- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Oral Biologic Delivery Platform Market Size, Share | CAGR 13.2%

Global Oral Biologic Delivery Platform Market Size, Share & Analysis By Tech (Nanoparticles, Lipid, Polymeric), Molecule (Peptides, mAbs, RNA), Therapy (Diabetes, Oncology, Autoimmune), End-User (Pharma, Biotech, Academic) - Global Region, Key Players, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 4.18 Billion | USD 12.78 Billion | 13.2% | North America, 47.5% |

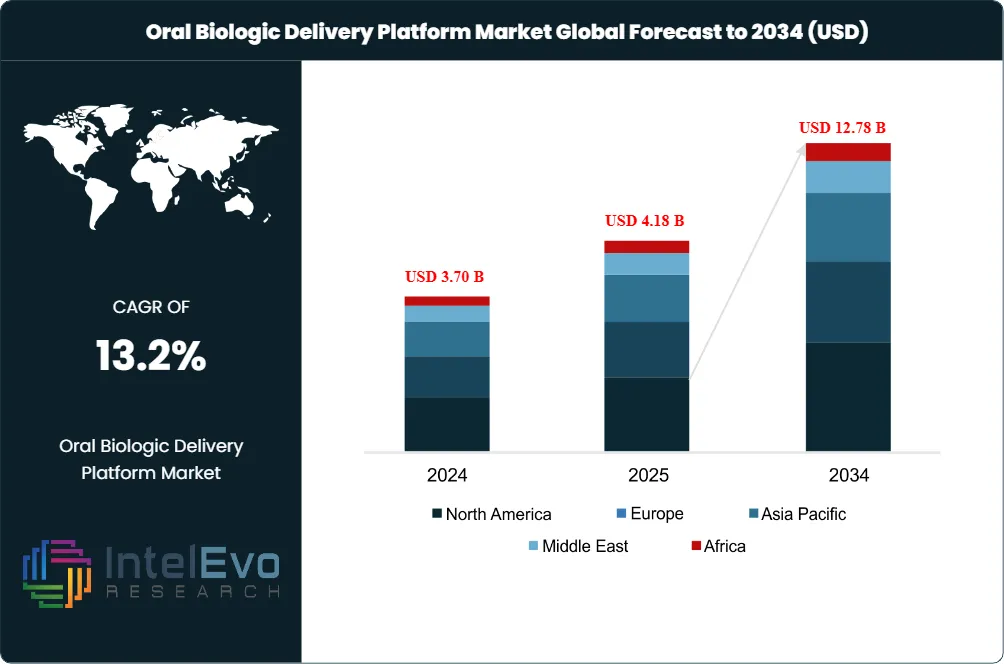

The Oral Biologic Delivery Platform Market was valued at USD 3.70 Billion in 2024 and USD 4.18 Billion in 2025. The market is projected to reach USD 12.78 Billion by 2034, expanding at a CAGR of 13.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.60 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe oral biologic delivery platform market sits at the intersection of pharmaceutical formulation science and device-enabled drug delivery. It encompasses technologies that allow peptides, proteins, antibodies, and vaccines to be administered orally rather than by injection or infusion. Demand momentum accelerated sharply when the FDA approved Rybelsus for cardiovascular risk reduction in adults with type 2 diabetes on October 17, 2025, followed by approval of the Wegovy pill (oral semaglutide 25 mg) for chronic weight management on December 22, 2025. The Wegovy pill demonstrated 16.6% mean weight loss in the Phase III OASIS 4 trial, validating the oral GLP-1 thesis at obesity-grade efficacy and resetting platform valuation multiples.

Regulatory anchors are tightening across the value chain. The FDA's Center for Drug Evaluation and Research now operates standardized review pathways for oral peptide formulations leveraging absorption enhancers such as SNAC (salcaprozate sodium), and the European Medicines Agency reviewed Novo Nordisk's oral semaglutide 25 mg application during the second half of 2025. ICH guidelines on bioequivalence for oral peptide formulations and 21 CFR Part 320 bioavailability rules govern submission expectations. China's NMPA accepted a Marketing Authorization Application from Hefei Tianhui Biotech for oral insulin during 2025, opening a second commercial gateway.

Technology innovation is bifurcating into two competing tracks. The first uses permeation enhancers and enzyme inhibitors integrated into solid oral dosage forms, exemplified by Novo Nordisk's SNAC-enabled tablet platform commercialized through Rybelsus and the Wegovy pill. The second uses device-enabled or precision-formulation approaches to deliver larger biologics including monoclonal antibodies, exemplified by Rani Therapeutics' RaniPill capsule and Vivtex Corporation's GI-ORIS robotics screening system. The Rani-Chugai collaboration of October 17, 2025 valued at up to USD 1.085 Billion validated the device-enabled track as commercially viable for rare-disease antibodies.

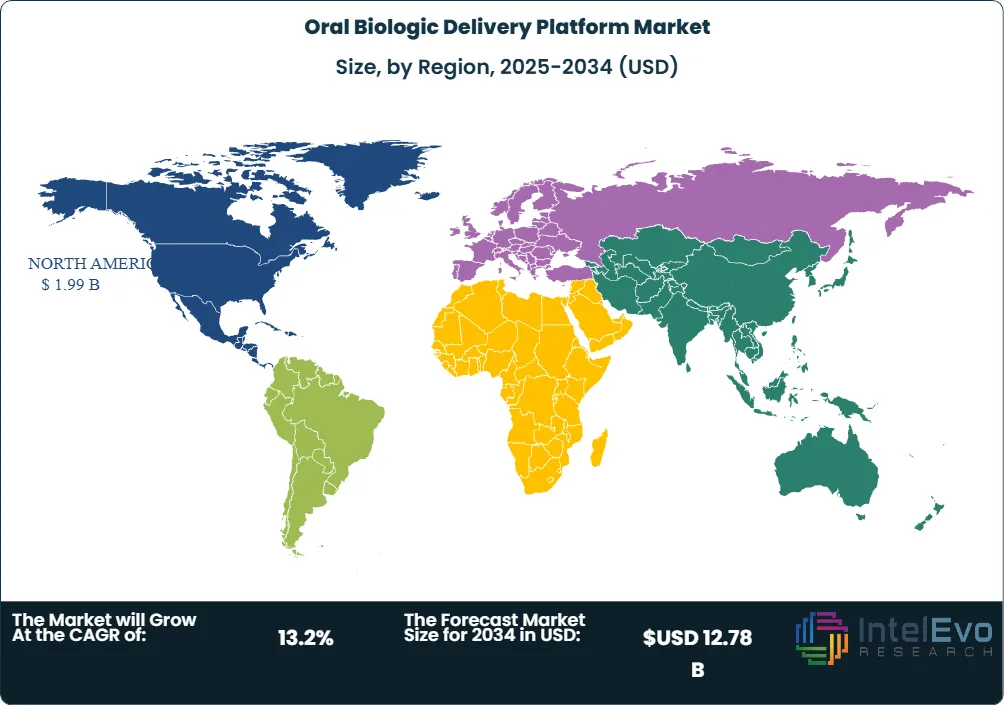

Regionally, North America held 47.5% revenue share in the oral biologic delivery platform market in 2025, anchored by Novo Nordisk Inc.'s United States commercialization of Rybelsus and the Wegovy pill, the FDA's leadership in approving novel oral peptide formats, and concentrated venture funding in Boston, San Francisco, and San Jose. Asia Pacific represented 22.4% share with Japan, China, and South Korea as the principal demand centers. Outlook through 2034 hinges on Phase 3 readouts for oral parathyroid hormone (Entera Bio's EB613 oral PTH(1-34) tablet), oral macrocycles (Orbis Medicines' nCycles), and second-generation device capsules entering registration trials.

Market Definition and Scope

The oral biologic delivery platform market is defined as the technology, formulation, and device ecosystem that enables therapeutic biologics, including peptides, proteins, antibodies, oligonucleotides, and vaccines, to be administered through oral routes with adequate systemic bioavailability. The market encompasses permeation-enhancer-based oral tablets, ingestible robotic capsules, lipid and polymer nanoparticle carriers, mucoadhesive and gastric-retentive systems, and macrocyclic peptide discovery platforms designed to mimic biologic targets with oral pharmacokinetics.

This analysis covers platform licensing revenue, formulation services, device-component supply, and direct product sales attributable to platform IP. It includes Novo Nordisk's SNAC-based tablet, Rani Therapeutics' RaniPill capsule, Entera Bio's N-Tab tablet, Lyndra Therapeutics' LYNX gastric-retentive capsule, Vivtex Corporation's GI-ORIS screening platform, and Vaxart's pill vaccine system. Excluded from this scope are conventional small-molecule oral drug delivery (modified-release tablets and orally disintegrating tablets unrelated to biologics), parenteral biologics with no oral analog in development, and pure CDMO bulk capsule manufacturing without proprietary platform IP. The parent oral drug delivery market exceeds USD 80 Billion in 2025; oral biologic delivery platforms account for approximately 5.2% of that parent.

, Molecule (Peptides, mAbs, RNA), Therapy (Diabetes, Oncology, Autoimmune), End-User (Pharma, Biotech, Academic) - Global Region, Key Players, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The oral biologic delivery platform market expanded from USD 4.18 Billion in 2025 toward a projected USD 12.78 Billion by 2034, registering a CAGR of 13.2% during the forecast period.

- Segment Dominance by Technology: Permeation-enhancer-based oral tablets, led by SNAC (salcaprozate sodium) formulations, captured approximately 38.4% share in 2025 due to Rybelsus and Wegovy pill commercial scale.

- Segment Dominance by Therapeutic Area: Cardiometabolic indications, including type 2 diabetes and obesity, represented 56.7% of platform value in 2025, driven by GLP-1 receptor agonist demand.

- Driver: Approval of the Wegovy pill on December 22, 2025 expanded the obesity oral GLP-1 category to a 13.6% mean weight-loss benchmark in Phase III OASIS 4, materially raising platform valuation multiples and partner-deal economics.

- Restraint: Native oral bioavailability of unmodified peptides remains 0% to 2%, requiring permeation enhancers, enzyme inhibitors, or capsule devices that can add USD 0.50 to 2.00 per dose to manufacturing cost and complicate scale-up.

- Opportunity: Oral conversion of injectable monoclonal antibodies represents an addressable opportunity exceeding USD 30 Billion in source-injectable revenue, validated by the Rani-Chugai collaboration up to USD 1.085 Billion in October 2025.

- Trend: Strategic alliances between platform developers and large-pharma sponsors increased meaningfully through 2025-2026, with Novo Nordisk-Vivtex (up to USD 2.1 Billion, February 2026) and Rani-Chugai (up to USD 1.085 Billion, October 2025) anchoring deal flow.

- Regional: North America held the largest regional share at 47.5%, equating to approximately USD 1.99 Billion in 2025, with the United States contributing the bulk via roughly 3.2 million Rybelsus prescriptions to date.

Key Insights Summary

- Oral semaglutide 14 mg reduced major adverse cardiovascular events by 14% versus placebo across 9,650 patients in the SOUL trial, with results published in the New England Journal of Medicine in May 2025 (NEJM 2025; 392:2001-2012) and supporting FDA approval on October 17, 2025.

- The Wegovy pill (oral semaglutide 25 mg) achieved 16.6% mean weight loss at 64 weeks under full adherence in the Phase III OASIS 4 trial, with FDA approval granted December 22, 2025 and US commercial launch in early January 2026 at USD 149 per month for the starting dose.

- Rani Therapeutics initiated a Phase 1 study of RT-114, a GLP-1/GLP-2 dual agonist delivered via the RaniPill capsule, in December 2025 with bioequivalence to subcutaneous administration demonstrated preclinically across four incretin-based molecules.

- Entera Bio's EB613 oral PTH(1-34) tablet showed cortical bone improvements comparable to injectable teriparatide and abaloparatide after six months of treatment in 161 postmenopausal women, presented at the ASBMR 2025 Annual Meeting in Seattle, Washington in September 2025.

- Vivtex Corporation's GI-ORIS robotic screening platform, published in Nature Biomedical Engineering, demonstrated near-perfect correlation with human intestinal absorption and supported a partnership with Novo Nordisk worth up to USD 2.1 Billion announced February 25, 2026.

- Approximately 11 of 102 FDA-approved peptide drugs are administered orally as of 2025, indicating a structural underpenetration of the oral route across approved peptide therapeutics and a multi-decade conversion runway.

Competitive Landscape Overview

The oral biologic delivery platform market is moderately consolidated with concentrated leadership at the top tier. The combined share of the top four players, Novo Nordisk A/S, Eli Lilly and Company, Rani Therapeutics Holdings, Inc., and Entera Bio Ltd., reached approximately 58% of platform-attributable value in 2025. Competition is technology-led rather than price-led, with three distinct technology tracks competing across modalities: permeation-enhancer tablets (Novo Nordisk's SNAC platform), device-enabled robotic capsules (Rani Therapeutics' RaniPill), and oral macrocycle discovery platforms (Orbis Medicines and Pinnacle Medicines). The competitive frontier is shifting from formulation science alone to combined platform-plus-asset partnerships, illustrated by Novo Nordisk's USD 2.1 Billion Vivtex agreement in February 2026 and Rani's USD 1.085 Billion Chugai collaboration in October 2025. New entrants include Vivtex Corporation, Pinnacle Medicines, and Orbis Medicines, each backed by leading life-science investors including New Enterprise Associates, OrbiMed, and Novo Holdings.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

| Novo Nordisk A/S | Bagsvaerd, Denmark | Leader | SNAC oral tablet (Rybelsus, Wegovy pill) | North America, Europe | Wegovy pill FDA approval, December 22, 2025 |

| Eli Lilly and Company | Indianapolis, USA | Leader | Orforglipron oral GLP-1 | North America, Global | Orforglipron NDA submission under FDA priority voucher, 2025 |

| Rani Therapeutics Holdings, Inc. | San Jose, USA | Challenger | RaniPill capsule device | North America, Japan | Chugai collaboration up to USD 1.085 Billion, October 2025 |

| Entera Bio Ltd. | Jerusalem, Israel | Niche Player | N-Tab oral peptide platform (EB613) | United States, Israel | Phase 3 EB613 protocol submission to FDA, March 2026 |

| Vivtex Corporation | Boston, USA | Challenger | GI-ORIS robotics screening platform | United States | Novo Nordisk deal up to USD 2.1 Billion, February 2026 |

| OraTech Pharmaceuticals Inc. | New York, USA | Niche Player | POD oral protein delivery | United States, China | OraTech JV launched February 2025; NMPA filing in China |

| Orbis Medicines | Copenhagen, Denmark | Niche Player | nGen platform; nCycles oral macrocycles | Europe | Series A EUR 90 Million closed January 6, 2025 |

| Pinnacle Medicines | Doylestown, USA & Shanghai | Niche Player | AI-physics oral peptide platform | United States, China | Series B USD 89 Million closed March 26, 2026 |

| OPKO Health, Inc. | Miami, USA | Niche Player | Long-acting PTH oral tablet (with Entera) | United States, Israel | LA-PTH partnership expansion, February 4, 2026 |

By Technology Platform

The oral biologic delivery platform market by technology platform is led by permeation-enhancer-based oral tablets, which captured approximately 38.4% share in 2025. SNAC (salcaprozate sodium) tablets pioneered by Novo Nordisk through the Emisphere Technologies acquisition anchor this segment, with Rybelsus generating prescription volume of approximately 3.2 million in the United States since launch. Permeation enhancers facilitate transcellular peptide absorption across intestinal epithelium, raising oral bioavailability from sub-1% baseline to 1% to 2% systemic exposure. Manufacturing scale advantages and regulatory familiarity favor the segment, though the approach is constrained to peptides with favorable physicochemical properties.

Device-enabled capsules represented approximately 16.8% of segment value in 2025, anchored by Rani Therapeutics' RaniPill, which deploys a self-orienting microneedle in the small intestine to inject peptides through the intestinal wall. Preclinical data presented at ObesityWeek 2025 in Atlanta, Georgia in November 2025 demonstrated that orally delivered semaglutide via RaniPill achieved bioavailability and weight-loss outcomes comparable to subcutaneous administration. The Chugai collaboration of October 2025 validated this approach commercially. Lyndra Therapeutics' LYNX gastric-retentive platform also occupies this segment, although Lyndra began winding down operations in March 2025.

Nanoparticle and lipid carrier systems accounted for 21.6% share in 2025, with academic and CDMO-driven innovation in solid lipid nanoparticles, nanostructured lipid carriers, and PLGA polymer formulations. Approximately 60% of new oral drug delivery research uses nanocarrier platforms, per peer-reviewed pharmaceutical research published in 2025. Macrocyclic peptide discovery platforms, including Orbis Medicines' nGen system and Pinnacle Medicines' AI-physics platform, captured 12.5% share in 2025. Engineered biologic and gastric-retentive systems made up the remaining 10.7%.

By Molecule Type

The oral biologic delivery platform market by molecule type is dominated by peptides, which accounted for approximately 64.3% share in 2025. GLP-1 receptor agonists, including semaglutide, orforglipron, and PG-102, drive volume. Parathyroid hormone analogs (EB613, EB612), oxyntomodulin (EB618), and somatostatin analogs add depth. Proteins, including insulin and growth hormone, captured 18.7% share, anchored by OraTech Pharmaceuticals' ORMD-0801 oral insulin program (Phase 3 enrollment of 710 patients) and HTIT's Marketing Authorization Application in China. Monoclonal antibodies represented 9.4% share, growing fastest as device-enabled platforms mature; the Rani-Chugai program targeting an oral rare-disease antibody is the lead clinical asset. Vaccines, primarily through Vaxart Inc.'s recombinant pill platform, contributed 7.6% in 2025. Peptide platforms hold a 3.4x revenue advantage over protein platforms because absorbed peptide mass per dose can clear approved efficacy thresholds, whereas oral insulin still requires variable-dose calibration that increases regulatory friction.

By Therapeutic Area

The oral biologic delivery platform market by therapeutic area is led by cardiometabolic indications at 56.7% share in 2025, encompassing type 2 diabetes, obesity, dyslipidemia, and cardiovascular risk reduction. The October 17, 2025 FDA approval of Rybelsus for MACE reduction and the December 22, 2025 approval of the Wegovy pill expanded eligible patient populations meaningfully. Bone and endocrine disorders captured 12.4% share, driven by oral PTH programs for postmenopausal osteoporosis and hypoparathyroidism, where injectable adoption is suppressed by patient burden. Immunology and inflammation accounted for 14.2% share, with oral cyclic peptides such as icotrokinra (JNJ-77242113), co-developed by Johnson and Johnson and Protagonist Therapeutics and submitted to the FDA in July 2025 for plaque psoriasis. Rare diseases held 8.1% share given the small-population economics that justify higher-cost device approaches. Vaccines and infectious disease comprised 5.4%, while oncology trailed at 3.2% as antibody-drug conjugate oral routes remain preclinical.

By End-User

The oral biologic delivery platform market by end-user is led by global pharmaceutical sponsors at 61.2% share in 2025, including Novo Nordisk, Eli Lilly, Pfizer, AbbVie, F. Hoffmann-La Roche, and Johnson and Johnson. These sponsors license platforms or acquire developers to convert injectable assets to oral. Mid-cap and specialty biotech firms held 24.5% share, including Rani Therapeutics, Entera Bio, Pinnacle Medicines, Vivtex, and Orbis Medicines. CDMOs and contract research organizations captured 10.6% share, including Thermo Fisher Scientific Inc., Lonza Group AG, and Evonik Industries AG, which launched EUDRACAP colon-targeted capsules in September 2024. Academic and government institutions accounted for the residual 3.7% share. For procurement leads evaluating oral biologic delivery platform vendors, the selection checklist should weight peptide-versus-protein cargo compatibility, bioavailability data from human studies, manufacturing scalability, and IP exclusivity terms. Vendor pricing benchmarks for platform licensing range from low-single-digit royalties (typical of Rani's deal structure) to mid-single-digit royalties for highly differentiated systems.

Regional Analysis

The oral biologic delivery platform market by region is led by North America at 47.5% revenue share in 2025, equating to USD 1.99 Billion. The United States dominates with FDA-driven regulatory leadership, deep venture funding, and concentrated platform innovation in Boston, San Francisco, San Jose, and Cambridge, Massachusetts. Approximately 3.2 million Rybelsus prescriptions in the United States support Novo Nordisk's commercial scale, while Wegovy pill production occurs domestically at a starting-dose price of USD 149 per month. Canada contributes through clinical trial sites and Health Canada review pathways. Mexico's role remains limited to commercial distribution. Recent activity includes the Vivtex-Novo Nordisk USD 2.1 Billion partnership announced February 25, 2026 and Pinnacle Medicines' USD 89 Million Series B closed March 26, 2026.

Europe held 22.8% share in 2025, equivalent to USD 953 Million. Denmark anchors the region through Novo Nordisk's headquarters in Bagsvaerd and the Novo Holdings investment ecosystem, which seeded Orbis Medicines and supports oral peptide platform innovation through the EUR 90 Million Series A closed January 6, 2025. Germany contributes through BioMed X Heidelberg, which launched a Novo Nordisk-funded oral peptide research collaboration on August 19, 2025 focused on prolonged retention of oral peptide formulations in the lower small intestine. The United Kingdom, Italy (Chiesi Farmaceutici S.p.A.), and Switzerland (Lonza Group AG) round out the European footprint. The European Medicines Agency reviewed oral semaglutide 25 mg during the second half of 2025, signaling regional regulatory momentum.

Asia Pacific captured 22.4% share in 2025, valued at USD 936 Million. China leads regional innovation through Hefei Tianhui Biotech's Marketing Authorization Application for oral insulin filed with the NMPA, supported by USD 60 Million invested into the OraTech Pharmaceuticals joint venture in February 2025. Japan contributes through Chugai Pharmaceutical's October 2025 collaboration with Rani Therapeutics valued at up to USD 1.085 Billion. South Korea, India, and Australia round out the regional landscape, with Asia Pacific expanding faster than the global average due to large diabetes and obesity populations and improving regulatory harmonization through ICH-aligned bodies.

Latin America held 4.3% share in 2025, approximately USD 180 Million, with Brazil and Mexico as principal demand markets. Anvisa review pathways largely align with FDA decisions, accelerating market access; government reimbursement programs in Brazil expanded GLP-1 access during 2025.

The Middle East and Africa contributed 3.0% share, valued at USD 125 Million in 2025. Israel anchors this region through Entera Bio Ltd. (NASDAQ: ENTX), OraTech Pharmaceuticals, and the Hadassah Medical Center research base in Jerusalem. Saudi Arabia's Vision 2030 healthcare investments expanded specialty pharmacy infrastructure, while the United Arab Emirates' Dubai Health Authority approved Rybelsus for cardiovascular indications in late 2025. Sub-Saharan Africa remains underdeveloped due to cold-chain limitations that ironically favor oral biologics over injectables for last-mile distribution.

Country Analysis

United States

The oral biologic delivery platform market in the United States was valued at approximately USD 1.85 Billion in 2025 and is projected to grow at a CAGR of 13.5% during the forecast period 2025-2034. The FDA's Center for Drug Evaluation and Research approved Rybelsus for MACE reduction on October 17, 2025 based on the SOUL trial of 9,650 patients, and approved the Wegovy pill on December 22, 2025 with January 2026 commercial availability. The National Institutes of Health funds peptide delivery research through the National Institute of Diabetes and Digestive and Kidney Diseases, while the Massachusetts Life Sciences Center supports MIT-affiliated platforms including Vivtex Corporation.

Denmark

Denmark's oral biologic delivery platform market reached approximately USD 360 Million in 2025 with a country CAGR of 14.1% during 2025-2034. Novo Nordisk A/S anchors domestic activity through Rybelsus and the Wegovy pill, while Novo Holdings deployed substantial capital into oral peptide and macrocycle platforms including Orbis Medicines (Copenhagen). The Danish Center for AI Innovation enabled Orbis to use the Gefion supercomputer for nCycle design starting June 2025, accelerating computational design of oral macrocycle candidates.

Israel

Israel's oral biologic delivery platform market reached USD 175 Million in 2025 with a country CAGR of 14.6%, the fastest among major country markets. Entera Bio Ltd. (NASDAQ: ENTX) submitted a streamlined Phase 3 protocol for EB613 oral PTH(1-34) to the FDA on March 4, 2026, with topline data expected in the second half of 2028. Entera and OPKO Health expanded their collaboration on February 4, 2026 to advance the first oral long-acting PTH tablet for hypoparathyroidism with IND filing planned for late 2026. OraTech Pharmaceuticals, the spin-out from Oramed announced February 11, 2025, retains Israeli R&D operations focused on the POD oral protein delivery technology.

China

China's oral biologic delivery platform market reached approximately USD 320 Million in 2025 with a country CAGR of 15.2% during 2025-2034. Hefei Tianhui Biotech operates a manufacturing facility in Hefei and submitted a Marketing Authorization Application to the NMPA for oral insulin. The OraTech joint venture with HTIT, capitalized at USD 75 Million in February 2025, positions China as both a manufacturing and commercial market. Chinese pharma sponsors increasingly partner with United States biotech for technology transfer, illustrated by the Rani-Chugai agreement leveraging Chugai's Tokyo and Shanghai operations and Pinnacle Medicines' joint Doylestown-Shanghai operating model.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology Platform

- Nanoparticle-Based Delivery Platforms

- Lipid-Based Delivery Systems

- Polymeric Delivery Platforms

- Permeation Enhancer Technologies

- Mucoadhesive Delivery Systems

- Enteric-Coated Oral Delivery Platforms

- Microencapsulation Technologies

- Protease Inhibitor-Based Delivery Platforms

- Carrier-Mediated Oral Delivery Systems

- Others

By Molecule Type

- Peptides

- Monoclonal Antibodies

- Proteins

- Hormones

- Enzymes

- Vaccines

- Nucleic Acid Therapeutics

- RNA-Based Therapeutics

- Others

By Therapeutic Area

- Diabetes

- Oncology

- Autoimmune Diseases

- Gastrointestinal Disorders

- Infectious Diseases

- Cardiovascular Diseases

- Neurological Disorders

- Rare Diseases

- Hormonal Disorders

- Others

By End-User

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic and Research Institutes

- Hospitals and Specialty Clinics

- Clinical Research Organizations

- Government Research Organizations

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.18 B |

| Forecast Revenue (2034) | USD 12.78 B |

| CAGR (2025-2034) | 13.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology Platform, (Nanoparticle-Based Delivery Platforms, Lipid-Based Delivery Systems, Polymeric Delivery Platforms, Permeation Enhancer Technologies, Mucoadhesive Delivery Systems, Enteric-Coated Oral Delivery Platforms, Microencapsulation Technologies, Protease Inhibitor-Based Delivery Platforms, Carrier-Mediated Oral Delivery Systems, Others), By Molecule Type, (Peptides, Monoclonal Antibodies, Proteins, Hormones, Enzymes, Vaccines, Nucleic Acid Therapeutics, RNA-Based Therapeutics, Others), By Therapeutic Area, (Diabetes, Oncology, Autoimmune Diseases, Gastrointestinal Disorders, Infectious Diseases, Cardiovascular Diseases, Neurological Disorders, Rare Diseases, Hormonal Disorders, Others), By End-User, (Pharmaceutical Companies, Biotechnology Companies, Contract Research Organizations (CROs), Academic and Research Institutes, Hospitals and Specialty Clinics, Clinical Research Organizations, Government Research Organizations, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVO NORDISK A/S, ELI LILLY AND COMPANY, RANI THERAPEUTICS HOLDINGS, INC., ENTERA BIO LTD., VIVTEX CORPORATION, ORATECH PHARMACEUTICALS INC., ORBIS MEDICINES, PINNACLE MEDICINES, OPKO HEALTH, INC., CHIESI FARMACEUTICI S.P.A., VAXART, INC., LONZA GROUP AG, THERMO FISHER SCIENTIFIC INC., EVONIK INDUSTRIES AG, HEFEI TIANHUI BIOTECH CO., LTD., BIOMED X, AMGEN INC., F. HOFFMANN-LA ROCHE LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Molecule (Peptides, mAbs, RNA), Therapy (Diabetes, Oncology, Autoimmune), End-User (Pharma, Biotech, Academic) - Global Region, Key Players, Trends & Forecast 2026-2034")

, Molecule (Peptides, mAbs, RNA), Therapy (Diabetes, Oncology, Autoimmune), End-User (Pharma, Biotech, Academic) - Global Region, Key Players, Trends & Forecast 2026-2034")

, Molecule (Peptides, mAbs, RNA), Therapy (Diabetes, Oncology, Autoimmune), End-User (Pharma, Biotech, Academic) - Global Region, Key Players, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Oral Biologic Delivery Platform Market?

The Global Oral Biologic Delivery Platform Market was valued at USD 3.70 Billion in 2024 and USD 4.18 Billion in 2025, and is projected to reach USD 12.78 Billion by 2034, growing at a CAGR of 13.2% from 2026 to 2034. Market growth is driven by oral biologics, peptide therapeutics, advanced drug delivery technologies, and precision medicine.

Who are the major players in the Oral Biologic Delivery Platform Market?

NOVO NORDISK A/S, ELI LILLY AND COMPANY, RANI THERAPEUTICS HOLDINGS, INC., ENTERA BIO LTD., VIVTEX CORPORATION, ORATECH PHARMACEUTICALS INC., ORBIS MEDICINES, PINNACLE MEDICINES, OPKO HEALTH, INC., CHIESI FARMACEUTICI S.P.A., VAXART, INC., LONZA GROUP AG, THERMO FISHER SCIENTIFIC INC., EVONIK INDUSTRIES AG, HEFEI TIANHUI BIOTECH CO., LTD., BIOMED X, AMGEN INC., F. HOFFMANN-LA ROCHE LTD., Others

Which segments covered the Oral Biologic Delivery Platform Market?

By Technology Platform, (Nanoparticle-Based Delivery Platforms, Lipid-Based Delivery Systems, Polymeric Delivery Platforms, Permeation Enhancer Technologies, Mucoadhesive Delivery Systems, Enteric-Coated Oral Delivery Platforms, Microencapsulation Technologies, Protease Inhibitor-Based Delivery Platforms, Carrier-Mediated Oral Delivery Systems, Others), By Molecule Type, (Peptides, Monoclonal Antibodies, Proteins, Hormones, Enzymes, Vaccines, Nucleic Acid Therapeutics, RNA-Based Therapeutics, Others), By Therapeutic Area, (Diabetes, Oncology, Autoimmune Diseases, Gastrointestinal Disorders, Infectious Diseases, Cardiovascular Diseases, Neurological Disorders, Rare Diseases, Hormonal Disorders, Others), By End-User, (Pharmaceutical Companies, Biotechnology Companies, Contract Research Organizations (CROs), Academic and Research Institutes, Hospitals and Specialty Clinics, Clinical Research Organizations, Government Research Organizations, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Oral Biologic Delivery Platform Market

Published Date : 30 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date