- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

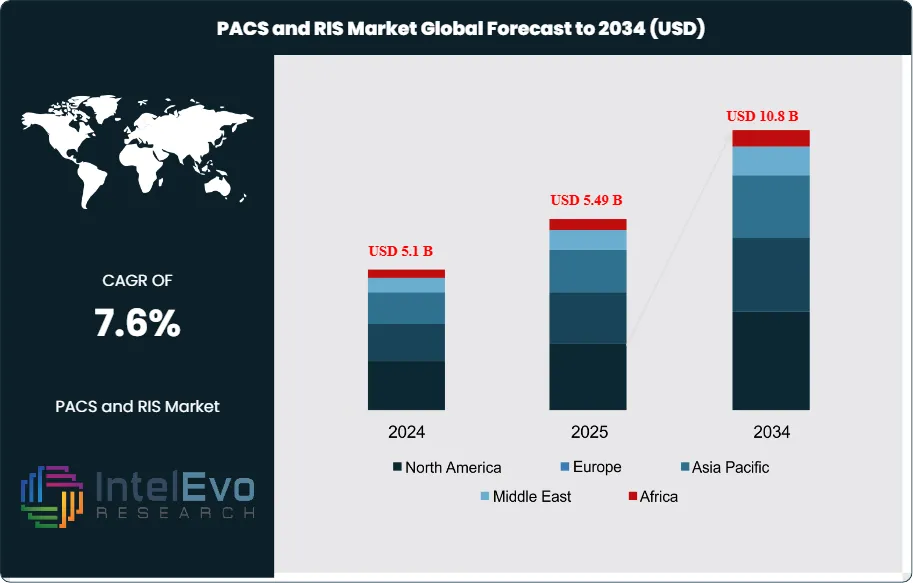

Global PACS/RIS Market: $10.8B by 2034 with CAGR of 7.6%

Global PACS and RIS Market Size, Share, Analysis Report By Product Type (Integrated PACS-RIS, Standalone PACS, Standalone RIS, AI-Powered Imaging Analytics, Cloud-Based Imaging Platforms) Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

The Global PACS and RIS Market size is expected to be worth around USD 10.8 Billion by 2034, up from USD 5.1 Billion in 2024, growing at a CAGR of 7.6% during the forecast period from 2024 to 2034. The PACS (Picture Archiving and Communication System) and RIS (Radiology Information System) market encompasses a comprehensive ecosystem of digital imaging and information management solutions that support diagnostic imaging, workflow automation, and data management in healthcare.

Get More Information about this report -

Request Free Sample ReportPACS enables the storage, retrieval, management, and distribution of medical images, while RIS streamlines patient scheduling, reporting, and radiology department operations. Together, these systems form the backbone of modern radiology, serving hospitals, outpatient imaging centers, specialty clinics, and diagnostic laboratories.

The market is experiencing robust growth driven by the global shift toward digital healthcare, the rising volume of diagnostic imaging procedures, and the need for integrated, interoperable IT solutions. Key growth catalysts include the adoption of cloud-based PACS and RIS, the integration of artificial intelligence (AI) for image analysis and workflow optimization, and the increasing focus on patient-centric care. The COVID-19 pandemic further accelerated digital transformation in healthcare, highlighting the importance of remote access, tele-radiology, and secure data sharing.

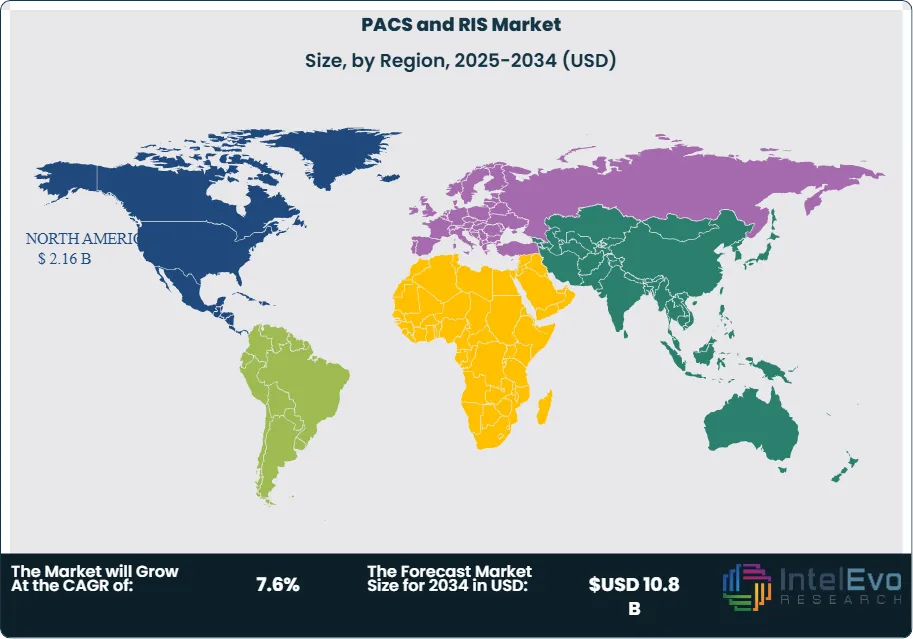

North America dominates the global PACS and RIS market, generating significant revenue due to advanced healthcare infrastructure, high imaging volumes, and favorable reimbursement policies. The Asia-Pacific region presents the fastest-growing market segment, driven by healthcare modernization, rising investments in digital health, and expanding access to diagnostic services. Europe maintains a significant market presence due to established healthcare systems and regulatory mandates for electronic health records.

The market is also shaped by regulatory requirements for data privacy and security, ongoing innovation in AI-powered diagnostics, and the growing demand for scalable, cost-effective cloud solutions. As healthcare providers seek to improve efficiency, accuracy, and patient outcomes, the adoption of integrated PACS and RIS platforms is expected to accelerate globally.

Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The PACS and RIS Market is expected to reach USD 10.8 Billion by 2034, fueled by digital transformation, rising imaging volumes, and the need for efficient data management and workflow automation.

- Product Type Dominance: Integrated PACS-RIS solutions lead the segment, offering seamless workflow, interoperability, and enhanced clinical decision support.

- Deployment Model Dominance: Cloud-based solutions are rapidly gaining market share due to scalability, cost-effectiveness, and remote accessibility.

- End-User Dominance: Hospitals remain the largest end-user segment, but outpatient imaging centers and specialty clinics are rapidly adopting PACS and RIS.

- Driver: Key drivers accelerating growth include the demand for efficient workflow, regulatory compliance, and the integration of AI and analytics.

- Restraint: Growth is hindered by data security concerns, high implementation costs, and interoperability challenges.

- Opportunity: The market is poised for expansion due to opportunities like AI-powered diagnostics, tele-radiology, and emerging market penetration.

- Trend: Emerging trends including cloud adoption, AI integration, and patient-centric digital health are reshaping the market.

- Regional Analysis: North America leads owing to advanced healthcare infrastructure and high imaging volumes. Asia-Pacific shows high promise due to healthcare modernization and digital health investments.

Product Type Analysis

Integrated PACS-RIS Solutions Lead the Market: Integrated PACS-RIS solutions represent the leading product category within the global market, primarily due to their ability to streamline radiology workflows, reduce manual data entry, and improve diagnostic accuracy. These platforms enable seamless data exchange between imaging devices, radiologists, and referring physicians, supporting faster turnaround times and better patient outcomes. The integration of PACS and RIS with electronic health records (EHRs) further enhances clinical collaboration and regulatory compliance.

Standalone PACS and RIS solutions remain relevant, particularly in smaller facilities or regions with limited IT infrastructure. However, the trend is toward unified platforms that offer advanced analytics, AI-powered image interpretation, and interoperability with other healthcare IT systems.

Deployment Model Analysis

Cloud-Based Solutions Gain Momentum: Cloud-based PACS and RIS are transforming the market by offering scalable, cost-effective, and remotely accessible solutions. Cloud deployment reduces the need for on-premises hardware, lowers maintenance costs, and enables secure data sharing across multiple sites. This is particularly valuable for tele-radiology, multi-site hospital networks, and healthcare systems in emerging markets.

On-premises solutions persist in regions with strict data residency requirements or limited internet connectivity. Hybrid models, combining local and cloud storage, are also gaining popularity for balancing security and accessibility.

End-User Analysis

Hospitals Dominate, Outpatient Centers and Clinics Expand: Hospitals remain the largest end-user segment, accounting for the majority of PACS and RIS deployments due to high imaging volumes, complex workflows, and regulatory requirements. Large hospital networks benefit from integrated, enterprise-wide solutions that support multi-modality imaging and cross-departmental collaboration.

Outpatient imaging centers, specialty clinics, and diagnostic laboratories are rapidly adopting PACS and RIS to improve efficiency, reduce turnaround times, and enhance patient experience. The growth of telemedicine and remote diagnostics is further expanding the market among non-hospital providers.

Region Analysis

North America Leads, Asia-Pacific Fastest-Growing: North America holds the commanding position in the global PACS and RIS market, establishing its leadership through advanced healthcare infrastructure, high adoption of digital imaging, and supportive reimbursement policies. The United States is a key market, with widespread use of PACS and RIS in hospitals, imaging centers, and academic medical centers.

The Asia-Pacific region emerges as the most rapidly expanding market, driven by healthcare modernization, rising investments in digital health, and expanding access to diagnostic imaging. China, India, Japan, and Southeast Asia are key growth markets, with increasing demand for affordable, scalable PACS and RIS solutions.

Europe continues to maintain a substantial market footprint through its established healthcare systems, regulatory mandates for electronic health records, and a strong focus on quality and safety.

Latin America and the Middle East & Africa are emerging markets, with growth driven by healthcare infrastructure development, government initiatives, and rising awareness of digital health benefits.

Get More Information about this report -

Request Free Sample Report

Key Market Segment

Product Type

- Integrated PACS-RIS

- Standalone PACS

- Standalone RIS

- AI-Powered Imaging Analytics

- Cloud-Based Imaging Platforms

Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

End-User

- Hospitals

- Outpatient Imaging Centers

- Specialty Clinics

- Diagnostic Laboratories

Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.49 B |

| Forecast Revenue (2034) | USD 10.8 B |

| CAGR (2025-2034) | 7.6% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product Type (Integrated PACS-RIS, Standalone PACS, Standalone RIS, AI-Powered Imaging Analytics, Cloud-Based Imaging Platforms) Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GE HealthCare Technologies Inc., Philips Healthcare (Koninklijke Philips N.V.), Siemens Healthineers AG, Fujifilm Holdings Corporation, Carestream Health Inc., Agfa-Gevaert Group, Sectra AB, INFINITT Healthcare Co., Ltd., Novarad Corporation, Cerner Corporation (Oracle Health), IBM Watson Health, Merge Healthcare (an IBM Company), PaxeraHealth, Medavis GmbH, Esaote SpA, RamSoft Inc., Teledyne Technologies (Visage Imaging), Konica Minolta Healthcare Americas, Inc., Intelerad Medical Systems, Ambra Health |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Frequently Asked Questions

How big is the PACS and RIS Market?

Global PACS and RIS Market to grow from USD 5.1B in 2024 to USD 10.8B by 2034 with 7.6% CAGR, driven by rising digital healthcare needs and improved radiology workflow integration.

Who are the major players in the PACS and RIS Market?

GE HealthCare Technologies Inc., Philips Healthcare (Koninklijke Philips N.V.), Siemens Healthineers AG, Fujifilm Holdings Corporation, Carestream Health Inc., Agfa-Gevaert Group, Sectra AB, INFINITT Healthcare Co., Ltd., Novarad Corporation, Cerner Corporation (Oracle Health), IBM Watson Health, Merge Healthcare (an IBM Company), PaxeraHealth, Medavis GmbH, Esaote SpA, RamSoft Inc., Teledyne Technologies (Visage Imaging), Konica Minolta Healthcare Americas, Inc., Intelerad Medical Systems, Ambra Health

Which segments covered the PACS and RIS Market?

Product Type (Integrated PACS-RIS, Standalone PACS, Standalone RIS, AI-Powered Imaging Analytics, Cloud-Based Imaging Platforms) Deployment Model (Cloud-Based, On-Premises, Hybrid) End-User (Hospitals, Outpatient Imaging Centers, Specialty Clinics, Diagnostic Laboratories)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date