- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

PCB Manufacturer Insurance Market Size, Share & Forecast | CAGR 8.2%

Global PCB Manufacturer Insurance Market Size, Share, Growth Analysis By Insurance Type (General Liability Insurance, Product Liability Insurance, Property Insurance, Workers’ Compensation Insurance, Professional Liability Insurance, Others), By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution Channel (Direct, Brokers/Agents, Online) Industry Segment Overview, Risk Coverage Trends, Market Dynamics, Competitive Landscape, Strategic Developments & Forecast 2026–2034

Report Overview

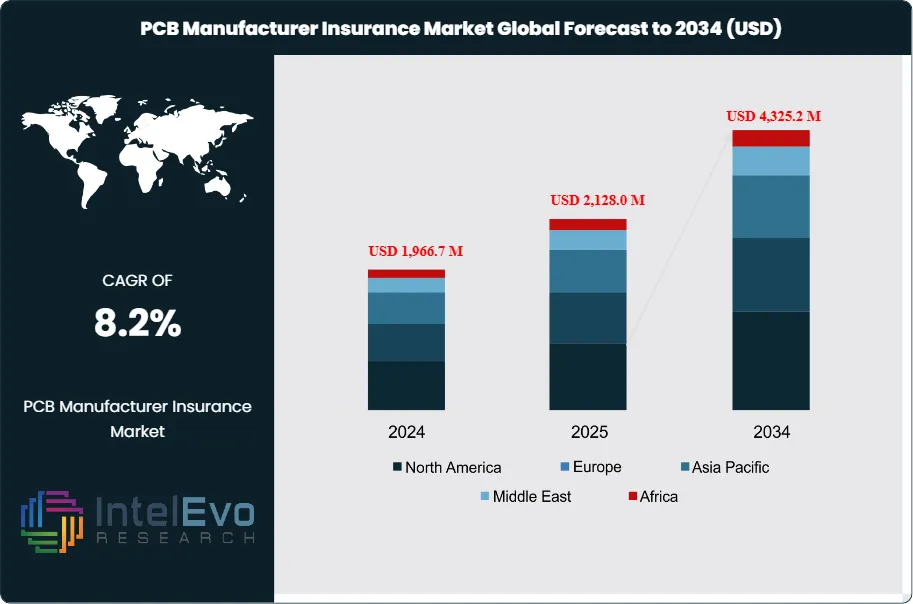

The PCB Manufacturer Insurance Market was valued at USD 1,966.7 million in 2024 and is projected to reach approximately USD 2,128.0 million in 2025. The market is further expected to expand to nearly USD 4,325.2 million by 2034, registering a compound annual growth rate (CAGR) of about 8.2% during the forecast period from 2026 to 2034. Growth in the market is driven by increasing demand for specialized insurance coverage for electronics manufacturing risks, including equipment damage, supply chain disruptions, cyber threats, and product liability. PCB manufacturers operate in highly complex production environments, which increases exposure to operational and technological risks.

Get More Information about this report -

Request Free Sample ReportAdditionally, the expansion of the global electronics, semiconductor, and consumer electronics industries, along with stricter compliance and risk management requirements, is encouraging manufacturers to adopt comprehensive insurance solutions to protect assets and ensure business continuity.

Growth tracks the rising value density of electronics production and the mounting cost of interruption across multilayer, HDI, and advanced substrate lines. Premium expansion also reflects higher insured limits as plants scale capex for imaging, drilling, plating, and cleanroom-controlled processes that carry tight uptime tolerances.

Demand strengthens as PCB producers serve regulated end-markets where a single defect can trigger recalls, warranty claims, and contractual penalties. Automotive electrification, aerospace reliability requirements, and medical device traceability increase manufacturers’ exposure to product liability and errors-and-omissions claims tied to field failures. Supply-side forces also lift coverage uptake. Insurers and brokers offer more specialized wordings that bundle property, machinery breakdown, business interruption, cargo, and environmental liability, while tightening exclusions and deductibles for fire, chemical releases, and contamination events. A hardening reinsurance backdrop and higher catastrophe modeling loss costs keep pricing disciplined, especially for flood and typhoon zones.

Regulation acts as a direct catalyst. Stricter controls on wastewater, heavy metals, and solvent handling, along with expanding ESG disclosures, raise compliance stakes and amplify remediation cost risk. As a result, manufacturers increase limits for pollution legal liability and invest in risk engineering, suppression systems, and monitoring to defend underwriting terms. Cyber risk increasingly enters underwriting because design files, CAM data, and factory OT networks face ransomware and IP theft threats that can halt production and compromise customers’ programs.

Technology shifts reshape both risk and underwriting. Automation and advanced process control reduce defect rates but concentrate exposure in fewer high-throughput tools. AI-enabled inspection and predictive maintenance improve loss prevention, while AI-driven underwriting accelerates quote-to-bind cycles using sensor feeds, claims history, and supplier telemetry. Digital claims handling and parametric triggers for outage and catastrophe events gain adoption in large, multi-site accounts.

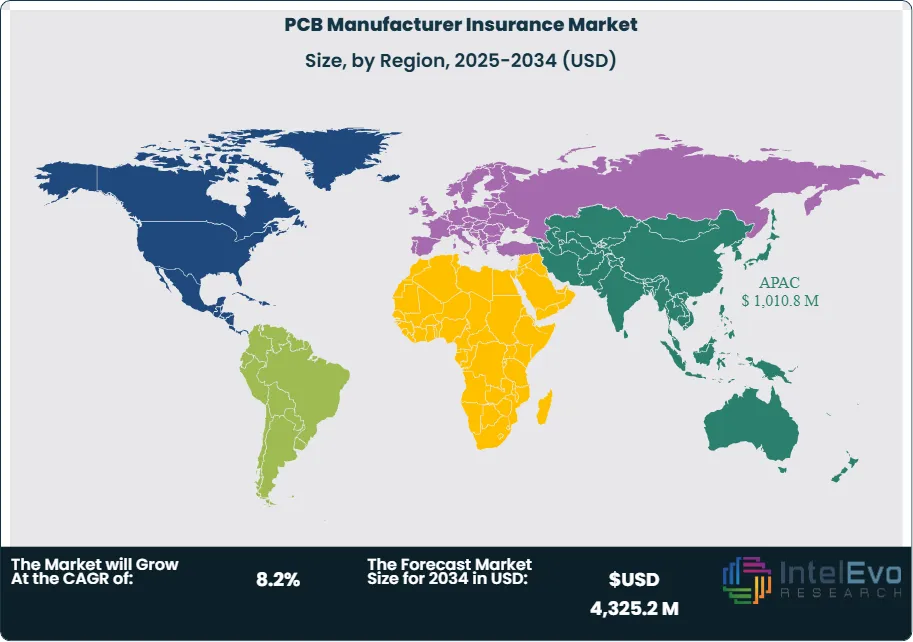

Asia Pacific led in 2024 with more than 47.5% share and USD 934.18 million revenue, supported by dense manufacturing clusters and expanding investment in China-plus-one capacity. India, Vietnam, Malaysia, and Thailand stand out as emerging hotspots as new plants seek export compliance and bank-mandated insurance programs. North America and Europe together are estimated to account for roughly 40–45% of premiums, driven by high-complexity boards, aerospace programs, and tighter liability norms, while insurers prioritize accounts with strong governance, audited quality systems, and transparent supply-chain controls.

, By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution Channel (Direct, Brokers/Agents, Online) Industry Segment Overview, Risk Coverage Trends, Market Dynamics, Competitive Landscape, Strategic Developments & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market expands at a 8.20% CAGR, 2026-2034, supported by scaling PCB output and broader risk-transfer adoption. It reaches estimated: 4.3 billion USD, 2034.

- Segment Dominance: Property insurance leads with 32.5% share, 2024, as manufacturers insure plants, tools, and inventory against fire and catastrophe loss. It represents estimated: 0.6 billion USD, 2024.

- Segment Dominance: Insurance companies lead with 91.3% share, 2024, by underwriting PCB-specific property, liability, and workers’ compensation programs. They generate estimated: 1.8 billion USD, 2024.

- Driver: Regulatory compliance and complex supply chains raise demand for comprehensive coverage, lifting large-enterprise participation to 73.2% share, 2024. Large enterprises contribute estimated: 1.4 billion USD, 2024.

- Restraint: Pricing pressure rises as brokers/agents capture 85.9% share, 2024, and negotiate higher limits amid higher modeled loss costs. Commission and placement costs reach estimated: 0.2 billion USD, 2024.

- Opportunity: Underwriters expand China programs as the China market reaches 283.9 million USD, 2025, and capacity follows localized electronics investment. China grows at estimated: 5.0% CAGR, 2024-2034.

- Trend: Carriers accelerate digital underwriting and automated risk scoring to shorten cycle times and improve loss selection. Automated workflows cover estimated: 35.0% of new submissions, 2025.

- Regional Analysis: Asia Pacific leads with 47.5% share, 2024, supported by dense PCB manufacturing clusters and expanding export supply chains. The region totals estimated: 0.9 billion USD, 2024.

By Type

Property insurance remains the largest line within the PCB manufacturer insurance landscape, accounting for about 32.5 percent of total premiums as of 2025. This segment underpins financial protection for production plants, precision machinery, cleanroom environments, and inventory that together represent a significant share of manufacturers’ balance sheets. As PCB fabrication shifts toward higher layer counts, finer line widths, and capital-intensive automation, insured asset values continue to rise, reinforcing the central role of property coverage.

Operational exposure further strengthens demand. PCB facilities face concentrated risks from fire, power instability, flooding, and equipment failure, all of which can halt production and delay downstream electronics supply chains. Insurers increasingly structure property policies alongside machinery breakdown and business interruption extensions, reflecting manufacturers’ need to restore output quickly and meet contractual delivery schedules in export-driven markets.

By Application

Insurance solutions for PCB manufacturers apply across multiple risk categories, with asset protection and liability coverage forming the core of most programs. Property-related applications dominate due to the high replacement cost of drilling, imaging, and plating equipment, which can exceed several million dollars per line. Coverage structures increasingly align limits with realistic downtime scenarios rather than nominal asset values.

Liability-focused applications are expanding in parallel. Product defects in automotive, industrial control, and medical electronics can trigger recalls and third-party claims that exceed direct manufacturing losses. As quality standards tighten across global OEMs, insurers report higher uptake of combined property and liability programs, particularly among exporters serving regulated industries.

By End-Use

Large enterprises continue to drive demand, representing roughly 73.2 percent of the PCB manufacturer insurance market in 2025. These firms operate multi-site facilities, manage cross-border logistics, and supply high-reliability sectors, which exposes them to layered operational and legal risks. Their insurance portfolios typically span property, general liability, product liability, environmental coverage, and cyber protection.

Scale influences purchasing behavior. Large manufacturers negotiate customized terms, higher sub-limits, and integrated claims services, often securing favorable pricing through long-term insurer relationships. Their emphasis on structured risk governance and audit readiness sustains steady premium growth in this segment, even during periods of electronics demand volatility.

By Region

Asia Pacific remains the leading regional market with approximately 47.5 percent share in 2025, supported by dense PCB manufacturing clusters in China, Taiwan, South Korea, and Japan. Strong output in consumer electronics, electric vehicles, and telecom infrastructure increases exposure to equipment damage, supply disruption, and liability events, driving higher insurance penetration.

China alone generates about USD 283.9 million in premiums and is expanding at a CAGR of roughly 4.9 percent through the forecast period. Growth reflects the country’s role as a global PCB hub, where export compliance, automation, and rising cyber exposure influence coverage decisions. As Chinese manufacturers expand overseas capacity and customer bases, insurance adoption continues to formalize, supporting sustained regional market development.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Insurance Type

- General Liability Insurance

- Product Liability Insurance

- Property Insurance

- Workers’ Compensation Insurance

- Professional Liability Insurance

- Others

By Provider

- Insurance Companies

- Brokers/Agents

- Others

By End-User

- Small and Medium Enterprises

- Large Enterprises

By Distribution Channel

- Direct

- Brokers/Agents

- Online

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2,128.0 M |

| Forecast Revenue (2034) | USD 4,325.2 M |

| CAGR (2025-2034) | 8.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Insurance Type (General Liability Insurance, Product Liability Insurance, Property Insurance, Workers’ Compensation Insurance, Professional Liability Insurance, Others), By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution (Channel, Direct, Brokers/Agents, Online) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AXA XL, Liberty Mutual, Swiss Re, AXA XL, CNA Financial, Munich Re, Tokio Marine HCC, Travelers Insurance, Sompo International, Markel Corporation, Allianz, The Hartford, Berkshire Hathaway, AIG, Zurich Insurance Group, Hanover Insurance Group, QBE Insurance Group, Assurant, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution Channel (Direct, Brokers/Agents, Online) Industry Segment Overview, Risk Coverage Trends, Market Dynamics, Competitive Landscape, Strategic Developments & Forecast 2026–2034")

, By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution Channel (Direct, Brokers/Agents, Online) Industry Segment Overview, Risk Coverage Trends, Market Dynamics, Competitive Landscape, Strategic Developments & Forecast 2026–2034")

, By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution Channel (Direct, Brokers/Agents, Online) Industry Segment Overview, Risk Coverage Trends, Market Dynamics, Competitive Landscape, Strategic Developments & Forecast 2026–2034")

Frequently Asked Questions

How big is the PCB Manufacturer Insurance Market?

Global PCB Manufacturer Insurance Market was valued at USD 1,966.7 million in 2024 and is projected to reach USD 4,325.2 million by 2034, growing at a CAGR of 8.2%. Explore market trends, drivers, and growth opportunities.

Who are the major players in the PCB Manufacturer Insurance Market?

AXA XL, Liberty Mutual, Swiss Re, AXA XL, CNA Financial, Munich Re, Tokio Marine HCC, Travelers Insurance, Sompo International, Markel Corporation, Allianz, The Hartford, Berkshire Hathaway, AIG, Zurich Insurance Group, Hanover Insurance Group, QBE Insurance Group, Assurant, Others

Which segments covered the PCB Manufacturer Insurance Market?

By Insurance Type (General Liability Insurance, Product Liability Insurance, Property Insurance, Workers’ Compensation Insurance, Professional Liability Insurance, Others), By Provider (Insurance Companies, Brokers/Agents, Others), By End-User (Small and Medium Enterprises, Large Enterprises), By Distribution (Channel, Direct, Brokers/Agents, Online)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

PCB Manufacturer Insurance Market

Published Date : 10 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date