- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

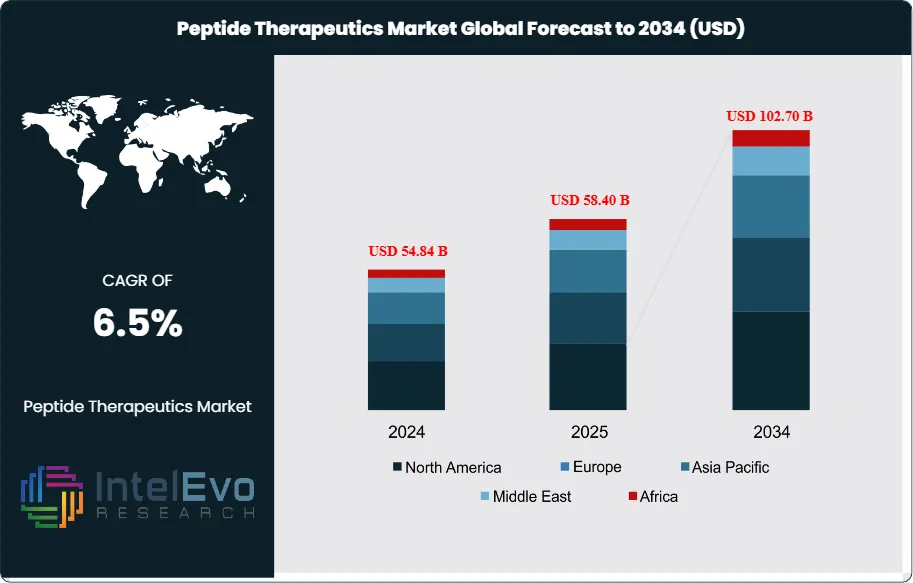

Global Peptide Therapeutics Market Forecast 2034 | CAGR 6.5%

Global Peptide Therapeutics Market Size, Share, Growth & Industry Analysis By Drug Type (Metabolic Peptides, Insulin & Insulin-Analog Peptides, Oncology & Endocrine-Regulatory Peptides, Anti-Infective & Acute-Care Peptides, Gastrointestinal & Rare-Disease Peptides), By Route of Administration (Injectable, Oral, Intranasal & Transdermal, Others), By Therapeutic Area (Metabolic Disorders, Oncology, Endocrine, Gastrointestinal, Infectious Diseases), By Distribution Channel (Hospital, Retail, Specialty Pharmacies) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 58.40 Billion | USD 102.70 Billion | 6.5% | North America, 42.8% |

The Peptide Therapeutics Market was valued at approximately USD 54.84 Billion in 2024 and reached USD 58.40 Billion in 2025. The market is projected to grow to USD 102.70 Billion by 2034, expanding at a CAGR of 6.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 44.30 Billion over the analysis period. The peptide therapeutics market entered 2025 with unusually strong momentum in metabolic disease, obesity care, endocrine therapy, and selected oncology niches. WHO reported that more than 1 billion people were living with obesity in 2022, while the IDF estimated that 589 million adults were living with diabetes in 2024; both figures continue to expand the treated population for GLP-1 and related peptide classes.

Get More Information about this report -

Request Free Sample ReportThe peptide therapeutics market now sits on a broader revenue base than it did three years ago because prescription growth has moved beyond legacy endocrine and hospital-use peptides into chronic cardiometabolic therapy. Novo Nordisk reported 2025 obesity-care sales of DKK 82.3 billion and stated that global branded GLP-1 obesity volume grew 104.0% in 2025, while Eli Lilly reported 2025 revenue of USD 22.97 Billion for Mounjaro and USD 13.54 Billion for Zepbound. Those two companies alone explain why metabolic peptides account for the largest revenue pool in the current market. FDA actions also widened access. The agency approved the first generic referencing Victoza in December 2024, later determined that semaglutide injection shortage conditions had been resolved in February 2025, and continued to support generic development for complex peptide products.

Demand-side strength remains clear, but supply-side execution still shapes revenue realization. Several 2025 industry updates still referred to capacity, device format, and supply continuity as commercial variables. That matters because peptide products require tight control over synthesis, purification, cold-chain handling, device integration, and regulatory comparability. EMA and FDA standards on quality, safety, labeling, and lifecycle management continue to raise the barrier for smaller entrants. In practice, the market rewards firms with integrated peptide chemistry, large-scale fill-finish capacity, and broad reimbursement reach.

Regional investment patterns remain favorable. North America leads due to early obesity-drug uptake, high biologics reimbursement, and FDA-centered launch sequencing. Europe holds a strong second position because of broad endocrine and oncology peptide use and EMA-backed access expansion. Asia Pacific is the fastest-expanding revenue pool on a volume basis, supported by diabetes prevalence, local generic entry, and manufacturing depth in India and China. India added a new access point in March 2026 when Dr. Reddy’s launched a DCGI-approved semaglutide injection for type 2 diabetes. Current market assessment indicates that cardiometabolic peptides, oral delivery formats, and selective genericization will keep peptide therapeutics market growth above the broader small-molecule prescription average through 2034.

, By Route of Administration (Injectable, Oral, Intranasal & Transdermal, Others), By Therapeutic Area (Metabolic Disorders, Oncology, Endocrine, Gastrointestinal, Infectious Diseases), By Distribution Channel (Hospital, Retail, Specialty Pharmacies) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The peptide therapeutics market stood at USD 58.40 Billion in 2025 and is projected to reach USD 102.70 Billion by 2034 at a 6.5% CAGR. Growth is being carried by obesity and diabetes peptides, with branded GLP-1 obesity volume up 104.0% in 2025 at Novo Nordisk and tirzepatide revenue above USD 36.5 Billion at Lilly across Mounjaro and Zepbound.

- Segment Dominance: By drug type, metabolic peptides led the market with a 39.2% share in 2025, equal to about USD 22.89 Billion. This dominance reflects semaglutide, tirzepatide, liraglutide, and adjacent incretin therapy uptake.

- Segment Dominance: By therapeutic area, metabolic disorders accounted for 48.6% of market revenue in 2025, or about USD 28.38 Billion. Diabetes and obesity treatment breadth remains far wider than oncology, gastrointestinal, or reproductive endocrine use.

- Driver: The core driver is rising obesity and diabetes treatment volume. More than 1 billion people were living with obesity in 2022, and 589 million adults lived with diabetes in 2024, creating a very large diagnosed and treatment-eligible pool.

- Restraint: Manufacturing complexity and reimbursement friction continue to limit faster conversion of demand into sales. Supply remained a revenue constraint well into 2025, especially in branded metabolic injectables.

- Opportunity: Oral and less-frequent dosing formats represent the largest expansion window. Oral GLP-1 and monthly obesity regimens support a substantial addressable shift toward easier chronic-use treatment models.

- Trend: The strongest trend is a move from single-mechanism endocrine peptides toward multi-target metabolic regimens and device-enabled delivery. Oral semaglutide, dual incretin franchises, and amylin combinations are reshaping competitive conditions.

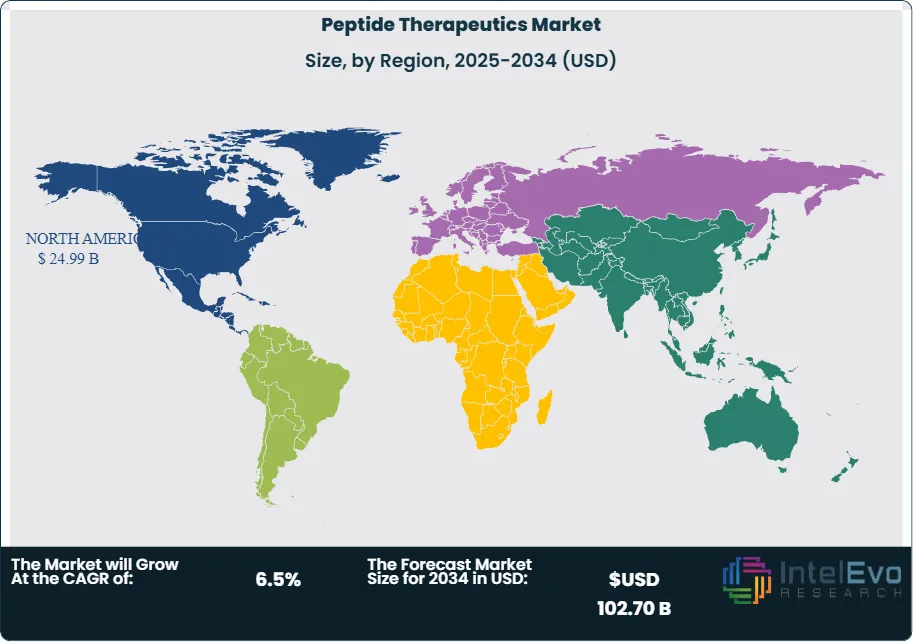

- Regional Analysis: North America led the market in 2025 with 42.8% share, equal to USD 24.99 Billion. The region benefits from early approvals, high branded uptake, and strong obesity-prescription monetization.

Competitive Landscape Overview

The peptide therapeutics market is moderately consolidated. The top four companies controlled an estimated 67.5% of 2025 revenue, with competition centered on metabolic peptides, long-acting injectables, differentiated delivery formats, and lifecycle management. Competitive intensity increased sharply in 2025 as generic liraglutide entered the market, oral GLP-1 programs advanced, and large players expanded manufacturing footprints to defend supply continuity. Novo Nordisk and Eli Lilly set the commercial pace; Ipsen retained strength in neuroendocrine peptide therapy, while Teva pushed pricing pressure through generic GLP-1 entry.

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| Novo Nordisk | Denmark | Leader | Wegovy / Ozempic / Rybelsus | North America, Europe | Closed acquisition of three Catalent sterile fill-finish sites in Dec 2024, expanding global footprint. |

| Eli Lilly and Company | United States | Leader | Mounjaro / Zepbound / orforglipron | North America | Advanced orforglipron regulatory filings and broadened Zepbound access with KwikPen in Feb 2026. |

| Ipsen | France | Challenger | Somatuline Depot / Autogel | Europe, North America | Benefited from generic-lanreotide supply disruption in 2025 and continued franchise support. |

| Teva Pharmaceutical Industries | Israel | Challenger | Generic liraglutide injection | United States | Won FDA approval and U.S. launch for the first generic GLP-1 indicated for weight loss in Aug 2025. |

| Zealand Pharma | Denmark | Niche Player | Petrelintide | Europe | Entered a global collaboration and license agreement with Roche in Mar 2025. |

| Amgen | United States | Niche Player | MariTide | North America | Presented 52-week Phase 2 obesity data in Jun 2025 and advanced the Phase 3 program. |

| Takeda Pharmaceutical Company | Japan | Niche Player | GATTEX / Revestive | North America, Europe | Continued defending short bowel syndrome positioning as lifecycle pressure intensified. |

| Sanofi | France | Niche Player | Insulin glargine franchise | Europe, Latin America | Continued protecting insulin-based peptide revenue through broad geographic coverage. |

By Drug Type

Peptide therapeutics market by drug type. Metabolic peptides accounted for 39.2% of 2025 revenue, or USD 22.89 Billion, and held the clear lead. This block includes semaglutide, tirzepatide, liraglutide, and related agents used in obesity and type 2 diabetes. Insulin and insulin-analog peptides ranked second with a 26.1% share, or USD 15.24 Billion. Oncology and endocrine-regulatory peptides represented 14.8% of revenue, or USD 8.64 Billion. Anti-infective and acute-care peptides contributed 11.7%, or USD 6.83 Billion, while gastrointestinal and rare-disease peptides held the remaining 8.2%, or USD 4.79 Billion. The competitive gap inside this segmentation reflects scale economics, device convenience, and real-world adherence.

By Route of Administration

Peptide therapeutics market by route of administration. Injectable products dominated with an 82.4% share in 2025, equal to USD 48.12 Billion. Most commercial peptide products still require subcutaneous or intravenous delivery to preserve bioavailability and dose control. Oral products reached 9.6% share, or USD 5.61 Billion, due largely to semaglutide tablets and the market’s willingness to back easier chronic-use regimens. Intranasal and transdermal formats held 4.1%, or USD 2.39 Billion, while implants, infusion-based delivery, and other specialized routes captured 3.9%, or USD 2.28 Billion.

By Therapeutic Area

Peptide therapeutics market by therapeutic area. Metabolic disorders led with 48.6% of 2025 revenue, or USD 28.38 Billion, reflecting the combination of obesity, type 2 diabetes, and cardiometabolic risk management. Oncology followed at 16.4%, or USD 9.58 Billion. Endocrine and reproductive disorders represented 14.2%, or USD 8.29 Billion. Gastrointestinal conditions accounted for 10.1%, or USD 5.90 Billion, while infectious disease and other hospital-led uses captured 10.7%, or USD 6.25 Billion.

By Distribution Channel

Peptide therapeutics market by distribution channel. Hospital pharmacies led with 46.8% of 2025 revenue, or USD 27.33 Billion. Retail pharmacies followed at 31.2%, or USD 18.22 Billion, supported by diabetes and obesity self-injection products with large refill volume. Specialty pharmacies accounted for 22.0%, or USD 12.85 Billion, and are gaining share because high-cost peptide therapies often require prior authorization, cold-chain management, patient education, and adherence follow-up.

Regional Analysis

North America

The North America peptide therapeutics market accounted for 42.8% of global revenue in 2025, equal to USD 24.99 Billion. The United States represented the clear center of gravity due to FDA-first launches, strong branded uptake, and broader reimbursement for diabetes and obesity therapy than any other single country. Canada added meaningful obesity-drug demand through high-income outpatient care, while Mexico supported volume growth through a large diabetes burden and expanding private-sector access.

Europe

The Europe peptide therapeutics market held 25.1% of 2025 revenue, or USD 14.66 Billion. Germany, France, the UK, and Italy made up the largest country pool due to advanced specialty care, broad endocrine and oncology peptide use, and EMA-aligned regulatory pathways. Europe remains strong in somatostatin analogs, reproductive endocrine peptides, and specialty metabolic treatment.

Asia Pacific

The Asia Pacific peptide therapeutics market represented 21.7% of 2025 revenue, or USD 12.67 Billion. China, Japan, India, and South Korea are the most strategic countries in this region. China and India provide the largest patient pool due to diabetes prevalence and rising obesity rates. Japan remains a high-value market with strong uptake of specialist therapies and rigorous reimbursement controls.

Latin America

The Latin America peptide therapeutics market accounted for 5.6% of global revenue in 2025, or USD 3.27 Billion. Brazil led the region, followed by Mexico, Argentina, and the rest of Latin America. The market is smaller in value terms than its disease burden would suggest because reimbursement remains uneven and branded obesity products still face affordability limits.

Middle East & Africa

The Middle East & Africa peptide therapeutics market held 4.8% of 2025 revenue, equal to USD 2.80 Billion. Saudi Arabia, the UAE, South Africa, and the rest of MEA form the main revenue base. The Gulf states are the strongest commercial pockets because obesity and diabetes prevalence is high and public healthcare budgets can absorb branded metabolic therapies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Drug Type

- Metabolic Peptides

- Insulin and Insulin-Analog Peptides

- Oncology and Endocrine-Regulatory Peptides

- Anti-infective and Acute-Care Peptides

- Gastrointestinal and Rare-Disease Peptides

By Route of Administration

- Injectable

- Oral

- Intranasal and Transdermal

- Other Specialized Routes

By Therapeutic Area

- Metabolic Disorders

- Oncology

- Endocrine and Reproductive Disorders

- Gastrointestinal Disorders

- Infectious Disease and Other Uses

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Specialty Pharmacies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 58.40 B |

| Forecast Revenue (2034) | USD 102.70 B |

| CAGR (2025-2034) | 6.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Drug Type, (Metabolic Peptides, Insulin and Insulin-Analog Peptides, Oncology and Endocrine-Regulatory Peptides, Anti-infective and Acute-Care Peptides, Gastrointestinal and Rare-Disease Peptides), By Route of Administration, (Injectable, Oral, Intranasal and Transdermal, Other Specialized Routes), By Therapeutic Area, (Metabolic Disorders, Oncology, Endocrine and Reproductive Disorders, Gastrointestinal Disorders, Infectious Disease and Other Uses), By Distribution Channel, (Hospital Pharmacies, Retail Pharmacies, Specialty Pharmacies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVO NORDISK, ELI LILLY AND COMPANY, IPSEN, TEVA PHARMACEUTICAL INDUSTRIES, ZEALAND PHARMA, AMGEN, TAKEDA PHARMACEUTICAL COMPANY, SANOFI, RECORDATI, ASCENDIS PHARMA, PFIZER, DR. REDDY'S LABORATORIES, BOEHRINGER INGELHEIM, ROCHE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Route of Administration (Injectable, Oral, Intranasal & Transdermal, Others), By Therapeutic Area (Metabolic Disorders, Oncology, Endocrine, Gastrointestinal, Infectious Diseases), By Distribution Channel (Hospital, Retail, Specialty Pharmacies) Industry Trends & Forecast 2026–2034")

, By Route of Administration (Injectable, Oral, Intranasal & Transdermal, Others), By Therapeutic Area (Metabolic Disorders, Oncology, Endocrine, Gastrointestinal, Infectious Diseases), By Distribution Channel (Hospital, Retail, Specialty Pharmacies) Industry Trends & Forecast 2026–2034")

, By Route of Administration (Injectable, Oral, Intranasal & Transdermal, Others), By Therapeutic Area (Metabolic Disorders, Oncology, Endocrine, Gastrointestinal, Infectious Diseases), By Distribution Channel (Hospital, Retail, Specialty Pharmacies) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Peptide Therapeutics Market?

Global Peptide therapeutics market valued at USD 54.84B in 2024, reaching USD 102.7B by 2034, growing at a CAGR of 6.5% from 2026–2034.

Who are the major players in the Peptide Therapeutics Market?

NOVO NORDISK, ELI LILLY AND COMPANY, IPSEN, TEVA PHARMACEUTICAL INDUSTRIES, ZEALAND PHARMA, AMGEN, TAKEDA PHARMACEUTICAL COMPANY, SANOFI, RECORDATI, ASCENDIS PHARMA, PFIZER, DR. REDDY'S LABORATORIES, BOEHRINGER INGELHEIM, ROCHE, Others

Which segments covered the Peptide Therapeutics Market?

By Drug Type, (Metabolic Peptides, Insulin and Insulin-Analog Peptides, Oncology and Endocrine-Regulatory Peptides, Anti-infective and Acute-Care Peptides, Gastrointestinal and Rare-Disease Peptides), By Route of Administration, (Injectable, Oral, Intranasal and Transdermal, Other Specialized Routes), By Therapeutic Area, (Metabolic Disorders, Oncology, Endocrine and Reproductive Disorders, Gastrointestinal Disorders, Infectious Disease and Other Uses), By Distribution Channel, (Hospital Pharmacies, Retail Pharmacies, Specialty Pharmacies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date