 1033 compliance, with over 71 million consumer accounts already accessible via FDX-compatible APIs as of 2025. Canada's open banking framework, being developed by the Department of Finance following the Advisory Committee on Open Banking's final report, is targeting implementation for 2026, creating a parallel North American compliance investment wave at Canadian banks and credit unions that mirrors the U.S. timeline. The combined North American regulatory mandate market represents the largest single compliance-driven API platform procurement opportunity globally over the 2025–2030 period.

Asia Pacific

Asia Pacific represented 24.6% of the global Open Banking API Platform market in 2025, approximately USD 1.32 Billion, with the region hosting the world's highest-volume open banking consent infrastructure in India's Account Aggregator framework and the most technically sophisticated market-led open banking ecosystem in Australia's Consumer Data Right. India's Account Aggregator system, operating under RBI regulation with nine licensed Account Aggregator entities including Finvu, CAMS FinServ, and Perfios, had enrolled over 80 million financial information users by 2025 and processed approximately 300 million consent artefacts annually, making it the world's largest operational open finance consent network by user count. The AA framework spans banking, insurance, tax, and pension data under the direction of India's Ministry of Finance, with SEBI extending it to securities account data and IRDAI to insurance policy data. Australia's Consumer Data Right, administered by the ACCC and operational for banking from 2020 and energy from 2022, is the world's most expansive sector-agnostic open data framework and has generated significant API platform investment among Australian banks and energy retailers. Singapore's SGFinDex, connecting 11 financial institutions through a government-operated public digital infrastructure layer, enables citizens to retrieve financial data from all participating institutions in a single consent transaction, demonstrating a centralized open banking architecture distinct from the distributed bank-operated API models in Europe and North America. Japan's FSA open API guidelines, covering approximately 1,400 registered bank-fintech API partnerships, and South Korea's myData framework with 52 licensed operators represent additional significant Asia Pacific market segments.

Latin America

Latin America held a 6.3% share of the global Open Banking API Platform market in 2025, approximately USD 338 Million, with Brazil operating the world's most comprehensive open finance regulatory framework by product scope. Banco Central do Brasil's Open Finance Brazil framework, launched in phases from 2021 through 2023, covers banking, payment, credit, investment, insurance, pension, and foreign exchange data, making it the only operational open finance ecosystem with regulatory mandates across the complete spectrum of retail financial products. The framework covers approximately 220 financial institutions and has generated API platform investment across Brazil's large and mid-tier bank population. The Brazilian Open Finance standardization body has published API standards for 11 product categories, with API call volumes exceeding 3 billion per month by early 2025, demonstrating commercial-scale adoption. Mexico's CNBV has implemented open banking provisions under the Fintech Law of 2018, requiring licensed financial entities to enable data portability, though implementation has proceeded more gradually than Brazil's framework. Colombia's financial regulator SFC and Chile's CMF are developing open finance regulatory frameworks modeled on Brazil's approach, with implementation timelines extending into 2026–2028. The Interoperability and inclusion characteristics of Brazil's framework are being studied by regulators in Argentina, Peru, and Ecuador as reference implementations for their own open finance program development.

Middle East & Africa

The Middle East and Africa region accounted for 4.2% of the global Open Banking API Platform market in 2025, approximately USD 225 Million, with Bahrain, the UAE, Saudi Arabia, and South Africa as the primary active markets. Bahrain became the first Gulf country to implement a mandatory open banking framework under the Central Bank of Bahrain's Open Banking Framework published in 2020, covering all retail banks operating in Bahrain and generating API platform investment among Bahrain's financial sector. The UAE's Abu Dhabi Global Market and Dubai International Financial Centre have implemented open banking frameworks for their regulated financial service ecosystems, and the UAE Central Bank's CBUAE Open Finance Framework consultation, published in 2024, signals the UAE's intent to implement a national open finance mandate covering all licensed financial institutions. Saudi Arabia's SAMA has published open banking guidelines and is progressing toward a mandatory framework under Vision 2030's financial sector modernization objectives, with Saudi banks beginning API platform investments in anticipation of regulatory requirements. South Africa's open banking development is market-led, with the Intergovernmental Fintech Working Group and Banking Association South Africa developing voluntary open banking standards, and several South African banks including Capitec and Standard Bank having implemented voluntary open banking API programs. Nigeria's Central Bank has issued open banking guidelines under the National Payments Systems Vision 2025, establishing a regulatory foundation for API platform investment among Nigeria's licensed banks.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- API Management and Gateway

- Developer Portal and Sandbox

- Consent and Identity Management

- Analytics and Monetization

By Deployment

- Cloud-Native SaaS

- On-Premise

- Hybrid

By Service Type

- Account Information Services (AIS)

- Payment Initiation Services (PIS)

- Open Finance Data Services (Investment, Insurance, Pension, Mortgage)

By End-User

- Retail and Commercial Banks

- Credit Unions and Building Societies

- Fintech and Neo-Banks

- Non-Banking Financial Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.36 B |

| Forecast Revenue (2034) | USD 43.18 B |

| CAGR (2025-2034) | 26.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (API Management and Gateway, Developer Portal and Sandbox, Consent and Identity Management, Analytics and Monetization), By Deployment, (Cloud-Native SaaS, On-Premise, Hybrid), By Service Type, (Account Information Services (AIS), Payment Initiation Services (PIS), Open Finance Data Services (Investment, Insurance, Pension, Mortgage)), By End-User, (Retail and Commercial Banks, Credit Unions and Building Societies, Fintech and Neo-Banks, Non-Banking Financial Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TINK (VISA), TRUELAYER, PLAID, YAPILY, AXWAY (AMPLIFY), SALT EDGE, MULESOFT (SALESFORCE), KONSENTUS, FINCLUDE, APIGEE (GOOGLE CLOUD), AWS API GATEWAY (FINANCIAL SERVICES), FINASTRA (OPEN API PLATFORM), BACKBASE, AIIA (MASTERCARD), MX TECHNOLOGIES, YODLEE (ENVESTNET), OPENBANKPROJECT, NORDIC API GATEWAY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Service Type (AIS, PIS, Open Finance Data Services), By Deployment (Cloud-Native SaaS, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

, By Service Type (AIS, PIS, Open Finance Data Services), By Deployment (Cloud-Native SaaS, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

, By Service Type (AIS, PIS, Open Finance Data Services), By Deployment (Cloud-Native SaaS, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Open Banking API Platform Market?

The Global Open Banking API Platform Market was valued at USD 4.25 Billion in 2024 and is projected to reach USD 43.18 Billion by 2034, growing at a CAGR of 26.1% from 2026 to 2034, driven by rising adoption of digital banking services, increasing demand for secure financial data sharing, expanding fintech-bank collaborations, and growing implementation of open banking regulations, embedded finance, and real-time payment ecosystems worldwide.

Who are the major players in the Open Banking API Platform Market?

TINK (VISA), TRUELAYER, PLAID, YAPILY, AXWAY (AMPLIFY), SALT EDGE, MULESOFT (SALESFORCE), KONSENTUS, FINCLUDE, APIGEE (GOOGLE CLOUD), AWS API GATEWAY (FINANCIAL SERVICES), FINASTRA (OPEN API PLATFORM), BACKBASE, AIIA (MASTERCARD), MX TECHNOLOGIES, YODLEE (ENVESTNET), OPENBANKPROJECT, NORDIC API GATEWAY, Others

Which segments covered the Open Banking API Platform Market?

By Component, (API Management and Gateway, Developer Portal and Sandbox, Consent and Identity Management, Analytics and Monetization), By Deployment, (Cloud-Native SaaS, On-Premise, Hybrid), By Service Type, (Account Information Services (AIS), Payment Initiation Services (PIS), Open Finance Data Services (Investment, Insurance, Pension, Mortgage)), By End-User, (Retail and Commercial Banks, Credit Unions and Building Societies, Fintech and Neo-Banks, Non-Banking Financial Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Open Banking API Platform Market

Published Date : 25 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date