- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Pharmacovigilance Software Market Size, Share & Forecast | CAGR 12.2%

Global Pharmacovigilance Software Market Size, Share, Growth Analysis By Component (Software, Implementation & Consulting Services, Support & Maintenance), By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Firms, CROs, Healthcare Providers), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 1.82 Billion | USD 5.11 Billion | 12.2% | North America, 38.5% |

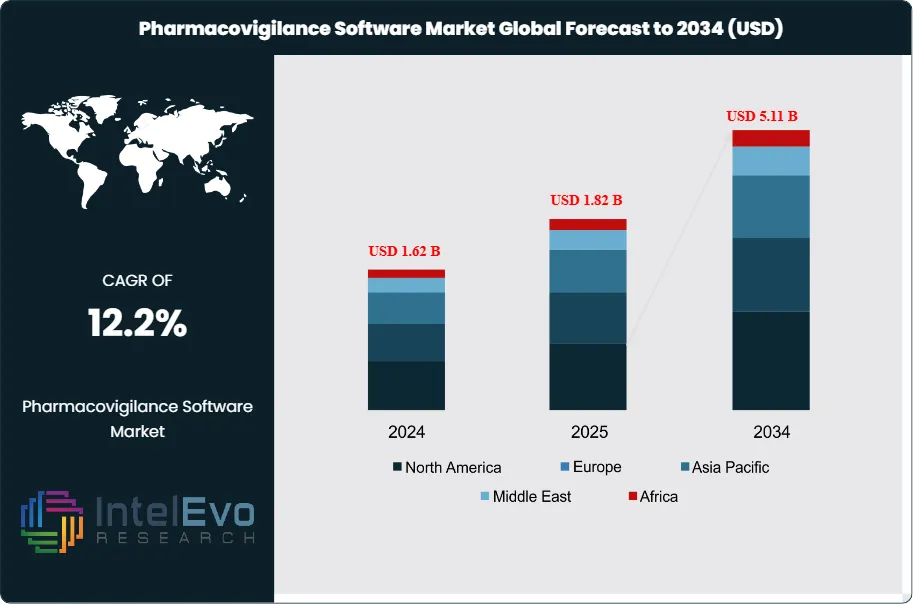

The Pharmacovigilance Software Market was valued at approximately USD 1.62 Billion in 2024 and reached USD 1.82 Billion in 2025. The market is projected to grow to USD 5.11 Billion by 2034, expanding at a CAGR of 12.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.29 Billion over the analysis period, driven by intensifying regulatory requirements, rapid digitalization of drug safety operations, and rising adverse event reporting volumes worldwide.

Get More Information about this report -

Request Free Sample ReportThe pharmacovigilance software market sits at the intersection of life sciences compliance, clinical data management, and enterprise software. Regulatory authorities including the FDA, EMA, and Japan's PMDA have progressively expanded mandatory Individual Case Safety Report (ICSR) submission requirements under ICH E2B(R3) standards, compelling pharmaceutical companies, biotechnology firms, contract research organizations, and medical device manufacturers to invest in robust, scalable software infrastructure. The transition from paper-based and legacy systems toward integrated cloud-native platforms marks the defining structural shift in the pharmacovigilance software market between 2025 and 2034.

Demand-side forces are concentrated among large pharmaceutical manufacturers, which account for approximately 44.2% of total market revenue in 2025. These companies process hundreds of thousands of case reports annually and require enterprise-grade solutions with multi-jurisdiction regulatory mapping, AI-assisted signal detection, and real-time aggregate reporting capabilities. Supply-side dynamics reflect intense product development competition, with vendors differentiating on the depth of their natural language processing (NLP) capabilities, the breadth of regulatory submissions coverage, and the speed of case processing automation.

Regulatory influences are accelerating market growth. The FDA's 2025 guidance on electronic submission of pharmacovigilance data and the EMA's continuous push toward real-world evidence integration have materially increased IT spend among pharmaceutical companies operating in regulated markets. The EU Pharmacovigilance Legislation (Directive 2010/84/EU and Regulation (EU) No 1235/2010) requires periodic safety update reports, risk management plans, and PSUR submissions through the EMA's eXeVaMP portal, all of which demand sophisticated software infrastructure.

Technology effects are bifurcating the competitive field. AI-driven automation, particularly in adverse event narrative writing, duplicate case detection, and automated medical coding, is compressing the labor content of core PV operations. Vendors embedding large language model (LLM)-based automation into their platforms are capturing premium pricing, while legacy on-premise solutions face displacement. Cloud deployment now represents 58.3% of all new pharmacovigilance software deployments in 2025, up from under 30% in 2020, reflecting infrastructure modernization across the pharmaceutical industry. North America leads total revenue at 38.5% share in 2025, while Asia Pacific is the fastest-growing region as Indian and Chinese pharmaceutical companies expand their global regulatory compliance programs. The pharmacovigilance software market is positioned for sustained double-digit expansion through 2034 as post-market surveillance obligations widen globally.

, By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Firms, CROs, Healthcare Providers), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global pharmacovigilance software market was valued at USD 1.82 Billion in 2025 and is projected to reach USD 5.11 Billion by 2034, registering a CAGR of 12.2% during the forecast period 2026–2034.

- Segment Dominance: By Component, the Software segment leads with a 68.4% revenue share in 2025, reflecting sustained enterprise investment in core PV platforms over services-only engagements.

- Segment Dominance: By Functionality, the Case Management segment holds the largest share at 34.7% in 2025, driven by high case volumes and mandatory ICSR submission timelines under FDA and EMA regulations.

- Driver: Expanding global adverse event reporting mandates, particularly ICH E2B(R3) adoption across 50+ countries, are compelling pharmaceutical companies to replace legacy systems, driving annual platform upgrade spending above USD 620 Million in 2025.

- Restraint: High implementation costs and data migration complexity associated with transitioning from legacy pharmacovigilance systems constrain adoption among small and mid-size pharmaceutical companies, limiting penetration to approximately 41% of potential SME customers in 2025.

- Opportunity: Integration of real-world evidence (RWE) and electronic health record (EHR) data into pharmacovigilance workflows presents an addressable expansion opportunity worth USD 1.1 Billion by 2034, as regulators increasingly accept RWE in benefit-risk assessments.

- Trend: AI-powered case automation and NLP-based narrative generation are advancing from pilot projects to production deployments across 38% of top-100 pharmaceutical companies by 2025, with adoption projected to reach 72% by 2030.

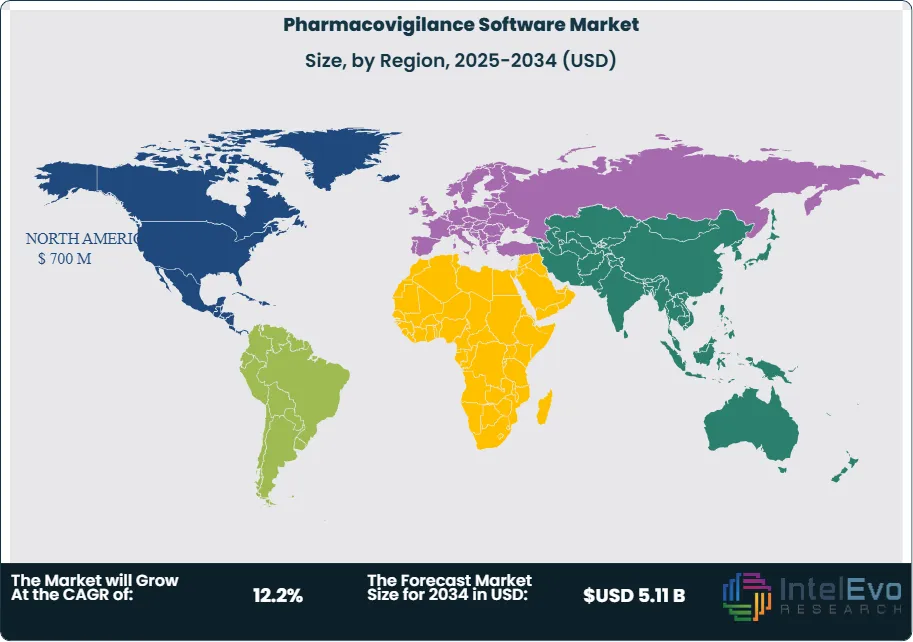

- Regional Analysis: North America leads the pharmacovigilance software market with a 38.5% revenue share in 2025, equivalent to USD 700 Million, supported by the FDA's comprehensive adverse event reporting framework and the highest density of FDA-registered pharmaceutical manufacturers globally.

Competitive Landscape Overview

The pharmacovigilance software market is moderately consolidated, with the top four vendors — Oracle Health Sciences, Veeva Systems, ArisGlobal, and IQVIA Holdings — collectively holding approximately 58% of global revenue in 2025. Competition centers on regulatory breadth, AI automation depth, and cloud infrastructure quality rather than price alone. Market dynamics have intensified with the entry of AI-native startups challenging legacy platform vendors on case processing speed and cost per case metrics. Strategic acquisitions and cloud migration partnerships accelerated through 2024–2026 as vendors raced to deliver integrated PV-to-regulatory submission workflows. The barriers to entry are high due to the extensive regulatory certification and validation requirements governing pharmacovigilance software under FDA 21 CFR Part 11 and EMA Good Pharmacovigilance Practices.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Oracle Health Sciences | USA | Leader | Oracle Argus Safety | North America, Europe | Launched Argus Safety Cloud 9.2 with AI-driven signal detection enhancements, Jan 2026 |

| Veeva Systems | USA | Leader | Veeva Vault Safety | North America, Europe | Acquired Crossix patient data network to deepen real-world evidence capabilities, Sep 2025 |

| ArisGlobal | USA | Leader | LifeSphere Safety | North America, Asia Pacific | Released LifeSphere AI v5 featuring automated case processing and SUSAR automation, Mar 2025 |

| IQVIA Holdings | USA | Leader | UNIFYGlobal | Global | Expanded UNIFYGlobal to cover post-market surveillance in 45+ countries, Jun 2025 |

| Cognizant | USA | Challenger | SafetyPilot PV | North America, Europe | Partnered with AWS to deploy SafetyPilot on cloud infrastructure for mid-size pharma, Dec 2024 |

| Wipro | India | Challenger | Wipro PharmaLife Safety | Asia Pacific, Europe | Launched multilingual PV reporting module covering 30 ICH-regulated markets, Apr 2025 |

| Tata Consultancy Services | India | Challenger | TCS BaNCS Safety | Asia Pacific, North America | Won five-year PV outsourcing contract with a top-10 global pharma company, Oct 2025 |

| PAREXEL International | USA | Niche Player | PAREXEL Pharmacovigilance Suite | Global | Opened dedicated PV center of excellence in Warsaw serving EU regulatory submissions, Aug 2025 |

| Advera Health Analytics | USA | Niche Player | VigiSearch AI | North America | Integrated FDA FAERS and EMA EudraVigilance feeds into real-time signal scoring engine, Feb 2026 |

| Ennov | France | Niche Player | Ennov Clinical Safety | Europe | Achieved EMA remote access compliance certification for its cloud PV platform, Nov 2025 |

By Component

The pharmacovigilance software market by component is divided into Software and Services. The Software segment dominates with a 68.4% revenue share in 2025, equivalent to USD 1.245 Billion. This reflects persistent enterprise preference for integrated platform ownership over managed services contracts, particularly among large pharmaceutical companies that require tight control over adverse event data governance and regulatory submission timelines. Core software categories include case management systems, signal detection engines, aggregate reporting platforms, and risk management modules. The Software segment is projected to grow at a CAGR of 12.9% through 2034, outpacing overall market growth, as AI-native platform upgrades drive average contract values higher. The Services segment, comprising implementation, support and maintenance, and strategic consulting, represents 31.6% of market revenue in 2025 or USD 575 Million. Service intensity is highest in the first 12–18 months post-deployment, during which vendors provide regulatory validation support, data migration, and user training. Growth in the Services segment is closely correlated with new software deployments, and the segment will benefit from expanded PV outsourcing by mid-size pharmaceutical companies that lack in-house PV technology teams.

By Deployment Mode

Cloud-Based deployment commands 58.3% of the pharmacovigilance software market in 2025, valued at USD 1.061 Billion, and is advancing rapidly as pharmaceutical companies prioritize infrastructure flexibility, automatic regulatory update propagation, and global multi-site access. Cloud platforms reduce the burden of system validation requalification after software updates — a time-consuming requirement under FDA 21 CFR Part 11 — because vendors manage the validation cycle and provide pre-qualified release packages. The Cloud-Based segment is growing at a CAGR of 14.1% during 2025–2034, the fastest rate of any sub-segment. Amazon Web Services, Microsoft Azure, and Google Cloud serve as the primary infrastructure providers, with HIPAA BAA agreements and ISO 27001 certifications forming baseline requirements. On-Premise deployment retains a 41.7% share in 2025 or USD 759 Million, concentrated among established Big Pharma companies and regulatory-conservative markets including Japan and China. Migration from On-Premise to Cloud is the dominant infrastructure trend shaping competitive dynamics, with an estimated 22% of On-Premise installations expected to migrate to hybrid or full-cloud configurations between 2025 and 2029.

By Functionality

Case Management leads functionality segmentation with a 34.7% share of the pharmacovigilance software market in 2025, generating USD 631 Million. Case Management systems process ICSRs from clinical trials, post-market sources, spontaneous reports, and literature, and must comply with FDA Form 3500A, EMA CIOMS I, and ICH E2B(R3) data element requirements. High volumes — large pharmaceutical companies process 200,000 to 1,000,000+ cases annually — make automation within this segment critical and command premium software licensing fees. Signal Detection and Management holds 21.8% share in 2025 (USD 397 Million), driven by the FDA's Sentinel System initiative and EMA's requirement for continuous benefit-risk evaluation under GVP Module IX. Signal detection capabilities incorporating disproportionality analysis, Bayesian statistical methods, and AI-assisted clustering are replacing manual pharmacovigilance review. Risk Management accounts for 16.2% (USD 295 Million), encompassing Risk Evaluation and Mitigation Strategies (REMS) in the US and Risk Management Plans (RMPs) in Europe. Regulatory Reporting holds 15.4% (USD 280 Million), covering periodic safety update reports, development safety update reports, and eMDR submissions. Analytics and Reporting represents the remaining 11.9% (USD 217 Million), with growth accelerating as companies adopt real-world evidence dashboards and executive-level safety intelligence tools.

By End User

Pharmaceutical Companies are the primary end-user segment with a 44.2% revenue share in 2025 (USD 804 Million), driven by their mandatory obligation to operate pharmacovigilance systems as a condition of drug approval and marketing authorization in all major jurisdictions. Global pharmaceutical revenue exceeding USD 1.5 Trillion in 2025 is accompanied by increasing adverse event volumes as more complex therapies enter post-market surveillance. Biotechnology Companies represent 22.6% (USD 411 Million) and are the fastest-growing end-user segment given the surge in novel biologics, cell and gene therapies, and mRNA products requiring extensive post-approval safety monitoring under FDA CBER oversight. Contract Research Organizations (CROs) account for 16.8% (USD 306 Million), as outsourcing of pharmacovigilance operations grows at approximately 9% per year — faster than in-house operations — creating sustained demand for multi-sponsor PV software platforms. Medical Device Manufacturers represent 9.7% (USD 176 Million), a segment expanding due to EU MDR (Medical Device Regulation 2017/745) and FDA UDI mandates requiring post-market surveillance reports, adverse event reporting through MedWatch, and field safety corrective actions. Healthcare Providers account for the remaining 6.7% (USD 122 Million), with growth driven by hospital pharmacovigilance units and academic medical centers expanding spontaneous reporting programs.

Regional Analysis

North America

North America holds the largest share of the pharmacovigilance software market at 38.5% in 2025, corresponding to USD 700 Million in annual revenue. The United States accounts for approximately 87% of regional revenue, underpinned by the FDA's comprehensive post-market drug safety architecture, which includes MedWatch, the Adverse Event Reporting System (FAERS), and the Sentinel System — a national electronic surveillance network monitoring the safety of FDA-regulated medical products in over 200 million patients' records. The FDA's expedited 15-day ICSR reporting requirement for serious unexpected adverse reactions creates continuous software demand for real-time case processing capabilities. Canada contributes approximately 8% of North American revenue, with Health Canada's Vigilance Adverse Reaction database operating under its own ICSR submission framework aligned with ICH E2B(R3). The United States hosts the highest global concentration of FDA-registered pharmaceutical manufacturers, with over 2,000 active domestic establishments and more than 3,000 foreign establishments supplying the US market. Investment in AI-powered PV automation by US-headquartered pharmaceutical companies is generating premium software contract values averaging USD 2.3 Million annually per large enterprise client in 2025. Government programs, including NIH-funded pharmacogenomics research and CMS post-market requirements for Medicare Part D drugs, are further expanding the scope of adverse event data that must be monitored through pharmacovigilance software.

Europe

Europe represents 27.4% of the global pharmacovigilance software market in 2025, valued at USD 499 Million. The regulatory framework is anchored by the EMA and governed by EU Pharmacovigilance Legislation (Regulation 726/2004 as amended, Directive 2010/84/EU), which mandates centrally authorized product holders to maintain pharmacovigilance systems, submit PSURs, and participate in the EMA's EudraVigilance electronic adverse reaction database. Germany is the largest national market, contributing approximately 22% of European revenue, supported by its high density of pharmaceutical manufacturers and the German Federal Institute for Drugs and Medical Devices (BfArM), which requires national ICSR submissions in addition to EMA filings. France accounts for 18% of European revenue, driven by ANSM oversight and France's role as home to Sanofi, one of the world's largest pharmaceutical companies by PV data volume. The United Kingdom, post-Brexit, operates its own Yellow Card pharmacovigilance system under the MHRA, creating a distinct national submission requirement that adds compliance complexity and software licensing demand for UK-operating companies. Switzerland contributes approximately 9% of European revenue, reflecting the headquarters concentration of Roche and Novartis, which operate some of the world's largest in-house PV infrastructure investments. The EU AI Act, applicable from 2025, is beginning to shape how AI components within pharmacovigilance software are validated and documented, adding a new layer of regulatory compliance demand.

Asia Pacific

Asia Pacific accounts for 21.8% of the global pharmacovigilance software market in 2025, equivalent to USD 397 Million, and is the fastest-growing region with a projected CAGR of 14.8% during 2025–2034. China leads regional revenue with approximately 31% share, driven by National Medical Products Administration (NMPA) reforms that have aligned Chinese adverse drug reaction reporting requirements progressively closer to ICH standards, compelling domestic and international pharmaceutical companies to upgrade their PV systems for China-specific submissions. Japan represents 28% of Asia Pacific revenue, supported by PMDA oversight and Japan's deep pharmaceutical market. Japanese pharmaceutical companies including Takeda, Astellas, and Daiichi Sankyo operate sophisticated global PV systems requiring multi-language case management. India accounts for 22% of regional revenue, with growth driven by the expansion of India's CDSCO-supervised PV program and the country's role as a major clinical trial hub and generic pharmaceutical exporter — both of which generate extensive adverse event data requiring structured software management. South Korea contributes 11% of regional revenue, supported by MFDS enforcement of expanded PV obligations and Korea's growing biosimilar export sector requiring global PV compliance. Government investment in digital health infrastructure across Southeast Asia is opening new market entry opportunities for regional and global PV software vendors between 2025 and 2034.

Latin America

Latin America holds a 7.8% share of the pharmacovigilance software market in 2025, valued at USD 142 Million. Brazil is the dominant national market, representing approximately 47% of regional revenue, driven by ANVISA's (National Health Surveillance Agency) structured pharmacovigilance requirements for marketing authorization holders, which mandate adverse event monitoring, PSUR submissions, and risk management plans for approved products. Brazil is one of the few Latin American markets with a developed national spontaneous reporting system (Notivisa), supporting structured ICSR data that benefits from software automation. Mexico accounts for approximately 23% of regional revenue, with COFEPRIS strengthening post-market surveillance requirements in line with its ongoing alignment to ICH Technical Guidelines. Argentina contributes 15% of regional revenue, supported by ANMAT's pharmacovigilance regulations and the concentration of regional pharmaceutical manufacturing. The broader Latin American market remains significantly underpenetrated relative to its pharmaceutical sector size, as fragmented regulatory harmonization and IT budget constraints at mid-size local pharmaceutical manufacturers limit software adoption. The Pan American Health Organization's efforts to harmonize pharmacovigilance standards across the region represent a structural medium-term growth catalyst.

Middle East and Africa

The Middle East and Africa region accounts for 4.5% of the global pharmacovigilance software market in 2025, generating USD 82 Million in annual revenue. The United Arab Emirates leads regional revenue with approximately 36% share, driven by the Dubai Health Authority and Abu Dhabi Department of Health's growing pharmacovigilance program requirements and UAE's strategic position as a pharmaceutical distribution hub for the broader GCC and MENA markets. Saudi Arabia accounts for approximately 29% of MEA revenue, supported by the Saudi Food and Drug Authority's (SFDA) mandatory adverse event reporting system and the Kingdom's Vision 2030 healthcare investment program, which is driving significant pharmaceutical industry modernization. South Africa represents approximately 21% of MEA revenue, anchored by the South African Health Products Regulatory Authority (SAHPRA) and the country's role as Africa's most developed pharmaceutical regulatory market. The broader Africa region is an early-stage market where international pharmaceutical companies operating in 30+ African countries face increasing pressure from the African Medicines Regulatory Harmonization (AMRH) initiative to implement consistent PV systems across their regional operations. GCC health authorities' adoption of the ICH E2B(R3) standard from 2024 is accelerating software upgrade demand in Saudi Arabia and UAE specifically.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software

- Services (Implementation, Support & Maintenance, Consulting)

By Deployment

- Cloud-Based

- On-Premise

By Functionality

- Case Management

- Signal Detection & Management

- Risk Management

- Regulatory Reporting

- Analytics & Reporting

By End User

- Pharmaceutical Companies

- Biotechnology Companies

- Medical Device Manufacturers

- Contract Research Organizations (CROs)

- Healthcare Providers

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.82 B |

| Forecast Revenue (2034) | USD 5.11 B |

| CAGR (2025-2034) | 12.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Software, Services (Implementation, Support & Maintenance, Consulting)), By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection & Management, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations (CROs), Healthcare Providers), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ORACLE HEALTH SCIENCES, VEEVA SYSTEMS, ARISGLOBAL, IQVIA HOLDINGS, COGNIZANT, WIPRO, TATA CONSULTANCY SERVICES, PAREXEL INTERNATIONAL, ADVERA HEALTH ANALYTICS, ENNOV, SYMPLR (FORMERLY HEALTHSTREAM SAFETY), SPARTA SYSTEMS (A HONEYWELL COMPANY), RELSYS, SAMARTH LIFE SCIENCES, ALLIANCE LIFE SCIENCES CONSULTING, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Firms, CROs, Healthcare Providers), Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Firms, CROs, Healthcare Providers), Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Firms, CROs, Healthcare Providers), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Pharmacovigilance Software Market?

The Global Pharmacovigilance Software Market was valued at USD 1.62 Billion in 2024 and is projected to reach USD 5.11 Billion by 2034, growing at a CAGR of 12.2% from 2026 to 2034, driven by rising adverse event reporting requirements, increasing drug safety regulations, and growing adoption of AI-powered pharmacovigilance solutions.

Who are the major players in the Pharmacovigilance Software Market?

ORACLE HEALTH SCIENCES, VEEVA SYSTEMS, ARISGLOBAL, IQVIA HOLDINGS, COGNIZANT, WIPRO, TATA CONSULTANCY SERVICES, PAREXEL INTERNATIONAL, ADVERA HEALTH ANALYTICS, ENNOV, SYMPLR (FORMERLY HEALTHSTREAM SAFETY), SPARTA SYSTEMS (A HONEYWELL COMPANY), RELSYS, SAMARTH LIFE SCIENCES, ALLIANCE LIFE SCIENCES CONSULTING, Others

Which segments covered the Pharmacovigilance Software Market?

By Component (Software, Services (Implementation, Support & Maintenance, Consulting)), By Deployment (Cloud-Based, On-Premise), By Functionality (Case Management, Signal Detection & Management, Risk Management, Regulatory Reporting, Analytics & Reporting), By End User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations (CROs), Healthcare Providers), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Pharmacovigilance Software Market

Published Date : 09 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date