- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Patient Recruitment Platform Market Size, Share & Forecast | CAGR 12.0%

Global Patient Recruitment Platform Market Size, Share, Growth Analysis By Deployment Model (Enterprise SaaS, On-Premise, Hybrid), By Offering (Software Platforms, Recruitment Services), By Therapeutic Area (Oncology, Cardiovascular & Metabolic Diseases, CNS Disorders, Rare Diseases), By End-User (Pharmaceutical & Biotechnology Companies, CROs, Academic Medical Centers), Industry Trends, Competitive Landscape & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

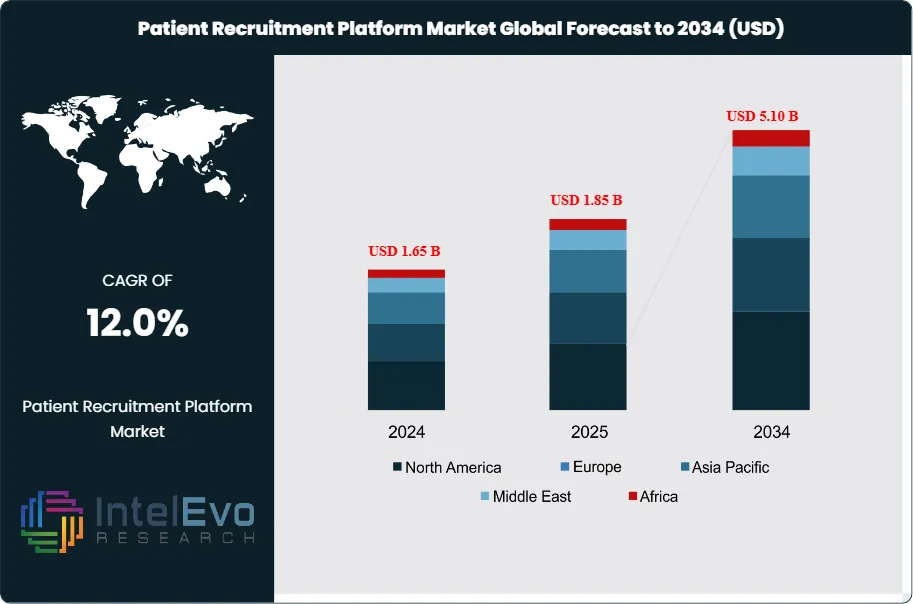

| USD 1.85 Billion | USD 5.10 Billion | 12.0% | North America, 42.5% |

The Patient Recruitment Platform Market was valued at approximately USD 1.65 Billion in 2024 and reached USD 1.85 Billion in 2025. The market is projected to grow to USD 5.10 Billion by 2034, expanding at a CAGR of 12.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.25 billion over the analysis period. Patient recruitment platforms serve as critical infrastructure for clinical trials, connecting sponsors, CROs, and research sites with eligible patient populations through digital tools, AI-driven matching algorithms, patient registries, and community outreach capabilities. The market is defined by platforms enabling pre-screening, electronic consent, patient engagement, retention tracking, and diversity analytics. Solutions range from enterprise SaaS offerings to specialized platforms for rare disease recruitment and decentralized trial management.

Get More Information about this report -

Request Free Sample ReportMarket expansion is driven by the FDA's commitment to clinical trial diversity, with 2025 enforcement actions targeting sponsors failing to meet Diversity Action Plan requirements. The FDA announced in January 2025 that future approvals will require documented evidence of diverse enrollment strategies, creating regulatory pressure on pharmaceutical companies and CROs to adopt specialized recruitment technology. Trial complexity has increased enrollment timelines by an average of 28% since 2020, according to clinical operations benchmarking data, while patient dropout rates reached 30% in oncology trials conducted during 2024. These inefficiencies translate to direct costs, with failed patient recruitment responsible for an estimated USD 8 million per day in delayed drug launches across the global pharmaceutical industry.

AI-powered patient identification represents the fastest-growing technology segment, capturing 31.2% of platform deployments in 2025. Natural language processing applied to electronic health records enables identification of eligible patients within hours rather than weeks, while predictive analytics assess enrollment likelihood and dropout risk with 78% accuracy based on historical trial data. Decentralized clinical trial adoption accelerated platform demand, with 62% of Phase II and Phase III trials in 2025 incorporating at least one decentralized element such as home health visits, wearable monitoring, or virtual site interactions. This shift requires recruitment platforms to support hybrid patient journeys across physical sites and digital touchpoints.

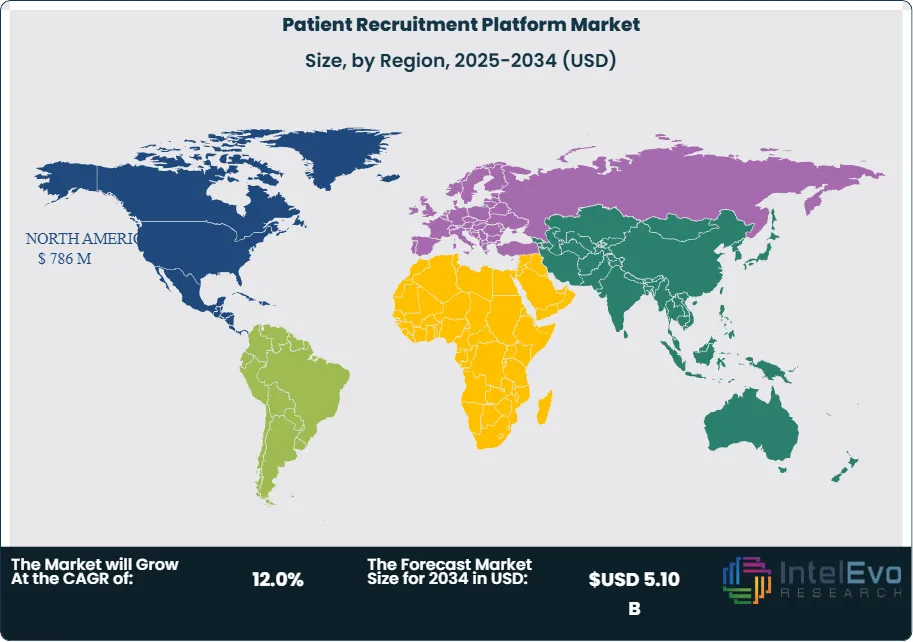

North America dominates the patient recruitment platform market with a 42.5% share in 2025, driven by the concentration of pharmaceutical R&D investment, stringent FDA diversity requirements, and mature digital health infrastructure. The region accounted for USD 786 million in platform spending during 2025, reflecting enterprise adoption by top 20 pharmaceutical companies and specialty CROs. Europe follows with a 28.7% market share, supported by the European Medicines Agency's Clinical Trials Regulation implementation and cross-border trial coordination requirements. Asia Pacific demonstrates the highest growth trajectory at 14.8% CAGR through 2034, fueled by clinical trial outsourcing to India and China, government support for clinical research infrastructure in Japan and South Korea, and patient registry development initiatives.

Competitive dynamics favor integrated platform providers offering end-to-end capabilities from patient identification through retention management. Market consolidation accelerated in 2024-2025, with three major acquisitions of specialized recruitment vendors by enterprise clinical trial management system providers seeking to close functional gaps. Emerging competition from healthcare data aggregators entering the recruitment space introduces new business models based on real-world data licensing and synthetic control arm generation. Patient privacy regulation remains a critical operational constraint, with HIPAA compliance costs, GDPR data localization requirements, and informed consent complexity adding 15-22% to platform operational budgets. Technology convergence between recruitment platforms and electronic data capture systems, patient engagement apps, and site management solutions is creating demand for API-first architectures and interoperability standards.

, By Offering (Software Platforms, Recruitment Services), By Therapeutic Area (Oncology, Cardiovascular & Metabolic Diseases, CNS Disorders, Rare Diseases), By End-User (Pharmaceutical & Biotechnology Companies, CROs, Academic Medical Centers), Industry Trends, Competitive Landscape & Forecast 2026-2034")

Key Takeaways

- Market Growth: The patient recruitment platform market is valued at USD 1.85 billion in 2025 and will reach USD 5.10 billion by 2034, expanding at a 12.0% CAGR. This growth is driven by regulatory mandates for diverse trial enrollment, rising clinical trial complexity, and digital transformation across pharmaceutical R&D operations.

- Segment Dominance: Enterprise SaaS platforms command 58.3% of the market by deployment model in 2025, reflecting pharmaceutical company preference for integrated, scalable solutions with dedicated support. These platforms offer multi-study management, cross-functional workflows, and compliance automation capabilities that custom-built systems cannot match at comparable cost.

- Segment Dominance: Oncology trials represent 37.4% of platform usage by therapeutic area in 2025, driven by high patient dropout rates, complex eligibility criteria, and the need for biomarker-based recruitment. Oncology recruitment platforms integrate genomic data, tumor registry access, and patient advocacy networks to address these unique challenges.

- Driver: FDA diversity enforcement in 2025 mandates documented recruitment strategies, driving pharmaceutical companies to adopt specialized platforms. Non-compliance risks include clinical hold actions and New Drug Application delays, creating a USD 420 million addressable market for diversity-focused recruitment tools through 2026.

- Restraint: Patient data privacy regulation adds 18% to platform total cost of ownership in 2025, including HIPAA technical safeguards, GDPR data processing agreements, and state-level privacy law compliance. Small CROs and academic institutions cite regulatory complexity as a barrier to platform adoption, constraining market penetration in the mid-market segment.

- Opportunity: Rare disease recruitment platforms address a USD 680 million unmet need in 2025, serving trials with fewer than 500 eligible patients globally. These specialized platforms integrate patient advocacy organizations, natural history registries, and genetic testing networks to identify ultra-rare patient populations that traditional recruitment methods cannot reach.

- Trend: Decentralized trial adoption reached 62% of Phase II-III studies in 2025, requiring recruitment platforms to support hybrid site models. Platform vendors are integrating telemedicine scheduling, home health visit coordination, and wearable device onboarding to enable end-to-end decentralized patient journeys, with 83% of new platform contracts including DCT capabilities.

- Regional Analysis: North America leads with 42.5% market share and USD 786 million in revenue for 2025, driven by pharmaceutical R&D concentration, FDA regulatory pressure, and mature digital health adoption. The US accounts for 89% of North American spending, reflecting enterprise platform deployments by top biopharmaceutical companies.

Competitive Landscape Overview

The patient recruitment platform market is moderately consolidated, with the top four providers capturing approximately 46% combined market share in 2025. Competition is technology-driven, characterized by AI capability differentiation, electronic health record integration depth, and patient engagement feature sets. Recent competitive intensity has increased due to acquisitions of specialized vendors by enterprise CTMS providers, entrance of healthcare data aggregators, and platform-based business model innovation around real-world data licensing.

Competitive Landscape Matrix

| Company Name | HQ | Position | Key Product | Geographic Strength | Recent Strategic Move |

| Oracle | USA | Leader | Oracle Health Clinical One | North America | Integrated AI-powered patient matching across EHR network, Feb 2025 |

| IQVIA | USA | Leader | IQVIA OCE Patient Finder | Global | Acquired decentralized trial platform TrialMatch for USD 240M, Jan 2025 |

| Medidata Solutions | USA | Leader | Medidata Patient Cloud | North America, Europe | Launched Patient Cloud Diversity Analytics for FDA compliance, Dec 2024 |

| Antidote Technologies | USA | Challenger | StudyKIK Platform | North America | Partnership with American Cancer Society for oncology trial matching, Mar 2025 |

| Science 37 | USA | Niche Player | NORA Decentralized Platform | North America | Raised USD 150M Series D for DCT infrastructure expansion, Jun 2025 |

| Veeva Systems | USA | Challenger | Veeva Site Connect | Global | Integrated patient recruitment into Vault CTMS ecosystem, Sep 2025 |

| TrialX | USA | Niche Player | TrialX Match Engine | North America | Launched Spanish-language patient portal for Hispanic enrollment, Nov 2024 |

| Florence Healthcare | USA | Niche Player | Florence Enroll Platform | North America | Integrated patient retention analytics with site payment automation, Apr 2025 |

| Deep 6 AI | USA | Challenger | Deep 6 EHR AI | North America | Expanded EHR network to cover 42M patient records across 18 health systems, Jan 2026 |

| Clara Health | USA | Niche Player | Clara Patient Engagement | North America | Launched multilingual SMS-based consent for low-literacy populations, Aug 2025 |

By Deployment Model

Enterprise SaaS platforms dominate the patient recruitment platform market with 58.3% share and USD 1.08 billion in revenue for 2025. These cloud-based solutions offer multi-study management, role-based access controls, compliance automation, and dedicated customer success teams. Pharmaceutical companies and large CROs prefer SaaS deployments for their scalability, automatic updates, and elimination of IT infrastructure overhead. The SaaS segment is growing at 13.2% CAGR through 2034, driven by expansion into mid-market CROs and academic medical centers. Leading vendors provide tiered pricing models with per-study fees, monthly active patient charges, and enterprise site licenses. Integration capabilities with existing CTMS, EDC, and eTMF systems represent a key competitive differentiator, with 74% of enterprise buyers requiring pre-built connectors to Oracle, Medidata, or Veeva platforms. Security certifications including SOC 2 Type II, HITRUST, and ISO 27001 are table stakes for enterprise deals.

On-premise deployment accounts for 22.4% of the market in 2025, concentrated among pharmaceutical companies with strict data sovereignty requirements or legacy IT architectures. This segment generates USD 414 million in annual license and maintenance revenue. On-premise installations are declining at 2.1% annually as cloud security matures and regulatory acceptance of SaaS models increases. Hybrid deployment models capture 19.3% market share, combining on-premise patient data storage with cloud-based recruitment tools. These configurations address healthcare organizations concerned about HIPAA compliance while enabling sponsor access to aggregated recruitment metrics. Hybrid platforms grew 9.8% in 2025, supported by health system partnerships and accountable care organization deployments seeking to monetize clinical research capabilities.

By Offering

Software platforms represent 71.2% of the patient recruitment market by offering type in 2025, generating USD 1.32 billion in revenue. Software includes patient identification engines, eligibility screening tools, electronic consent modules, engagement applications, and retention analytics dashboards. Advanced platforms incorporate AI-powered matching algorithms that analyze electronic health records, claims data, and patient registries to identify eligible candidates. Natural language processing extracts eligibility criteria from protocol documents and maps them to structured medical codes, reducing manual screening time by 68%. Predictive analytics assess enrollment likelihood and dropout risk using machine learning models trained on historical trial data. The software segment is expanding at 12.6% CAGR, fueled by increasing trial complexity and regulatory pressure for diverse enrollment.

Services account for 28.8% of the market in 2025, encompassing patient outreach campaigns, site training, community engagement programs, and recruitment strategy consulting. Service revenue reached USD 533 million during 2025, driven by sponsors lacking internal recruitment expertise. Managed recruitment services deliver end-to-end patient acquisition, from media campaign design through pre-screening call centers. Digital marketing services use programmatic advertising, social media targeting, and search engine optimization to reach patient populations. Community engagement services partner with patient advocacy organizations, disease-specific support groups, and healthcare providers to build trial awareness. Services are growing at 10.8% CAGR, with particular strength in rare disease trials where specialized outreach is required to identify ultra-rare patient populations.

By Therapeutic Area

Oncology represents 37.4% of platform usage by therapeutic area in 2025, reflecting the high volume of cancer drug development and recruitment challenges specific to oncology trials. Cancer trials face 35% patient dropout rates, complex biomarker-based eligibility requirements, and limited patient populations for specific tumor types and genetic subtypes. Oncology recruitment platforms integrate tumor registry access, genomic database queries, and molecular testing coordination. Partnerships with cancer centers, patient advocacy groups like the American Cancer Society, and survivorship networks provide referral pipelines. The oncology segment generated USD 692 million in platform revenue during 2025 and is growing at 13.8% CAGR, accelerated by immunotherapy trial expansion and precision medicine adoption requiring biomarker-driven patient selection.

Cardiovascular and metabolic diseases account for 24.1% of therapeutic area usage in 2025. This segment includes diabetes, hypertension, dyslipidemia, and heart failure trials. Recruitment platforms leverage primary care EHR data, pharmacy claims, and remote monitoring device integration to identify patients with specific cardiovascular risk profiles. Patient registries maintained by the American Heart Association and diabetes associations provide referral channels. The segment is valued at USD 446 million in 2025, growing at 11.2% CAGR driven by chronic disease prevalence and emphasis on real-world evidence studies requiring large diverse patient cohorts. Central nervous system disorders capture 18.7% share, covering Alzheimer's disease, Parkinson's disease, depression, schizophrenia, and epilepsy trials. CNS recruitment requires specialized cognitive assessment tools, caregiver engagement platforms, and partnerships with neurology clinics. Rare diseases represent 12.4% of usage, addressing trials with global patient populations under 10,000 individuals. Rare disease platforms integrate genetic testing results, natural history registries, and patient advocacy organization databases. Other therapeutic areas including infectious disease, respiratory, and dermatology comprise 7.4% of the market.

By End-User

Pharmaceutical and biotechnology companies represent 52.6% of platform end-users in 2025, accounting for USD 973 million in spending. Pharma companies use recruitment platforms to support global Phase II-IV trials, with typical deployments spanning 50-200 concurrent studies. Enterprise contracts include dedicated account management, protocol consulting, and integration services. Large pharmaceutical companies increasingly embed recruitment platforms into clinical development IT ecosystems alongside CTMS, safety databases, and data warehouses. Biotech companies focus on specialty disease areas and decentralized trial capabilities. The pharma segment is expanding at 12.4% CAGR, driven by pipeline growth in gene therapy, cell therapy, and precision medicine requiring targeted patient identification.

Contract research organizations account for 31.8% of end-users in 2025, spending USD 588 million on recruitment platforms. CROs manage clinical trials on behalf of pharmaceutical sponsors and require multi-client, multi-protocol platform capabilities. Top-tier CROs operate dedicated patient recruitment divisions using enterprise platforms for sponsor services. Mid-market CROs adopt platforms to compete on recruitment speed and quality. The CRO segment is growing at 11.6% CAGR as pharmaceutical outsourcing increases and CROs expand into full-service offerings. Academic medical centers and research hospitals comprise 15.6% of end-users, driven by investigator-initiated trials, clinical research networks, and infrastructure grants supporting translational research. Academic deployments focus on EHR integration and patient registry access within health system networks.

Regional Analysis

North America

North America dominates the patient recruitment platform market with 42.5% share and USD 786 million in revenue for 2025. The United States accounts for 89% of regional spending, driven by the concentration of pharmaceutical R&D investment, stringent FDA diversity requirements implemented in 2025, and mature digital health infrastructure. The FDA's enforcement of Diversity Action Plan requirements created immediate demand for platforms offering demographic analytics, community outreach tools, and enrollment tracking by race and ethnicity. Top 20 pharmaceutical companies collectively invested USD 340 million in recruitment platforms during 2025, reflecting enterprise-wide deployments supporting global clinical development portfolios.

The US market benefits from extensive EHR penetration, with 86% of office-based physicians using certified systems as of 2024, enabling platform integration with patient data sources. Health system partnerships provide recruitment platforms with access to aggregated patient populations across hospital networks, ambulatory clinics, and specialty centers. Canada represents 8% of North American spending, supported by government investment in clinical trial infrastructure and interprovincial research networks. Canadian platforms emphasize bilingual capabilities and integration with provincial health information systems. Mexico accounts for 3% of regional revenue, growing as pharmaceutical companies establish clinical trial sites to access diverse patient populations and reduce per-patient recruitment costs. North America is expanding at 11.8% CAGR through 2034, driven by decentralized trial adoption, AI capability advancement, and increasing clinical trial activity in gene therapy and cell therapy programs requiring complex patient identification.

Europe

Europe holds 28.7% of the global patient recruitment platform market with USD 531 million in revenue for 2025. The region is characterized by cross-border clinical trial coordination, GDPR data protection requirements, and implementation of the EU Clinical Trials Regulation which streamlined approval processes across member states. Germany leads European spending with 24% regional share, reflecting its position as the largest pharmaceutical market and strong clinical research infrastructure. German platforms emphasize integration with hospital information systems and compliance with German Medical Devices Act requirements. The United Kingdom accounts for 22% of European revenue, supported by National Health Service research networks providing access to centralized patient databases and the MHRA's adoption of decentralized trial frameworks.

France represents 18% of regional spending, driven by clinical trial tax incentives and government support for life sciences R&D. French platforms focus on integration with national health data systems and compliance with French data protection authority requirements. Spain captures 14% of European revenue, growing through expansion of clinical trial networks and hospital partnerships. Italy accounts for 12%, with platform adoption concentrated in northern research institutions and contract research organizations. The remaining 10% is distributed across smaller markets including Netherlands, Switzerland, Belgium, and Nordic countries. Europe is expanding at 10.4% CAGR through 2034, driven by harmonization of regulatory requirements under the Clinical Trials Regulation, increasing pharmaceutical R&D investment, and platform adoption by academic medical centers participating in European research consortia.

Asia Pacific

Asia Pacific represents 19.2% of the patient recruitment platform market with USD 355 million in revenue for 2025, demonstrating the fastest regional growth at 14.8% CAGR through 2034. China accounts for 38% of Asia Pacific spending, driven by government initiatives to strengthen clinical trial capabilities, NMPA regulatory reforms encouraging multinational trial participation, and pharmaceutical industry expansion. Chinese platforms integrate with hospital information systems, provincial health databases, and WeChat-based patient engagement tools. Patient recruitment faces challenges including limited EHR standardization and privacy concerns, addressed through hospital partnership models and regional patient registry development.

Japan represents 26% of regional revenue, supported by pharmaceutical industry leadership and government investment in clinical research infrastructure through the Agency for Medical Research and Development. Japanese platforms emphasize integration with DPC hospital data systems and compliance with Personal Information Protection Act requirements. India captures 18% of Asia Pacific spending, expanding as global CROs establish recruitment operations to access large diverse patient populations at lower per-patient costs. Indian platforms focus on site network management, mobile-first patient engagement, and integration with Aadhaar health records. South Korea accounts for 12% of regional revenue, driven by hospital adoption and pharmaceutical industry growth. Australia holds 6%, supported by government R&D incentives and clinical trial notification scheme participation. Asia Pacific growth is accelerated by increasing pharmaceutical outsourcing to the region, digital health infrastructure development, government support for clinical research capabilities, and platform localization for diverse languages and healthcare systems.

Latin America

Latin America holds 6.1% of the global patient recruitment platform market with USD 113 million in revenue for 2025. Brazil dominates with 56% of regional spending, driven by large patient populations, established clinical trial infrastructure, and ANVISA regulatory support for international trial participation. Brazilian platforms emphasize Portuguese language capabilities, integration with SUS public health system data, and compliance with Brazilian data protection law. Patient recruitment benefits from high disease burden, treatment-naive populations, and extensive hospital networks in major cities. Mexico represents 24% of Latin American revenue, supported by proximity to US pharmaceutical sponsors, COFEPRIS regulatory efficiency, and Spanish-language population access.

Argentina accounts for 12% of regional spending, with platform adoption driven by experienced clinical investigators and cost competitiveness. Colombia captures 8% of revenue, expanding through government initiatives to strengthen clinical research capabilities and pharmaceutical industry partnerships. Latin America is growing at 9.2% CAGR through 2034, driven by increasing multinational trial participation, platform localization investments, and expansion of middle-class populations with healthcare access. Challenges include economic volatility, currency fluctuations, and variation in regulatory approval timelines across countries. Platform vendors are addressing these through regional partnership models, multi-country patient registry integration, and flexible pricing denominated in US dollars.

Middle East & Africa

Middle East & Africa represents 3.5% of the global patient recruitment platform market with USD 65 million in revenue for 2025. The United Arab Emirates leads with 31% of regional spending, driven by government investment in healthcare infrastructure, Dubai Healthcare City development, and positioning as a regional clinical trial hub. UAE platforms integrate with Dubai Health Authority systems and support Arabic and English language capabilities. Saudi Arabia accounts for 27% of regional revenue, expanding through Vision 2030 healthcare transformation initiatives and Saudi Food and Drug Authority regulatory modernization. Platform adoption is concentrated in major hospital networks and research institutions in Riyadh and Jeddah.

South Africa represents 24% of Middle East & Africa spending, supported by established clinical trial infrastructure, experienced investigators, and access to treatment-naive populations. South African platforms emphasize integration with private hospital groups and public health facility networks. Israel captures 11% of regional revenue, driven by pharmaceutical and biotech industry strength and advanced digital health capabilities. Egypt accounts for 7% of spending, growing through government efforts to strengthen clinical research infrastructure and pharmaceutical manufacturing capabilities. The region is expanding at 8.6% CAGR through 2034, driven by healthcare infrastructure investment, government support for pharmaceutical industry development, and increasing participation in multinational clinical trials. Platform adoption faces challenges including fragmented healthcare systems, limited EHR penetration in some markets, and need for multi-language support across diverse populations.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Model

- Enterprise SaaS

- On-Premise

- Hybrid

By Offering

- Software Platforms

- Services

By Therapeutic Area

- Oncology

- Cardiovascular and Metabolic Diseases

- Central Nervous System Disorders

- Rare Diseases

- Other Therapeutic Areas

By End-User

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations

- Academic Medical Centers and Research Hospitals

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.85 B |

| Forecast Revenue (2034) | USD 5.10 B |

| CAGR (2025-2034) | 12.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Model, (Enterprise SaaS, On-Premise, Hybrid), By Offering, Software Platforms, Services), By Therapeutic Area, (Oncology, Cardiovascular and Metabolic Diseases, Central Nervous System Disorders, Rare Diseases, Other Therapeutic Areas), By End-User, (Pharmaceutical and Biotechnology Companies, Contract Research Organizations, Academic Medical Centers and Research Hospitals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ORACLE, IQVIA, MEDIDATA SOLUTIONS, ANTIDOTE TECHNOLOGIES, SCIENCE 37, VEEVA SYSTEMS, TRIALX, FLORENCE HEALTHCARE, DEEP 6 AI, CLARA HEALTH, THREAD RESEARCH, TRIAL INSIGHTS, ENGAGED CLINICAL TRIALS, BBK WORLDWIDE, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Offering (Software Platforms, Recruitment Services), By Therapeutic Area (Oncology, Cardiovascular & Metabolic Diseases, CNS Disorders, Rare Diseases), By End-User (Pharmaceutical & Biotechnology Companies, CROs, Academic Medical Centers), Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Offering (Software Platforms, Recruitment Services), By Therapeutic Area (Oncology, Cardiovascular & Metabolic Diseases, CNS Disorders, Rare Diseases), By End-User (Pharmaceutical & Biotechnology Companies, CROs, Academic Medical Centers), Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Offering (Software Platforms, Recruitment Services), By Therapeutic Area (Oncology, Cardiovascular & Metabolic Diseases, CNS Disorders, Rare Diseases), By End-User (Pharmaceutical & Biotechnology Companies, CROs, Academic Medical Centers), Industry Trends, Competitive Landscape & Forecast 2026-2034")

Frequently Asked Questions

How big is the Patient Recruitment Platform Market?

The Global Patient Recruitment Platform Market was valued at USD 1.65 Billion in 2024 and is projected to reach USD 5.10 Billion by 2034, growing at a CAGR of 12.0% from 2026 to 2034, driven by rising clinical trial complexity, increasing adoption of digital patient engagement tools, and growing demand for faster participant enrollment solutions.

Who are the major players in the Patient Recruitment Platform Market?

ORACLE, IQVIA, MEDIDATA SOLUTIONS, ANTIDOTE TECHNOLOGIES, SCIENCE 37, VEEVA SYSTEMS, TRIALX, FLORENCE HEALTHCARE, DEEP 6 AI, CLARA HEALTH, THREAD RESEARCH, TRIAL INSIGHTS, ENGAGED CLINICAL TRIALS, BBK WORLDWIDE, OTHERS

Which segments covered the Patient Recruitment Platform Market?

By Deployment Model, (Enterprise SaaS, On-Premise, Hybrid), By Offering, Software Platforms, Services), By Therapeutic Area, (Oncology, Cardiovascular and Metabolic Diseases, Central Nervous System Disorders, Rare Diseases, Other Therapeutic Areas), By End-User, (Pharmaceutical and Biotechnology Companies, Contract Research Organizations, Academic Medical Centers and Research Hospitals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Patient Recruitment Platform Market

Published Date : 09 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date