- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharma Lyophilization Equipment Market Size & Forecast | CAGR 10.9%

Global Pharmaceutical Lyophilization Equipment Market Size, Share, Growth & Industry Analysis By Equipment Type (Large-Scale Freeze Dryers, Pilot & Clinical-Scale Systems, Laboratory & Benchtop Units, Automated Loading & Unloading Systems), By Application (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Research Institutes) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.86 Billion | USD 7.24 Billion | 10.9% | North America, 38.2% |

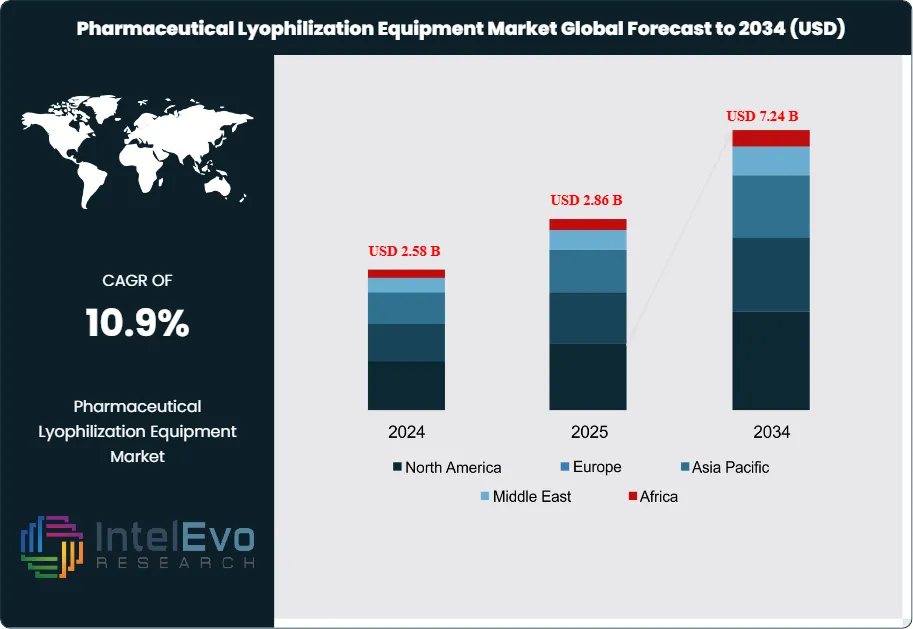

The Pharmaceutical Lyophilization Equipment Market was valued at approximately USD 2.58 Billion in 2024 and reached USD 2.86 Billion in 2025. The market is projected to grow to USD 7.24 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.38 Billion over the analysis period, as pharmaceutical manufacturers worldwide accelerate investment in freeze-drying capacity to support the commercialization of biologics, mRNA therapeutics, cell and gene therapy products, and complex small-molecule injectables that require lyophilization to achieve acceptable stability and shelf life.

Get More Information about this report -

Request Free Sample ReportPharmaceutical lyophilization, commonly referred to as freeze-drying, is a dehydration process in which a drug product is frozen and water is removed by sublimation under vacuum, yielding a dry cake or powder that can be reconstituted at the point of use. The process preserves the chemical and biological integrity of thermolabile compounds that cannot withstand conventional drying temperatures, making it the preservation method of choice for proteins, monoclonal antibodies, vaccines, peptides, and viral vectors. Lyophilization equipment encompasses freeze dryers (also termed lyophilizers) of various scales — from laboratory development units through clinical-scale pilot systems to large-format commercial production dryers — along with automated loading and unloading systems, condenser-dryer integrated units, and associated process analytical technology (PAT) instruments.

Demand growth in the pharmaceutical lyophilization equipment market is fundamentally linked to the biologics pipeline. FDA data confirms that more than 40% of novel drug approvals in 2024 were biologics, and a substantial proportion of approved and pipeline biologic drug products require lyophilization as their final dosage form. The global market for lyophilized injectable drugs exceeded USD 95 Billion in 2025 and is growing faster than the broader parenteral market, creating a structural pull on lyophilization capacity investment. EU GMP Annex 1 (revised 2022, effective 2023) has added additional regulatory pressure by establishing detailed requirements for lyophilizer sterilization validation, container closure integrity testing at the lyophilizer loading interface, and integration of lyophilizers within isolator-based fill-finish lines — all of which are prompting manufacturers to replace legacy equipment with modern, Annex 1-compliant systems.

On the technology side, suppliers are introducing lyophilization platforms with significantly improved energy efficiency, cycle time reduction through optimized sublimation control, and embedded process analytical tools including tunable diode laser absorption spectroscopy (TDLAS) for real-time water vapor flow measurement and Pirani/capacitance gauge endpoint detection. These advances reduce process cycle times by 15–25% compared to prior-generation systems, improving asset utilization for manufacturers operating under capacity constraints. Automation of lyophilizer loading and unloading — driven by EU GMP Annex 1's requirement to eliminate manual interventions within Grade A aseptic zones — is also increasing the average system value per installation.

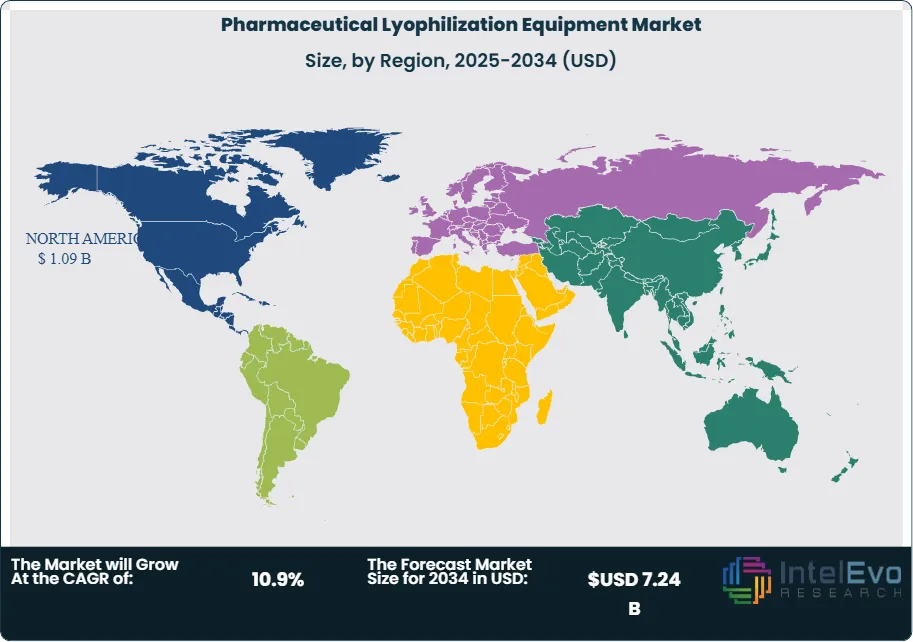

North America holds the largest share of the pharmaceutical lyophilization equipment market at 38.2% in 2025, anchored by the United States' dominant biologics manufacturing base and extensive CDMO fill-finish infrastructure. Europe is the second-largest region at 31.8%, where Annex 1 compliance is the primary capital investment driver. Asia Pacific is the fastest-growing region, led by China, India, and South Korea. The pharmaceutical lyophilization equipment market across all regions is supported by the structural shift toward outsourced manufacturing, which concentrates lyophilization equipment investment in CDMO facilities operating multiple pharmaceutical customer campaigns simultaneously.

, By Application (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Research Institutes) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global pharmaceutical lyophilization equipment market was valued at USD 2.86 Billion in 2025 and is projected to reach USD 7.24 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period 2025–2034.

- Segment Dominance: By equipment type, large-scale production freeze dryers account for approximately 54.6% of market revenue in 2025, driven by commercial-scale biologics and injectable drug manufacturing capacity expansion across integrated pharmaceutical companies and CDMOs.

- Segment Dominance: By application, biologics and biosimilars manufacturing is the leading application segment at 47.3% of market revenue in 2025, as the proliferation of approved and pipeline mAbs, ADCs, mRNA therapeutics, and recombinant proteins drives sustained lyophilization capacity investment.

- Driver: The global lyophilized injectable drug market exceeded USD 95 Billion in 2025, growing at approximately 9.2% annually and directly driving capital expenditure for pharmaceutical lyophilization equipment at both integrated manufacturer and CDMO facilities.

- Restraint: Long lyophilization cycle times — averaging 24–72 hours per batch for complex biologics — constrain asset utilization and limit the throughput of a given lyophilizer installation, requiring manufacturers to invest in multiple parallel units to meet commercial output targets and increasing total capital commitment.

- Opportunity: Continuous lyophilization technology, including spray freeze-drying and spin freeze-drying platforms, represents an emerging addressable opportunity exceeding USD 1.6 Billion through 2034, as pharmaceutical manufacturers seek throughput improvements and cycle time reductions that conventional batch freeze-drying cannot achieve.

- Trend: Automated loading and unloading systems for pharmaceutical lyophilizers are present in approximately 41.2% of new commercial freeze dryer installations in 2025, up from 18.6% in 2019, driven by EU GMP Annex 1 requirements to eliminate manual Grade A zone interventions.

- Regional Analysis: North America leads the global pharmaceutical lyophilization equipment market with a 38.2% share in 2025, generating approximately USD 1.09 Billion in revenue, anchored by extensive US biologics manufacturing capacity and a dense CDMO fill-finish infrastructure.

Competitive Landscape Overview

The pharmaceutical lyophilization equipment market is moderately consolidated, with the top four players — IMA Life, Getinge AB (Lyomax), GEA Group, and Optima Pharma — collectively accounting for approximately 53.8% of global market revenue in 2025. Competition centers on cycle development support, regulatory validation documentation capabilities, automated loading system integration, and proprietary PAT tool compatibility. M&A activity has increased, with major equipment groups acquiring loading automation and PAT instrument specialists to offer integrated lyophilizer platforms that align with EU GMP Annex 1 compliance requirements.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| IMA Life | Italy | Leader | IMA Life Lyophilizer Series | Europe / Global | Mar 2025: Launched an integrated lyophilizer-isolator platform with automated vial loading specifically engineered for EU GMP Annex 1 compliance in aseptic fill-finish lines. |

| Getinge AB (Lyomax) | Sweden | Leader | Lyomax Production Freeze Dryer | Europe / North America | Jan 2025: Expanded production freeze dryer manufacturing capacity at its German facility by 25% to address growing order backlog driven by Annex 1 compliance programs. |

| GEA Group | Germany | Leader | GEA LYOVAPOR Freeze Dryer | Europe / Global | May 2025: Introduced a smart lyophilization platform with integrated TDLAS monitoring and AI-assisted cycle development tools targeting biologics manufacturer productivity improvement. |

| Optima Pharma | Germany | Leader | OPTIMA LYOBOT Automated Loading System | Europe / North America | Feb 2026: Secured a multi-unit contract with a US-based CDMO for LYOBOT-equipped lyophilizer installations across two aseptic fill-finish sites, valued at approximately USD 38 Million. |

| SP Industries | USA | Challenger | VirTis Freeze Dryer Series | North America / Europe | Apr 2025: Launched a new pilot-scale R&D lyophilizer with modular PAT instrument ports targeting clinical-stage biopharmaceutical developers. |

| Millrock Technology | USA | Challenger | LyoStar 3 PAT Freeze Dryer | North America | Nov 2024: Released a firmware update enabling real-time primary drying endpoint detection via TDLAS integration across its LyoStar commercial series. |

| Telstar (Azbil Telstar) | Spain | Challenger | Lyobeta Pilot Freeze Dryer | Europe / Asia Pacific | Jul 2025: Delivered a pilot lyophilizer system to a major South Korean biologics CDMO as part of a multi-unit equipment supply framework agreement. |

| HOF Sonderanlagenbau | Germany | Niche Player | HOF Bulk Tray Freeze Dryer | Europe | Sep 2025: Installed a large-format bulk lyophilizer for an mRNA vaccine manufacturer requiring high-throughput bulk drug substance freeze-drying capacity. |

| Labconco Corporation | USA | Niche Player | FreeZone Benchtop Lyophilizer | North America | Jan 2025: Launched an upgraded benchtop freeze dryer series with improved condenser capacity and a redesigned manifold system targeting pharmaceutical R&D laboratories. |

| Syntegon Technology | Germany | Niche Player | Lyophilization Loading Interface | Europe / North America | Jun 2025: Released an automated lyophilizer loading module compatible with its Versynta vial filling platform for integrated Annex 1-compliant fill-freeze-finish lines. |

By Equipment Type

The pharmaceutical lyophilization equipment market by equipment type is led by large-scale production freeze dryers, which account for approximately 54.6% of total market revenue in 2025, valued at USD 1.56 Billion. These commercial freeze dryers — typically characterized by shelf areas exceeding 10 square meters and condenser capacities above 200 kg of ice — are the primary capital investment category for pharmaceutical manufacturers operating at commercial scale for biologics, vaccines, and injectable small molecules. Major manufacturers deploy production freeze dryers with shelf areas ranging from 30 to over 100 square meters for high-volume commercial campaigns, with individual unit values ranging from USD 1.5 Million to USD 5 Million depending on scale, automation level, and sterilization configuration. Demand in this category is driven directly by new biologic product launches and biosimilar market entry, with each new commercial lyophilized product typically requiring 2–4 dedicated freeze dryer units to meet initial launch supply. The large-scale production freeze dryer segment is projected to grow at a 11.1% CAGR through 2034, as biologics manufacturing capacity buildout continues across North America, Europe, and Asia Pacific.

Pilot and clinical-scale freeze dryers represent the second-largest equipment segment at 26.8% of market revenue in 2025, valued at USD 0.77 Billion. These mid-scale systems, with shelf areas typically between 1 and 10 square meters, serve two distinct functions: pharmaceutical process development and cycle optimization for new drug products, and clinical supply manufacturing for Phase I through Phase III clinical programs. The pharmaceutical industry's active biologics pipeline — with over 600 monoclonal antibody programs in clinical development as of 2025 — generates substantial demand for pilot-scale lyophilizers at CDMOs and integrated pharmaceutical companies conducting formulation development and clinical batch manufacturing. Pilot systems are also increasingly configured with the same PAT instrumentation as commercial units, enabling reliable scale-up of lyophilization cycles from clinical to commercial scale with reduced re-validation burden. Laboratory and benchtop freeze dryers account for 12.4% of market revenue in 2025, serving pharmaceutical R&D departments, universities, and analytical testing laboratories. Automated loading and unloading systems, priced separately from the freeze dryer itself, represent approximately 6.2% of market revenue and are the fastest-growing equipment category.

By Application

By application, biologics and biosimilars manufacturing is the dominant segment within the pharmaceutical lyophilization equipment market, accounting for 47.3% of market revenue in 2025 at USD 1.35 Billion. This segment encompasses lyophilization of monoclonal antibodies, recombinant proteins, fusion proteins, bispecific antibodies, ADCs, and biosimilars — all of which typically require freeze-drying to achieve the required 2–5 year shelf life at refrigerated storage conditions. The commercial approval of more than 160 monoclonal antibody products globally and the accelerating biosimilar wave following loss of exclusivity for original biologics are sustaining high levels of lyophilization equipment procurement from both large integrated biopharma companies and CDMOs. Vaccine manufacturing accounts for 21.8% of market revenue at USD 0.62 Billion. The COVID-19 pandemic demonstrated the centrality of lyophilization to vaccine manufacturing and distribution — freeze-dried vaccine formulations offer substantial cold chain advantages — and global vaccine manufacturers have invested accordingly in freeze-drying capacity.

Small-molecule injectable drugs requiring lyophilization represent 18.6% of market revenue in 2025 at USD 0.53 Billion. Despite biologics being the primary growth driver, a significant portion of chemotherapy agents, antifungals, beta-lactam antibiotics, and other parenteral drugs require lyophilization due to aqueous instability. The oncology injectable segment is particularly active, with multiple approved cytotoxic agents produced as lyophilized formulations. Cell and gene therapy manufacturing accounts for 7.4% of market revenue at USD 0.21 Billion, a share that is growing rapidly as autologous and allogeneic CGT products require specialized lyophilization protocols for viral vector components and cell-associated biologics. Other applications, including diagnostic reagents and nutraceutical actives, collectively make up the remaining 4.9% of market revenue.

By End-User

By end-user, pharmaceutical and biopharmaceutical manufacturers represent the largest purchaser group within the pharmaceutical lyophilization equipment market, generating 51.4% of market revenue in 2025 at USD 1.47 Billion. These integrated manufacturers invest in lyophilization capacity for both internally developed products and as part of broader sterile fill-finish facility capital programs. Large integrated companies such as Pfizer, Eli Lilly, Novartis, AstraZeneca, and their peers have collectively invested hundreds of millions of dollars in freeze dryer capacity over the 2021–2025 period to support commercial launches of new biologics and mRNA-based products. CDMOs represent the second-largest end-user segment at 34.8% of market revenue in 2025 or USD 1.00 Billion. CDMOs serve the lyophilization needs of emerging biotech companies and large pharma clients that have chosen to outsource sterile manufacturing, creating concentrated demand for multi-product, multi-campaign freeze dryer infrastructure. Research institutions and government organizations, including academic pharmaceutical science departments and public health manufacturing entities, account for 9.6% of market revenue. Hospital pharmacies and specialty compounding facilities account for the remaining 4.2%.

Regional Analysis

North America Pharmaceutical Lyophilization Equipment Market

North America holds the leading position in the global pharmaceutical lyophilization equipment market with a 38.2% share in 2025, generating approximately USD 1.09 Billion in revenue. The United States accounts for the vast majority of regional demand, driven by the world's largest biologics manufacturing base and a CDMO sector that has invested aggressively in sterile fill-finish and lyophilization capacity since 2020. US pharmaceutical manufacturers including Eli Lilly, Pfizer, Amgen, and Regeneron have expanded or greenfield-constructed lyophilization suites to support commercial launches of mAbs, ADCs, and GLP-1 receptor agonist drug substances requiring lyophilized formulation. The FDA's Guidance for Industry on Lyophilization of Parenterals and its Aseptic Processing Guidance together establish the US regulatory framework for freeze dryer validation, process characterization, and cycle qualification — requirements that drive investment in modern, compliant lyophilizer platforms as manufacturers replace legacy equipment to maintain inspection-ready status. The US also hosts the densest concentration of CDMO lyophilization capacity globally, with major operators in New Jersey, Massachusetts, Indiana, and North Carolina providing outsourced freeze-drying services. Canada contributes to regional demand through its domestic biologics manufacturing programs and pharmaceutical export orientation. North America's pharmaceutical lyophilization equipment market is projected to grow at a 10.4% CAGR through 2034.

Europe Pharmaceutical Lyophilization Equipment Market

Europe represents 31.8% of the pharmaceutical lyophilization equipment market in 2025 at USD 0.91 Billion. Germany, Italy, Switzerland, and Ireland are the primary markets, each hosting significant pharmaceutical manufacturing capacity with active lyophilization equipment procurement programs. The EU GMP Annex 1 revision has been the most significant recent catalyst for lyophilization equipment investment in Europe, as its requirements for integrated lyophilizer-isolator configurations, automated loading and unloading to eliminate Grade A manual interventions, and sterilization validation documentation have triggered widespread replacement of older freeze dryer installations that cannot be economically upgraded to meet the new standard. German pharmaceutical equipment manufacturers — particularly GEA Group and Optima Pharma — benefit from proximity to their primary customer base and from deep application expertise in GMP lyophilization, giving them a competitive advantage in the European market. Italy's pharmaceutical manufacturing sector, one of the largest in the EU by production volume, drives demand through its active injectables manufacturing base. Switzerland's biopharma cluster contributes through commercial-scale biologics fill-finish investment. Ireland's position as a European manufacturing hub for US pharmaceutical companies continues to attract multi-million-dollar lyophilizer investments. Europe's pharmaceutical lyophilization equipment market is expected to grow at a 10.7% CAGR through 2034.

Asia Pacific Pharmaceutical Lyophilization Equipment Market

Asia Pacific accounts for 20.6% of the global pharmaceutical lyophilization equipment market in 2025 at USD 0.59 Billion and is the fastest-growing region, with a projected CAGR of 13.8% through 2034. China is the dominant national market within the region, where domestic pharmaceutical manufacturers and CDMOs are investing heavily in lyophilization capacity to support the production of biologic drug products for both the domestic market and for global pharmaceutical clients. The NMPA's progressive alignment with ICH guidelines and its heightened enforcement of GMP standards at sterile manufacturing sites has accelerated equipment modernization among Chinese manufacturers, with older domestically-produced freeze dryers being replaced by internationally-manufactured systems meeting EU and FDA compliance standards. India's pharmaceutical sector, already a global leader in generic drug manufacturing, is adding lyophilized injectable capacity through PLI scheme-supported investments, targeting export markets in the US and EU. South Korea's growing biologics CDMO sector, anchored by Samsung Biologics and Celltrion, has added substantial lyophilization capacity to serve global pharmaceutical clients. Japan's domestic pharmaceutical market sustains demand through its established injectables manufacturing base and regulatory environment aligned with ICH Q standards. The Asia Pacific pharmaceutical lyophilization equipment market represents the primary geographic growth opportunity for suppliers through 2034.

Latin America Pharmaceutical Lyophilization Equipment Market

Latin America holds a 5.8% share of the pharmaceutical lyophilization equipment market in 2025 at approximately USD 0.17 Billion. Brazil is the dominant regional market, driven by ANVISA-regulated pharmaceutical manufacturing and the active investment programs of Fiocruz and Instituto Butantan in vaccine and biologic drug production capacity. Fiocruz's partnership-based vaccine manufacturing programs include lyophilized vaccine formulations that require dedicated freeze-drying capacity, making it a direct buyer of production-scale pharmaceutical lyophilizers. Mexico's pharmaceutical manufacturing sector, serving both domestic and North American markets, represents the second-largest country market in the region. Argentina contributes through its active domestic pharmaceutical industry. The primary constraints in Latin America remain the high cost of imported GMP lyophilization equipment, limited local validation engineering expertise, and foreign exchange considerations affecting capital procurement decisions for US dollar-denominated equipment purchases. International lyophilizer suppliers are addressing these barriers through equipment financing arrangements and by establishing local service partnerships. Latin America's pharmaceutical lyophilization equipment market is projected to grow at a 9.2% CAGR through 2034.

Middle East & Africa Pharmaceutical Lyophilization Equipment Market

The Middle East and Africa region accounts for 3.6% of global pharmaceutical lyophilization equipment market revenue in 2025 at approximately USD 0.10 Billion. Saudi Arabia and the UAE are the primary demand centers within the GCC, where national pharmaceutical manufacturing programs are investing in sterile drug production infrastructure including lyophilization capacity. Saudi Arabia's SFDA has aligned its sterile pharmaceutical manufacturing requirements with international GMP standards, creating a regulatory foundation for pharmaceutical-grade lyophilizer procurement. South Africa's pharmaceutical manufacturing sector, the most developed in sub-Saharan Africa, contributes to regional demand through its established injectables production base. The MEA region's lyophilization equipment market is in an early growth phase, with most current activity concentrated in feasibility assessments, single-unit pilot installations, and technology transfer partnerships with international equipment suppliers. Government healthcare self-sufficiency strategies across the GCC are the primary long-term demand catalyst. MEA's pharmaceutical lyophilization equipment market is projected to grow at a 11.4% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Equipment Type

- Large-Scale Production Freeze Dryers

- Pilot & Clinical-Scale Freeze Dryers

- Laboratory & Benchtop Freeze Dryers

- Automated Loading & Unloading Systems

By Application

- Biologics & Biosimilars Manufacturing

- Vaccine Manufacturing

- Small-Molecule Injectable Drugs

- Cell & Gene Therapy Manufacturing

- Other Applications (Diagnostics, Nutraceuticals)

By End-User

- Pharmaceutical & Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Research Institutions & Government Organizations

- Hospital Pharmacies & Specialty Compounding Facilities

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.86 B |

| Forecast Revenue (2034) | USD 7.24 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment Type, (Large-Scale Production Freeze Dryers, Pilot & Clinical-Scale Freeze Dryers, Laboratory & Benchtop Freeze Dryers, Automated Loading & Unloading Systems), By Application, (Biologics & Biosimilars Manufacturing, Vaccine Manufacturing, Small-Molecule Injectable Drugs, Cell & Gene Therapy Manufacturing, Other Applications (Diagnostics, Nutraceuticals)), By End-User, (Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Research Institutions & Government Organizations, Hospital Pharmacies & Specialty Compounding Facilities) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IMA LIFE, GETINGE AB (LYOMAX), GEA GROUP, OPTIMA PHARMA, SP INDUSTRIES, MILLROCK TECHNOLOGY, TELSTAR (AZBIL TELSTAR), HOF SONDERANLAGENBAU, LABCONCO CORPORATION, SYNTEGON TECHNOLOGY, SERAIL SAS, TOFFLON SCIENCE AND TECHNOLOGY, VENNIX, LYOPHILIZATION TECHNOLOGY INC. (LTI), BUCHI LABORTECHNIK AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Research Institutes) Industry Trends & Forecast 2026–2034")

, By Application (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Research Institutes) Industry Trends & Forecast 2026–2034")

, By Application (Biologics, Vaccines, Injectable Drugs, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Research Institutes) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Pharmaceutical Lyophilization Equipment Market?

Global Pharma lyophilization equipment market valued at USD 2.58B in 2024, reaching USD 7.24B by 2034, growing at a CAGR of 10.9% from 2026–2034.

Who are the major players in the Pharmaceutical Lyophilization Equipment Market?

IMA LIFE, GETINGE AB (LYOMAX), GEA GROUP, OPTIMA PHARMA, SP INDUSTRIES, MILLROCK TECHNOLOGY, TELSTAR (AZBIL TELSTAR), HOF SONDERANLAGENBAU, LABCONCO CORPORATION, SYNTEGON TECHNOLOGY, SERAIL SAS, TOFFLON SCIENCE AND TECHNOLOGY, VENNIX, LYOPHILIZATION TECHNOLOGY INC. (LTI), BUCHI LABORTECHNIK AG, Others

Which segments covered the Pharmaceutical Lyophilization Equipment Market?

By Equipment Type, (Large-Scale Production Freeze Dryers, Pilot & Clinical-Scale Freeze Dryers, Laboratory & Benchtop Freeze Dryers, Automated Loading & Unloading Systems), By Application, (Biologics & Biosimilars Manufacturing, Vaccine Manufacturing, Small-Molecule Injectable Drugs, Cell & Gene Therapy Manufacturing, Other Applications (Diagnostics, Nutraceuticals)), By End-User, (Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Research Institutions & Government Organizations, Hospital Pharmacies & Specialty Compounding Facilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharmaceutical Lyophilization Equipment Market

Published Date : 01 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date