- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Organic Deodorant Market Size, Share & Growth Outlook | CAGR 17.4%

Global Organic Deodorant Market Size, Share & Analysis By Type (Sprays, Roll Ons, Sticks/Creams), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex), Clean-Label Trends, Brand Positioning & Forecast 2025–2034

Report Overview

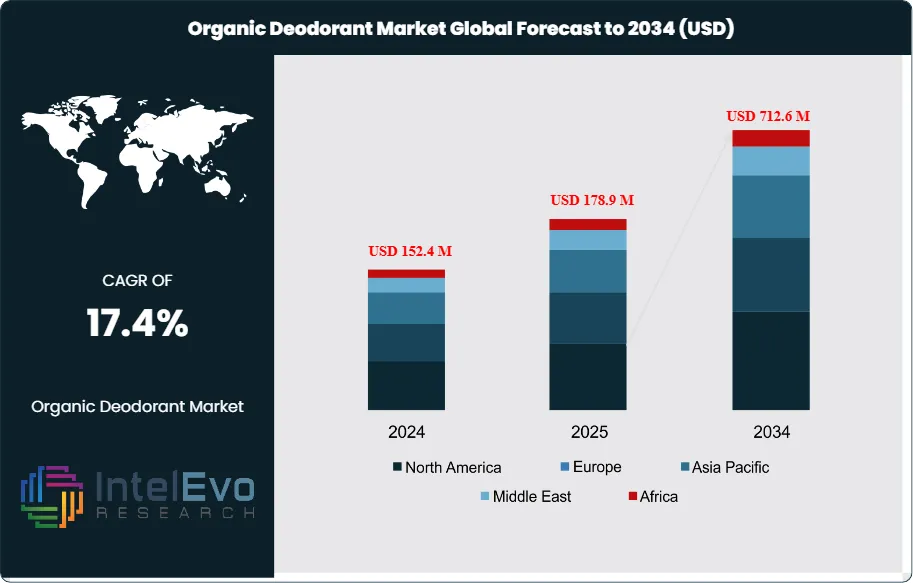

The Organic Deodorant Market was valued at approximately USD 152.4 Million in 2024 and is expected to reach around USD 712.6 Million by 2034, expanding at an estimated CAGR of about 17.4% during 2025–2034. Growing consumer preference for clean-label, aluminum-free, and skin-safe formulations continues to accelerate global market adoption. With sustainability, zero-waste packaging, and gender-neutral fragrances rising in popularity, the organic deodorant segment is rapidly becoming a mainstream personal care choice.

Get More Information about this report -

Request Free Sample ReportOnce a specialized segment in the natural personal care sector, organic deodorants are becoming mainstream, as more consumers demand transparency around ingredients and seek alternatives free from aluminum and parabens. Influencer-led marketing and strong e-commerce penetration are pushing the trend even faster across Asia-Pacific, Europe, and North America.

Consumer interest in this space is reflected in behavior trends—searches for "best deodorants" have grown by over 60% in the past two years, and the use of natural deodorant products has increased by nearly 9%. Although organic options still make up a small part of the overall deodorant market, global import data shows room for growth. For instance, the U.S. brought in over USD 320 million worth of deodorants in 2022, and Germany imported roughly USD 264.7 million, indicating robust retail potential for certified organic products.

This demand is largely shaped by increasing awareness around safety and sustainability. Plant-based ingredients like magnesium hydroxide, zinc ricinoleate, and arrowroot powder are becoming popular, alongside products containing essential oils and gentle, hypoallergenic bases. Brands are adapting to stricter regulations, especially in North America and Europe, by introducing products certified by COSMOS and USDA Organic, and using recyclable or refillable packaging.

However, the supply chain is not without its challenges. Price volatility in organic raw materials and the difficulty in achieving the same performance as traditional deodorants are key concerns. Common risks include skin sensitivity to baking soda, the higher pricing of organic alternatives (often 20–40% more than conventional products), and increased scrutiny over potentially misleading eco-friendly claims. This makes third-party certifications and clinically backed results essential for consumer trust.

Innovation is helping bridge the gap between sustainability and performance. Emerging product features like microencapsulated odor control, probiotic ferments, and waterless balm formats are gaining popularity for their skin-friendly and low-carbon benefits. On the marketing side, companies are leveraging direct-to-consumer (D2C) platforms, subscription models, and AI-based personalization tools to retain customers and enhance their shopping experience.

From a regional perspective, North America and Europe continue to dominate in revenue and regulatory leadership. Meanwhile, Asia Pacific is poised for substantial growth, driven by an expanding middle class and a growing preference for clean-label products in markets like China, India, and Southeast Asia. Regions such as Latin America and the Middle East & Africa are also showing potential, thanks to the rise of modern retail infrastructure and consumer demand for long-lasting deodorant solutions, particularly in warmer climates.

, By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex), Clean-Label Trends, Brand Positioning & Forecast 2025–2034")

Key Takeaways

- Market Growth: The organic deodorant market was USD 152.4 Million in 2024 and is projected to reach USD 712.6 Million by 2034, reflecting a 17.4% CAGR (2025–2034). Growth is propelled by clean-label preferences, stricter EU/US claims regulations, and sustained digital demand—online searches for “best deodorants” rose >60% in the past two years.

- Type (Sprays): Sprays led the product mix with a 48.6% share in 2024, supported by quick-dry formats, even coverage, and growing adoption of compressed/non-propellant systems that reduce packaging and propellant use. Sticks and creams are gaining traction in sensitivity-focused and travel retail channels but remain secondary in volume.

- Distribution Channel (Supermarkets & Hypermarkets): Supermarkets/Hypermarkets commanded the largest channel share in 2024 (est. ~45%), benefiting from breadth of assortment, visibility for certified organic labels, and private-label expansion. Omnichannel services (click-and-collect, same-day delivery) further consolidate their advantage over specialty and pure-play D2C.

- End User (Women): Women accounted for the majority of purchases in 2024 (est. ~60% share), driven by higher adoption of natural beauty and sensitivity-care routines. Brands targeting female cohorts with microbiome-friendly and aluminum-free claims see above-average repeat rates and premium mix.

- Driver: Rising health and environmental awareness is accelerating trade-up from conventional antiperspirants to aluminum-free, plant-based formulas; adoption of “natural” formats has increased by ~9 percentage points recently. Certification (USDA, COSMOS) and recyclable/refill packaging are key purchase triggers that support premium pricing.

- Restraint: Price premiums of 20–40% versus mass deodorants and occasional irritation with baking-soda bases constrain penetration among price-sensitive and sensitive-skin users. Supply-side volatility in organic essential oils and butters pressures margins, elevating the need for reformulation and diversified sourcing.

- Opportunity: Asia Pacific is the fastest-growing demand pool (projected >16% CAGR through 2033), as urban middle-class consumers in China, India, and Southeast Asia shift to “clean” personal care. Refill sticks, waterless concentrates, and subscription bundles create incremental ARPU and retailer shelf advantages.

- Trend: Performance-led natural innovation—microencapsulated odor control, enzyme/probiotic actives, and magnesium/zinc systems—is narrowing efficacy gaps with conventional products. Sustainability moves (PCR materials, refill cartridges) and D2C data-driven personalization are scaling, with leading brands reporting double-digit online subscription growth.

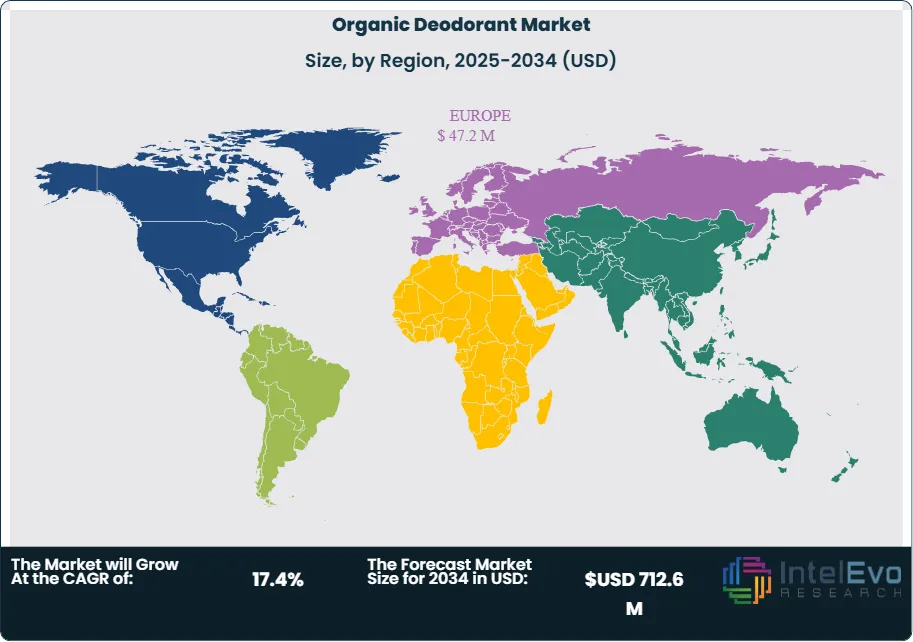

- Regional Analysis: Europe leads with 34.8% of global revenue, underpinned by mature organic standards and high eco-awareness; North America follows with strong premium willingness to pay and active indie/D2C brands. Asia Pacific is the investment hotspot for mid-to-premium trade-ups, while Latin America and the Middle East & Africa show emerging momentum as modern retail expands.

Type Analysis

Sprays remain the category’s scale anchor, holding 48.6% of global organic deodorant value in 2024 and expected to sustain leadership through 2025 on the back of quick-dry formats, fine mist delivery, and strong shelf presence in mass retail. Advances in compressed aerosols and non-propellant pumps are reducing packaging weight and propellant use, improving cost-to-serve and sustainability scores—key purchase triggers in Europe and North America. Premium brands are layering microencapsulated odor-control and magnesium/zinc systems into spray bases to close efficacy gaps with conventional antiperspirants, supporting modest mix-led price realization in 2025.

Roll-ons capture a sizable follower position, benefiting consumers who prefer precise, no-overspray application and economical dosing. Water-based, low-irritant formulations and fragrance-free SKUs are broadening roll-on appeal among sensitive-skin cohorts, while travel-size packs extend convenience-led usage. Sticks and creams, though smaller in share, are the fastest premiumizers; solid balms in paperboard tubes and refill cartridges align with plastic-reduction goals, and waterless concentrates offer higher wear time—features that support premium pricing and online subscription attach.

Distribution Channel Analysis

Supermarkets and hypermarkets remain the dominant route-to-market in 2025, leveraging breadth of assortment, visibility for certified (USDA/COSMOS) labels, and growing private-label organic ranges. End-cap education, clean-beauty adjacencies, and click-and-collect options reinforce shopper conversion, keeping the channel at the top of household replenishment missions.

Convenience stores are expanding shelf space for organic SKUs in urban, transit, and campus locations, capturing “need-it-now” occasions and smaller pack formats. The online channel, however, is the clear growth outlier, supported by D2C subscriptions, auto-replenishment, and algorithmic scent/strength quizzes. With digital search interest for “best deodorants” up >60% over the last two years, e-commerce is projected to post the highest CAGR through 2030, aided by marketplace reviews and influencer-led discovery.

End User Analysis

Women account for the majority of category spend, reflecting higher adoption of clean-beauty routines and willingness to pay for verified aluminum-free, cruelty-free, and microbiome-friendly claims. Brand portfolios skew toward female-led fragrance lines and sensitive-skin variants, with repeat rates strengthened by subscription models and refill ecosystems.

Men’s participation is rising from a smaller base as discreet fragrances, sport/endurance claims, and non-tacky textures improve parity with mainstream options. Unisex lines are gaining traction in 2025, simplifying inventory and appealing to households consolidating purchases; neutral scents, minimalist packaging, and shared-value bundles (e.g., family multipacks) support penetration of budget-conscious consumers without diluting premium cues.

Regional Analysis

Europe remains the value leader with 34.8% share in 2024 (≈USD 47.2 million) and is set to defend that position in 2025 as stringent claim and packaging rules favor certified players and established retail networks. Northern and Western Europe drive premium mix via refill sticks and paper-based packaging, while Central/Eastern Europe adds incremental volume as modern trade expands and private labels scale.

North America follows with strong D2C penetration, indie-brand innovation, and higher ARPU, but Asia Pacific is the medium-term growth engine. Rising middle-class cohorts in China, India, and Southeast Asia are trading up to “clean” personal care; with modern retail and cross-border e-commerce maturing, APAC is projected to outpace the global CAGR (often >16%). Latin America and the Middle East & Africa are emerging opportunity zones where climate-driven need for long-wear formats and improving modern retail footprints support above-market growth, especially for price-accessible sprays and roll-ons.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Sprays

- Roll Ons

- Sticks/Creams

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Online

By End User

- Women

- Men

- Unisex

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 152.4 M |

| Forecast Revenue (2034) | USD 712.6 M |

| CAGR (2024-2034) | 17.4% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Sprays, Roll Ons, Sticks/Creams), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Weleda, Sebamed, Buyindusvalley, Alverde, EO Products, Laverana Digital GmbH & Co. KG, Lavanila, Elsa’s Organic Skinfoods, Speick Naturkosmetik, Unilever |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex), Clean-Label Trends, Brand Positioning & Forecast 2025–2034")

, By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex), Clean-Label Trends, Brand Positioning & Forecast 2025–2034")

, By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex), Clean-Label Trends, Brand Positioning & Forecast 2025–2034")

Frequently Asked Questions

How big is the Organic Deodorant Market?

The Organic Deodorant Market will rise from USD 152.4M in 2024 to USD 712.6M by 2034, driven by clean-label demand, zero-waste packaging, and premium natural formulations.

Who are the major players in the Organic Deodorant Market?

Weleda, Sebamed, Buyindusvalley, Alverde, EO Products, Laverana Digital GmbH & Co. KG, Lavanila, Elsa’s Organic Skinfoods, Speick Naturkosmetik, Unilever

Which segments covered the Organic Deodorant Market?

By Type (Sprays, Roll Ons, Sticks/Creams), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online), By End User (Women, Men, Unisex)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date