- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharma Water Treatment Market Size & Forecast | CAGR 8.7%

Global Pharma Grade Water Treatment System Market Size, Share, Growth & Industry Analysis By System Type (WFI Generation Systems, Purified Water Systems, Pure Steam Generators, Pre-Treatment & Distribution), By Technology (Membrane RO/NF/UF, Thermal Distillation MED & VC, EDI, UV & Ozone), By End User (Biopharma, Pharma, CDMOs, Labs) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 4.2 Billion | USD 8.9 Billion | 8.7% | North America, 36.4% |

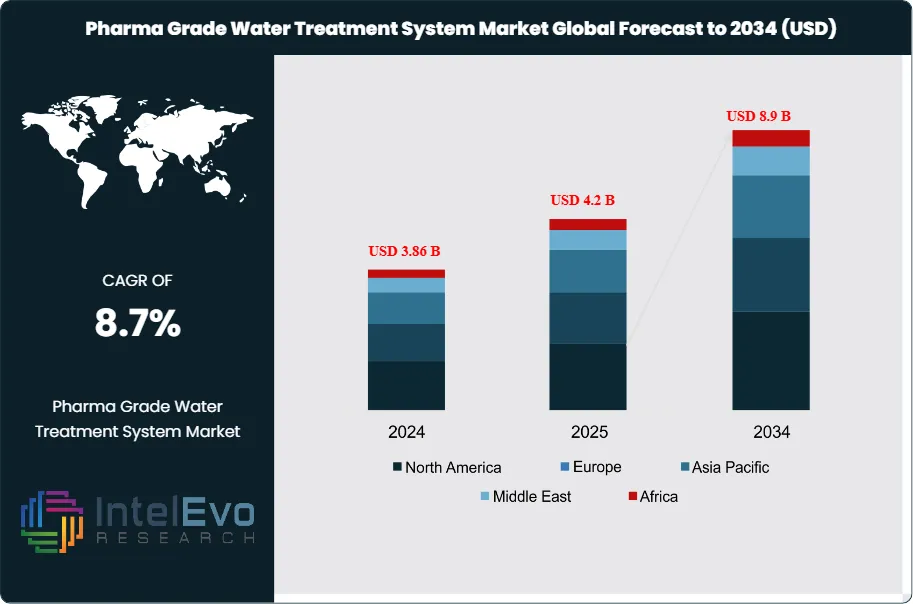

The Pharma Grade Water Treatment System Market was valued at approximately USD 3.86 Billion in 2024 and reached USD 4.2 Billion in 2025. The market is projected to grow to USD 8.9 Billion by 2034, expanding at a CAGR of 8.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.7 Billion over the analysis period. Pharma grade water treatment systems encompass the full spectrum of purification equipment required to produce Purified Water (PW), Highly Purified Water (HPW), and Water for Injection (WFI) in compliance with United States Pharmacopeia (USP), European Pharmacopoeia (Ph. Eur.), and Japanese Pharmacopoeia (JP) monographs. These systems integrate reverse osmosis, electrodeionization, ultrafiltration, UV oxidation, distillation, and ozone sanitation into validated process trains that meet cGMP standards enforced by the U.S. FDA, EMA, and PMDA.

The pharma grade water treatment system market is expanding because of three structural forces. First, global biologic drug revenue surpassed USD 480 Billion in 2025, and biologics manufacturing consumes 3–5 times more WFI per batch than traditional small-molecule production. Second, the 2017 revision to Ph. Eur. Monograph 0169 that permitted membrane-based WFI generation (non-distillation methods) continues to drive capital replacement cycles, with an estimated 38% of European pharmaceutical plants having upgraded to membrane-based WFI by 2025. Third, regulatory enforcement intensity is rising; FDA issued 127 Form 483 observations related to water system deficiencies across inspected facilities in fiscal year 2024, a 14% increase over 2022.

Get More Information about this report -

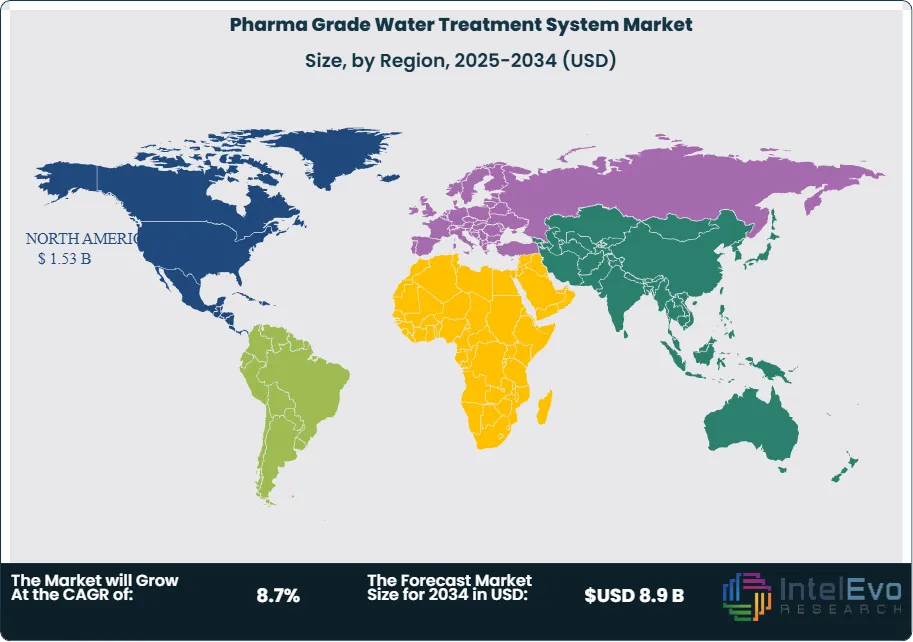

Request Free Sample ReportNorth America commanded 36.4% of global pharma grade water treatment system revenue in 2025 at USD 1.53 Billion, driven by concentrated biopharmaceutical manufacturing in the U.S. Northeast corridor and Gulf Coast biologics expansion. Europe accounted for 28.6% (USD 1.20 Billion), with significant investment in CDMO water infrastructure in Ireland, Switzerland, and Germany. Asia Pacific captured 24.3% (USD 1.02 Billion), fueled by vaccine production scale-up in India and cell therapy facility construction in China, Japan, and South Korea. Digital transformation is accelerating across the market; approximately 42% of new pharma water system installations in 2025 included IoT-connected sensors for real-time conductivity, total organic carbon (TOC), and microbial monitoring. AI-driven predictive maintenance platforms reduced unplanned downtime by 30–35% at early-adopter facilities, creating measurable return on investment that is broadening adoption. The pharma grade water treatment system market serves a regulated, non-discretionary demand base where compliance failure carries severe financial and reputational consequences, making it structurally resilient to macroeconomic cycles.

, By Technology (Membrane RO/NF/UF, Thermal Distillation MED & VC, EDI, UV & Ozone), By End User (Biopharma, Pharma, CDMOs, Labs) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The pharma grade water treatment system market was valued at USD 4.2 Billion in 2025 and is projected to reach USD 8.9 Billion by 2034, expanding at a CAGR of 8.7% over the nine-year forecast period.

- Segment Dominance (By System Type): Water for Injection (WFI) generation systems held the largest share at 38.7% of global revenue in 2025, reflecting the high capital intensity and stringent validation requirements of WFI production equipment.

- Segment Dominance (By End User): Biopharmaceutical manufacturers represented 44.2% of pharma grade water treatment system demand in 2025, driven by biologics production volumes that require significantly higher WFI consumption per batch.

- Driver: The global biologics pipeline expanded to over 8,400 active clinical programs in 2025, driving a 12% year-over-year increase in new GMP water system procurement for biologics manufacturing suites.

- Restraint: Validation complexity and extended commissioning timelines (12–18 months for large WFI loops) constrain rapid deployment; validation costs represent 15–20% of total installed system cost.

- Opportunity: Membrane-based WFI generation in Asia Pacific and Latin America represents a USD 1.4 Billion incremental revenue opportunity by 2034 as regulators in India, China, and Brazil align pharmacopeial standards with Ph. Eur. allowances.

- Trend: IoT-enabled water quality monitoring penetration reached 42% of new system installations in 2025, up from 18% in 2021, reducing unplanned downtime by 30–35% at adopter facilities.

- Regional Analysis: North America led the pharma grade water treatment system market with a 36.4% share valued at USD 1.53 Billion in 2025, anchored by concentrated U.S. biopharmaceutical manufacturing and FDA compliance requirements.

Competitive Landscape Overview

The pharma grade water treatment system market is moderately consolidated, with the top four players; Veolia Water Technologies, Evoqua (Xylem), SUEZ Water Technologies, and Pall Corporation (Danaher); commanding an estimated 47% of global revenue in 2025. Competition centers on validated system design expertise, regulatory compliance track record, and aftermarket service contract breadth. M&A activity accelerated through 2024–2025 as industrial water conglomerates acquired specialty pharma water businesses to access higher-margin, compliance-driven segments. Regional challengers in India (Thermax) and Asia Pacific (Organo Corporation) gained share through cost-competitive offerings tailored to emerging-market GMP standards.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product/Solution | Geo Strength | Recent Strategic Move (2024–2026) |

| Veolia Water Technologies | France | Leader | AQUAVISTA Digital Water Platform | Europe | Acquired Elga LabWater pharma division to expand PW/WFI portfolio, Mar 2025 |

| Evoqua Water Technologies (Xylem) | United States | Leader | Vantage M-Series USP Purification | North America | Launched IoT-enabled predictive maintenance module for pharma WFI systems, Jun 2025 |

| SUEZ Water Technologies (Veolia Group) | France | Leader | Orion Pharma-Grade RO Systems | Europe | Deployed membrane-based WFI generation at three new EU CDMO sites, Jan 2025 |

| Pall Corporation (Danaher) | United States | Leader | Cascada Bioprocessing Water Platform | North America | Introduced single-use WFI point-of-use filtration cartridge for cell therapy labs, Sep 2025 |

| MECO (a Grundfos company) | United States | Challenger | MASTERfit Vapor Compression Distillation | North America | Commissioned 120 m3/hr vapor compression unit for a Texas biologics facility, Apr 2025 |

| BWT Pharma & Biotech | Austria | Challenger | Osmotron WFI Generation Systems | Europe | Expanded Asian sales network with new Singapore service center, Dec 2024 |

| Merck KGaA (MilliporeSigma) | Germany | Challenger | Milli-Q IQ 7000 Lab Water System | Europe | Released validated TOC monitoring upgrade for USP <643> compliance, Feb 2025 |

| Mar Cor Purification (Cantel Medical) | United States | Niche Player | PuriTech Pharma Water Skids | North America | Signed 5-year service contract with top-5 U.S. CDMO for WFI loop management, Jul 2025 |

| Thermax Limited | India | Niche Player | PUREMAX Pharma Water Solutions | Asia Pacific | Won INR 450 Cr order from Indian vaccine manufacturer for new PW facility, May 2025 |

| Spirax Sarco (Spirax Group) | United Kingdom | Niche Player | FINN-AQUA Pure Steam Generators | Europe | Launched energy-recovery module reducing pure steam OPEX by 22%, Nov 2025 |

By System Type.

Water for Injection (WFI) generation systems led the pharma grade water treatment system market in 2025, capturing 38.7% of total revenue at approximately USD 1.63 Billion. WFI systems carry the highest capital cost per unit due to multi-effect distillation or validated hot-water-sanitizable membrane trains, along with extensive distribution loop piping in electropolished 316L stainless steel. The average installed cost for a 10 m3/hr WFI system at a biologics facility ranged from USD 2.8 Million to USD 4.5 Million in 2025, depending on configuration complexity and loop length. Demand is driven by biologic drug manufacturing, where WFI serves as the final rinse agent, formulation vehicle, and CIP (clean-in-place) medium.

Purified Water (PW) generation systems held 31.4% of market share at USD 1.32 Billion in 2025. PW systems serve as the primary utility water for solid-dose manufacturing, cleaning operations, and API synthesis. These systems typically combine multimedia filtration, water softening, reverse osmosis (RO), and electrodeionization (EDI) in modular skid configurations. Pure Steam generators accounted for 16.8% of revenue (USD 0.71 Billion), supplying sterilization-grade steam to autoclaves, SIP (sterilize-in-place) circuits, and lyophilizer chambers. Pre-treatment and distribution systems comprised the remaining 13.1% (USD 0.55 Billion), covering raw water conditioning, storage tanks, UV disinfection units, and recirculation loop components.

By Technology.

Membrane-based systems (reverse osmosis, nanofiltration, ultrafiltration) represented 43.5% of market revenue at USD 1.83 Billion in 2025. The Ph. Eur. revision permitting membrane-based WFI generation accelerated adoption in Europe, and U.S. manufacturers increasingly specify membrane systems for new greenfield facilities due to 25–40% lower energy consumption compared to multi-effect distillation. Thermal distillation systems (multi-effect distillation and vapor compression) held 28.6% at USD 1.20 Billion, retaining dominance in legacy installations and in markets such as Japan where pharmacopeial preference for distillation persists. Electrodeionization (EDI) modules captured 15.2% (USD 0.64 Billion), functioning as polishing stages downstream of RO to achieve conductivity below 0.1 µS/cm. UV and ozone treatment systems comprised 12.7% (USD 0.53 Billion), serving sanitation and TOC reduction functions within distribution loops.

By End User.

Biopharmaceutical manufacturers represented 44.2% of pharma grade water treatment system demand in 2025 at USD 1.86 Billion. Biologics production requires significantly greater WFI volumes than small-molecule synthesis; a typical monoclonal antibody batch consumes 50,000–80,000 liters of WFI across upstream media preparation, downstream chromatography buffer dilution, and final formulation. The cell and gene therapy sub-segment within biologics is the fastest-growing water system buyer, with over 120 new cGMP suites commissioned globally in 2025 alone. Traditional pharmaceutical (small-molecule) manufacturers accounted for 30.1% (USD 1.26 Billion), primarily consuming PW and pure steam for oral solid dose and injectable drug production. CDMOs captured 16.5% (USD 0.69 Billion), driven by multi-product facility expansions requiring flexible, multi-train water systems validated for rapid changeover. Academic, research, and quality control laboratories represented 9.2% (USD 0.39 Billion), purchasing bench-scale and semi-centralized purification units for analytical and R&D applications.

By Service Model.

Equipment sales (CAPEX) dominated the market at 58.4% of revenue (USD 2.45 Billion) in 2025, reflecting the capital-intensive nature of validated pharma water installations. New system procurement cycles typically align with facility construction, capacity expansion, or pharmacopeial upgrade mandates. Aftermarket services, parts, and consumables held 28.3% (USD 1.19 Billion), encompassing membrane replacement, resin regeneration, filter cartridge supply, and annual revalidation services. Managed services and outsourced water utility contracts captured 13.3% (USD 0.56 Billion), an emerging model where water treatment vendors own and operate on-site systems under long-term performance-based agreements. This segment grew at 15% year-over-year in 2025 as mid-size pharma companies sought to reduce operational burden and transfer compliance risk to specialist providers.

Regional Analysis

North America.

North America led the pharma grade water treatment system market with 36.4% of global revenue, totaling USD 1.53 Billion in 2025. The United States accounted for approximately 89% of regional demand, driven by concentrated biopharmaceutical manufacturing clusters in Massachusetts, New Jersey, North Carolina's Research Triangle, and emerging biologics corridors in Texas and Maryland. FDA enforcement rigor remained the primary compliance catalyst; 127 water-system-related Form 483 observations were issued in fiscal year 2024, prompting facility-wide remediation investments averaging USD 1.5–3.0 Million per occurrence. The Inflation Reduction Act and CHIPS Act indirectly stimulated pharma water system demand by encouraging domestic manufacturing reshoring, with over USD 45 Billion in announced U.S. biomanufacturing capital expenditure between 2022 and 2025. Canada contributed approximately USD 95 Million, led by biologics facility investments in Ontario and Quebec. Mexico's pharmaceutical manufacturing sector, concentrated in Guadalajara and Mexico City, generated USD 70 Million in pharma water system demand in 2025, primarily for oral solid dose and vaccine fill-finish operations.

Europe.

Europe captured 28.6% of global pharma grade water treatment system revenue at USD 1.20 Billion in 2025. Germany held the largest national share at 22% of regional revenue, supported by its dense pharmaceutical manufacturing base including facilities operated by Bayer, Boehringer Ingelheim, and Merck KGaA. Ireland represented the fastest-growing European market for pharma water systems, absorbing approximately USD 140 Million in 2025 as multinational biopharmaceutical companies expanded CDMO and drug substance production in Cork and Dublin. Switzerland generated USD 110 Million, anchored by Roche, Novartis, and Lonza biologics operations in Basel and Visp. The United Kingdom invested approximately USD 105 Million, with the Cell and Gene Therapy Catapult driving specialized WFI installations at advanced therapy manufacturing centers. The Ph. Eur. Monograph 0169 revision continued to drive capital equipment replacement; an estimated 62% of European pharma water systems installed before 2017 remained based on thermal distillation, representing a substantial upgrade pipeline for membrane-based WFI suppliers. The EU GMP Annex 1 revision (effective August 2023) tightened requirements for microbiological monitoring and contamination control in sterile manufacturing, further increasing demand for validated water distribution systems with continuous bioburden monitoring.

Asia Pacific.

Asia Pacific held 24.3% of the pharma grade water treatment system market at USD 1.02 Billion in 2025. China led the region with approximately USD 380 Million in system revenue, driven by rapid expansion of biologic drug manufacturing capacity in Shanghai Zhangjiang, Suzhou BioBay, and Wuhan Optics Valley industrial parks. The NMPA's increasing alignment with ICH guidelines raised water quality compliance expectations at Chinese API and finished dose manufacturers, triggering widespread system upgrades. India generated USD 260 Million, supported by the country's position as the world's largest vaccine producer and a major generic API exporter; Serum Institute, Bharat Biotech, and Biological E collectively commissioned new WFI systems totaling over 200 m3/hr combined capacity in 2025. Japan contributed USD 190 Million, maintaining preference for multi-effect distillation systems aligned with JP pharmacopeial tradition. South Korea invested approximately USD 115 Million, concentrated in Samsung Biologics' Songdo campus and Celltrion's Incheon biologics complex, where WFI demand scaled with expanded monoclonal antibody and biosimilar production capacity.

Latin America.

Latin America represented 6.2% of global pharma grade water treatment system revenue at USD 0.26 Billion in 2025. Brazil dominated the region with approximately USD 130 Million, supported by Fiocruz and Butantan Institute vaccine manufacturing operations and private-sector generics expansions by EMS and Eurofarma. ANVISA's harmonization with PIC/S (Pharmaceutical Inspection Co-operation Scheme) standards raised compliance requirements for water system validation, driving replacement of legacy equipment at an estimated 45% of Brazilian pharma plants. Mexico accounted for USD 70 Million across pharmaceutical and medical device water system installations, with Guadalajara, Monterrey, and Mexico City serving as primary manufacturing hubs. Argentina contributed approximately USD 35 Million, with ANMAT regulatory updates prompting water system upgrades at state-owned and private pharmaceutical facilities. The region's growth is constrained by currency volatility and capital access limitations, but CDMO expansion and biosimilar production ambitions are creating new demand pockets through 2034.

Middle East & Africa.

The Middle East & Africa captured 4.5% of the pharma grade water treatment system market at USD 0.19 Billion in 2025. The UAE led regional demand at approximately USD 55 Million, driven by Abu Dhabi's pharmaceutical manufacturing zone (KIZAD) and Dubai's healthcare free zones that attracted GMP-compliant production facilities. Saudi Arabia generated USD 50 Million, supported by NUPCO's (National Unified Procurement Company) localization mandates under Vision 2030 that require 40% of pharmaceutical products consumed domestically to be manufactured locally by 2030. South Africa accounted for USD 40 Million, with Aspen Pharmacare and Biovac Institute water system investments linked to vaccine and injectable drug manufacturing. The region faces unique water treatment challenges due to high ambient temperatures (exceeding 45°C in Gulf states), elevated feed water TDS (total dissolved solids) levels, and intermittent raw water supply quality, all of which increase system design complexity and operating costs. Despite these constraints, the region's pharmaceutical manufacturing localization push is generating sustained investment in validated water infrastructure.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By System Type

- Water for Injection (WFI) Generation Systems

- Purified Water (PW) Generation Systems

- Pure Steam Generators

- Pre-Treatment and Distribution Systems

By Technology

- Membrane-Based Systems (RO, NF, UF)

- Thermal Distillation Systems (MED, Vapor Compression)

- Electrodeionization (EDI) Modules

- UV and Ozone Treatment Systems

By End User

- Biopharmaceutical Manufacturers

- Traditional Pharmaceutical (Small-Molecule) Manufacturers

- Contract Development and Manufacturing Organizations (CDMOs)

- Academic, Research, and QC Laboratories

By Service Model

- Equipment Sales (CAPEX)

- Aftermarket Services, Parts, and Consumables

- Managed Services and Outsourced Water Utility Contracts

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.2 B |

| Forecast Revenue (2034) | USD 8.9 B |

| CAGR (2025-2034) | 8.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By System Type, (Water for Injection (WFI) Generation Systems, Purified Water (PW) Generation Systems, Pure Steam Generators, Pre-Treatment and Distribution Systems), By Technology, (Membrane-Based Systems (RO, NF, UF), Thermal Distillation Systems (MED, Vapor Compression), Electrodeionization (EDI) Modules, UV and Ozone Treatment Systems), By End User, (Biopharmaceutical Manufacturers, Traditional Pharmaceutical (Small-Molecule) Manufacturers, Contract Development and Manufacturing Organizations (CDMOs), Academic, Research, and QC Laboratories), By Service Model, (Equipment Sales (CAPEX), Aftermarket Services, Parts, and Consumables, Managed Services and Outsourced Water Utility Contracts) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | VEOLIA WATER TECHNOLOGIES, EVOQUA WATER TECHNOLOGIES (XYLEM), SUEZ WATER TECHNOLOGIES (VEOLIA GROUP), PALL CORPORATION (DANAHER), MECO (GRUNDFOS), BWT PHARMA & BIOTECH, MERCK KGAA (MILLIPORESIGMA), MAR COR PURIFICATION (CANTEL MEDICAL), THERMAX LIMITED, SPIRAX SARCO (SPIRAX GROUP), ORGANO CORPORATION, AQUA-CHEM INC., STILMAS S.P.A., BRAM-COR S.P.A., SYNTEGON TECHNOLOGY, CHRIST WATER TECHNOLOGY (BWT GROUP), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Membrane RO/NF/UF, Thermal Distillation MED & VC, EDI, UV & Ozone), By End User (Biopharma, Pharma, CDMOs, Labs) Industry Trends & Forecast 2026–2034")

, By Technology (Membrane RO/NF/UF, Thermal Distillation MED & VC, EDI, UV & Ozone), By End User (Biopharma, Pharma, CDMOs, Labs) Industry Trends & Forecast 2026–2034")

, By Technology (Membrane RO/NF/UF, Thermal Distillation MED & VC, EDI, UV & Ozone), By End User (Biopharma, Pharma, CDMOs, Labs) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Pharma Grade Water Treatment System Market?

Global Pharma water treatment market valued at USD 3.86B in 2024, reaching USD 8.9B by 2034, growing at a CAGR of 8.7% from 2026–2034.

Who are the major players in the Pharma Grade Water Treatment System Market?

VEOLIA WATER TECHNOLOGIES, EVOQUA WATER TECHNOLOGIES (XYLEM), SUEZ WATER TECHNOLOGIES (VEOLIA GROUP), PALL CORPORATION (DANAHER), MECO (GRUNDFOS), BWT PHARMA & BIOTECH, MERCK KGAA (MILLIPORESIGMA), MAR COR PURIFICATION (CANTEL MEDICAL), THERMAX LIMITED, SPIRAX SARCO (SPIRAX GROUP), ORGANO CORPORATION, AQUA-CHEM INC., STILMAS S.P.A., BRAM-COR S.P.A., SYNTEGON TECHNOLOGY, CHRIST WATER TECHNOLOGY (BWT GROUP), OTHERS

Which segments covered the Pharma Grade Water Treatment System Market?

By System Type, (Water for Injection (WFI) Generation Systems, Purified Water (PW) Generation Systems, Pure Steam Generators, Pre-Treatment and Distribution Systems), By Technology, (Membrane-Based Systems (RO, NF, UF), Thermal Distillation Systems (MED, Vapor Compression), Electrodeionization (EDI) Modules, UV and Ozone Treatment Systems), By End User, (Biopharmaceutical Manufacturers, Traditional Pharmaceutical (Small-Molecule) Manufacturers, Contract Development and Manufacturing Organizations (CDMOs), Academic, Research, and QC Laboratories), By Service Model, (Equipment Sales (CAPEX), Aftermarket Services, Parts, and Consumables, Managed Services and Outsourced Water Utility Contracts)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharma Grade Water Treatment System Market

Published Date : 28 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date