- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharma Isolator Technology Market Size & Forecast | CAGR 10.9%

Global Pharmaceutical Isolator Technology Market Size, Share, Growth & Industry Analysis By Isolator Type (Aseptic Processing Isolators, Containment Isolators OEB 4/5, Combination Isolators), By Application (Sterile Fill-Finish, HPAPI Handling, Radiopharma Manufacturing, Cell & Gene Therapy, R&D Labs), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

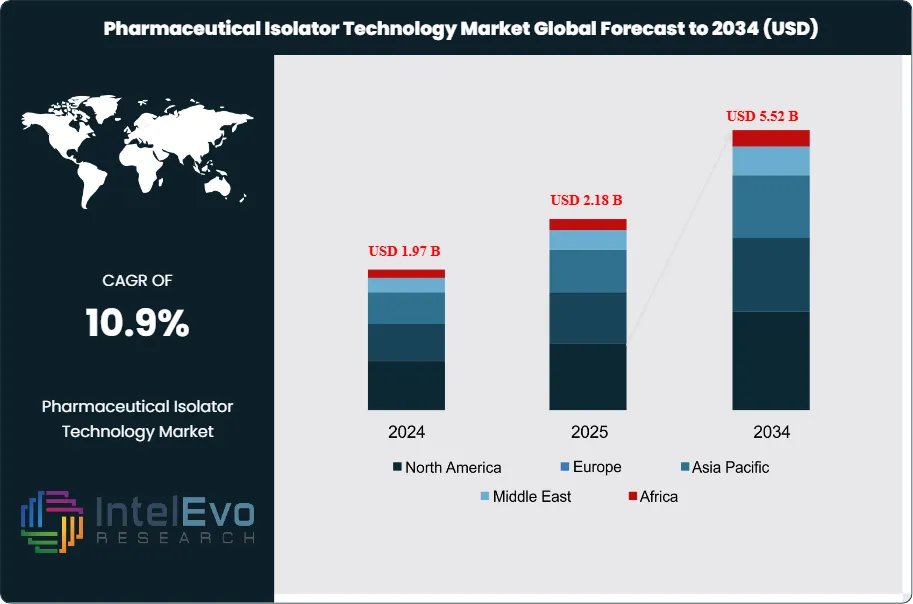

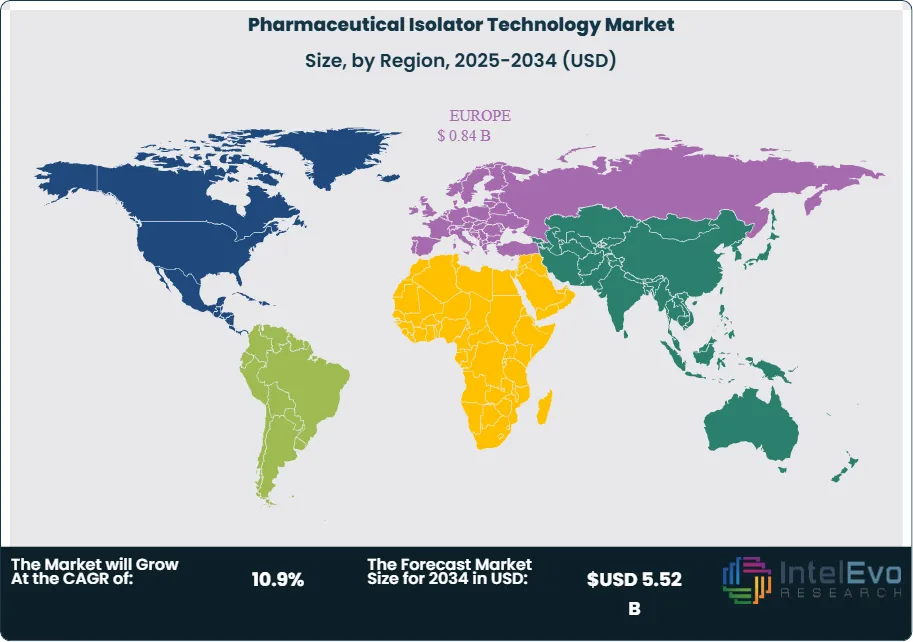

| USD 2.18 Billion | USD 5.52 Billion | 10.9% | Europe, 38.5% |

The Pharmaceutical Isolator Technology Market was valued at approximately USD 1.97 Billion in 2024 and reached USD 2.18 Billion in 2025. The market is projected to grow to USD 5.52 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.34 Billion over the analysis period, driven by intensifying aseptic manufacturing requirements, the commercial expansion of highly potent active pharmaceutical ingredients (HPAPIs), and the global buildout of cell and gene therapy production infrastructure.

Get More Information about this report -

Request Free Sample ReportPharmaceutical isolators are enclosed, controlled environments that separate manufacturing personnel from drug products and production processes. They maintain defined pressure differentials, HEPA-filtered airflow, and are sterilized in-situ using vaporized hydrogen peroxide (VHP) or other validated sterilants. Isolators serve two primary functions within pharmaceutical manufacturing: containment isolators protect operators from hazardous compounds including cytotoxic APIs and radiopharmaceuticals, while aseptic processing isolators protect sterile drug products from environmental contamination during filling, stoppering, and lyophilization operations. As regulatory expectations for sterile drug manufacturing have tightened under FDA 21 CFR Part 211, EU GMP Annex 1 (revised 2022), and WHO Technical Report Series guidelines, isolator-based cleanroom designs have increasingly displaced traditional open-barrier RABS and open-cleanroom architectures.

The revised EU GMP Annex 1, which became fully effective in August 2023 and has since defined global sterility assurance expectations, explicitly elevates isolator technology as the preferred sterile manufacturing environment. This regulatory shift has triggered a wave of facility modernization across European, US, and Asia Pacific pharmaceutical manufacturers, with capital expenditure programs for aseptic isolator installation accelerating sharply between 2023 and 2025. The FDA's Guidance for Industry on Sterile Drug Products Produced by Aseptic Processing similarly endorses barrier isolation technology, creating alignment between US and EU regulatory expectations that is compelling multi-regional manufacturers to standardize on isolator-based production formats.

On the demand side, the rapid expansion of the oncology biologics pipeline, including antibody-drug conjugates (ADCs), bispecific antibodies, and radiolabeled therapeutics, is generating sustained demand for containment isolators capable of handling highly potent compounds with occupational exposure limits (OELs) below 1 microgram per cubic meter. The radiopharmaceutical segment, in particular, is experiencing extraordinary growth as FDA approvals for radioligand therapies have accelerated, creating urgent demand for hot-cell type isolators with integrated radiation shielding for both clinical and commercial manufacturing.

Europe holds the largest share of the pharmaceutical isolator technology market at 38.5% in 2025, driven by the region's established sterile manufacturing base and the direct impact of EU GMP Annex 1 compliance investments. North America is the second-largest region, anchored by US pharmaceutical manufacturers and CDMOs upgrading aseptic fill-finish capacity. Asia Pacific is the fastest-growing market, with China, India, and South Korea investing heavily in GMP-compliant aseptic manufacturing infrastructure. The pharmaceutical isolator technology market across all regions is expected to benefit from increasing CDMO outsourcing activity and the proliferation of high-potency and sterile biologic drug modalities through 2034.

, By Application (Sterile Fill-Finish, HPAPI Handling, Radiopharma Manufacturing, Cell & Gene Therapy, R&D Labs), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global pharmaceutical isolator technology market was valued at USD 2.18 Billion in 2025 and is projected to reach USD 5.52 Billion by 2034, growing at a CAGR of 10.9% over the forecast period 2026–2034.

- Segment Dominance: By isolator type, aseptic processing isolators lead with approximately 52.4% of market revenue in 2025, driven by EU GMP Annex 1 compliance investments and the expansion of sterile biologic and small-molecule injectable manufacturing capacity globally.

- Segment Dominance: By application, sterile fill-finish manufacturing accounts for the largest application share at 44.8% of market revenue in 2025, reflecting the concentrated demand for aseptic isolators in liquid injectable, lyophilized, and pre-filled syringe production lines.

- Driver: The EU GMP Annex 1 revision (effective August 2023) and its global regulatory influence have directly accelerated isolator procurement, with European pharmaceutical manufacturers collectively committing an estimated USD 1.2 Billion in isolator-related capital expenditure between 2023 and 2025.

- Restraint: High capital costs for pharmaceutical-grade isolator systems — ranging from USD 300,000 for single-unit containment isolators to USD 3–5 Million for fully integrated aseptic fill-finish isolator lines — constrain adoption among smaller CDMOs and emerging-market manufacturers, limiting market penetration by an estimated 12–18% in cost-sensitive segments.

- Opportunity: The radiopharmaceutical manufacturing segment represents a concentrated growth opportunity, with the global radioligand therapy market expected to exceed USD 8.5 Billion by 2030, creating demand for shielded isolators, hot-cell enclosures, and integrated radiopharmaceutical dispensing systems valued at over USD 1.4 Billion through 2034.

- Trend: Integration of in-situ VHP sterilization with automated cycle validation and continuous environmental monitoring systems is now present in approximately 34.6% of new pharmaceutical isolator installations in 2025, up from 17.2% in 2020, as regulatory expectations for documented, automated sterility assurance increase.

- Regional Analysis: Europe leads the global pharmaceutical isolator technology market with a 38.5% share in 2025, generating approximately USD 0.84 Billion in revenue, underpinned by EU GMP Annex 1 compliance demands and the region's dense sterile pharmaceutical manufacturing base.

Competitive Landscape Overview

The pharmaceutical isolator technology market is moderately consolidated, with the top four players — SKAN AG, Getinge AB, Comecer S.p.A., and Telstar (Azbil Telstar) — collectively holding approximately 51.3% of global market revenue in 2025. Competition is primarily technology-driven, with suppliers differentiating on isolator barrier integrity, VHP sterilization cycle validation capabilities, integration with robotic fill-finish systems, and modular cleanroom interface design. Strategic acquisitions have accelerated since 2022, with equipment groups acquiring specialized hot-cell and radiopharmaceutical isolator firms to address the rapidly growing radioligand therapy manufacturing segment.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| SKAN AG | Switzerland | Leader | SKAN Aseptic Filling Isolator | Europe / Global | Feb 2025: Launched a next-generation modular aseptic filling isolator with integrated robotic arm interface and automated VHP cycle validation for single-use fill-finish lines. |

| Getinge AB | Sweden | Leader | Getinge Barrier Isolator System | Europe / North America | Apr 2025: Acquired a specialist radiopharmaceutical isolator manufacturer to expand its hot-cell and shielded enclosure portfolio for radioligand therapy production. |

| Comecer S.p.A. | Italy | Leader | Comecer ISOCON Containment Isolator | Europe / Global | Jan 2026: Entered a strategic partnership with a major European CDMO to supply integrated radiopharmaceutical dispensing isolators across five GMP production sites. |

| Telstar (Azbil Telstar) | Spain | Leader | Telstar AIS-1200 Aseptic Isolator | Europe / Asia Pacific | Sep 2025: Expanded manufacturing capacity in Barcelona by 30% to meet growing demand for aseptic isolators from EU GMP Annex 1 compliance programs. |

| Extract Technology | UK | Challenger | Sentinel Containment Isolator | Europe / North America | Mar 2025: Launched an upgraded high-potency containment isolator with OEB 5 classification and integrated continuous liner waste management for HPAPI manufacturers. |

| Bioquell (Ecolab) | UK | Challenger | Bioquell VHP Isolator Systems | North America / Europe | Nov 2024: Introduced a new portable VHP generator module compatible with third-party aseptic isolator platforms, expanding its installed base service opportunity. |

| Esco Pharma | Singapore | Challenger | Pharmos Aseptic Processing Isolator | Asia Pacific / Global | Jun 2025: Secured contracts with three Indian pharmaceutical manufacturers for aseptic filling isolator installations under India's PLI scheme for sterile injectables. |

| Azbil Telstar | Spain | Niche Player | Lyophilization Loading Isolator | Europe | Aug 2025: Launched an isolator system integrating automated lyophilizer loading robotics for the sterile biologic drug product segment. |

| Hosokawa Micron (Containment) | Japan | Niche Player | Micron Containment Isolator | Asia Pacific | May 2025: Delivered a custom OEB 5 containment isolator system to a South Korean ADC manufacturer for clinical-stage HPAPI handling. |

| Syntegon Technology | Germany | Niche Player | Pharmatec Aseptic Isolator Interface | Europe / North America | Jan 2025: Launched an integrated isolator interface module for its vial filling lines, enabling direct Annex 1-compliant coupling without cleanroom boundary modification. |

By Isolator Type

The pharmaceutical isolator technology market by isolator type is led by aseptic processing isolators, which account for approximately 52.4% of total market revenue in 2025, valued at USD 1.14 Billion. Aseptic processing isolators are engineered to maintain an ISO 5 (Grade A) internal environment through HEPA-filtered unidirectional airflow, positive pressure differentials relative to the surrounding cleanroom, and validated in-situ VHP sterilization cycles. These systems are the primary technology deployed in sterile drug product fill-finish operations for vials, syringes, and cartridges, and are increasingly integrated with robotic transfer and filling systems to eliminate manual interventions within the critical zone. The EU GMP Annex 1 revision has made aseptic processing isolators the reference design for new or refurbished sterile fill-finish suites across the EU, with adoption accelerating sharply in Germany, Ireland, Switzerland, and Italy since 2023. In North America, FDA endorsement of barrier isolation in its Aseptic Processing Guidance continues to drive capital investment, particularly among large integrated pharmaceutical manufacturers and CDMOs constructing new vial and pre-filled syringe filling capacity. The aseptic isolator segment is projected to grow at a 11.2% CAGR through 2034.

Containment isolators represent the second-largest segment at 38.6% of market revenue in 2025, or USD 0.84 Billion. These systems provide negative pressure containment environments that protect operators handling cytotoxic APIs, ADC payloads, radiolabeled compounds, and other HPAPIs with OELs below 10 micrograms per cubic meter (OEB 4) or below 1 microgram per cubic meter (OEB 5). Containment isolators are used across formulation, dispensing, sampling, milling, and tablet pressing operations for potent compounds. The growth of the ADC market — with more than 15 ADC products approved globally and over 100 in clinical development as of 2025 — is generating sustained incremental demand for OEB 5-rated containment isolators at both HPAPI manufacturer and CDMO sites. Containment isolators for radiopharmaceutical manufacturing, including shielded hot-cell type enclosures, are the fastest-growing sub-category, driven by the commercial expansion of radioligand therapies. Combination isolators (systems serving both aseptic and containment functions simultaneously) account for the remaining 9.0% of market revenue.

By Application

By application, sterile fill-finish manufacturing is the dominant use case within the pharmaceutical isolator technology market, accounting for 44.8% of market revenue in 2025 at USD 0.98 Billion. Sterile fill-finish encompasses the aseptic transfer, filling, stoppering, and sealing of parenteral drug products into primary containers including vials, pre-filled syringes, cartridges, and infusion bags. Regulatory requirements across FDA, EMA, and WHO technical guidelines mandate Grade A / ISO 5 conditions at the point of fill, which isolator technology reliably delivers with fewer contamination variables than traditional open-cleanroom filling. The expansion of biologics manufacturing — particularly for mAbs, mRNA vaccines, and protein therapeutics — is increasing the volume and complexity of aseptic fill-finish operations requiring isolator-based environments.

HPAPI and cytotoxic drug handling represents 28.4% of market revenue in 2025 at USD 0.62 Billion. This application encompasses all isolator deployments for manufacturing, formulation, weighing, and dispensing of compounds classified OEB 4 and above. The global HPAPI market is growing at approximately 9.8% annually through 2034, propelled by oncology drug development, and the CDMOs serving this segment are major buyers of OEB 5 containment isolator systems. Radiopharmaceutical manufacturing accounts for 14.6% of market revenue in 2025 at USD 0.32 Billion and is the fastest-growing application, with a projected CAGR of 16.8% through 2034. Cell and gene therapy manufacturing and research and development laboratory applications account for approximately 7.4% and 4.8% of market revenue respectively, with CGT-specific isolators gaining traction as autologous cell therapy manufacturers seek GMP-compliant contained environments for patient-specific batch processing.

By End-User

By end-user, pharmaceutical and biopharmaceutical manufacturers are the primary purchasers of pharmaceutical isolator technology, generating 52.6% of market revenue in 2025 at USD 1.15 Billion. This segment includes large integrated drug manufacturers investing in facility upgrades for Annex 1 compliance and capacity expansion for new biologic drug products. CDMOs represent the second-largest end-user group at 31.4% of revenue in 2025, or USD 0.68 Billion, reflecting the structural shift toward outsourced sterile manufacturing and HPAPI handling. CDMOs operating shared-use, multi-client facilities have a particularly strong demand for isolator technology, as it enables rapid validated product changeover without full suite decontamination between campaigns. Research institutions, hospital pharmacies — including those operating nuclear medicine departments and compounding sterile preparations — and government agencies collectively account for approximately 16.0% of market revenue. Hospital nuclear pharmacies are a distinct growth sub-segment, purchasing compact shielded isolators for patient-specific radiopharmaceutical dispensing under USP Chapter 825 and EU pharmacopoeial standards.

Regional Analysis

Europe Pharmaceutical Isolator Technology Market

Europe holds the largest share of the global pharmaceutical isolator technology market at 38.5% in 2025, generating approximately USD 0.84 Billion in revenue. The region's dominance reflects the direct impact of the EU GMP Annex 1 revision, which became fully enforceable in August 2023 and established isolator technology as the reference standard for new Grade A aseptic manufacturing environments across EU member states. Germany, Switzerland, Italy, and Ireland are the primary markets, hosting the European headquarters and production sites of numerous global pharmaceutical manufacturers, all of which have active Annex 1 compliance capital programs. Germany's dense pharmaceutical manufacturing base, including major sterile injectables producers and HPAPI-handling CDMOs, makes it the single largest national market within Europe. Switzerland's pharmaceutical cluster, anchored by the operations of global biopharma leaders in Basel and Zurich, has driven significant investment in aseptic isolator infrastructure for biologics fill-finish. Ireland, as a hub for US pharmaceutical company European manufacturing operations, has seen multiple multi-million-dollar isolator installation projects at fill-finish facilities in Cork, Waterford, and Dublin since 2023. The EMA's alignment with ICH Q guidelines and its active promotion of quality risk management frameworks further reinforce isolator adoption as the GMP-preferred containment design. Europe's pharmaceutical isolator technology market is projected to grow at a 10.4% CAGR through 2034.

North America Pharmaceutical Isolator Technology Market

North America represents 31.2% of the pharmaceutical isolator technology market in 2025 at approximately USD 0.68 Billion. The United States is the dominant national market, driven by large pharmaceutical manufacturers and CDMOs undertaking aseptic capacity expansion and GMP modernization across New Jersey, Pennsylvania, North Carolina, and Indiana — the country's primary pharmaceutical manufacturing corridors. FDA's ongoing enforcement of its Aseptic Processing Guidance, combined with the agency's increased focus on sterility assurance in 483 observations and Warning Letters since 2020, has elevated isolator investment from optional to operationally critical for many manufacturers. The US radioligand therapy market is growing rapidly following FDA approvals for lutetium-based therapeutics, with Novartis, Eli Lilly, and Bristol-Myers Squibb all investing in dedicated radiopharmaceutical manufacturing infrastructure requiring GMP-grade shielded isolators. The United States Pharmacopeia (USP) Chapter 825, governing radiopharmaceutical compounding and manufacturing, has added specific isolator environment requirements that are expanding the addressable market within hospital radiopharmacies and nuclear medicine departments. Canada contributes to regional demand through Health Canada-regulated pharmaceutical manufacturing, particularly in Ontario and Quebec. North America's pharmaceutical isolator technology market is expected to grow at a 10.8% CAGR through 2034.

Asia Pacific Pharmaceutical Isolator Technology Market

Asia Pacific accounts for 21.4% of the global pharmaceutical isolator technology market in 2025 at USD 0.47 Billion and is the fastest-growing region with a projected CAGR of 13.6% through 2034. China's pharmaceutical manufacturing sector is undergoing a quality-driven modernization following NMPA GMP revisions that increasingly align with EU GMP and WHO standards. Several major Chinese CDMOs and sterile injectables manufacturers have invested in aseptic isolator lines as part of broader facility qualification programs targeting US and EU export market access. India's sterile injectables manufacturing base is expanding rapidly under the PLI scheme, with government incentives driving construction of new aseptic fill-finish facilities, many of which incorporate isolator technology to meet FDA and EMA export market compliance requirements. Japan's advanced pharmaceutical manufacturing sector, regulated by PMDA, has adopted EU GMP Annex 1-equivalent aseptic manufacturing standards, driving isolator adoption at both domestic and export-oriented facilities. South Korea's growing CDMO sector, particularly in biologics and cell therapy manufacturing, is adding isolator-equipped capacity to serve global pharmaceutical clients. The Asia Pacific pharmaceutical isolator technology market represents the most significant geographic growth opportunity for equipment suppliers through 2034.

Latin America Pharmaceutical Isolator Technology Market

Latin America holds a 5.6% share of the pharmaceutical isolator technology market in 2025 at approximately USD 0.12 Billion. Brazil is the largest market in the region, driven by ANVISA's GMP framework and domestic pharmaceutical manufacturers investing in aseptic fill-finish capacity for biologics, vaccines, and oncology injectables. Fiocruz's substantial vaccine production mandate has included investment in GMP-grade filling infrastructure, including isolator-equipped lines for sterile biological products. Mexico's pharmaceutical sector, supplying both domestic and North American markets, is increasing isolator adoption at sterile manufacturing sites oriented toward FDA-regulated export production. Argentina's domestic pharmaceutical industry contributes to regional demand through sterile injectables capacity investment. The primary constraints in Latin America remain the high cost of imported isolator equipment and limited local engineering expertise for installation, validation, and lifecycle maintenance. International isolator suppliers are addressing this through local partnerships and service center establishment. Latin America's pharmaceutical isolator technology market is projected to grow at a 9.4% CAGR through 2034.

Middle East & Africa Pharmaceutical Isolator Technology Market

The Middle East and Africa region accounts for 3.3% of global pharmaceutical isolator technology market revenue in 2025 at approximately USD 0.07 Billion. Saudi Arabia and the UAE are the primary demand centers, where national pharmaceutical manufacturing programs under Vision 2030 and similar strategies are building domestic sterile drug production capacity that requires GMP-grade aseptic equipment. The Saudi Food and Drug Authority (SFDA) and UAE's Ministry of Health have progressively aligned GMP standards with EU and ICH requirements, establishing a regulatory basis for isolator technology adoption in new manufacturing investments. South Africa's pharmaceutical manufacturing sector, the most developed in sub-Saharan Africa, contributes to regional demand through investment in sterile and oncology drug manufacturing. Hospital pharmacies in the GCC region, where nuclear medicine programs are expanding as part of healthcare infrastructure development, represent a growing market for compact radiopharmaceutical dispensing isolators. MEA's pharmaceutical isolator technology market is expected to grow at a 10.6% CAGR through 2034, supported by healthcare infrastructure investment and pharmaceutical self-sufficiency programs across the GCC and North Africa.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Isolator Type

- Aseptic Processing Isolators

- Containment Isolators (OEB 4 / OEB 5)

- Combination Isolators (Aseptic + Containment)

By Application

- Sterile Fill-Finish Manufacturing

- HPAPI & Cytotoxic Drug Handling

- Radiopharmaceutical Manufacturing

- Cell & Gene Therapy Manufacturing

- Research & Development Laboratories

By End-User

- Pharmaceutical & Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Hospital Pharmacies & Nuclear Medicine Departments

- Research Institutions & Government Agencies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.18 B |

| Forecast Revenue (2034) | USD 5.52 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Isolator Type, (Aseptic Processing Isolators, Containment Isolators (OEB 4 / OEB 5), Combination Isolators (Aseptic + Containment)), By Application, (Sterile Fill-Finish Manufacturing, HPAPI & Cytotoxic Drug Handling, Radiopharmaceutical Manufacturing, Cell & Gene Therapy Manufacturing, Research & Development Laboratories), By End-User, (Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Hospital Pharmacies & Nuclear Medicine Departments, Research Institutions & Government Agencies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SKAN AG, GETINGE AB, COMECER S.P.A., TELSTAR (AZBIL TELSTAR), EXTRACT TECHNOLOGY, BIOQUELL (ECOLAB), ESCO PHARMA, SYNTEGON TECHNOLOGY, HOSOKAWA MICRON (CONTAINMENT DIVISION), ILC DOVER, WEISS TECHNIK (SCHUNK GROUP), DEC GROUP, BOSCH PACKAGING TECHNOLOGY (SYNTEGON), NNE A/S, VANRX PHARMASYSTEMS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Sterile Fill-Finish, HPAPI Handling, Radiopharma Manufacturing, Cell & Gene Therapy, R&D Labs), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

, By Application (Sterile Fill-Finish, HPAPI Handling, Radiopharma Manufacturing, Cell & Gene Therapy, R&D Labs), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

, By Application (Sterile Fill-Finish, HPAPI Handling, Radiopharma Manufacturing, Cell & Gene Therapy, R&D Labs), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Pharmaceutical Isolator Technology Market?

Global Pharma isolator technology market valued at USD 1.97B in 2024, reaching USD 5.52B by 2034, growing at a CAGR of 10.9% from 2026–2034.

Who are the major players in the Pharmaceutical Isolator Technology Market?

SKAN AG, GETINGE AB, COMECER S.P.A., TELSTAR (AZBIL TELSTAR), EXTRACT TECHNOLOGY, BIOQUELL (ECOLAB), ESCO PHARMA, SYNTEGON TECHNOLOGY, HOSOKAWA MICRON (CONTAINMENT DIVISION), ILC DOVER, WEISS TECHNIK (SCHUNK GROUP), DEC GROUP, BOSCH PACKAGING TECHNOLOGY (SYNTEGON), NNE A/S, VANRX PHARMASYSTEMS, Others

Which segments covered the Pharmaceutical Isolator Technology Market?

By Isolator Type, (Aseptic Processing Isolators, Containment Isolators (OEB 4 / OEB 5), Combination Isolators (Aseptic + Containment)), By Application, (Sterile Fill-Finish Manufacturing, HPAPI & Cytotoxic Drug Handling, Radiopharmaceutical Manufacturing, Cell & Gene Therapy Manufacturing, Research & Development Laboratories), By End-User, (Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Hospital Pharmacies & Nuclear Medicine Departments, Research Institutions & Government Agencies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharmaceutical Isolator Technology Market

Published Date : 30 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date