- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharma Aseptic Processing Market Size & Forecast | CAGR 10.9%

Global Pharmaceutical Aseptic Processing Market Size, Share, Growth & Industry Analysis By Product Type (Sterile Injectables Vials & Ampoules, Prefilled Syringes, Cartridges, Flexible Bags), By Drug Type (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By Technology (Isolators, RABS, Cleanroom Systems, Monitoring Automation) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 88.46 Billion | USD 223.80 Billion | 10.9% | North America, 40.2% |

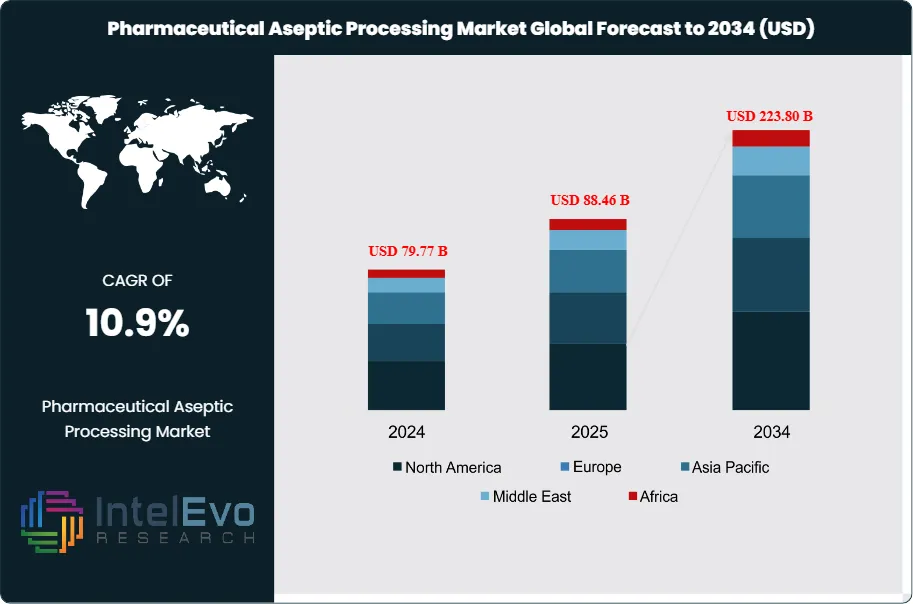

The Pharmaceutical Aseptic Processing Market was valued at approximately USD 79.77 Billion in 2024 and reached USD 88.46 Billion in 2025. The market is projected to grow to USD 223.80 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 135.34 Billion over the analysis period, driven by the sustained commercial expansion of biologics, biosimilars, and sterile injectable drug products, combined with regulatory-driven modernization of aseptic manufacturing infrastructure across all major pharmaceutical markets.

Get More Information about this report -

Request Free Sample ReportPharmaceutical aseptic processing refers to the collection of manufacturing operations conducted under strictly controlled microbiological conditions to produce sterile drug products without terminal sterilization. The process encompasses aseptic formulation, aseptic filling of primary containers including vials, prefilled syringes, cartridges, and ampoules, lyophilization, and finished product inspection. Aseptic processing differs from terminal sterilization in that the drug substance, excipients, and primary containers are sterilized separately before being combined in an ISO Class 5 (Grade A) cleanroom or isolator environment; the final drug product therefore cannot withstand the heat or radiation treatments used in terminal sterilization. This characteristic makes aseptic processing the mandatory production method for thermolabile biologics, recombinant proteins, monoclonal antibodies, mRNA therapeutics, and a wide range of complex parenteral small-molecule drugs.

Demand within the pharmaceutical aseptic processing market is structurally driven by the biologics pipeline. More than 40% of novel FDA drug approvals in 2024 were biologics, and all commercially approved biologic drug products require aseptic processing as their primary manufacturing pathway. The global market for sterile injectable drugs exceeded USD 320 Billion in 2025 and is growing faster than the overall pharmaceutical market, creating proportional demand for aseptic manufacturing infrastructure, services, and equipment. The biosimilar wave — accelerating as originator biologic patents expire — is adding volume demand for aseptic processing capacity at CDMOs and integrated manufacturers, with over 40 biosimilar products approved in the United States by 2025.

Regulatory forces are simultaneously expanding quality expectations and compelling capital investment. The revised EU GMP Annex 1 (effective August 2023) established isolator-based Grade A environments, continuous environmental monitoring, automated container handling, and media fill validation as mandatory elements for sterile drug product manufacturing across the EU. Because most pharmaceutical companies seek simultaneous FDA and EMA market access, Annex 1 functions as a de facto global standard. FDA's current Good Manufacturing Practice enforcement — with sterility-related Form 483 observations and Warning Letters issuing at elevated rates since 2020 — reinforces the imperative for aseptic processing infrastructure investment among US-based manufacturers.

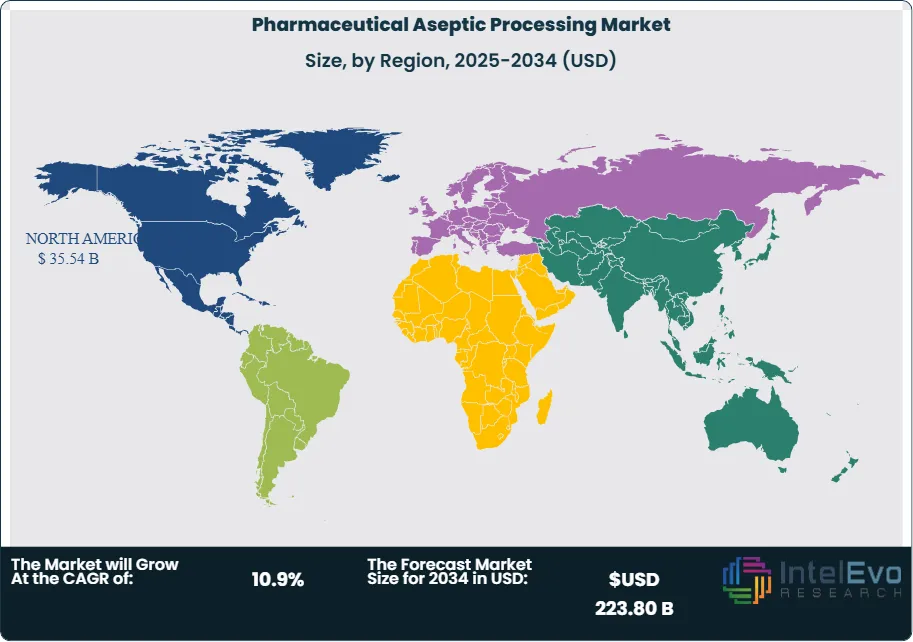

North America leads the pharmaceutical aseptic processing market with a 40.2% share in 2025, generating approximately USD 35.54 Billion in revenue, anchored by the United States' dominant biologics and sterile injectables manufacturing base. Europe holds a 28.6% share, driven by Germany, Ireland, Switzerland, and Italy. Asia Pacific represents 21.8% and is the fastest-growing region, with China, India, and South Korea investing materially in GMP-compliant aseptic manufacturing capacity. The pharmaceutical aseptic processing market across all regions benefits from the structural shift toward CDMO outsourcing and the technology upgrade cycle driven by Annex 1 compliance programs.

, By Drug Type (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By Technology (Isolators, RABS, Cleanroom Systems, Monitoring Automation) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global pharmaceutical aseptic processing market was valued at USD 88.46 Billion in 2025 and is projected to reach USD 223.80 Billion by 2034, expanding at a CAGR of 10.9% over the forecast period 2026–2034.

- Segment Dominance: By product type, sterile injectables (vials and ampoules) account for the largest product segment at approximately 46.8% of pharmaceutical aseptic processing market revenue in 2025, driven by the broad applicability of vial format across biologic, vaccine, and small-molecule parenteral drug products.

- Segment Dominance: By end-user, integrated pharmaceutical and biopharmaceutical manufacturers represent 54.2% of pharmaceutical aseptic processing market revenue in 2025, as large pharma companies operate proprietary aseptic manufacturing capacity for their commercial biologic and injectable drug portfolios.

- Driver: The global sterile injectable drug market exceeded USD 320 Billion in 2025 and is growing at approximately 9.6% annually, directly generating proportional capital expenditure for pharmaceutical aseptic processing infrastructure, equipment, and CDMO services across all major regions.

- Restraint: Cleanroom construction lead times of 2–4 years and the complexity of aseptic process validation — including media fill programs requiring 10,000 or more filled units per qualification run — constrain the speed at which new pharmaceutical aseptic processing capacity can respond to accelerated demand signals.

- Opportunity: The Asia Pacific pharmaceutical aseptic processing market is projected to grow at a 13.6% CAGR through 2034, generating an incremental USD 28.4 Billion in regional revenue above 2025 levels, as China, India, and South Korea build GMP-compliant aseptic infrastructure for export-oriented biologic and biosimilar manufacturing.

- Trend: Isolator-based Grade A aseptic environments are now specified in approximately 68.4% of all new aseptic fill-finish line installations globally in 2025, up from 38.6% in 2018, as EU GMP Annex 1 compliance and FDA aseptic processing guidance converge on isolator technology as the preferred barrier design.

- Regional Analysis: North America leads the global pharmaceutical aseptic processing market with a 40.2% share in 2025, generating approximately USD 35.54 Billion in revenue, driven by the United States' concentration of FDA-regulated biologic manufacturers and the highest density of licensed aseptic CDMO capacity globally.

Competitive Landscape Overview

The pharmaceutical aseptic processing market is fragmented at the service level and moderately consolidated at the equipment supply tier. The top four CDMO operators — Lonza Group, Pfizer CentreOne, Baxter BioPharma Solutions, and Samsung Biologics — collectively hold approximately 18.6% of global aseptic processing service revenue in 2025, while the equipment segment is led by Syntegon Technology, IMA Life, Getinge AB, and Bausch+Stroebel with a combined equipment market share of approximately 44.2%. Competition is technology- and regulatory-capability-driven. M&A activity among CDMOs has accelerated since 2022 as operators seek to add aseptic capacity, container format breadth, and geographic coverage across major regulatory jurisdictions.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Service | Geo Strength | Recent Strategic Move (2024–2026) |

| Lonza Group | Switzerland | Leader | Lonza Drug Product Aseptic Services | Europe / North America | Feb 2025: Added two new isolator-coupled aseptic filling lines at Visp, Switzerland, expanding biologics aseptic fill-finish capacity by an estimated 25 Million vial equivalents per year. |

| Pfizer CentreOne | USA | Leader | Pfizer Aseptic CDMO Services | North America / Europe | Sep 2025: Opened external CDMO aseptic services to third-party pharmaceutical clients at its Kalamazoo and Freiburg sites, adding significant licensed aseptic capacity to the outsourced market. |

| Baxter BioPharma Solutions | USA | Leader | Baxter Aseptic Fill-Finish CDMO | North America / Europe | Apr 2025: Signed a multi-year aseptic fill-finish partnership with a top-10 global pharmaceutical company for pre-filled syringe biologic filling at its Indiana facility. |

| Samsung Biologics | South Korea | Leader | Samsung Aseptic Drug Product Services | Asia Pacific / Global | Jan 2026: Broke ground on Plant 5 in Incheon, South Korea, adding 180,000 L of upstream capacity with integrated aseptic fill-finish capability for commercial biologics. |

| Syntegon Technology | Germany | Challenger | Versynta Aseptic Filling Platform | Europe / Global | Mar 2025: Launched Versynta microBatch for small-lot aseptic filling, targeting clinical-stage and orphan drug markets with rapid changeover and isolator-ready design. |

| IMA Life | Italy | Challenger | IMA Life Integrated Fill-Finish Line | Europe / North America | Jun 2025: Launched a fully integrated lyophilizer-isolator-filling platform engineered for EU GMP Annex 1 compliance, targeting greenfield aseptic facility projects. |

| Getinge AB | Sweden | Challenger | Getinge Barrier Isolator & Sterilization | Europe / North America | Jan 2025: Expanded pharmaceutical isolator and steam sterilizer manufacturing capacity at its German facility by 25% to meet Annex 1 compliance-driven demand. |

| Bausch+Stroebel | Germany | Challenger | VarioSys Flexible Aseptic Filling System | Europe / North America | Nov 2024: Launched the upgraded VarioSys supporting vials, syringes, and cartridges within a single isolator-compatible platform for multi-format CDMO operations. |

| Vetter Pharma | Germany | Niche Player | Vetter Prefilled Syringe Aseptic Services | Europe / North America | Sep 2025: Commissioned new PFS aseptic fill-finish capacity at Ravensburg adding 30 Million syringe units per year for biologic and GLP-1 products. |

| WuXi Biologics | China | Niche Player | WuXi Aseptic Drug Product Services | Asia Pacific / Global | Aug 2025: Opened a new GMP aseptic fill-finish facility in Wuxi with 12 filling lines supporting vials, syringes, and lyophilization for global pharmaceutical clients. |

By Product Type

The pharmaceutical aseptic processing market by product type is led by sterile injectables in vial and ampoule formats, which account for approximately 46.8% of total market revenue in 2025 at USD 41.40 Billion. Vials remain the most versatile primary container for aseptic drug products, accommodating both liquid and lyophilized presentations across biologics, vaccines, oncology agents, and small-molecule parenterals. The broad compatibility of the vial format with diverse drug formulations, combined with established regulatory precedent across FDA, EMA, and WHO frameworks, sustains its leading position within the pharmaceutical aseptic processing market. The vial segment encompasses both glass and polymer primary containers, with integrated lyophilization as a significant sub-process for thermolabile biologic drugs. Prefilled syringe aseptic processing represents 28.4% of market revenue in 2025 at USD 25.12 Billion, reflecting the structural shift toward self-injection drug delivery formats and the extraordinary commercial demand for GLP-1 receptor agonist prefilled auto-injectors. Prefilled syringe aseptic processing is the fastest-growing product type segment within the market at an estimated 13.6% CAGR through 2034, driven by biologic subcutaneous formulation trends and the biosimilar market. Cartridge aseptic processing accounts for 10.6% of market revenue, primarily for insulin pen cartridges and other hormonal therapies. Flexible bag and other specialty container formats account for the remaining 14.2%, including biologics infusion bags and unit-dose ophthalmics.

By Drug Type

By drug type, biologics and biosimilars dominate the pharmaceutical aseptic processing market, accounting for 55.4% of revenue in 2025 at USD 48.99 Billion. This segment encompasses aseptic processing of monoclonal antibodies, recombinant proteins, bispecific antibodies, ADCs, fusion proteins, mRNA therapeutics, GLP-1 receptor agonists, and biosimilars. Every approved biologic drug product requires aseptic processing as its manufacturing pathway, making the biologics category the foundational demand driver for the market. The continued growth of the global biologics pipeline — with over 600 mAb programs in clinical development and the expanding mRNA and ADC modality pipelines — sustains aseptic processing capacity demand at both integrated manufacturer and CDMO levels. Small-molecule sterile injectables represent 28.8% of market revenue in 2025 at USD 25.48 Billion, encompassing chemotherapy agents, antifungals, analgesics, and a broad range of parenteral drug products that require aseptic processing due to aqueous instability or heat sensitivity. Vaccines account for 11.4% of market revenue at USD 10.08 Billion, with global immunization programs and pandemic preparedness stockpiling sustaining demand for vaccine aseptic processing capacity. Cell and gene therapy aseptic processing constitutes the remaining 4.4% of market revenue, a modest current share growing at a projected 18.2% CAGR through 2034.

By Technology

By technology, isolator-based aseptic processing systems represent the leading technology category within the pharmaceutical aseptic processing market at 44.6% of equipment and facility revenue in 2025, valued at USD 39.45 Billion. Pharmaceutical-grade isolators — which provide HEPA-filtered Grade A environments separated from the surrounding cleanroom background by physical barriers and sterilized in-situ with vaporized hydrogen peroxide — have become the reference technology for new and significantly modified aseptic fill-finish lines under EU GMP Annex 1 and FDA aseptic processing guidance. Approximately 68.4% of all new aseptic fill-finish line installations globally in 2025 specify isolator-based Grade A environments, a sharp increase from 38.6% in 2018. Restricted Access Barrier Systems (RABS) account for 22.8% of technology revenue in 2025, representing a significant installed base of aseptic line technology — particularly in North America and Japan — where RABS remains compliant under existing regulatory frameworks for legacy facilities. Open-cleanroom aseptic processing, while declining as a share of new installations, maintains 19.4% of market revenue through its presence in the large installed base of older facilities, and through certain vaccine and large-volume parenteral applications where open systems remain operationally necessary. New cleanroom construction and automation technologies, including continuous environmental monitoring and robotics, account for 13.2% of market revenue across technology segments.

By End-User

By end-user, integrated pharmaceutical and biopharmaceutical manufacturers represent the largest purchaser segment within the pharmaceutical aseptic processing market, generating 54.2% of revenue in 2025 at USD 47.94 Billion. These manufacturers operate proprietary aseptic processing suites for their commercial drug product portfolios and invest capital in GMP modernization programs aligned with FDA and EMA quality system expectations. Large integrated companies including Pfizer, Eli Lilly, AstraZeneca, Roche, Novartis, and Sanofi each operate multiple GMP-certified aseptic manufacturing sites globally, with aggregate capital investment in aseptic infrastructure running into the multi-billion-dollar range over the 2020–2025 period. CDMOs account for 36.4% of pharmaceutical aseptic processing market revenue in 2025 at USD 32.20 Billion, serving the outsourced aseptic manufacturing needs of biotechnology companies, specialty pharma developers, and large pharma groups that choose not to operate all sterile production in-house. Government and public health manufacturing organizations, including national vaccine institutes and defense-related pharmaceutical manufacturing entities, account for approximately 6.8% of market revenue. Research institutions and hospital pharmacies collectively represent the remaining 2.6%.

Regional Analysis

North America Pharmaceutical Aseptic Processing Market

North America holds the leading position in the global pharmaceutical aseptic processing market with a 40.2% share in 2025, generating approximately USD 35.54 Billion in revenue. The United States is the world's largest individual aseptic processing market, anchored by the highest concentration of FDA-approved biologic drug products, the most extensive CDMO aseptic fill-finish infrastructure globally, and the FDA's sustained emphasis on sterility assurance through its GMP enforcement program. FDA Form 483 observations related to aseptic process failures and environmental monitoring deficiencies have been issued at an elevated rate since 2020, compelling manufacturers to invest in modernized aseptic systems including isolator-based fill-finish lines, automated inspection, and continuous environmental monitoring. US pharmaceutical manufacturers including Eli Lilly, Pfizer, Amgen, and Regeneron have collectively invested over USD 10 Billion in aseptic manufacturing capacity between 2020 and 2025, driven by the commercial launches of high-volume biologics, mRNA products, and GLP-1 agonists. The CDMO sector in the United States hosts numerous licensed GMP aseptic fill-finish facilities in New Jersey, Indiana, North Carolina, and Massachusetts, each serving multiple pharmaceutical clients across clinical and commercial supply campaigns. Canada contributes to regional aseptic processing revenue through federal biomanufacturing strategy investments. North America's pharmaceutical aseptic processing market is projected to grow at a 10.2% CAGR through 2034.

Europe Pharmaceutical Aseptic Processing Market

Europe represents 28.6% of the global pharmaceutical aseptic processing market in 2025 at USD 25.30 Billion. Germany, Ireland, Switzerland, and Italy are the primary manufacturing centers, each hosting major aseptic processing operations for global pharmaceutical companies and expanding CDMO sectors. The EU GMP Annex 1 revision (effective August 2023) is the decisive regulatory force driving European aseptic processing investment, mandating isolator-based Grade A environments, continuous environmental monitoring, automated container handling in critical zones, and revised media fill frequency and scale requirements. Industry estimates place cumulative Annex 1 compliance investment in European aseptic manufacturing infrastructure at USD 5.2 Billion between 2023 and 2026. Ireland's position as a hub for US pharmaceutical company European manufacturing has attracted multi-billion-dollar aseptic fill-finish investments in Cork and Dublin. Germany's aseptic processing market is served by domestic pharmaceutical manufacturers including Bayer and Boehringer Ingelheim, as well as a dense concentration of aseptic equipment manufacturers including Syntegon, Bausch+Stroebel, Groninger, and Optima Pharma. Switzerland's biopharma cluster drives demand through commercial biologics fill-finish programs at Lonza, Novartis, and Roche. Europe's pharmaceutical aseptic processing market is expected to grow at a 10.6% CAGR through 2034.

Asia Pacific Pharmaceutical Aseptic Processing Market

Asia Pacific accounts for 21.8% of the global pharmaceutical aseptic processing market in 2025 at USD 19.28 Billion and is the fastest-growing region with a projected CAGR of 13.6% through 2034. China is the largest and fastest-growing national market in the region, where domestic pharmaceutical manufacturers and CDMOs are building GMP-compliant aseptic processing capacity to serve both the domestic biologic market and global pharmaceutical outsourcing clients. NMPA's GMP reforms, progressively aligning with ICH Q10 quality system requirements and EU GMP standards, are compelling Chinese manufacturers to upgrade legacy aseptic facilities — many originally built to lower standards — to international GMP specifications. South Korea's Samsung Biologics is one of the world's largest CDMO operators and is expanding its aseptic fill-finish and upstream bioprocessing capacity through Plant 5 construction in Incheon, targeting commercial biologics manufacturing for global pharmaceutical clients. India's sterile injectables manufacturing sector is growing rapidly under the PLI scheme, with new GMP aseptic facilities under construction across Hyderabad, Ahmedabad, and Bangalore to serve FDA- and EMA-regulated export markets. Japan's pharmaceutical aseptic processing market is mature and well-regulated under PMDA GMP requirements that align with ICH Q standards. The Asia Pacific pharmaceutical aseptic processing market represents the most significant growth opportunity for both equipment suppliers and CDMO service providers through 2034.

Latin America Pharmaceutical Aseptic Processing Market

Latin America holds a 5.8% share of the pharmaceutical aseptic processing market in 2025 at approximately USD 5.13 Billion. Brazil is the dominant regional market, where ANVISA-regulated aseptic manufacturing supports domestic pharmaceutical production and export-oriented generic drug supply. Fiocruz and Instituto Butantan operate aseptic processing capacity for vaccine and biologic drug products serving domestic public health programs, including technology transfer partnerships with international vaccine manufacturers that have included aseptic process technology transfer. Mexico's pharmaceutical manufacturing sector, supplying both domestic and North American markets, includes CDMO operators with GMP aseptic fill-finish capacity oriented toward FDA-regulated export production. Argentina's domestic pharmaceutical industry maintains aseptic processing facilities for the domestic and regional market. The Latin American pharmaceutical aseptic processing market is constrained by the high cost of imported aseptic equipment, limited local availability of GMP-qualified engineering resources for cleanroom construction and validation, and foreign exchange constraints on capital expenditure planning. International CDMO operators are selectively establishing regional aseptic capacity as the biologic and biosimilar market in Latin America grows. The region's pharmaceutical aseptic processing market is projected to grow at a 9.4% CAGR through 2034.

Middle East & Africa Pharmaceutical Aseptic Processing Market

The Middle East and Africa region accounts for 3.6% of global pharmaceutical aseptic processing market revenue in 2025 at approximately USD 3.18 Billion. Saudi Arabia, the UAE, and South Africa are the primary demand centers. GCC national pharmaceutical manufacturing programs under Vision 2030 and equivalent strategies are directing investment into domestic sterile drug production facilities, including aseptic fill-finish capacity for vaccines, biologics, and generic injectables. The SFDA in Saudi Arabia and health regulators in the UAE have adopted GMP standards aligned with WHO and ICH requirements, creating the regulatory foundation for commercial GMP aseptic operations. South Africa's pharmaceutical manufacturing base, the most developed in sub-Saharan Africa, contributes aseptic processing capacity through established injectable drug manufacturers serving domestic and export markets. The African Union's pharmaceutical manufacturing agenda, supported by multilateral development financing, is directing investment toward domestic aseptic capacity in multiple African markets beyond South Africa, including Egypt, Kenya, and Nigeria. Hospital pharmacy aseptic compounding, conducted under national pharmacopoeial standards, contributes a distinct revenue sub-segment across the MEA region. MEA's pharmaceutical aseptic processing market is projected to grow at a 11.4% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Sterile Injectables (Vials & Ampoules)

- Prefilled Syringes

- Cartridges

- Flexible Bags & Specialty Containers

By Drug Type

- Biologics & Biosimilars

- Small-Molecule Sterile Injectables

- Vaccines

- Cell & Gene Therapy Products

By Technology

- Isolator-Based Aseptic Processing

- Restricted Access Barrier Systems (RABS)

- Open Cleanroom Aseptic Processing

- Continuous Environmental Monitoring & Automation

By End-User

- Integrated Pharmaceutical & Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Government & Public Health Manufacturing Organizations

- Research Institutions & Hospital Pharmacies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 88.46 B |

| Forecast Revenue (2034) | USD 223.80 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Sterile Injectables (Vials & Ampoules), Prefilled Syringes, Cartridges, Flexible Bags & Specialty Containers), By Drug Type, (Biologics & Biosimilars, Small-Molecule Sterile Injectables, Vaccines, Cell & Gene Therapy Products), By Technology, (Isolator-Based Aseptic Processing, Restricted Access Barrier Systems (RABS), Open Cleanroom Aseptic Processing, Continuous Environmental Monitoring & Automation), By End-User, (Integrated Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Government & Public Health Manufacturing Organizations, Research Institutions & Hospital Pharmacies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LONZA GROUP, PFIZER CENTREONE, BAXTER BIOPHARMA SOLUTIONS, SAMSUNG BIOLOGICS, SYNTEGON TECHNOLOGY, IMA LIFE, GETINGE AB, BAUSCH+STROEBEL, VETTER PHARMA, WUXI BIOLOGICS (WUXI APPTEC), RECIPHARM, CATALENT, BOEHRINGER INGELHEIM BIOPHARMACEUTICALS, FRESENIUS KABI, HIKMA PHARMACEUTICALS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Drug Type (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By Technology (Isolators, RABS, Cleanroom Systems, Monitoring Automation) Industry Trends & Forecast 2026–2034")

, By Drug Type (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By Technology (Isolators, RABS, Cleanroom Systems, Monitoring Automation) Industry Trends & Forecast 2026–2034")

, By Drug Type (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By Technology (Isolators, RABS, Cleanroom Systems, Monitoring Automation) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Pharmaceutical Aseptic Processing Market?

Global Pharma aseptic processing market valued at USD 79.77B in 2024, reaching USD 223.80B by 2034, growing at a CAGR of 10.9% from 2026–2034.

Who are the major players in the Pharmaceutical Aseptic Processing Market?

LONZA GROUP, PFIZER CENTREONE, BAXTER BIOPHARMA SOLUTIONS, SAMSUNG BIOLOGICS, SYNTEGON TECHNOLOGY, IMA LIFE, GETINGE AB, BAUSCH+STROEBEL, VETTER PHARMA, WUXI BIOLOGICS (WUXI APPTEC), RECIPHARM, CATALENT, BOEHRINGER INGELHEIM BIOPHARMACEUTICALS, FRESENIUS KABI, HIKMA PHARMACEUTICALS, Others

Which segments covered the Pharmaceutical Aseptic Processing Market?

By Product Type, (Sterile Injectables (Vials & Ampoules), Prefilled Syringes, Cartridges, Flexible Bags & Specialty Containers), By Drug Type, (Biologics & Biosimilars, Small-Molecule Sterile Injectables, Vaccines, Cell & Gene Therapy Products), By Technology, (Isolator-Based Aseptic Processing, Restricted Access Barrier Systems (RABS), Open Cleanroom Aseptic Processing, Continuous Environmental Monitoring & Automation), By End-User, (Integrated Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Government & Public Health Manufacturing Organizations, Research Institutions & Hospital Pharmacies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharmaceutical Aseptic Processing Market

Published Date : 05 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date