- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharma Cold Chain Logistics Market Forecast 2034 | CAGR 9.9%

Global Pharma Cold Chain Logistics Market Size, Share, Growth & Industry Analysis By Service Type (Transportation Services, Storage & Warehousing, Packaging Solutions, Monitoring & Tracking), By Product Category (Biopharmaceuticals, Vaccines, Cell & Gene Therapies, Clinical Trial Materials), By Temperature Range (Refrigerated, Frozen, Cryogenic) Industry Trends, Supply Chain Insights, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 18.4 Billion | USD 42.8 Billion | 9.9% | North America, 38.5% |

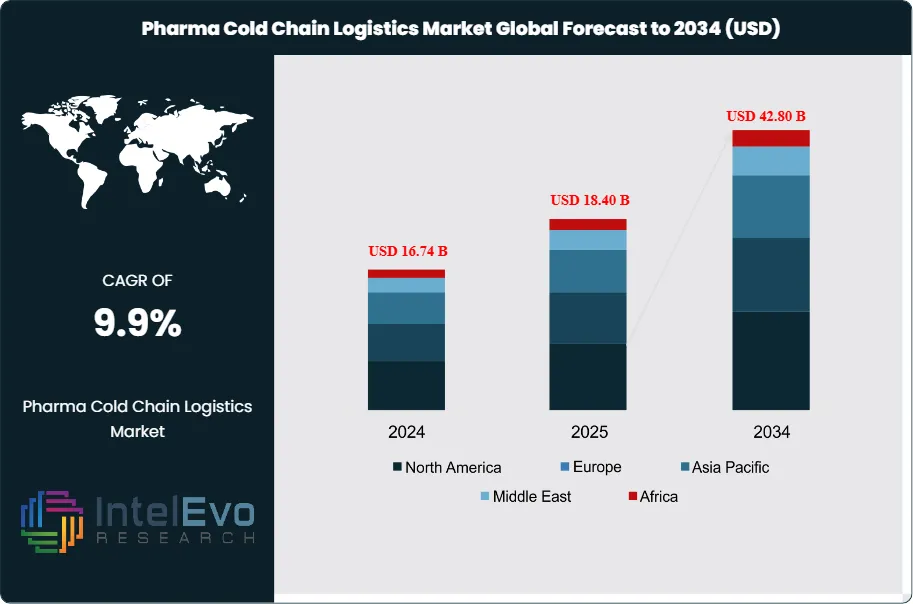

The Pharma Cold Chain Logistics Market was valued at approximately USD 16.74 Billion in 2024 and reached USD 18.40 Billion in 2025. The market is projected to grow to USD 42.80 Billion by 2034, expanding at a CAGR of 9.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 24.4 Billion over the analysis period. Pharma cold chain logistics encompasses temperature-controlled storage, transportation, packaging, and monitoring services required for pharmaceutical products that must maintain specific temperature ranges throughout distribution. The market expansion reflects the accelerating shift toward biologic therapies, mRNA-based vaccines, and cell and gene therapies that require strict temperature control from manufacturing through patient administration.

Get More Information about this report -

Request Free Sample ReportThe pharmaceutical industry's pipeline composition has fundamentally shifted toward temperature-sensitive products. Biologic drugs now represent 42% of the global pharmaceutical pipeline and 55% of new FDA approvals in 2025, compared to 28% in 2015. These products typically require storage between 2 and 8 degrees Celsius, while advanced therapies including CAR-T and gene therapies demand cryogenic conditions below minus 150 degrees Celsius. The pharma cold chain logistics market growth directly correlates with this pipeline evolution. mRNA vaccine platforms established during the COVID-19 pandemic continue to expand applications, with 87 mRNA therapeutics currently in clinical development requiring ultra-cold storage at minus 70 degrees Celsius or below.

Regulatory requirements have intensified across major pharmaceutical markets. The FDA Drug Supply Chain Security Act mandates serialization and temperature documentation for all pharmaceutical shipments. EU Good Distribution Practice guidelines require continuous temperature monitoring with validated packaging and qualified shipping lanes. World Health Organization prequalification standards govern vaccine distribution to over 100 countries, establishing minimum cold chain requirements. Non-compliance penalties have increased 35% since 2022, with temperature excursion events resulting in average product losses of USD 35,000 per incident. The pharma cold chain logistics industry has responded with investments in real-time monitoring technology, validated packaging systems, and expanded temperature-controlled infrastructure.

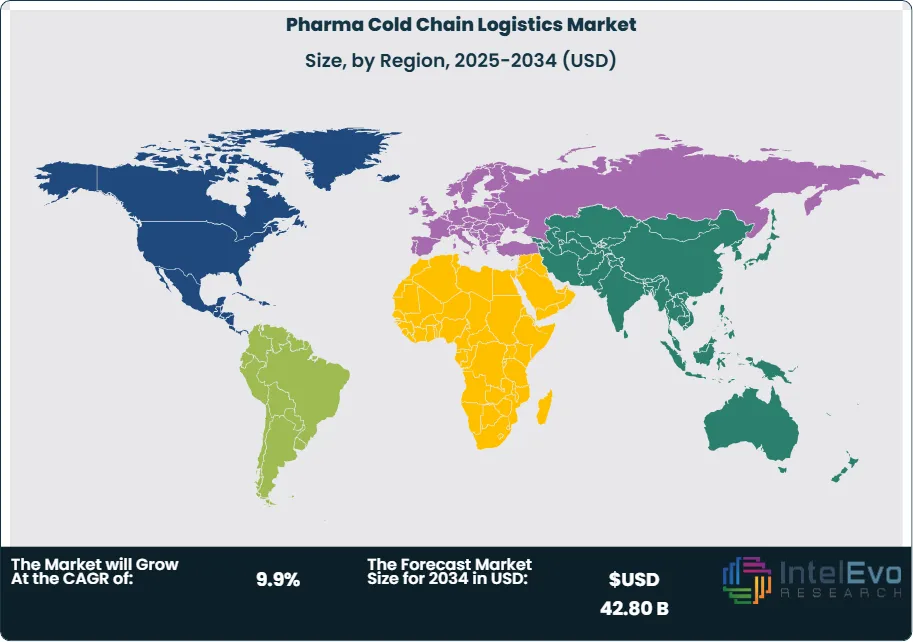

Geographic expansion patterns reveal emerging growth opportunities in pharma cold chain logistics. North America maintains market leadership with 38.5% share in 2025, driven by biopharmaceutical manufacturing concentration and advanced distribution networks. Asia Pacific represents the fastest-growing region at 12.2% CAGR through 2034 as pharmaceutical production expands in China, India, and Southeast Asia. European markets benefit from stringent regulatory frameworks driving quality investments. Latin America and Middle East Africa present infrastructure development opportunities as vaccine distribution programs expand access to previously underserved populations. Cell and gene therapy logistics represent a high-growth niche, with specialized cryogenic services growing at 18.5% annually through the forecast period.

, By Product Category (Biopharmaceuticals, Vaccines, Cell & Gene Therapies, Clinical Trial Materials), By Temperature Range (Refrigerated, Frozen, Cryogenic) Industry Trends, Supply Chain Insights, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The pharma cold chain logistics market expands from USD 18.4 Billion in 2025 to USD 42.8 Billion by 2034, registering a CAGR of 9.9% across the nine-year forecast period.

- Segment Dominance: Transportation services command the largest share by service type at 45.2% in 2025, driven by expanding global distribution networks and specialized vehicle fleet investments.

- Segment Dominance: Biopharmaceuticals and biologics lead product category segmentation with 52.8% market share in 2025, reflecting the pipeline shift toward temperature-sensitive biologic therapies.

- Driver: The surge in biologic drug approvals has increased cold chain logistics demand by 38% since 2020, with 55% of FDA new molecular entity approvals in 2025 requiring temperature-controlled distribution.

- Restraint: Temperature excursion events affect approximately 12% of pharmaceutical shipments annually, causing USD 15 Billion in global product losses and constraining supply chain reliability.

- Opportunity: Cell and gene therapy logistics represent a USD 4.2 Billion incremental opportunity through 2034, with cryogenic transport demand growing at 18.5% CAGR as commercial CGT approvals multiply.

- Trend: Real-time IoT monitoring adoption has reached 68% penetration among major logistics providers in 2025, up from 34% in 2020, enabling predictive temperature management and reducing excursions by 42%.

- Regional Analysis: North America maintains market leadership with 38.5% share representing USD 7.08 Billion in 2025, supported by biopharmaceutical manufacturing concentration and regulatory compliance requirements.

Competitive Landscape Overview

The pharma cold chain logistics market exhibits moderate consolidation with the top four providers controlling approximately 42% of global revenue in 2025. Competition centers on temperature control technology, geographic network coverage, regulatory compliance capabilities, and specialized handling expertise. Mergers and acquisitions have intensified since 2023 as integrated logistics providers seek healthcare vertical depth. DHL Supply Chain, FedEx, UPS Healthcare, and Marken lead through global infrastructure and dedicated pharmaceutical service portfolios. Regional challengers compete on local expertise, particularly in emerging markets where cold chain infrastructure development lags. Technology investment has become a key differentiator, with IoT monitoring platforms, blockchain traceability, and AI-powered route optimization commanding premium pricing.

Competitive Landscape Matrix

| Company Name | HQ | Position | Key Solution | Geographic Strength | Recent Strategic Move (2024-2026) |

| DHL Supply Chain | Germany | Leader | DHL LifeSciences Logistics | Global | Jan 2025: Opened USD 85M cryogenic hub in Indianapolis |

| FedEx Custom Critical | USA | Leader | FedEx HealthCare Solutions | North America, Europe | Mar 2025: Deployed IoT monitoring across 40,000 shipments |

| UPS Healthcare | USA | Leader | UPS Temperature True | North America, Asia Pacific | Dec 2024: Acquired Bomi Group for EUR 350M |

| Marken Ltd. | USA | Leader | Cell and Gene Therapy Logistics | Global | Jun 2025: Expanded cryogenic depot network to 60 facilities |

| World Courier | USA | Challenger | Specialty Pharma Logistics | Global | Apr 2025: Launched autonomous temperature monitoring system |

| AmerisourceBergen | USA | Challenger | Cold Chain Distribution | North America | Sep 2025: Invested USD 120M in automated cold storage |

| McKesson Corporation | USA | Challenger | Specialty Biologics Distribution | North America | Feb 2025: Partnered with 3 biosimilar manufacturers |

| Cryoport Inc. | USA | Niche Player | Cryogenic Logistics Platform | North America, Europe | Nov 2024: Integrated AI-based logistics optimization |

| Kuehne + Nagel | Switzerland | Challenger | KN PharmaChain | Europe, Asia Pacific | Aug 2025: Opened pharma-dedicated hub in Singapore |

| DB Schenker | Germany | Challenger | Schenker Healthcare Logistics | Europe | Oct 2025: Achieved GDP certification across 25 countries |

By Service Type

Transportation services dominate the pharma cold chain logistics market with 45.2% share valued at USD 8.32 Billion in 2025. This segment encompasses temperature-controlled trucking, refrigerated air cargo, ocean reefer containers, and specialized last-mile delivery vehicles. Growth is propelled by pharmaceutical globalization requiring multi-modal cold chain capabilities across continents. Air freight remains the premium channel for time-sensitive biologics, representing 62% of transportation segment revenue despite constituting only 18% of shipment volume. Ground transportation handles the majority of domestic distribution with dedicated pharmaceutical vehicle fleets featuring real-time GPS tracking and continuous temperature monitoring. The segment is projected to grow at 10.2% CAGR through 2034 as geographic reach expands and temperature requirements tighten.

Storage and warehousing services account for 32.6% market share representing USD 6.00 Billion in 2025. Temperature-controlled warehouse facilities provide ambient, refrigerated, frozen, and cryogenic storage options across pharmaceutical distribution networks. Inventory management systems integrated with enterprise resource planning platforms enable real-time stock visibility and regulatory lot tracking. The expansion of biopharmaceutical manufacturing in Asia has driven warehouse investment in Singapore, China, and India as regional distribution hubs. Automated storage and retrieval systems have gained adoption in large facilities, improving picking accuracy and reducing temperature exposure during order fulfillment. Cold storage capacity constraints in certain markets command premium warehouse rates.

Packaging solutions hold 15.8% share at USD 2.91 Billion in 2025. Temperature-controlled packaging ranges from simple insulated shippers with gel packs to sophisticated active containers with compressor-based refrigeration units. Passive packaging using phase-change materials provides 48 to 120 hour temperature maintenance for most pharmaceutical shipments. Active containers enable longer duration shipping for high-value biologics requiring precise temperature control. Sustainable packaging alternatives have gained traction as pharmaceutical companies pursue environmental commitments, with reusable container programs reducing packaging waste by 40% compared to single-use systems.

Monitoring and tracking services represent 6.4% market share valued at USD 1.18 Billion in 2025. Real-time IoT sensors provide continuous temperature, humidity, and location data throughout pharmaceutical shipments. Cloud-based platforms aggregate sensor data enabling exception-based management and regulatory documentation. Blockchain technology has emerged for immutable chain-of-custody records meeting track-and-trace requirements. The segment experiences rapid growth at 14.8% CAGR as regulatory requirements intensify and technology costs decline, with monitoring increasingly bundled into transportation and storage service offerings.

By Product Category

Biopharmaceuticals and biologics command the largest share of pharma cold chain logistics demand at 52.8% representing USD 9.72 Billion in 2025. This category encompasses monoclonal antibodies, therapeutic proteins, fusion proteins, and biosimilars requiring 2 to 8 degree Celsius storage. The concentration reflects pipeline dominance of biologic therapies, with 8 of the top 10 revenue-generating drugs globally classified as biologics. Cold chain requirements extend from manufacturing through patient administration, with specialty pharmacy distribution adding complexity. Growth in biosimilar adoption following patent expirations has expanded biologic distribution volumes while intensifying price competition among logistics providers.

Vaccines account for 24.5% market share at USD 4.51 Billion in 2025. Vaccine cold chain logistics spans routine immunization programs, pandemic preparedness stockpiles, and travel vaccine distribution. Temperature requirements range from 2 to 8 degrees Celsius for most traditional vaccines to minus 70 degrees Celsius for mRNA platforms. Global immunization initiatives coordinated through WHO and UNICEF drive vaccine cold chain investment in developing countries. The expansion of mRNA vaccine applications beyond COVID-19 to respiratory syncytial virus, influenza, and oncology indications sustains ultra-cold logistics demand.

Cell and gene therapies represent 12.2% share valued at USD 2.24 Billion in 2025. These advanced therapies require cryogenic logistics at temperatures below minus 150 degrees Celsius using liquid nitrogen dry shippers or specialized cryogenic containers. Autologous cell therapies add complexity through vein-to-vein logistics connecting patient apheresis collection sites to manufacturing facilities and back to treatment centers. The segment grows at 18.5% CAGR through 2034 as commercial CGT approvals expand beyond oncology into genetic diseases, representing the highest-growth niche in pharma cold chain logistics.

Clinical trial materials hold 10.5% share at USD 1.93 Billion in 2025. Investigational medicinal product distribution requires regulatory-compliant chain of custody documentation and often involves comparator drugs alongside experimental therapies. Direct-to-patient clinical trial logistics has expanded following COVID-19 pandemic adoption of decentralized trial models. Temperature requirements vary widely based on study protocols, necessitating flexible logistics solutions.

By Temperature Range

Refrigerated storage at 2 to 8 degrees Celsius dominates temperature segmentation with 58.4% share valued at USD 10.75 Billion in 2025. This range accommodates the majority of biologic therapies, vaccines, and insulin products. Standard pharmaceutical-grade refrigeration equipment and validated packaging systems readily address this temperature band. Frozen storage at minus 20 degrees Celsius accounts for 22.8% share at USD 4.20 Billion, serving products including certain vaccines, plasma-derived products, and some biologics. Deep frozen and cryogenic storage below minus 40 degrees Celsius represents 18.8% share at USD 3.46 Billion, with this segment growing fastest at 14.2% CAGR driven by mRNA vaccines and cell therapy expansion.

Regional Analysis

North America Pharma Cold Chain Logistics Market

North America dominates the pharma cold chain logistics market with 38.5% share valued at USD 7.08 Billion in 2025. The region benefits from the highest concentration of biopharmaceutical manufacturing globally, with the United States producing approximately 40% of global biologic drugs by value. The United States alone represents USD 6.24 Billion in cold chain logistics spending, driven by FDA Drug Supply Chain Security Act compliance requirements and specialty pharmacy distribution networks. Canada contributes USD 542 Million through its pharmaceutical distribution infrastructure connecting to US markets. Mexico generates USD 298 Million as pharmaceutical manufacturing expands under USMCA trade provisions. The region leads adoption of advanced cold chain technologies including IoT monitoring, blockchain traceability, and autonomous temperature control systems. Cell and gene therapy logistics have concentrated in major biopharmaceutical hubs including Boston, San Francisco, and Philadelphia, creating specialized cryogenic service corridors.

Europe Pharma Cold Chain Logistics Market

Europe holds 28.2% market share representing USD 5.19 Billion in 2025 within pharma cold chain logistics. Germany leads regional demand at USD 1.35 Billion, anchored by pharmaceutical manufacturing concentration and GDP-compliant distribution networks. The United Kingdom maintains a strong position at USD 892 Million following post-Brexit establishment of independent regulatory frameworks. France generates USD 786 Million through its extensive hospital pharmacy distribution system. Switzerland contributes disproportionately at USD 624 Million relative to population, reflecting the concentration of biopharmaceutical headquarters and manufacturing. European Medicines Agency Good Distribution Practice guidelines establish the most stringent cold chain documentation requirements globally, driving quality investment across the region. The EU Falsified Medicines Directive serialization mandate extends temperature monitoring requirements. Cross-border pharmaceutical distribution within the European Union benefits from harmonized regulatory standards, while Brexit has created complexity for UK-EU pharmaceutical flows.

Asia Pacific Pharma Cold Chain Logistics Market

Asia Pacific represents the fastest-growing region at 12.2% CAGR, holding 22.8% market share valued at USD 4.20 Billion in 2025 for pharma cold chain logistics. China dominates regional activity at USD 1.68 Billion, driven by domestic biopharmaceutical manufacturing expansion and NMPA regulatory modernization. Japan contributes USD 1.12 Billion through sophisticated pharmaceutical distribution networks serving its aging population with high biologic drug consumption. India generates USD 724 Million as vaccine manufacturing hub supplying global immunization programs and expanding domestic biopharmaceutical production. South Korea adds USD 412 Million through its growing biosimilar manufacturing and distribution capabilities. Cold chain infrastructure development remains uneven across the region, with advanced networks in Japan, South Korea, and Singapore contrasting with developing capabilities in Southeast Asia and India. Chinese pharmaceutical cold chain investment has accelerated 28% annually since 2022 following regulatory reforms enabling accelerated drug approvals.

Latin America Pharma Cold Chain Logistics Market

Latin America accounts for 6.5% market share valued at USD 1.20 Billion in 2025 within pharma cold chain logistics. Brazil leads regional demand at USD 524 Million through extensive public health system pharmaceutical distribution. Mexico contributes USD 298 Million as pharmaceutical manufacturing destination serving North and Latin American markets. Argentina maintains clinical research activity and specialty drug distribution generating USD 168 Million. Chile and Colombia emerge as secondary hubs with combined USD 124 Million contribution. Regional cold chain infrastructure faces challenges including power reliability concerns, limited cryogenic capabilities, and fragmented last-mile distribution networks. Pan American Health Organization vaccine procurement programs drive cold chain investment for immunization distribution across the region. The segment grows at 10.8% CAGR through 2034 as biosimilar access expands and specialty pharmacy networks develop.

Middle East and Africa Pharma Cold Chain Logistics Market

Middle East and Africa represent 4.0% market share valued at USD 736 Million in 2025 for pharma cold chain logistics. The United Arab Emirates serves as regional logistics hub at USD 198 Million, leveraging Dubai's position as global air cargo transit point with pharmaceutical-grade cold chain facilities. Saudi Arabia generates USD 172 Million through Vision 2030 healthcare infrastructure investments and domestic pharmaceutical manufacturing expansion. South Africa anchors Sub-Saharan African activity at USD 186 Million, providing access to the African continent's largest pharmaceutical market. Israel contributes through advanced biopharmaceutical capabilities at USD 98 Million. Regional cold chain development focuses on vaccine distribution infrastructure supporting expanded immunization programs coordinated through WHO and GAVI initiatives. Cold chain gaps in Sub-Saharan Africa present significant infrastructure development opportunities as pharmaceutical access improves. The region grows at 11.5% CAGR through 2034, the second-fastest rate globally after Asia Pacific.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Transportation Services

- Storage and Warehousing Services

- Packaging Solutions

- Monitoring and Tracking Services

By Product Category

- Biopharmaceuticals and Biologics

- Vaccines

- Cell and Gene Therapies

- Clinical Trial Materials

By Temperature Range

- Refrigerated (2 to 8 Degrees Celsius)

- Frozen (Minus 20 Degrees Celsius)

- Deep Frozen and Cryogenic (Below Minus 40 Degrees Celsius)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 18.40 B |

| Forecast Revenue (2034) | USD 42.80 B |

| CAGR (2025-2034) | 9.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Transportation Services, Storage and Warehousing Services, Packaging Solutions, Monitoring and Tracking Services), By Product Category, (Biopharmaceuticals and Biologics, Vaccines, Cell and Gene Therapies, Clinical Trial Materials), By Temperature Range, (Refrigerated (2 to 8 Degrees Celsius), Frozen (Minus 20 Degrees Celsius), Deep Frozen and Cryogenic (Below Minus 40 Degrees Celsius)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | DHL SUPPLY CHAIN, FEDEX CUSTOM CRITICAL, UPS HEALTHCARE, MARKEN LTD., WORLD COURIER, AMERISOURCEBERGEN, MCKESSON CORPORATION, CRYOPORT INC., KUEHNE + NAGEL, DB SCHENKER, CARDINAL HEALTH, BIOCAIR, QUICK INTERNATIONAL COURIER, ENVIROTAINER, CSA GROUP, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Product Category (Biopharmaceuticals, Vaccines, Cell & Gene Therapies, Clinical Trial Materials), By Temperature Range (Refrigerated, Frozen, Cryogenic) Industry Trends, Supply Chain Insights, Competitive Landscape & Forecast 2026–2034")

, By Product Category (Biopharmaceuticals, Vaccines, Cell & Gene Therapies, Clinical Trial Materials), By Temperature Range (Refrigerated, Frozen, Cryogenic) Industry Trends, Supply Chain Insights, Competitive Landscape & Forecast 2026–2034")

, By Product Category (Biopharmaceuticals, Vaccines, Cell & Gene Therapies, Clinical Trial Materials), By Temperature Range (Refrigerated, Frozen, Cryogenic) Industry Trends, Supply Chain Insights, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Pharma Cold Chain Logistics Market?

Global Pharma cold chain logistics market valued at USD 16.74B in 2024, reaching USD 42.8B by 2034, growing at a CAGR of 9.9% from 2026–2034.

Who are the major players in the Pharma Cold Chain Logistics Market?

DHL SUPPLY CHAIN, FEDEX CUSTOM CRITICAL, UPS HEALTHCARE, MARKEN LTD., WORLD COURIER, AMERISOURCEBERGEN, MCKESSON CORPORATION, CRYOPORT INC., KUEHNE + NAGEL, DB SCHENKER, CARDINAL HEALTH, BIOCAIR, QUICK INTERNATIONAL COURIER, ENVIROTAINER, CSA GROUP, OTHERS

Which segments covered the Pharma Cold Chain Logistics Market?

By Service Type, (Transportation Services, Storage and Warehousing Services, Packaging Solutions, Monitoring and Tracking Services), By Product Category, (Biopharmaceuticals and Biologics, Vaccines, Cell and Gene Therapies, Clinical Trial Materials), By Temperature Range, (Refrigerated (2 to 8 Degrees Celsius), Frozen (Minus 20 Degrees Celsius), Deep Frozen and Cryogenic (Below Minus 40 Degrees Celsius))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharma Cold Chain Logistics Market

Published Date : 16 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date