- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Payroll-as-a-Service Market Size, Share & Forecast | CAGR 10.9%

Global Payroll-as-a-Service Market Size, Share, Analysis By Service Type (Payroll Processing Services, Tax Filing & Compliance Services, Managed Payroll Services, Multi-Country Payroll Services, Payroll Analytics & Reporting Services, Employee Self-Service & Payroll Administration Services), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Organization Size (Large Enterprises, SMEs), By End-User Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 22.80 Billion | USD 57.60 Billion | 10.9% | North America, 38.6% |

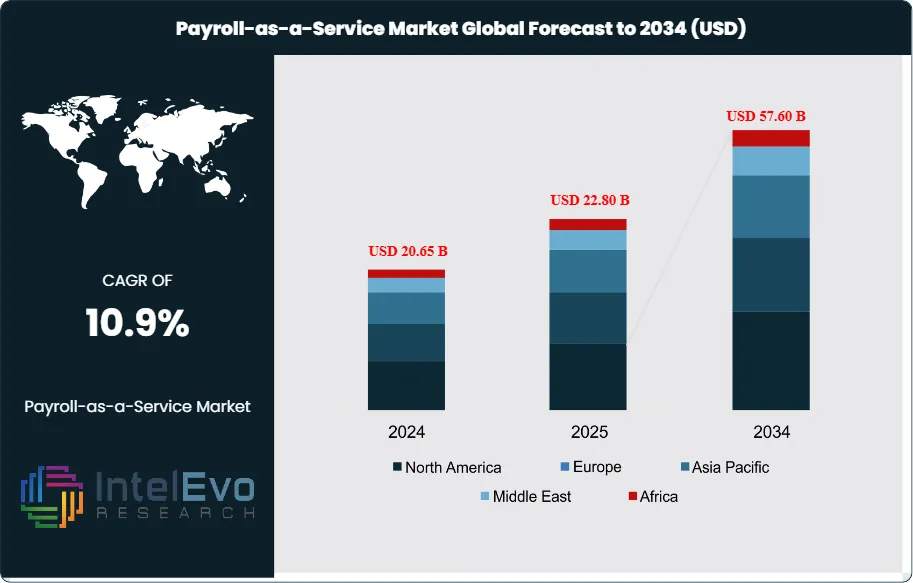

The Payroll-as-a-Service Market was valued at approximately USD 20.65 Billion in 2024 and reached USD 22.80 Billion in 2025. The market is projected to grow to USD 57.60 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 34.80 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportGrowth in the payroll-as-a-service market is anchored in three structural forces. First, legacy enterprise payroll is migrating to cloud-native multi-tenant platforms, with Automatic Data Processing (ADP) reporting fiscal 2025 revenue of USD 20.6 Billion (up 7%) and issuing fiscal 2026 guidance for 5% to 6% revenue growth on July 30, 2025, while Paychex reported Q2 FY2026 revenue of USD 1.56 Billion, up 18% year-over-year. Second, global-first platforms reshaped competitive dynamics, with Deel reaching a USD 1 Billion annual recurring revenue run rate in Q1 2025 with 75% year-over-year growth after turning profitable in Q3 2023, and Rippling reaching USD 570 Million ARR in February 2025 at a USD 13.5 Billion private valuation. Third, SMB digitization accelerated, with Gusto generating USD 600 Million of 2023 revenue, running a USD 200+ Million tender offer at a USD 9.3 Billion valuation, and targeting 150,000 new SMB customers in 2025.

The regulatory environment for payroll-as-a-service is framed by overlapping tax, employment, and data-protection regimes. In the United States, IRS Form 941 quarterly tax filing and Department of Labor Fair Labor Standards Act (FLSA) overtime rules underpin processing requirements, with California AB5 independent-contractor classification and New York state-level frameworks adding complexity. In the United Kingdom, HM Revenue & Customs (HMRC) enforces Pay As You Earn (PAYE) and Real Time Information (RTI) reporting. In the European Union, the General Data Protection Regulation (GDPR) governs cross-border payroll data flows, and the EU AI Act's general-purpose AI provisions effective August 2, 2025 intersect with AI-enhanced payroll-anomaly detection. India's Code on Wages 2019 and Code on Social Security 2020 consolidate earlier statutes into integrated payroll frameworks, and SOC 2 Type II and ISO 27001 certifications set industry compliance baselines.

Demand is consolidating around measurable adoption milestones. Digital payroll and HR solution adoption reached 73% of US mid-to-large enterprises by 2025 per Industry Research, with the US accounting for approximately 32% of the global market. More than 67% of global organizations now operate on digital payroll platforms, with 1.2 Billion-plus workers managed through these systems. Approximately 61% of newly launched HR products feature machine-learning algorithms for payroll forecasting and fraud detection per 360 Research Reports. Cloud-based deployment models are projected to capture approximately 46% share of the payroll and HR solutions market by 2035 per Research Nester. The US payroll software market alone is expected to reach USD 47 Billion by 2028 per Deel's competitive positioning. Approximately 41% of new payroll deployments are SMEs, reflecting a broadening buyer base beyond the Fortune 500.

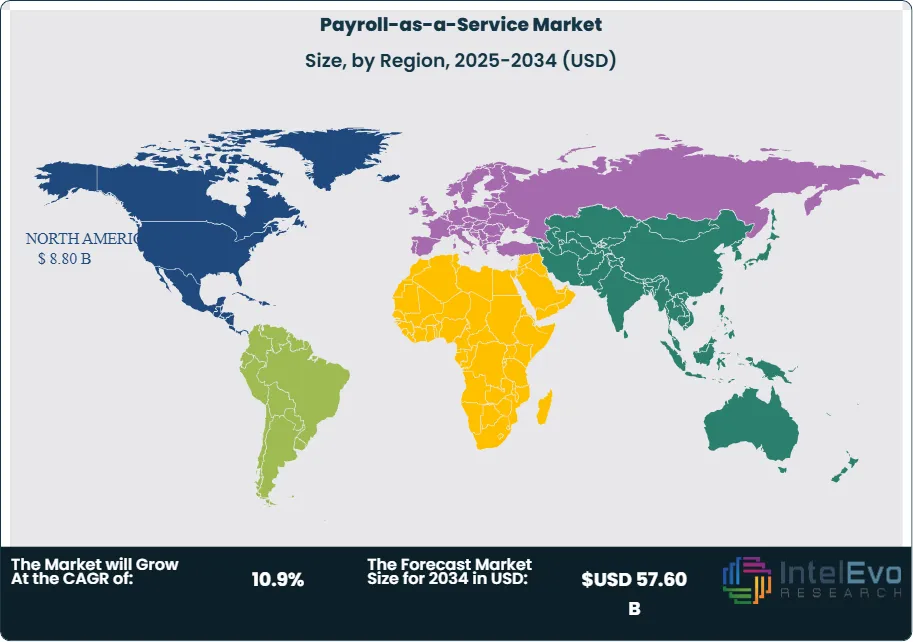

North America held the largest payroll-as-a-service market share at 38.6% in 2025, approximately USD 8.80 Billion, anchored by ADP, Paychex, Gusto, Paylocity, Paycom, Rippling, and Intuit QuickBooks Payroll. Europe held 26.4% through SAP SuccessFactors, Sage, and regional specialists, and Asia Pacific held 24.8% through Ramco Systems, Neeyamo, TMF Group, and emerging Southeast Asian providers. The payroll-as-a-service technology roadmap through 2034 tilts toward AI-driven anomaly detection, embedded fintech (exemplified by Deel generating 25% to 30% of revenue from fintech services and moving over USD 2 Billion monthly across currencies), earned-wage access, and unified HR-IT-Finance platforms where Rippling's 185+ country workforce coverage and ADP's 140-country Celergo plus GlobalView footprint set the benchmark.

Market Definition & Scope

The payroll-as-a-service market is defined as the global commercial activity in cloud-delivered payroll processing, tax filing, benefits administration, time and attendance, reporting, and analytics sold on a subscription or transaction-based model. The market encompasses SaaS platforms (ADP Workforce Now, Paychex Flex, Rippling Payroll, Gusto, Paycom, Paylocity), global multi-country payroll (ADP Celergo, ADP GlobalView, Deel Global Payroll, Papaya Global, Rippling Global Payroll), employer of record (EOR) and professional employer organization (PEO) models, and embedded payroll-fintech capabilities.

Included in the scope are platform subscription revenues, per-employee-per-month fees, PEO service revenues net of wage pass-through, employer-of-record markups, interest on funds held for clients, and fintech FX and payment-rail revenues tied to payroll transactions. Explicitly excluded are pure desktop payroll software licenses without service delivery, accounting-bureau bookkeeping services that are not payroll-primary, and direct-to-consumer tax-filing platforms. The payroll-as-a-service market is a subset of the broader global human capital management (HCM) category and sits adjacent to the larger global HR technology stack.

, By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Organization Size (Large Enterprises, SMEs), By End-User Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The payroll-as-a-service market expands from USD 22.80 Billion in 2025 to USD 57.60 Billion by 2034, a CAGR of 10.9% over the forecast period.

- Segment Dominance by Service Type: Payroll processing led in 2025 with 42.4% share, anchored by ADP, Paychex, Gusto, Rippling, Paylocity, and Paycom core payroll SKUs processing billions of transactions annually.

- Segment Dominance by Deployment: Cloud-based deployment held 74.6% of 2025 revenue, reflecting the dominance of SaaS multi-tenant platforms over on-premises legacy systems.

- Driver: Deel reached a USD 1 Billion annual recurring revenue run rate in Q1 2025 with 75% year-over-year growth at approximately 85% gross margins, validating the global-first payroll category.

- Restraint: Complex multi-jurisdiction compliance remains the largest constraint on growth, with approximately 48% of US employers struggling to navigate multi-state tax variations per IRS compliance research.

- Opportunity: Global payroll expansion is the fastest-growing sub-segment, with Deel covering payroll in 130+ countries and EOR in 150+ countries, and Rippling covering 185+ countries.

- Trend: AI-embedded payroll anomaly detection and embedded fintech expanded in 2025, with approximately 61% of newly launched HR products featuring machine-learning algorithms and Deel generating 25% to 30% of revenue from fintech services.

- Regional: North America led the payroll-as-a-service market with 38.6% share and approximately USD 8.80 Billion in revenue in 2025, followed by Europe at 26.4%.

Key Insights Summary

- ADP reported fiscal 2025 (ended June 30, 2025) revenue of USD 20.6 Billion (up 7%), net earnings of USD 4.1 Billion (up 9%), and adjusted EBIT margin of 26.0% (expanded 50 basis points), and issued fiscal 2026 guidance of 5% to 6% revenue growth and 50 to 70 basis-point adjusted EBIT margin expansion in its July 30, 2025 earnings release filed with the SEC on Form 8-K.

- Paychex reported fiscal 2025 (ended May 31, 2025) total revenue of USD 5.57 Billion, up 5.56% year-over-year, with Q4 FY25 revenue of USD 1.43 Billion up 10%, and Q2 FY2026 revenue of USD 1.56 Billion up 18% year-over-year with Management Solutions revenue up 21% to USD 1.17 Billion, per the Paychex December 2025 Form 8-K earnings filing.

- Deel hit a USD 1 Billion annual recurring revenue run rate in Q1 2025 with 75% year-over-year growth, achieved profitability in Q3 2023, reached a 16% EBITDA margin and approximately 85% gross margins in 2025 (versus ADP at 46% gross margin), and generates 25% to 30% of revenue from fintech services moving over USD 2 Billion monthly, per Sacra's April 2025 analyst report.

- Rippling reached USD 570 Million annual recurring revenue in February 2025 at a USD 13.5 Billion valuation across 25,000+ customers, covers workforces in 185+ countries, scores 4.8/5.0 on G2 from 10,000+ verified users (versus ADP's 4.2/5.0 from 3,700+ users), and charges approximately USD 8 per employee per month starting pricing per Remotexa September 2025 comparative analysis.

- Gusto generated USD 600 Million of 2023 revenue, has been free cash flow positive since early 2023, conducted a USD 200+ Million tender offer at a USD 9.3 Billion valuation, and targets 150,000 new SMB customers in 2025 per SaaStr's July 2025 coverage of the USD 400 Billion-plus HR technology market.

- US digital payroll and HR solution adoption reached 73% of mid-to-large enterprises by 2025, with the US accounting for approximately 32% of the global market, 67% of global organizations on digital payroll platforms, 1.2 Billion-plus workers managed through digital payroll systems, 61% of newly launched HR products featuring ML algorithms, and 41% of new deployments representing SMEs per Industry Research and 360 Research Reports.

- India's Reserve Bank of India-administered Trade Receivables Discounting System (TReDS) mandate effective March 2025 interacts with payroll-adjacent workforce finance through earned-wage-access extensions, and India's Code on Wages 2019 plus Code on Social Security 2020 consolidate multi-statute payroll frameworks, supporting Ramco Systems' continued domestic leadership and Neeyamo's global payroll expansion.

Competitive Landscape Overview

The payroll-as-a-service market is fragmented across three tiers. The top four companies, ADP, Paychex, Deel, and Rippling, represented an estimated 43.6% of combined 2025 revenue based on public disclosures, private ARR estimates, and analyst commentary. Competition is platform-breadth and multi-country coverage led rather than price-led, because ERP integration depth, country-footprint, and compliance sophistication drive enterprise and mid-market renewal economics more than per-employee pricing stickers.

Competitive dynamics shifted materially through 2025. Deel passed USD 1 Billion ARR with 75% year-over-year growth and is preparing for an IPO after eliminating third-party EOR partners (which had charged 20% to 30% fees) and replacing local payroll processors (typically taking 15% markups) with Deel's own payroll engine. Rippling crossed USD 570 Million ARR in February 2025 at a USD 13.5 Billion valuation with 25,000+ customers after expanding into global payroll and EOR. Gusto completed a USD 200+ Million tender offer at a USD 9.3 Billion valuation. Traditional incumbents invested in AI: ADP deepened automation across its 140-country Celergo plus GlobalView footprint, Paychex scaled Paychex Flex AI features, and Paylocity extended its Blue Marble global-payroll acquisition across more than 100 countries. Market cap benchmarks as of April 2025 included ADP at approximately USD 121.9 Billion and Paychex at approximately USD 49.2 Billion per Sacra.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Automatic Data Processing, Inc. (NASDAQ: ADP) | United States | Leader | ADP Workforce Now; ADP Celergo; ADP GlobalView; RUN by ADP | North America, Europe, APAC | Reported FY2025 revenue of USD 20.6 Billion (up 7%) and issued FY2026 guidance of 5% to 6% revenue growth on July 30, 2025 |

| Paychex, Inc. (NASDAQ: PAYX) | United States | Leader | Paychex Flex; Paychex PEO; Paychex HR Solutions | North America | Reported Q2 FY2026 revenue of USD 1.56 Billion, up 18% year-over-year, per Paychex's December 2025 earnings filing |

| Deel, Inc. | United States | Leader | Deel Global Payroll; Deel EOR; Deel Contractor Payments | Global (130+ payroll, 150+ EOR) | Achieved USD 1 Billion ARR run rate with 75% year-over-year growth in Q1 2025 while preparing for an IPO |

| Rippling People Center, Inc. | United States | Leader | Rippling Payroll; Rippling Global Payroll; Rippling EOR | Global (185+ countries) | Reached USD 570 Million ARR in February 2025 at a USD 13.5 Billion private valuation across 25,000+ customers |

| Gusto, Inc. | United States | Challenger | Gusto Payroll; Gusto Benefits; Gusto Embedded | North America | Conducted a USD 200+ Million tender offer in 2025 at a USD 9.3 Billion valuation, targeting 150,000 new SMB customers |

| Paylocity Corporation (NASDAQ: PCTY) | United States | Challenger | Paylocity Web Pay; Paylocity Global Payroll via Blue Marble | North America | Scaled Blue Marble global payroll integration across 100+ countries to complement US SMB and mid-market platform |

| Paycom Software, Inc. (NYSE: PAYC) | United States | Challenger | Paycom Payroll; Beti self-service payroll | North America | Expanded Beti employee-driven payroll adoption across US mid-market through 2025 |

| Papaya Global Ltd. | Israel | Challenger | Papaya Global Payroll; Papaya EOR; Papaya Workforce OS | Global (160+ countries) | Extended segregated IBAN account architecture and 24/7 payment monitoring for global distributed teams |

| SAP SE (ETR: SAP) | Germany | Niche Player | SAP SuccessFactors Employee Central Payroll | Global | Deepened SAP SuccessFactors Payroll integration with SAP S/4HANA Cloud across multinational enterprise customers |

| Workday, Inc. (NASDAQ: WDAY) | United States | Niche Player | Workday Payroll; Workday Global Payroll Connect | North America, Europe, APAC | Expanded Workday Global Payroll Connect certified-partner network for multi-country enterprise payroll coverage |

Segmentation Analysis

The payroll-as-a-service market segments by service type, deployment mode, organization size, and end-user vertical. Each segmentation type maps to distinct buying criteria on a payroll-as-a-service procurement checklist, including country coverage, ERP integration depth, SOC 2 Type II certification, and per-employee pricing transparency.

By Service Type

Payroll processing led the payroll-as-a-service market at 42.4% share in 2025, approximately USD 9.67 Billion, representing core direct-deposit, gross-to-net calculation, and check-run services. Tax filing and compliance services held 19.8%, approximately USD 4.51 Billion, including IRS Form 941 quarterly filings, state unemployment insurance reporting, and year-end W-2 and 1099 generation. Benefits administration held 13.6%, approximately USD 3.10 Billion, covering health insurance enrollment, 401(k) plan administration, and flexible spending accounts.

Time, attendance, and scheduling held 9.2%, approximately USD 2.10 Billion, with growing integration of biometric and location-based timekeeping. Global payroll and employer of record (EOR) services held 8.4%, approximately USD 1.92 Billion, the fastest-growing sub-segment at approximately 22% CAGR through 2034 led by Deel, Rippling, Papaya Global, and ADP Celergo plus GlobalView. Reporting and analytics held 4.2%, and earned-wage access and payroll-linked fintech held 2.4%, approximately USD 547 Million, with Deel generating 25% to 30% of its revenue from fintech services moving over USD 2 Billion monthly.

By Deployment Mode

Cloud-based deployment led the payroll-as-a-service market at 74.6% share in 2025, approximately USD 17.01 Billion, reflecting the dominance of SaaS multi-tenant platforms including ADP Workforce Now, Paychex Flex, Rippling, Gusto, Paycom, Paylocity Web Pay, Deel, and Papaya Global. Cloud adoption is projected to capture approximately 46% of the broader payroll and HR solutions market by 2035 per Research Nester, with employer preference for automatic updates, 24/7 accessibility, and lower infrastructure cost. On-premises deployment held 25.4%, approximately USD 5.79 Billion, concentrated in large banks with legacy mainframe payroll (often running ADP-acquired or Ultimate Software installations), government agencies, and sovereign-cloud-restricted deployments.

The fastest-growing deployment sub-segment is hybrid cloud with sovereign-data-residency architecture, exemplified by sovereign-cloud payroll deployments in regulated European, Indian, and Middle Eastern markets. Cloud-based HR deployments in the US accounted for 57% of active installations among American enterprises in 2025 per 360 Research Reports, and US cloud-based HR solutions grew by approximately 39% since 2022.

By Organization Size

Large enterprises held the largest share of the payroll-as-a-service market at 56.8% in 2025, approximately USD 12.95 Billion, anchored by ADP Celergo and GlobalView multi-country deployments, Workday Payroll, SAP SuccessFactors Employee Central Payroll, and Deel enterprise programs. Large enterprise pricing benchmarks reach USD 500 to USD 600 per employee per month for ADP enterprise outsourcing models per Rippling's October 2025 competitive analysis. Small and medium-sized enterprises (SMEs) held 43.2%, approximately USD 9.85 Billion, led by Gusto (targeting 150,000 new SMBs in 2025), Paychex Flex (800,000+ clients), Rippling at approximately USD 8 per employee per month, QuickBooks Payroll, OnPay, and Wave Payroll.

The fastest-growing organization-size sub-segment is US small-size companies, which held 47.15% of the US payroll services market share in 2025 and are projected to log a 10.95% CAGR through 2031 per Mordor Intelligence. SMB adoption is supported by Paychex's dedicated account manager model, Gusto's free-cash-flow-positive financial profile since early 2023, and Rippling's all-in-one HR-IT-Finance SKU bundles. Enterprise renewal risk is rising for legacy platforms, with Rippling scoring 4.8/5.0 on G2 versus ADP's 4.2/5.0 per Rippling's September 2025 comparative disclosure, highlighting user-experience divergence between modern unified platforms and legacy acquisition-assembled stacks.

By End-User Vertical

Healthcare held the largest US payroll services vertical share at 21.05% in 2025 per Mordor Intelligence, propelled by multi-layer wage rules and union accords including shift differentials, on-call premiums, and statutory overtime multipliers requiring configurable rule engines. Professional services held 17.85%, supporting granular project billing and client cost allocation. Manufacturing held 10.90%, relying on providers for prevailing wage compliance, union payroll, and complex overtime averaging. Information technology was the fastest-growing US vertical at an expected 10.49% CAGR through 2031, driven by stock-based compensation and fully remote workforces operating across tax regimes.

BFSI (banking, financial services, and insurance) held 9.2% of the global payroll-as-a-service market in 2025, anchored by regulated SOX compliance requirements and high-assurance audit trails. Retail and consumer goods held 8.6%, government held 6.4%, hospitality held 4.8%, education held 3.6%, and other verticals including logistics, energy, and non-profit held 7.6%. The payroll-as-a-service compliance requirements vary by vertical, with FLSA overtime rules, state-level minimum wage statutes, and California AB5 independent-contractor classification imposing the highest configurability demands.

Regional Analysis

The payroll-as-a-service market is geographically led by North America, Europe, and Asia Pacific, together accounting for 89.8% of 2025 revenue. Regional dynamics differ on regulatory posture, multi-country payroll complexity, and vendor ecosystem maturity, with North America leading on platform scale and Asia Pacific recording the fastest growth.

North America

North America held 38.6% of the payroll-as-a-service market in 2025, approximately USD 8.80 Billion. The United States dominates through ADP in Roseland, New Jersey, Paychex in Rochester, New York, Intuit QuickBooks Payroll in Mountain View, Gusto in San Francisco, Rippling in San Francisco, Paylocity in Schaumburg, Paycom in Oklahoma City, Workday in Pleasanton, and TriNet. Canada hosts Ceridian Dayforce (now Dayforce Inc.) in Minneapolis with Canadian roots. Mexico is served primarily via ADP Mexico and regional partners. US digital payroll adoption reached 73% of mid-to-large enterprises by 2025 per Industry Research, and US cloud-based HR solutions grew by approximately 39% since 2022. The South controlled 34.98% of the US payroll services market in 2025 with 8.05% projected CAGR through 2031, buoyed by corporate relocations to Texas and Florida per Mordor Intelligence.

Europe

Europe accounted for 26.4% of the payroll-as-a-service market in 2025, approximately USD 6.02 Billion. Germany leads through SAP SE's SuccessFactors Employee Central Payroll in Walldorf and DATEV bookkeeping integrations. The United Kingdom leads through Sage Group plc in Newcastle, MHR, and Moorepay. France hosts ADP France, Silae, and Sage France. The Netherlands hosts SD Worx (via acquisitions), and Belgium hosts Partena Professional and Acerta. Europe's regulatory complexity includes GDPR cross-border payroll-data flows, the EU Pay Transparency Directive (Directive (EU) 2023/970), and the EU AI Act's general-purpose AI provisions effective August 2, 2025 which intersect with AI-enhanced payroll-anomaly detection and anti-fraud tooling. The UK's HMRC PAYE and RTI frameworks underpin British payroll compliance requirements.

Asia Pacific

Asia Pacific held 24.8% of the payroll-as-a-service market in 2025, approximately USD 5.65 Billion, and recorded the fastest regional growth per Mordor Intelligence's 2025-2030 forecast. India hosts Ramco Systems in Chennai, Neeyamo in Pune, and Greythr supporting domestic and offshore payroll. Singapore hosts Payboy, Justlogin, and serves as a regional headquarters for Papaya Global APAC operations. Australia hosts MYOB, Xero Payroll, and Employment Hero. Japan hosts Works Applications and SmartHR. China hosts Kingdee and Yonyou domestic payroll modules. India's Code on Wages 2019 and Code on Social Security 2020 consolidate earlier statutes into integrated payroll frameworks, and the Ministry of Labour and Employment's e-Shram portal expansion through 2024-2025 supports formal-sector payroll integration. Japan's Ministry of Health, Labour and Welfare's Social Insurance Agency reforms continue to drive enterprise-grade payroll compliance investment.

Latin America

Latin America held 5.2% of the payroll-as-a-service market in 2025, approximately USD 1.19 Billion. Brazil leads through Senior Sistemas, TOTVS, and domestic payroll modules, with Deel and Papaya Global serving multinational employers. Mexico follows through Meta4, Aspel Nomina, and CONTPAQi. Argentina, Chile, and Colombia contribute growing SCF platform deployments. Brazil's eSocial electronic reporting framework, administered by Receita Federal, mandates digital payroll reporting for all employers, driving continuous cloud-payroll platform adoption. Mexico's IMSS (Instituto Mexicano del Seguro Social) and INFONAVIT electronic reporting requirements similarly anchor domestic vendor scale, and Colombia's PILA (Planilla Integrada de Liquidacion de Aportes) framework drives local specialist platform adoption.

Middle East & Africa

Middle East & Africa accounted for 5.0% of the payroll-as-a-service market in 2025, approximately USD 1.14 Billion. The United Arab Emirates leads regional adoption through Bayzat, PeopleHum, and ADP Middle East, with the Wage Protection System (WPS) mandated by the UAE Ministry of Human Resources and Emiratisation driving digital-payroll compliance. Saudi Arabia follows through Mudad, Palm HR, and domestic providers aligned with Vision 2030 digital-workforce transformation. South Africa hosts Sage VIP, SimplePay, and Payspace (which was acquired by Deel). Egypt contributes through Etijah Technology and regional payroll specialists. Sub-Saharan Africa is anchored by Workpay, PayDay, and regional digital-payroll ventures. The region's compliance requirements include the UAE's Federal Decree-Law No. 33 of 2021 on the Regulation of Labour Relations, South Africa's Basic Conditions of Employment Act, and Egypt's Labour Law No. 12 of 2003 updated through 2024.

Country Analysis

Four national payroll-as-a-service markets, the United States, the United Kingdom, Germany, and India, collectively accounted for approximately 58.2% of 2025 revenue. These countries concentrate platform vendor headquarters, regulatory complexity, and the workforce scale that sets payroll-as-a-service procurement priorities.

United States

The United States represented approximately USD 7.30 Billion in 2025 payroll-as-a-service revenue, with a country CAGR estimated at 11.2% through 2034. ADP in Roseland, Paychex in Rochester, Intuit QuickBooks Payroll, Gusto, Rippling, Paylocity, Paycom, Workday, and TriNet anchor the national platform supplier base. The IRS administers Form 941 quarterly federal tax filings, and the Department of Labor enforces FLSA overtime rules. State-level complexity includes California AB5 independent-contractor classification, New York's NYSDOL WARN Act, Texas Workforce Commission unemployment insurance, and Florida Department of Economic Opportunity frameworks. The US Bureau of Labor Statistics reported employer costs for employee compensation averaging USD 44.40 per hour worked in September 2024, with benefits accounting for a meaningful share of total compensation, supporting continued payroll outsourcing. The US payroll software market alone is expected to reach USD 47 Billion by 2028 per Deel's market analysis.

United Kingdom

The United Kingdom represented approximately USD 1.78 Billion in 2025 payroll-as-a-service revenue, with a country CAGR estimated at 9.8% through 2034. Sage Group plc in Newcastle, MHR, Moorepay, ADP UK, Paycircle, and IRIS Software anchor the national platform base. HMRC administers PAYE and Real Time Information (RTI) reporting, with full Making Tax Digital for Payroll integration in force through 2024-2025. The Pensions Regulator enforces auto-enrolment obligations under the Pensions Act 2008 as amended, and the UK Gender Pay Gap Reporting Regulations administered by the Equalities Office add mandatory annual disclosures. The UK's 2017 IR35 off-payroll working rules shape contractor-versus-employee classification, influencing Deel, Remote, and Rippling contractor-payment product design. The UK Information Commissioner's Office (ICO) oversees UK GDPR compliance for payroll data.

Germany

Germany represented approximately USD 1.31 Billion in 2025 payroll-as-a-service revenue, with a country CAGR estimated at 10.2% through 2034. SAP SE in Walldorf anchors the global enterprise HCM leadership alongside domestic specialists including DATEV, Sage Germany, P&I, SD Worx Germany, and ADP Germany. The Bundeszentralamt fur Steuern (BZSt) and Elster Online Portal govern German payroll tax and social insurance reporting. The Deutsche Rentenversicherung (German pension insurance) and statutory health insurance funds add required monthly reporting. German Works Council (Betriebsrat) co-determination rights under the Works Constitution Act (Betriebsverfassungsgesetz) influence payroll-system selection for enterprises with 5+ employees. The EU Pay Transparency Directive (Directive (EU) 2023/970), which member states must transpose by June 2026, adds gender pay-gap reporting obligations.

India

India represented approximately USD 878 Million in 2025 payroll-as-a-service revenue, with a country CAGR estimated at 13.4% through 2034, the fastest among the four profiled countries. Ramco Systems in Chennai, Neeyamo in Pune, Greythr, Zoho Payroll, and Keka anchor the domestic platform supplier base. The Central Board of Direct Taxes (CBDT) administers TDS (Tax Deducted at Source) for salary income, and the Employees' Provident Fund Organisation (EPFO) administers Provident Fund compliance. The Code on Wages 2019, Code on Social Security 2020, Industrial Relations Code 2020, and Occupational Safety, Health and Working Conditions Code 2020 consolidated 29 earlier central-level statutes into integrated frameworks. The Ministry of Labour and Employment's e-Shram portal, launched in 2021 and expanded through 2024-2025, supports unorganized-sector worker registration. India's Digital Personal Data Protection Act, 2023 (DPDP Act) adds data-protection requirements to cross-border payroll processing.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Service Type

- Payroll Processing Services

- Tax Filing & Compliance Services

- Managed Payroll Services

- Multi-Country Payroll Services

- Payroll Analytics & Reporting Services

- Employee Self-Service & Payroll Administration Services

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By End-User Vertical

- BFSI

- IT & Telecommunications

- Healthcare & Life Sciences

- Manufacturing

- Retail & E-Commerce

- Government & Public Sector

- Education

- Hospitality & Travel

- Others (Media, Logistics, Energy & Utilities)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 22.80 B |

| Forecast Revenue (2034) | USD 57.60 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Payroll Processing Services, Tax Filing & Compliance Services, Managed Payroll Services, Multi-Country Payroll Services, Payroll Analytics & Reporting Services, Employee Self-Service & Payroll Administration Services), By Deployment Mode, (Cloud-Based, On-Premises, Hybrid), By Organization Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User Vertical, (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel, Others (Media, Logistics, Energy & Utilities)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AUTOMATIC DATA PROCESSING, INC. (NASDAQ: ADP), PAYCHEX, INC. (NASDAQ: PAYX), DEEL, INC., RIPPLING PEOPLE CENTER, INC., GUSTO, INC., PAYLOCITY CORPORATION (NASDAQ: PCTY), PAYCOM SOFTWARE, INC. (NYSE: PAYC), PAPAYA GLOBAL LTD., SAP SE (ETR: SAP), WORKDAY, INC. (NASDAQ: WDAY), ORACLE CORPORATION (NYSE: ORCL), SAGE GROUP PLC (LON: SGE), TRINET GROUP, INC. (NYSE: TNET), DAYFORCE, INC. (NYSE: DAY), INTUIT INC. (NASDAQ: INTU) / QUICKBOOKS PAYROLL, RAMCO SYSTEMS LIMITED (BOM: 532370), NEEYAMO ENTERPRISE SOLUTIONS PVT LTD, TMF GROUP B.V., REMOTE TECHNOLOGY, INC., BAMBOOHR LLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Organization Size (Large Enterprises, SMEs), By End-User Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Organization Size (Large Enterprises, SMEs), By End-User Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Organization Size (Large Enterprises, SMEs), By End-User Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Payroll-as-a-Service Market?

The Global Payroll-as-a-Service Market was valued at USD 20.65 Billion in 2024 and is projected to reach USD 57.60 Billion by 2034, growing at a CAGR of 10.9% from 2026 to 2034. Growth is driven by increasing adoption of payroll automation, cloud-based HR platforms, workforce management solutions, payroll outsourcing services, regulatory compliance requirements, AI-powered payroll processing, remote workforce expansion, and integrated human capital management technologies worldwide.

Who are the major players in the Payroll-as-a-Service Market?

AUTOMATIC DATA PROCESSING, INC. (NASDAQ: ADP), PAYCHEX, INC. (NASDAQ: PAYX), DEEL, INC., RIPPLING PEOPLE CENTER, INC., GUSTO, INC., PAYLOCITY CORPORATION (NASDAQ: PCTY), PAYCOM SOFTWARE, INC. (NYSE: PAYC), PAPAYA GLOBAL LTD., SAP SE (ETR: SAP), WORKDAY, INC. (NASDAQ: WDAY), ORACLE CORPORATION (NYSE: ORCL), SAGE GROUP PLC (LON: SGE), TRINET GROUP, INC. (NYSE: TNET), DAYFORCE, INC. (NYSE: DAY), INTUIT INC. (NASDAQ: INTU) / QUICKBOOKS PAYROLL, RAMCO SYSTEMS LIMITED (BOM: 532370), NEEYAMO ENTERPRISE SOLUTIONS PVT LTD, TMF GROUP B.V., REMOTE TECHNOLOGY, INC., BAMBOOHR LLC, Others

Which segments covered the Payroll-as-a-Service Market?

By Service Type, (Payroll Processing Services, Tax Filing & Compliance Services, Managed Payroll Services, Multi-Country Payroll Services, Payroll Analytics & Reporting Services, Employee Self-Service & Payroll Administration Services), By Deployment Mode, (Cloud-Based, On-Premises, Hybrid), By Organization Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User Vertical, (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, Government & Public Sector, Education, Hospitality & Travel, Others (Media, Logistics, Energy & Utilities))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date