- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharmaceutical Pricing and Market Size, Share | CAGR 6.2%

Global Pharmaceutical Pricing and Market Size, Share, Analysis By Product (Branded Prescription Drugs, Generic Drugs, Biologics, Biosimilars, Specialty Pharmaceuticals, OTC Drugs, Orphan Drugs, Cell & Gene Therapies), By Molecule Type (Small Molecules, Biologics, RNA-Based Therapeutics, Peptides), By Therapeutic Area (Oncology, Cardiovascular, Neurology, Infectious Diseases, Immunology), By Route of Administration, By Distribution Channel, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 1.77 Trillion | USD 3.03 Trillion | 6.2% | North America, 41.0% |

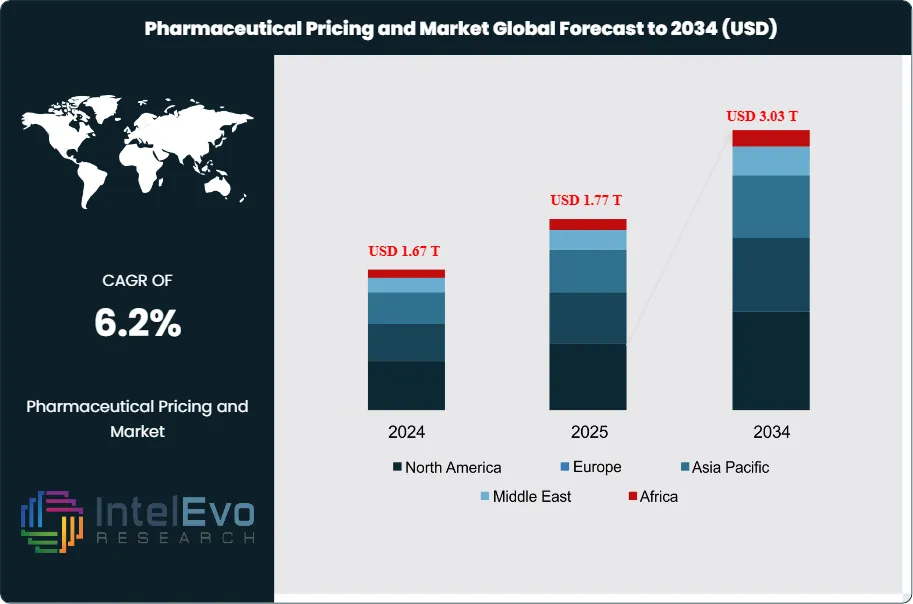

The Pharmaceutical Pricing and Market was valued at approximately USD 1.67 Trillion in 2024 and reached USD 1.77 Trillion in 2025. The market is projected to grow to USD 3.03 Trillion by 2034, expanding at a CAGR of 6.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.26 Trillion over the analysis period. The Pharmaceutical Pricing and Market reflects aggregate global spending on prescription and over-the-counter medicines across branded, generic, biosimilar, and specialty categories, measured at manufacturer invoice prices net of rebates and statutory discounts.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in an aging population, rising chronic disease prevalence, and expanding healthcare access in emerging markets. The International Diabetes Federation reported 89.8 million adults living with diabetes in India alone in 2024, a primary demand pool for the Pharmaceutical Pricing and Market. Eli Lilly's Zepbound and Mounjaro franchise, together with Novo Nordisk's Wegovy, has driven obesity therapeutics toward a projected USD 150 Billion annual run-rate by the early 2030s, with Eli Lilly becoming the first healthcare company to reach a USD 1 trillion market capitalization in November 2025.

Pricing policy has moved decisively toward payer-led constraint. The U.S. Centers for Medicare and Medicaid Services began applying Inflation Reduction Act maximum fair prices on 1 January 2026 for the first ten negotiated drugs, including Eliquis, Jardiance, Xarelto, Januvia, Farxiga, Entresto, Enbrel, Imbruvica, Stelara, and NovoLog, at an average 38% reduction against 2023 list prices. CMS announced the next 15 Part D drugs for 2027 negotiation on 17 January 2025, extending the program to Ozempic and other high-expenditure therapies. Executive Order 14273 of 15 April 2025 directed HHS to propose guidance addressing Most-Favored-Nation pricing and MFN-adjacent mechanisms.

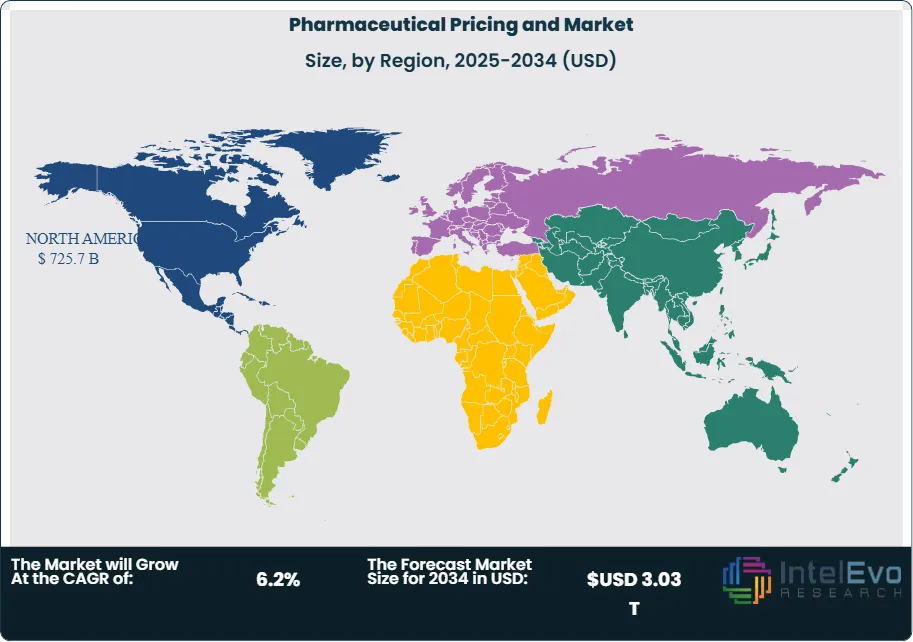

Competitive consolidation accelerated through the second half of 2025. Johnson & Johnson closed the year's largest pharma deal with its USD 14.6 billion acquisition of Intra-Cellular Therapies in January 2025, followed by Novartis's USD 12 billion Avidity Biosciences announcement on 26 October 2025 and Pfizer's completed USD 10 billion Metsera acquisition on 13 November 2025. GlobalData reported a 36.7% quarter-over-quarter increase in pharma M&A deal value in Q3 2025, totaling USD 43.2 billion. North America held 41.0% of global Pharmaceutical Pricing and Market revenue in 2025, with the United States contributing USD 520.38 Billion in 2025 and projected to reach USD 907.86 Billion by 2034 at a 6.34% country CAGR.

Forward visibility to 2034 turns on three dynamics. First, the Medicare Drug Price Negotiation Program expands to 20 new drugs per year from 2029 onward, compressing gross-to-net margins on roughly 19% of Medicare Part D spending. Second, patent cliffs for Entresto, Xolair, Keytruda, and several high-revenue biologics between 2026 and 2030 are driving the GLP-1, ADC, RNA therapeutic, and neuroscience M&A cycle. Third, the EU Joint Clinical Assessment regulation, effective from 12 January 2025, is adding a supranational evidence requirement that increases development costs and delays European launch revenue. These forces together shape the 6.2% CAGR trajectory in the Pharmaceutical Pricing and Market through 2034.

Market Definition & Scope

The Pharmaceutical Pricing and Market is defined as the global commercial space for human medicines, measured at manufacturer invoice prices and inclusive of prescription small-molecule drugs, biologics, biosimilars, monoclonal antibodies, vaccines, and over-the-counter medicines. The market covers innovator branded products, authorized generics, unbranded generics, and biosimilars across oral, parenteral, topical, inhalation, and other routes of administration.

This analysis includes spending by governments, commercial payers, and out-of-pocket consumers across hospital pharmacies, retail pharmacies, online pharmacies, and specialty distribution channels. The scope excludes medical devices, in-vitro diagnostics, contract research and manufacturing services (CDMO revenue of approximately USD 146 Billion in 2023), veterinary pharmaceuticals, nutritional supplements, and pharmaceutical distributor markups captured downstream of manufacturer invoice. Prescription drugs contribute the dominant share of the Pharmaceutical Pricing and Market, with OTC medicines representing a minority share.

, By Molecule Type (Small Molecules, Biologics, RNA-Based Therapeutics, Peptides), By Therapeutic Area (Oncology, Cardiovascular, Neurology, Infectious Diseases, Immunology), By Route of Administration, By Distribution Channel, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Pharmaceutical Pricing and Market grew from USD 1.77 Trillion in 2025 to a projected USD 3.03 Trillion in 2034, expanding at a 6.2% CAGR.

- Segment Dominance (By Product): Branded prescription drugs held 59% revenue share in 2025, led by Keytruda, Eliquis, and the GLP-1 franchise; generics represent the fastest-growing product category through 2034.

- Segment Dominance (By Disease): Oncology therapeutics accounted for 19% of 2024 revenue, anchored by Merck's Keytruda; obesity is projected to be the fastest-growing disease segment through 2030.

- Driver: Global obesity prevalence exceeds 1 billion adults, with Eli Lilly and Novo Nordisk GLP-1 revenues driving Eli Lilly to a USD 1 trillion market cap on 12 November 2025.

- Restraint: IRA maximum fair prices applied to the first ten negotiated drugs from 1 January 2026 reduce 2026 Medicare Part D net spending by USD 2.3 billion, an 8.8% reduction versus the historical benchmark.

- Opportunity: Patent cliffs on Humira, Keytruda, Entresto, and Xolair through 2030 open a USD 180 billion biosimilar and follow-on opportunity, with MSD acquiring Verona Pharma for USD 10 billion to backfill Keytruda exclusivity loss.

- Trend: Contingent Value Rights structured deals rose sharply in 2025, with Pfizer's Metsera acquisition using CVRs of up to USD 22.50 per share tied to clinical and regulatory milestones.

- Regional: North America held 41.0% revenue share in 2025 at USD 725.7 Billion, supported by the United States market of USD 520.38 Billion and 6.34% country CAGR through 2034.

Key Insights Summary

- CMS applied Medicare Drug Price Negotiation Program maximum fair prices to ten Part D drugs from 1 January 2026, with prices averaging 38% below 2023 list prices and projected to reduce 2026 Part D net spending by USD 2.3 billion per published ScienceDirect analysis.

- The first ten IRA-negotiated drugs accounted for approximately USD 46.4 billion, or 19% of Medicare Part D spending in 2022, according to the Medicare Rights Center.

- Johnson & Johnson closed the USD 14.6 billion acquisition of Intra-Cellular Therapies in January 2025 to acquire Caplyta (lumateperone), setting the tone for 2025 pharma M&A.

- Novartis announced a USD 12 billion acquisition of Avidity Biosciences on 26 October 2025, paying USD 72 per share and raising its 2024-2029 sales CAGR guidance from +5% to +6%.

- Pfizer completed the USD 10 billion Metsera acquisition on 13 November 2025 at USD 65.60 per share plus up to USD 20.65 per share in CVR payments tied to clinical and regulatory milestones.

- Eli Lilly became the first healthcare company to reach a USD 1 trillion market capitalization in November 2025, driven by GLP-1 franchise revenue on Zepbound and Mounjaro.

- China's NMPA approved 289 new drug applications in 2025 under expanded Class I review pathways, including a 30-day clinical trial review option introduced by Announcement No. 86 on 14 October 2025.

Competitive Landscape Overview

The Pharmaceutical Pricing and Market is moderately consolidated at the top tier, with the ten largest companies including Johnson & Johnson, Eli Lilly, Pfizer, Novartis, Merck, Roche, AbbVie, AstraZeneca, Bristol-Myers Squibb, and Sanofi accounting for an estimated 42 to 46% of global innovator branded revenue in 2025. Competition is structured around therapeutic-area leadership and late-stage pipeline durability rather than price. Eli Lilly leads in cardiometabolic therapeutics through Zepbound and Mounjaro; Merck dominates oncology with Keytruda; J&J leads neuroscience post-Intra-Cellular.

Consolidation through the 2020s has been driven by patent cliff exposure and a corresponding appetite for late-stage asset acquisition. Of the top ten biopharma M&A deals in 2025, six closed in Q4 2025, with combined top-ten deal value approaching USD 86 billion according to industry M&A trackers. Average acquisition premiums ranged from 60 to 120% over unaffected stock prices, reflecting scarcity of clinical-stage assets with differentiated intellectual property. Contingent Value Rights structures, used in Pfizer's Metsera deal and several 2025 transactions, are becoming a standard mechanism for bridging valuation gaps on clinical-stage pipelines.

| Company | HQ | Position | Key Products | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Johnson & Johnson | New Brunswick, NJ, USA | Leader | Innovative Medicine portfolio; Caplyta | Global | Acquired Intra-Cellular Therapies for USD 14.6 billion in January 2025 |

| Eli Lilly and Company | Indianapolis, IN, USA | Leader | Zepbound; Mounjaro (GLP-1 franchise) | Global | First healthcare company to reach USD 1 trillion market cap in Nov 2025 |

| Pfizer Inc. | New York, NY, USA | Leader | Comirnaty; oncology and internal medicine | Global | Completed USD 10 billion Metsera acquisition on 13 Nov 2025 |

| Novartis AG | Basel, Switzerland | Leader | Kisqali; Entresto; Cosentyx | Global | Announced USD 12 billion Avidity Biosciences acquisition on 26 Oct 2025 |

| Merck & Co., Inc. | Rahway, NJ, USA | Challenger | Keytruda; oncology franchise | Global | Announced USD 10B Verona Pharma and USD 9.2B Cidara deals 2025 |

| Roche Holding AG | Basel, Switzerland | Leader | Ocrevus; Hemlibra; Tecentriq | Global | Continued oncology and neurology pipeline advancement in 2025 |

| AbbVie Inc. | North Chicago, IL, USA | Challenger | Skyrizi; Rinvoq (post-Humira) | Global | Post-Humira growth execution continues through 2025 |

| AstraZeneca plc | Cambridge, United Kingdom | Challenger | Tagrisso; Farxiga; Fasenra | Global | Farxiga subject to IRA negotiation effective Jan 2026 |

| Bristol-Myers Squibb Company | Princeton, NJ, USA | Challenger | Eliquis; Opdivo; Breyanzi | Global | Eliquis among first 10 IRA-negotiated drugs for 2026 |

| Sanofi | Paris, France | Challenger | Dupixent; vaccines | Global | Continued Dupixent label expansion through 2025 |

Segmentation Analysis

The Pharmaceutical Pricing and Market segments across product type, molecule type, therapeutic area, route of administration, and distribution channel. Procurement leaders building a pharmaceutical procurement checklist should benchmark vendors on rebate depth, formulary coverage, 340B eligibility, and manufacturer discount program participation across each segmentation dimension.

By Product

Branded prescription drugs led the Pharmaceutical Pricing and Market with 59% revenue share in 2025, equivalent to approximately USD 1.04 Trillion. This category includes first-in-class innovators such as Eli Lilly's Zepbound, Merck's Keytruda, and J&J's Caplyta, along with legacy franchises such as AbbVie's Humira facing biosimilar competition. Branded products dominate despite a shrinking volume share because gross-to-net pricing averages 60 to 70% of list for innovator therapies, compared with generic net realizations that often fall below 10% of branded list. Generics accounted for 41% of revenue in 2025 and are growing fastest within the product dimension through 2034.

Biosimilars represent a structurally important subsegment within the branded-to-generic transition. Sandoz, Celltrion, Biocon Biologics, and Samsung Bioepis lead this subsegment, with Humira biosimilars such as Cyltezo, Hyrimoz, and Yusimry capturing a meaningful share of the US adalimumab market by 2025. Investors evaluating pharmaceutical pricing ROI calculation models must factor biosimilar erosion timing, as biologics typically retain 50 to 70% of revenue two years after biosimilar entry, compared with small molecule generics that capture only 10 to 20% of pre-generic revenue in the same window.

By Molecule Type

Conventional small-molecule drugs held the largest revenue share in 2024 at approximately 58%, driven by low cost-of-goods, oral administration, and well-established manufacturing under FDA 21 CFR Part 211. Pfizer's Eliquis, AstraZeneca's Farxiga, and Bristol-Myers Squibb's Opdivo illustrate the category's revenue concentration. Small molecules face the Inflation Reduction Act 7-year post-approval negotiation window, compared with biologics at 11 years, creating a structural disadvantage that the proposed EPIC Act seeks to equalize.

Biologics and biosimilars represented approximately 42% of molecule-level revenue in 2024 and are growing at higher single-digit CAGR through 2034. Monoclonal antibodies, antibody-drug conjugates, and antibody-oligonucleotide conjugates each contribute to this trajectory. Novartis's October 2025 Avidity Biosciences acquisition, at USD 12 billion, secured access to AOC platform technology for neuromuscular diseases. Conventional drugs remain the fastest-growing molecule segment in unit volume terms because of generic availability and oral administration.

By Therapeutic Area

Oncology led therapeutic-area revenue at approximately USD 217 Billion in 2025, anchored by Merck's Keytruda, Roche's Hemlibra and Tecentriq, Bristol-Myers Squibb's Opdivo, and AstraZeneca's Tagrisso. Cardiometabolic and diabetes therapeutics contributed approximately USD 175 Billion in 2025, with GLP-1 receptor agonists from Eli Lilly and Novo Nordisk driving category growth. Immunology accounted for approximately USD 140 Billion, anchored by AbbVie's Skyrizi and Rinvoq. Neuroscience, at approximately USD 95 Billion, is positioned for accelerated growth following J&J's Intra-Cellular and Novartis's Avidity acquisitions.

Obesity is the fastest-growing disease subsegment, projected to reach USD 150 Billion annual revenue by the early 2030s per Reports and Data analysis cited in BioSpace reporting. Vaccine revenue, excluding the one-time COVID-19 surge, contributed approximately USD 50 Billion in 2025. Rare disease and orphan drug categories together represented approximately USD 120 Billion, with NICE's 2025 approval of exa-cel at GBP 1.65 million per course illustrating the pricing premium the category commands in developed markets.

By Distribution Channel

Hospital pharmacies dominated with 54% revenue share in 2024, reflecting the channel's dominance in specialty and biologic drug dispensing. Retail pharmacies are the fastest-growing channel through 2034, propelled by online pharmacy expansion and the pharmacy benefit manager direct-to-patient mail order model. Specialty distribution channels managed by Cardinal Health, AmerisourceBergen, and McKesson capture the majority of specialty pharmacy dispensing. Pharmaceutical pricing benchmarks for outpatient infusion indicate that J-coded drugs reimbursed under Medicare Part B carry a 6% administrative markup over average sales price, a mechanism the IRA begins modifying in 2028.

By Route of Administration

Oral administration held 58% revenue share in 2024, leveraging patient-compliance economics and retail pharmacy distribution efficiency. Parenteral administration is growing fastest within the route dimension, propelled by monoclonal antibodies, GLP-1 injectables, and gene therapies such as exa-cel. Inhalation and topical routes account for mid-single-digit shares each. The shift toward parenteral administration creates incremental demand for pharmaceutical filtration infrastructure, the parent market for which reached USD 12.83 Billion in 2023 and is growing at an 8.08% CAGR through 2033.

Regional Analysis

The Pharmaceutical Pricing and Market divides across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with North America leading in 2025 and Asia Pacific growing fastest through 2034.

North America

North America held 41.0% of global Pharmaceutical Pricing and Market revenue in 2025, equivalent to USD 725.7 Billion. The United States accounted for USD 520.38 Billion, Canada for approximately USD 35 Billion, and Mexico for approximately USD 22 Billion. FDA approval pathways including Breakthrough Therapy Designation, Accelerated Approval, and Priority Review support rapid commercialization. The Inflation Reduction Act's Medicare Drug Price Negotiation Program, CMS Transparency in Coverage rules, and Executive Order 14273 of 15 April 2025 are reshaping commercial pricing. Canada's Patented Medicine Prices Review Board applies reference-pricing against an international basket of comparator countries.

Europe

Europe held 27.5% share in 2025 at approximately USD 486.8 Billion, with Germany, France, Italy, Spain, and the United Kingdom leading consumption. The EU Joint Clinical Assessment regulation became effective on 12 January 2025, introducing a supranational evidence requirement for oncology and ATMP products. AIFA's updated HTA guidelines take effect 1 April 2026 in Italy. Germany's AMNOG price-negotiation framework and the UK's National Institute for Health and Care Excellence continue to anchor European pricing benchmarks. NICE approved exa-cel at GBP 1.65 million per course in 2025 for sickle-cell disease and beta-thalassaemia, illustrating the pricing ceiling for curative gene therapies in Europe.

Asia Pacific

Asia Pacific captured 22.0% share in 2025 at approximately USD 389.4 Billion and is growing fastest at 7.0% CAGR through 2034. China, Japan, South Korea, India, and Australia are the primary demand centers. China's NMPA approved 289 new drug applications in 2025, a record level, under the Announcement No. 86 30-day clinical trial review pathway effective 14 October 2025. Announcement No. 96 of 28 November 2025 enables import of pre-approval commercial-scale batches of overseas-marketed drugs. Japan's PMDA Sakigake designation continues to fast-track breakthrough therapies, while India's Ayushman Bharat scheme expands public insurance coverage for branded medicines.

Latin America

Latin America held 5.5% share in 2025 at approximately USD 97.4 Billion, led by Brazil, Mexico, and Argentina. Brazil's ANVISA has harmonized with FDA and ICH guidelines for biosimilar evaluation, enabling faster market entry for follow-on biologics. Mexico's COFEPRIS has expedited priority review for oncology and rare disease therapeutics through 2025. Regional growth is constrained by foreign-exchange volatility and public-system reimbursement gaps, though private-pay specialty markets continue to expand in Sao Paulo, Rio de Janeiro, and Mexico City.

Middle East & Africa

The Middle East & Africa region held 4.0% share in 2025 at approximately USD 70.8 Billion. Saudi Arabia, the United Arab Emirates, and South Africa are the largest contributors. Saudi Arabia's Vision 2030 healthcare reforms and the Saudi Food and Drug Authority's 2025 pricing transparency initiative are expanding market access for specialty therapies. The UAE Ministry of Health and Prevention granted fast-track review in 2025 for multiple oncology combination products. South Africa's SAHPRA oversees a Section 21 pathway for compassionate access to unregistered medicines, supporting a 6.2% regional CAGR projection through 2034.

United States

The United States generated USD 520.38 Billion in Pharmaceutical Pricing and Market revenue in 2025 and is projected to reach USD 907.86 Billion by 2034, growing at a country CAGR of 6.34%. The Inflation Reduction Act applied the first ten negotiated drug prices effective 1 January 2026, averaging 38% below 2023 list prices. CMS selected 15 additional Part D drugs on 17 January 2025 for 2027 negotiation, including Ozempic. Executive Order 14273 of 15 April 2025 directed HHS to propose MFN-adjacent guidance. The FDA, operating under the Prescription Drug User Fee Act Reauthorization (PDUFA VII), approved over 70 novel drugs in 2025. Medicare Part B and Part D together cover approximately 54.1 million beneficiaries, the largest single-payer book in the market.

Country Analysis

The Pharmaceutical Pricing and Market concentrates in four national markets that together contribute more than 55% of 2025 global revenue: the United States, China, Japan, and Germany.

China

China contributed approximately USD 195 Billion in Pharmaceutical Pricing and Market revenue in 2025, growing at a country CAGR of 8.1% through 2034. NMPA approved 289 new drug applications in 2025, including chemical drugs, biological products, and traditional Chinese medicines, under the accelerated 30-day review pathway introduced by Announcement No. 86. China's Volume-Based Procurement program continues to compress generic and biosimilar prices by 40 to 70% through national tendering cycles. The National Healthcare Security Administration's 2025 Essential Drug List update added multiple oncology and rare disease therapies with negotiated ceiling prices. Domestic innovators such as BeiGene, Innovent Biologics, and Jiangsu Hengrui are scaling cross-border licensing deals with Western partners.

Japan

Japan generated approximately USD 100 Billion in Pharmaceutical Pricing and Market revenue in 2025, with a projected country CAGR of 4.0% through 2034. The Pharmaceuticals and Medical Devices Agency applies biennial National Health Insurance price revisions that typically reduce listed prices by 4 to 8%. Japan's 2025 revision expanded the foreign-average-price adjustment mechanism and tightened reference-basket calculations against the United States, United Kingdom, Germany, and France. Takeda Pharmaceutical, Daiichi Sankyo, and Astellas Pharma lead domestic innovation, while the aging population, with 29% of citizens over age 65 in 2025, sustains long-term demand for chronic disease medicines.

Germany

Germany accounted for approximately USD 75 Billion in Pharmaceutical Pricing and Market revenue in 2025, with a projected country CAGR of 4.5% through 2034. The AMNOG (Pharmaceutical Market Reorganization Act) framework operated by the Gemeinsamer Bundesausschuss sets reference prices for new therapies following early benefit assessment. The German Institute for Quality and Efficiency in Health Care (IQWiG) conducts the Phase 1 benefit assessment on which AMNOG negotiations rest. Germany's statutory health insurance system covers approximately 73 million beneficiaries, supporting robust oncology and rare disease demand. Bayer, Boehringer Ingelheim, and Merck KGaA headquartered innovators maintain domestic commercial infrastructure, while the country's export profile ranks among the top five globally.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product

- Branded Prescription Drugs

- Generic Drugs

- Biologics

- Biosimilars

- Specialty Pharmaceuticals

- Over-the-Counter (OTC) Drugs

- Orphan Drugs

- Cell & Gene Therapies

By Molecule Type

- Small Molecules

- Biologics

- Monoclonal Antibodies (mAbs)

- Recombinant Proteins

- Vaccines

- Biosimilars

- Cell Therapies

- Gene Therapies

- RNA-Based Therapeutics

- Peptide-Based Therapeutics

By Therapeutic Area

- Oncology

- Cardiovascular Diseases

- Neurology

- Infectious Diseases

- Immunology & Autoimmune Disorders

- Endocrinology & Metabolic Disorders

- Respiratory Diseases

- Gastrointestinal Disorders

- Rare Diseases

- Hematology

- Dermatology

- Ophthalmology

- Others

By Route of Administration

- Oral

- Injectable

- Intravenous (IV)

- Subcutaneous (SC)

- Intramuscular (IM)

- Topical

- Inhalation

- Nasal

- Transdermal

- Ophthalmic

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies / E-Pharmacies

- Specialty Pharmacies

- Drug Wholesalers & Distributors

- Government Procurement Programs

- Direct-to-Hospital / Institutional Sales

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.77 T |

| Forecast Revenue (2034) | USD 3.03 T |

| CAGR (2025-2034) | 6.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Branded Prescription Drugs, Generic Drugs, Biologics, Biosimilars, Specialty Pharmaceuticals, Over-the-Counter (OTC) Drugs, Orphan Drugs, Cell & Gene Therapies), By Molecule Type, (Small Molecules, Biologics, Biosimilars, Cell Therapies, Gene Therapies, RNA-Based Therapeutics, Peptide-Based Therapeutics), By Therapeutic Area, (Oncology, Cardiovascular Diseases, Neurology, Infectious Diseases, Immunology & Autoimmune Disorders, Endocrinology & Metabolic Disorders, Respiratory Diseases, Gastrointestinal Disorders, Rare Diseases, Hematology, Dermatology, Ophthalmology, Others), By Route of Administration, (Oral, Injectable, Topical, Inhalation, Nasal, Transdermal, Ophthalmic, Others), By Distribution Channel, (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies / E-Pharmacies, Specialty Pharmacies, Drug Wholesalers & Distributors, Government Procurement Programs, Direct-to-Hospital / Institutional Sales, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | JOHNSON & JOHNSON, ELI LILLY AND COMPANY, PFIZER INC., NOVARTIS AG, MERCK & CO., INC., F. HOFFMANN-LA ROCHE LTD, ABBVIE INC., ASTRAZENECA PLC, BRISTOL-MYERS SQUIBB COMPANY, SANOFI, NOVO NORDISK A/S, GLAXOSMITHKLINE PLC, TAKEDA PHARMACEUTICAL COMPANY LIMITED, AMGEN INC., GILEAD SCIENCES, INC., BAYER AG, BOEHRINGER INGELHEIM GMBH, TEVA PHARMACEUTICAL INDUSTRIES LTD., VIATRIS INC., BIOGEN INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Molecule Type (Small Molecules, Biologics, RNA-Based Therapeutics, Peptides), By Therapeutic Area (Oncology, Cardiovascular, Neurology, Infectious Diseases, Immunology), By Route of Administration, By Distribution Channel, Industry Trends & Forecast 2026-2034")

, By Molecule Type (Small Molecules, Biologics, RNA-Based Therapeutics, Peptides), By Therapeutic Area (Oncology, Cardiovascular, Neurology, Infectious Diseases, Immunology), By Route of Administration, By Distribution Channel, Industry Trends & Forecast 2026-2034")

, By Molecule Type (Small Molecules, Biologics, RNA-Based Therapeutics, Peptides), By Therapeutic Area (Oncology, Cardiovascular, Neurology, Infectious Diseases, Immunology), By Route of Administration, By Distribution Channel, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Pharmaceutical Pricing and Market?

The Global Pharmaceutical Pricing and Market was valued at USD 1.67 Trillion in 2024 and is projected to reach USD 3.03 Trillion by 2034, growing at a CAGR of 6.2% from 2026 to 2034. Growth is driven by increasing demand for innovative drugs, specialty pharmaceuticals, biologics, biosimilars, precision medicine, rising chronic disease prevalence, expanding healthcare access, evolving reimbursement models, and growing pharmaceutical R&D investments across global healthcare markets.

Who are the major players in the Pharmaceutical Pricing and Market?

JOHNSON & JOHNSON, ELI LILLY AND COMPANY, PFIZER INC., NOVARTIS AG, MERCK & CO., INC., F. HOFFMANN-LA ROCHE LTD, ABBVIE INC., ASTRAZENECA PLC, BRISTOL-MYERS SQUIBB COMPANY, SANOFI, NOVO NORDISK A/S, GLAXOSMITHKLINE PLC, TAKEDA PHARMACEUTICAL COMPANY LIMITED, AMGEN INC., GILEAD SCIENCES, INC., BAYER AG, BOEHRINGER INGELHEIM GMBH, TEVA PHARMACEUTICAL INDUSTRIES LTD., VIATRIS INC., BIOGEN INC., Others

Which segments covered the Pharmaceutical Pricing and Market?

By Product, (Branded Prescription Drugs, Generic Drugs, Biologics, Biosimilars, Specialty Pharmaceuticals, Over-the-Counter (OTC) Drugs, Orphan Drugs, Cell & Gene Therapies), By Molecule Type, (Small Molecules, Biologics, Biosimilars, Cell Therapies, Gene Therapies, RNA-Based Therapeutics, Peptide-Based Therapeutics), By Therapeutic Area, (Oncology, Cardiovascular Diseases, Neurology, Infectious Diseases, Immunology & Autoimmune Disorders, Endocrinology & Metabolic Disorders, Respiratory Diseases, Gastrointestinal Disorders, Rare Diseases, Hematology, Dermatology, Ophthalmology, Others), By Route of Administration, (Oral, Injectable, Topical, Inhalation, Nasal, Transdermal, Ophthalmic, Others), By Distribution Channel, (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies / E-Pharmacies, Specialty Pharmacies, Drug Wholesalers & Distributors, Government Procurement Programs, Direct-to-Hospital / Institutional Sales, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharmaceutical Pricing and Market

Published Date : 04 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date