- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharmaceutical Excipient Market Size, Share & Forecast | CAGR 7.3%

Global Pharmaceutical Excipient Market Size, Share, Growth Analysis By Functionality (Fillers & Diluents, Binders, Disintegrants, Lubricants, Coating Excipients, Solubilizers & Stabilizers), By Route of Administration (Oral Solid Dosage, Parenteral, Topical, Ophthalmic, Transdermal, Inhalation, Oral Liquid & Semi-Solid), By Source, Industry Trends, Regional Outlook, Competitive Landscape, Strategic Insights & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 9.64 Billion | USD 18.26 Billion | 7.3% | Asia Pacific, 36.4% |

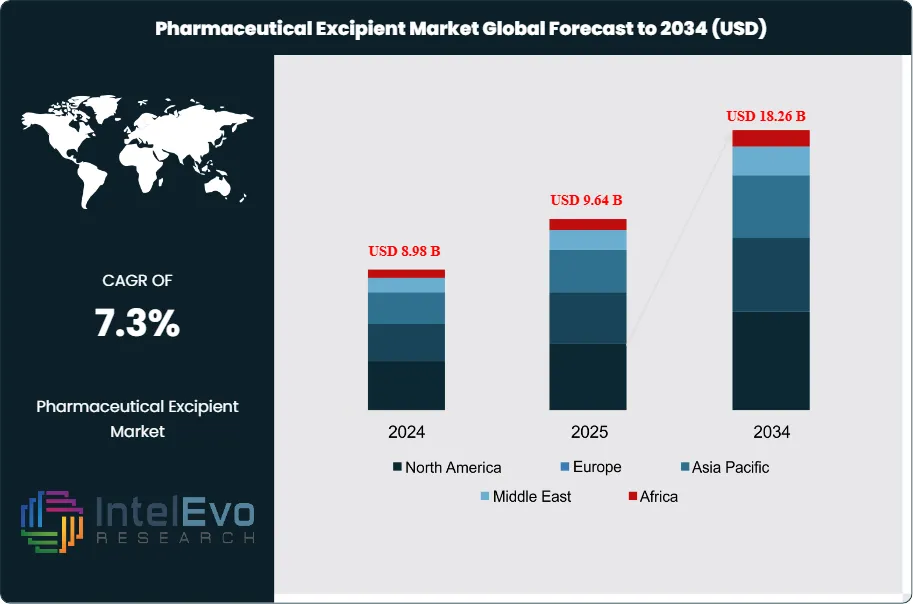

The Pharmaceutical Excipient Market was valued at approximately USD 8.98 Billion in 2024 and reached USD 9.64 Billion in 2025. The market is projected to grow to USD 18.26 Billion by 2034, expanding at a CAGR of 7.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.62 Billion over the analysis period, driven by the accelerating generic drug wave, the commercial expansion of complex drug delivery formulations, the growth of oral solid dosage manufacturing in emerging markets, and the increasing adoption of novel multifunctional excipients for biologic and modified-release drug product development.

Get More Information about this report -

Request Free Sample ReportPharmaceutical excipients are the inactive ingredients present in a drug formulation that serve functional purposes including binding, disintegration, lubrication, solubilization, stabilization, taste masking, viscosity control, and preservative action. While excipients are pharmacologically inert in the traditional sense, their selection and quality have profound effects on drug bioavailability, stability, manufacturability, and patient compliance. Major excipient functional categories include fillers and diluents (microcrystalline cellulose, lactose, dicalcium phosphate), binders (polyvinylpyrrolidone, hydroxypropyl cellulose), disintegrants (croscarmellose sodium, sodium starch glycolate), lubricants (magnesium stearate, stearic acid), coatings (hydroxypropyl methylcellulose, Eudragit polymers), and solubilizers (cyclodextrins, polysorbates).

Demand for pharmaceutical excipients is primarily generated by the oral solid dosage (OSD) drug manufacturing sector, which accounts for approximately 62% of global pharmaceutical production by dosage unit volume. The generic drug industry is the largest single end-user segment of excipient consumption, driven by the wave of branded drug patent expirations that continues through 2030 and beyond. FDA Orange Book data indicates that over 1,500 new ANDA filings are submitted annually in the United States, each requiring validated excipient-API compatibility data and excipient specification documentation meeting USP, NF, EP, and JP pharmacopoeial standards.

Novel excipient development is a key driver of higher-value segment growth within the pharmaceutical excipient market. Multifunctional excipients that combine binding, disintegration, and lubrication functions in a single material are gaining adoption among tablet manufacturers seeking to simplify formulation processes and reduce variable count. Co-processed excipients — physically combined rather than chemically bonded — offer improved flow, compressibility, and direct compression suitability compared to individual component excipients, enabling manufacturers to eliminate wet granulation steps. The biopharmaceutical sector's growing use of lipid-based excipients, cyclodextrins, and polymer-based stabilizers for protein formulation and mRNA lipid nanoparticle (LNP) formulation has created new high-value excipient sub-markets growing at 10–14% annually.

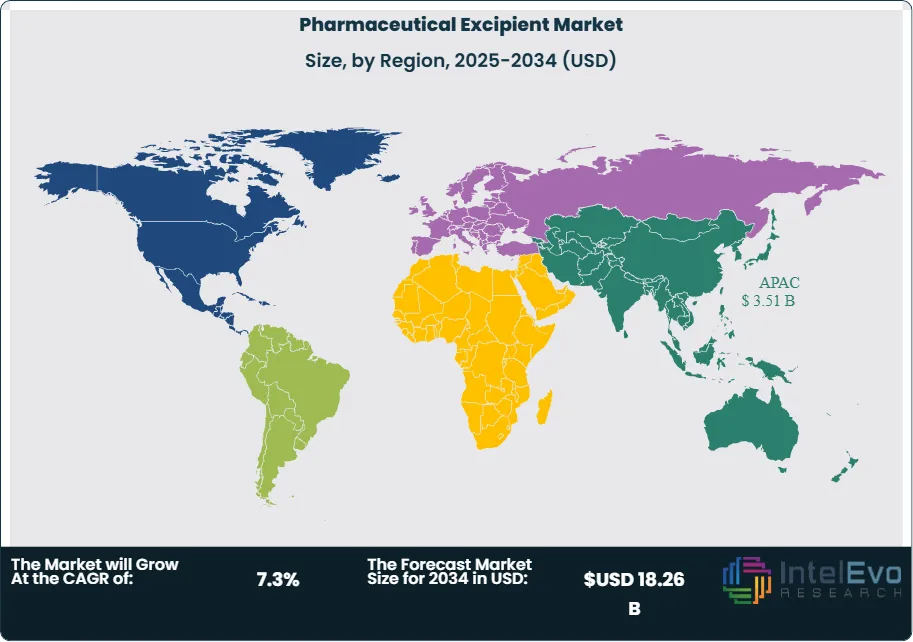

Asia Pacific leads the global pharmaceutical excipient market with a 36.4% share in 2025, generating approximately USD 3.51 Billion, anchored by India and China as the world's largest generic drug manufacturing nations and the primary growth engines of excipient demand. North America is the second-largest region at 27.8%, driven by the United States' substantial OSD and specialty formulation manufacturing base. Europe holds a 22.6% share. The pharmaceutical excipient market across all regions benefits from structural drivers including population growth in emerging markets, healthcare access expansion, and the increasing complexity of modern drug formulations.

, By Route of Administration (Oral Solid Dosage, Parenteral, Topical, Ophthalmic, Transdermal, Inhalation, Oral Liquid & Semi-Solid), By Source, Industry Trends, Regional Outlook, Competitive Landscape, Strategic Insights & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global pharmaceutical excipient market was valued at USD 9.64 Billion in 2025 and is projected to reach USD 18.26 Billion by 2034, expanding at a CAGR of 7.3% over the forecast period 2026–2034.

- Segment Dominance: By functionality, fillers and diluents account for the largest excipient category at approximately 28.4% of pharmaceutical excipient market revenue in 2025, with microcrystalline cellulose (MCC) and lactose monohydrate as the highest-volume individual excipient materials globally.

- Segment Dominance: By route of administration, oral solid dosage (OSD) formulations account for approximately 62.6% of pharmaceutical excipient market revenue in 2025, reflecting the dominance of tablet and capsule manufacturing in both generic and branded pharmaceutical production worldwide.

- Driver: Over 1,500 ANDA filings are submitted annually in the United States, with global generic drug market volume exceeding USD 450 Billion in 2025 — the largest single driver of pharmaceutical excipient demand, as each new generic formulation requires validated excipient selection, compatibility testing, and regulatory documentation.

- Restraint: Pharmacopoeial regulatory complexity — with excipients required to meet simultaneous compliance with USP/NF, EP, JP, and CP monograph specifications for global product registration — adds USD 200,000–500,000 per excipient-product combination in qualification costs, constraining the pace of new excipient adoption and limiting formulation flexibility.

- Opportunity: Lipid-based excipients and polymer excipients for mRNA and LNP drug delivery represent a fast-growing opportunity within the pharmaceutical excipient market, with the global mRNA therapeutics market projected to exceed USD 30 Billion by 2030, each product requiring pharmaceutical-grade ionizable lipids, helper lipids, PEG-lipids, and polymer-based LNP excipients.

- Trend: Co-processed multifunctional excipients are present in approximately 24.6% of new OSD generic formulations filed globally in 2025, up from 11.8% in 2019, as tablet manufacturers adopt direct compression-enabling excipient systems that eliminate wet granulation and reduce manufacturing steps.

- Regional Analysis: Asia Pacific leads the global pharmaceutical excipient market with a 36.4% share in 2025, generating approximately USD 3.51 Billion in revenue, anchored by India and China as the world's dominant generic drug manufacturing markets and largest consumers of bulk excipient volumes.

Competitive Landscape Overview

The pharmaceutical excipient market is moderately fragmented, with the top four suppliers — BASF SE, DowDuPont (IFF Health), Roquette Freres, and Ashland Global Holdings — collectively holding approximately 34.6% of global market revenue in 2025. Competition is primarily product-quality-driven, with differentiation centering on pharmacopoeial compliance breadth, particle engineering capabilities, technical support for formulation development, and supply chain reliability. M&A activity has increased since 2021, with specialty chemical and ingredient companies acquiring pharmaceutical excipient producers to gain access to the high-margin pharmaceutical-grade ingredients market and to build technical service capabilities alongside raw material supply.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| BASF SE | Germany | Leader | Kollidon (PVP) Excipient Range | Europe / Global | Jan 2025: Expanded pharmaceutical-grade Kollidon PVP production capacity at its Ludwigshafen site by 20% to meet growing demand from generic drug manufacturers in Asia Pacific and North America. |

| IFF (International Flavors & Fragrances) | USA | Leader | Avicel PH Microcrystalline Cellulose | North America / Global | Mar 2025: Launched Avicel PH-302 — a new large-particle MCC grade specifically engineered for high-speed direct compression of high-dose tablet formulations with improved compressibility. |

| Roquette Freres | France | Leader | PEARLITOL Mannitol Excipient | Europe / Global | May 2025: Inaugurated a new pharmaceutical excipient production facility in India, adding 30,000 metric tons of capacity for sorbitol, mannitol, and co-processed excipients targeting Indian and Asian generic manufacturers. |

| Ashland Global Holdings | USA | Leader | Klucel HPC Hydroxypropyl Cellulose | North America / Europe | Feb 2026: Launched a new low-substitution HPC grade optimized for disintegrant and binder dual functionality in orally disintegrating tablet (ODT) formulations targeting geriatric and pediatric patient populations. |

| Colorcon | USA | Challenger | Opadry Film Coating System | North America / Global | Sep 2025: Released Opadry EZ — a simplified aqueous film coating system requiring 40% fewer process steps than conventional Opadry, targeting mid-sized generic tablet manufacturers seeking productivity improvements. |

| Lubrizol (Berkshire Hathaway) | USA | Challenger | Carbopol Polymer Excipients | North America / Europe | Apr 2025: Expanded Carbopol pharmaceutical-grade production at its Wickliffe, Ohio facility to address growing demand for controlled-release polymer excipients in modified-release oral solid dosage products. |

| DAICEL Corporation | Japan | Challenger | Celphere Microcrystalline Cellulose Spheres | Asia Pacific / Global | Nov 2024: Launched a new Celphere CP series for multiparticulate pellet coating applications, targeting orally disintegrating and sustained-release dosage forms in Japanese and global pharmaceutical markets. |

| Shin-Etsu Chemical | Japan | Challenger | HPMC Pharmacoat Grade Excipients | Asia Pacific / Europe | Jun 2025: Expanded production of pharmaceutical-grade HPMC (Pharmacoat) at its Niigata plant to serve growing demand for matrix former excipients in extended-release tablet manufacturing. |

| JRS Pharma | Germany | Niche Player | PROSOLV SMCC Co-Processed Excipient | Europe / North America | Jan 2026: Launched PROSOLV SMCC HD90, a high-density silicified MCC grade enabling high-fill weight direct compression tablets for API-dense formulations targeting cardiovascular and diabetes drug products. |

| Signet Chemical Corporation | India | Niche Player | Castor Oil Pharmaceutical Grade | Asia Pacific | Jul 2025: Expanded pharmaceutical-grade castor oil and hydrogenated castor oil production capacity in Gujarat, India, targeting lubricant excipient demand from India's rapidly expanding generic tablet manufacturing sector. |

By Functionality

The pharmaceutical excipient market by functionality is led by fillers and diluents, which account for approximately 28.4% of total market revenue in 2025 at USD 2.74 Billion. Fillers and diluents are the highest-volume excipients by mass in tablet and capsule manufacturing, providing the bulk needed to produce tablets of compressible size and weight when the API dose is small. Microcrystalline cellulose (MCC), marketed under trade names including Avicel (IFF) and Celphere (DAICEL), is the world's most widely used pharmaceutical excipient by volume, valued for its excellent compressibility, binding capacity, and compatibility with a broad range of APIs across wet granulation, dry granulation, and direct compression processes. Lactose monohydrate and spray-dried lactose variants are the second most widely used filler category, though their application is constrained by lactose intolerance in certain patient populations and by incompatibility with specific API functional groups. Dicalcium phosphate dihydrate and anhydrous variants serve as calcium-supplementing fillers for nutritional supplement and generic tablet manufacturing. The filler and diluent segment is projected to grow at a 6.8% CAGR through 2034, slightly below the market average, as direct compression excipient systems displace some wet granulation-required filler formulations.

Binders represent 18.6% of market revenue in 2025 at USD 1.79 Billion. Povidone (polyvinylpyrrolidone/PVP) and its crosslinked variant crospovidone (which functions as both binder and disintegrant) are the dominant synthetic binder materials, marketed by BASF under the Kollidon brand. Hydroxypropyl cellulose (HPC), hydroxypropyl methylcellulose (HPMC), and gelatin serve as cellulosic and natural binders across wet granulation tablet manufacturing. Disintegrants account for 12.4% of market revenue at USD 1.20 Billion, with croscarmellose sodium (Ac-Di-Sol, FMC BioPolymer) and sodium starch glycolate (Explotab, JRS Pharma) as the primary superdisintegrant materials. Lubricants — primarily magnesium stearate and its functional alternatives including sodium stearyl fumarate (Pruv) — contribute 8.6% of revenue. Coating excipients, encompassing film-forming polymers, plasticizers, pigments, and enteric coating materials, account for 14.2% of market revenue at USD 1.37 Billion. Solubilizers, stabilizers, preservatives, and other functional excipients collectively represent the remaining 17.8% of the excipient market.

By Route of Administration

By route of administration, oral solid dosage (OSD) formulations account for the largest segment within the pharmaceutical excipient market at 62.6% of revenue in 2025 at USD 6.03 Billion. Tablet and capsule manufacturing consumes the highest volume of excipients by mass of any dosage form, as API doses typically represent only 10–40% of finished tablet mass, with the remainder comprising excipients. India's generic tablet manufacturing sector alone consumes an estimated 600,000 metric tons of excipients annually, while China's pharmaceutical manufacturing contributes comparable volumes. The OSD excipient segment is growing at a 6.8% CAGR through 2034, reflecting steady generic drug volume growth globally. Parenteral excipients, including tonicity agents (sodium chloride, mannitol), pH adjusters (citric acid, sodium phosphate), preservatives (benzalkonium chloride, parabens), and solubilizers (polysorbate 80, cyclodextrins), represent 14.4% of market revenue at USD 1.39 Billion. Parenteral excipient demand is growing at a faster rate than OSD — approximately 9.2% CAGR — driven by the biologics and sterile injectable market expansion. Topical, ophthalmic, and transdermal formulation excipients account for 10.8% of market revenue. Inhalation excipients — primarily lactose carriers for dry powder inhaler formulations — account for 7.4% of revenue. Oral liquid and semi-solid formulations contribute the remaining 4.8%.

By Source

By source, synthetic and semi-synthetic excipients dominate the pharmaceutical excipient market at approximately 64.8% of revenue in 2025 at USD 6.25 Billion. This category encompasses the major cellulose derivatives (MCC, HPMC, HPC, croscarmellose sodium), synthetic polymers (PVP/crospovidone, Carbopol, Eudragit), and petrochemical-derived materials (magnesium stearate, propylene glycol, PEG) that form the backbone of modern tablet, capsule, and parenteral formulations. Synthetic excipients offer consistent quality, defined pharmacopoeial monograph specifications, and reliable supply chain characteristics that natural materials sometimes cannot match at commercial pharmaceutical scale. Plant-derived natural excipients — including starch (corn, potato, tapioca), cellulose, lactose, sucrose, mannitol, and sorbitol — represent 28.4% of market revenue at USD 2.74 Billion. Plant-derived excipients benefit from generally recognized as safe (GRAS) status and consumer-positive perceptions, making them preferred for over-the-counter drug products and dietary supplements where clean label attributes have commercial value. Animal-derived excipients, including gelatin (for hard and soft capsule shells), stearic acid, and shellac, account for 6.8% of market revenue — a share under pressure from vegan formulation trends driving substitution toward plant-based capsule shell alternatives such as hydroxypropyl methylcellulose (HPMC) capsules.

Regional Analysis

Asia Pacific Pharmaceutical Excipient Market

Asia Pacific leads the global pharmaceutical excipient market with a 36.4% share in 2025, generating approximately USD 3.51 Billion in revenue. India and China collectively drive the regional market, each operating as one of the world's largest pharmaceutical manufacturing bases by output volume. India, the world's largest generic drug producer by volume and a major supplier to US, European, and emerging market prescription drug markets, consumes excipients at scale across its generic OSD manufacturing sector concentrated in Hyderabad, Ahmedabad, and Mumbai pharmaceutical clusters. India's annual excipient imports — primarily MCC, PVP, croscarmellose sodium, and HPMC — represent one of the world's largest national excipient trade flows, supplemented by growing domestic excipient production. China's pharmaceutical manufacturing sector, transitioning toward higher-quality GMP production under NMPA reforms, is a growing consumer of premium pharmacopoeial-grade excipients meeting USP, EP, and JP standards as manufacturers pursue US and EU export market access. Japan's advanced pharmaceutical manufacturing sector consumes high-quality domestic and imported excipients for both domestic market production and export-oriented specialty pharmaceutical manufacturing. South Korea's biopharmaceutical and generic drug sector is a growing excipient market. The Asia Pacific pharmaceutical excipient market is projected to grow at an 8.4% CAGR through 2034, reaching approximately USD 6.96 Billion.

North America Pharmaceutical Excipient Market

North America represents 27.8% of the global pharmaceutical excipient market in 2025 at approximately USD 2.68 Billion. The United States is the dominant national market, where the pharmaceutical manufacturing sector — comprising both branded drug manufacturers and a large generic drug production base supplying FDA-regulated products — generates substantial and sustained excipient demand. The FDA's current Good Manufacturing Practice (cGMP) regulations under 21 CFR Parts 210 and 211, combined with the USP/NF pharmacopoeial standards, define excipient quality requirements for US-market drug products and reward suppliers offering pharmaceutical-grade materials with full USP/NF monograph compliance and complete documentation packages. US-based specialty excipient manufacturers including Ashland, Lubrizol (Berkshire Hathaway), Colorcon, and FMC BioPolymer serve both domestic and global pharmaceutical formulation markets with differentiated, technology-intensive excipient products including modified-release polymer systems, film coating systems, and specialty solubilizers. The US over-the-counter (OTC) drug market is also a significant excipient consumer, with OTC solid dosage forms, topicals, and liquid formulations collectively driving demand for functional excipient categories including disintegrants, thickeners, and preservatives. Canada's generic pharmaceutical manufacturing sector contributes incremental regional demand. North America's pharmaceutical excipient market is projected to grow at a 6.8% CAGR through 2034.

Europe Pharmaceutical Excipient Market

Europe accounts for 22.6% of the global pharmaceutical excipient market in 2025 at USD 2.18 Billion. Germany, France, Italy, and Spain are the primary national markets, hosting both major pharmaceutical manufacturers and several of the world's leading pharmaceutical excipient producers. BASF SE (Ludwigshafen, Germany) is the world's largest pharmaceutical excipient supplier and one of the market's most influential competitive forces, with its Kollidon (PVP), Lutrol (poloxamer), and Soluplus (polyvinyl caprolactam-polyvinyl acetate-polyethylene glycol) product families serving formulation scientists globally. Roquette (Lestrem, France) is the leading supplier of starch-derived excipients including mannitol, sorbitol, and maltodextrin for pharmaceutical use. JRS Pharma (Germany) is a specialist in cellulose-based excipients including Prosolv SMCC (silicified MCC). Europe's pharmaceutical excipient market is driven by branded pharmaceutical manufacturing, generic drug production for EU markets, and the growing use of novel excipients in specialty formulations developed at European R&D centers. The European Pharmacopoeia (EP) sets the quality benchmark for excipients used in EU-marketed drug products. Europe's pharmaceutical excipient market is projected to grow at a 6.4% CAGR through 2034.

Latin America Pharmaceutical Excipient Market

Latin America holds a 8.2% share of the pharmaceutical excipient market in 2025 at approximately USD 0.79 Billion. Brazil is the dominant regional market, with a large domestic pharmaceutical manufacturing sector serving both branded and generic drug markets, regulated by ANVISA. Brazil's mandatory generic drug substitution policies and its government-funded pharmaceutical access programs generate sustained volume demand for excipients used in generic oral solid dosage formulations. Mexico's pharmaceutical manufacturing sector serves both domestic and US export markets, with several manufacturing facilities holding FDA approval for generic drug production. Argentina's domestic pharmaceutical industry and Colombia's growing branded generic sector contribute regional excipient demand. The Latin American pharmaceutical excipient market is characterized by high import dependency for specialty and polymeric excipients, with most regional manufacturers sourcing MCC, PVP, and disintegrants from European and US producers. Local commodity excipient production — primarily starch, lactose, and sucrose — exists in Brazil and Argentina. Regional demand is supported by population growth, expanding healthcare access, and government health insurance program expansion. The region's pharmaceutical excipient market is projected to grow at a 7.8% CAGR through 2034.

Middle East & Africa Pharmaceutical Excipient Market

The Middle East and Africa region accounts for 5.0% of global pharmaceutical excipient market revenue in 2025 at approximately USD 0.48 Billion. Saudi Arabia, Egypt, and South Africa are the primary national markets within the region. Saudi Arabia's domestic pharmaceutical manufacturing sector has expanded significantly under Vision 2030, with several facilities now producing generic oral solid dosage forms requiring pharmacopoeial-grade excipients aligned with SFDA GMP standards. Egypt is one of the largest pharmaceutical manufacturers in Africa and the Middle East, with a substantial domestic industry supplying regional markets and generating excipient demand for tablet and capsule production. South Africa's pharmaceutical manufacturing sector, the most developed in sub-Saharan Africa, serves domestic and regional distribution markets and consumes pharmaceutical-grade excipients across multiple dosage form categories. The MEA region's excipient market is primarily dependent on imports from European and Asian suppliers for pharmacopoeial-grade materials, though some commodity excipient production exists domestically in Egypt and Saudi Arabia. Growing healthcare infrastructure investment and pharmaceutical self-sufficiency programs are the primary long-term demand catalysts. MEA's pharmaceutical excipient market is projected to grow at a 8.6% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Functionality

- Fillers & Diluents (MCC, Lactose, Dicalcium Phosphate)

- Binders (PVP, HPC, HPMC)

- Disintegrants (Croscarmellose Sodium, Sodium Starch Glycolate)

- Lubricants (Magnesium Stearate, Sodium Stearyl Fumarate)

- Coating Excipients (HPMC, Eudragit, Plasticizers)

- Solubilizers, Stabilizers & Other Functional Excipients

By Route of Administration

- Oral Solid Dosage (OSD) — Tablets & Capsules

- Parenteral (Injectable & Infusion)

- Topical, Ophthalmic & Transdermal

- Inhalation (Dry Powder & Metered Dose Inhaler)

- Oral Liquid & Semi-Solid

By Source

- Synthetic & Semi-Synthetic Excipients

- Plant-Derived Natural Excipients

- Animal-Derived Excipients

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.64 B |

| Forecast Revenue (2034) | USD 18.26 B |

| CAGR (2025-2034) | 7.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Functionality, (Fillers & Diluents (MCC, Lactose, Dicalcium Phosphate), Binders (PVP, HPC, HPMC), Disintegrants (Croscarmellose Sodium, Sodium Starch Glycolate), Lubricants (Magnesium Stearate, Sodium Stearyl Fumarate), Coating Excipients (HPMC, Eudragit, Plasticizers), Solubilizers, Stabilizers & Other Functional Excipients), By Route of Administration, (Oral Solid Dosage (OSD) — Tablets & Capsules, Parenteral (Injectable & Infusion), Topical, Ophthalmic & Transdermal, Inhalation (Dry Powder & Metered Dose Inhaler), Oral Liquid & Semi-Solid), By Source, (Synthetic & Semi-Synthetic Excipients, Plant-Derived Natural Excipients, Animal-Derived Excipients) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BASF SE, IFF (INTERNATIONAL FLAVORS & FRAGRANCES), ROQUETTE FRERES, ASHLAND GLOBAL HOLDINGS, COLORCON, LUBRIZOL (BERKSHIRE HATHAWAY), DAICEL CORPORATION, SHIN-ETSU CHEMICAL, JRS PHARMA, SIGNET CHEMICAL CORPORATION, MEGGLE GMBH & CO., FMC CORPORATION (BIOPOLYMER DIVISION), CRODA INTERNATIONAL (AVANTI POLAR LIPIDS), AVANTOR (VWR MATERIALS), SPI PHARMA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Route of Administration (Oral Solid Dosage, Parenteral, Topical, Ophthalmic, Transdermal, Inhalation, Oral Liquid & Semi-Solid), By Source, Industry Trends, Regional Outlook, Competitive Landscape, Strategic Insights & Forecast 2026-2034")

, By Route of Administration (Oral Solid Dosage, Parenteral, Topical, Ophthalmic, Transdermal, Inhalation, Oral Liquid & Semi-Solid), By Source, Industry Trends, Regional Outlook, Competitive Landscape, Strategic Insights & Forecast 2026-2034")

, By Route of Administration (Oral Solid Dosage, Parenteral, Topical, Ophthalmic, Transdermal, Inhalation, Oral Liquid & Semi-Solid), By Source, Industry Trends, Regional Outlook, Competitive Landscape, Strategic Insights & Forecast 2026-2034")

Frequently Asked Questions

How big is the Pharmaceutical Excipient Market?

The Global Pharmaceutical Excipient Market was valued at USD 8.98 Billion in 2024 and is projected to reach USD 18.26 Billion by 2034, growing at a CAGR of 7.3% from 2026 to 2034, driven by rising pharmaceutical production, drug formulation advancements, and growing demand for functional excipients.

Who are the major players in the Pharmaceutical Excipient Market?

BASF SE, IFF (INTERNATIONAL FLAVORS & FRAGRANCES), ROQUETTE FRERES, ASHLAND GLOBAL HOLDINGS, COLORCON, LUBRIZOL (BERKSHIRE HATHAWAY), DAICEL CORPORATION, SHIN-ETSU CHEMICAL, JRS PHARMA, SIGNET CHEMICAL CORPORATION, MEGGLE GMBH & CO., FMC CORPORATION (BIOPOLYMER DIVISION), CRODA INTERNATIONAL (AVANTI POLAR LIPIDS), AVANTOR (VWR MATERIALS), SPI PHARMA, Others

Which segments covered the Pharmaceutical Excipient Market?

By Functionality, (Fillers & Diluents (MCC, Lactose, Dicalcium Phosphate), Binders (PVP, HPC, HPMC), Disintegrants (Croscarmellose Sodium, Sodium Starch Glycolate), Lubricants (Magnesium Stearate, Sodium Stearyl Fumarate), Coating Excipients (HPMC, Eudragit, Plasticizers), Solubilizers, Stabilizers & Other Functional Excipients), By Route of Administration, (Oral Solid Dosage (OSD) — Tablets & Capsules, Parenteral (Injectable & Infusion), Topical, Ophthalmic & Transdermal, Inhalation (Dry Powder & Metered Dose Inhaler), Oral Liquid & Semi-Solid), By Source, (Synthetic & Semi-Synthetic Excipients, Plant-Derived Natural Excipients, Animal-Derived Excipients)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharmaceutical Excipient Market

Published Date : 07 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date