- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Photodynamic Therapy Market Size, Share & Forecast 2034 | CAGR 7.6%

Global Photodynamic Therapy Market Size, Share & Growth Analysis By Product Type (Photosensitizer Drugs – ALA, Porphyrins, Chlorins; PDT Devices – Diode Lasers, LED Systems; Light Delivery Accessories – Fiber Optics), By Application (Oncology – Skin, Lung, Esophageal Cancer; Dermatology – Actinic Keratosis, Acne, Psoriasis; Ophthalmology – AMD), By End-User (Hospitals, Dermatology Clinics, Cancer Centers, Research Institutes) Industry Trends, Competitive Landscape & Forecast 2025–2034

Report Overview

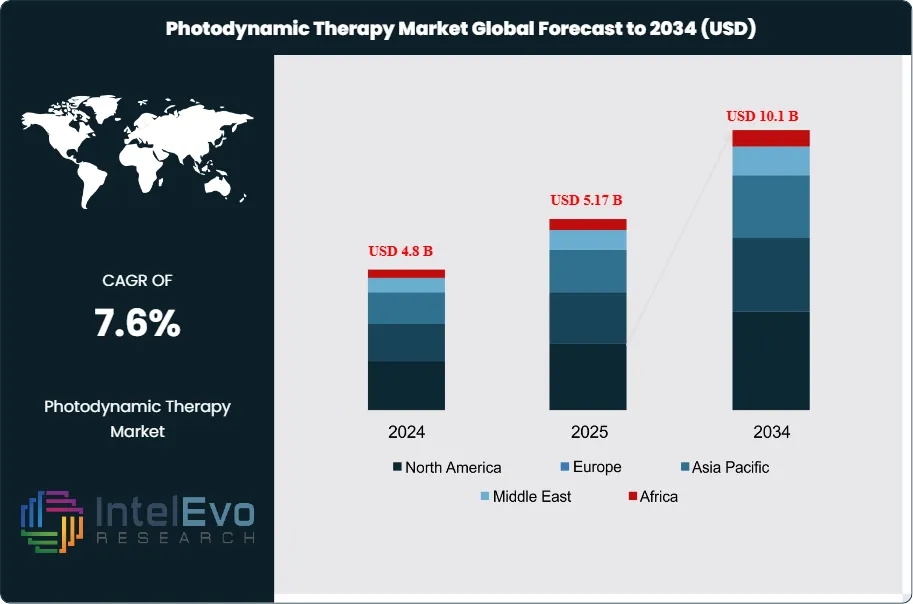

The Photodynamic Therapy Market was valued at around USD 4.8 billion in 2024 and is expected to reach nearly USD 10.1 billion by 2034. This growth is driven by the rising rates of skin cancers, the increasing demand for less invasive cancer treatments, and fast advancements in laser delivery systems. Based on this growth trend, the market size for 2025 is estimated at about USD 5.17 billion. Starting in 2026, the market is projected to grow at an annual rate of about 7.6% from 2026 to 2034, ultimately reaching around USD 10.1 billion by 2034. This growth shows a significant shift towards targeted therapies that aim to destroy cancer cells accurately while protecting nearby healthy tissue. The demand for these therapies is also boosted by supportive regulatory approvals and the inclusion of next-generation photosensitizers in standard clinical practices.

Get More Information about this report -

Request Free Sample ReportThe rising number of chronic skin conditions and cancer cases creates a strong demand. In 2024, the United States is expected to report over 2 million new cancer cases, and global numbers are likely to rise significantly by 2035 due to aging populations and environmental factors. This increase puts pressure on traditional surgical resources and highlights the need for outpatient-friendly alternatives like PDT. At the same time, the growing number of cases of actinic keratosis—affecting millions worldwide—keeps photodynamic therapy central to dermatological policies and reimbursement discussions.

On the supply side, vendors are expanding their offerings from basic light lamps to integrated "drug-device" combinations that pair third-generation photosensitizers with AI-driven light dosing systems. Intelligent systems capable of real-time monitoring are becoming more popular, aided by advancements in nanotechnology and portable LED arrays. Nanoparticle-based photosensitizers, which enhance tumor selectivity and lower patient sensitivity to light, are changing how doctors treat deep-seated tumors. Photosensitizer drugs are expected to make up about 75% of market revenues by 2034, while hardware such as lasers and LED systems remains an important growth segment at nearly 20%, with professional and managed services making up the remainder.

Regulation and clinical standardization are key to the market. Stricter safety protocols, mandatory validation for the effectiveness of light sources, and increased reimbursement for non-cancer treatments, such as severe acne and psoriasis, help maintain steady funding flows. Hospitals and specialized cancer centers account for more than 60% of spending, along with increasing adoption in private dermatology and cosmetic clinics. North America currently accounts for about 36% of global revenues, followed by Europe at around 29%. Asia Pacific is the fastest-growing region, thanks to rapidly improving healthcare systems and a large patient base in emerging markets like China and India.

, By Application (Oncology – Skin, Lung, Esophageal Cancer; Dermatology – Actinic Keratosis, Acne, Psoriasis; Ophthalmology – AMD), By End-User (Hospitals, Dermatology Clinics, Cancer Centers, Research Institutes) Industry Trends, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Photodynamic Therapy Market records 4.8 billion USD, 2024 in revenues. It is projected to reach 10.1 billion USD, 2034, representing a CAGR of 7.6%, 2024-2034.

- Segment Dominance: Photosensitizer Drugs lead the product segment with a 75.4%, 2024 revenue share. This dominance underscores their critical role as the primary agent in triggering therapeutic biochemical reactions.

- Segment Dominance: Hospitals command a 48.5%, 2024 share of the end-user segment. This leadership position highlights the necessity of specialized medical staff and advanced infrastructure for delivering complex PDT procedures.

- Driver: Oncology (Cancer Treatment) acts as the primary demand catalyst, holding a 42.9%, 2024 application share. This concentration signals the high clinical value placed on PDT for treating skin, lung, and esophageal malignancies.

- Restraint: High treatment costs and prolonged photosensitivity continue to limit widespread adoption. As a result, estimated: 15.0% of potential patients in low-income regions face accessibility barriers, 2024.

- Opportunity: Vendors can expand by addressing underpenetrated outpatient segments and home-based "Daylight-PDT" kits. These represent estimated: 1.2 billion USD, 2034 in additional addressable spending, 2024-2034.

- Trend: Nanotechnology and AI-guided dosimetry increasingly shape PDT deployments. Estimated: 45.0% of new PDT devices, 2028 are expected to feature smart light-delivery sensors, 2024-2034.

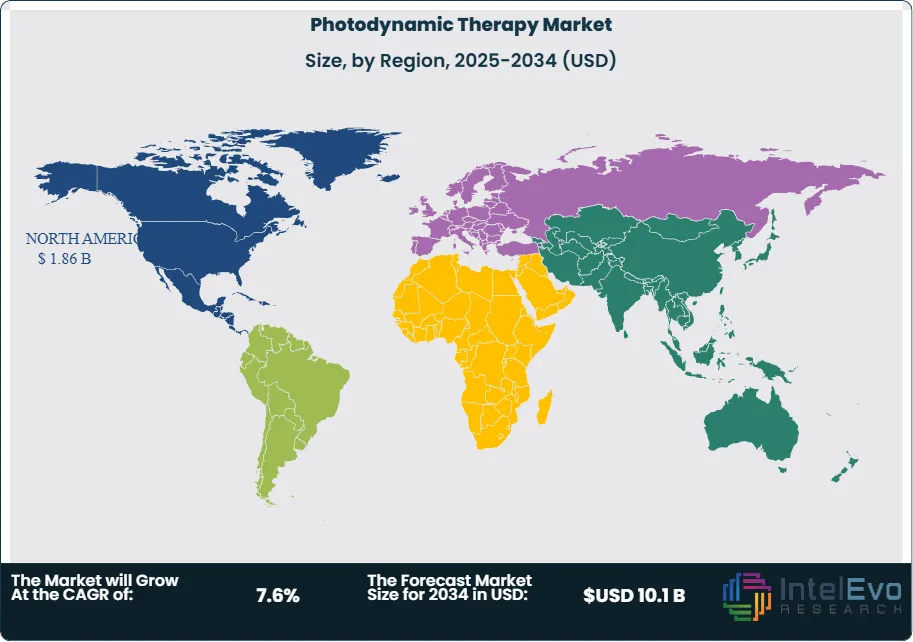

- Regional Analysis: North America leads the regional landscape with a 36.1%, 2024 market share and 1.7 billion USD, 2024 in revenues. The Asia-Pacific region is projected to contribute estimated: 38.0% of incremental global market expansion, 2024-2034.

By Product Type

Photosensitizer drugs play a significant role in the 2025 market, making up 75.4 percent of global revenues. Their size reflects the importance of chemical agents such as Aminolevulinic Acid (ALA) and Porphyrin derivatives in the PDT process. Adoption is rising as second and third-generation drugs provide better tissue-specific targeting and fewer side effects. This segment is expected to grow steadily through 2030 as pharmaceutical R&D introduces new formulations that need shorter incubation periods.

Photodynamic therapy devices are gaining strong traction, especially in the laser and LED categories. Diode lasers allow for precise light delivery for internal oncology. LED panels have become the standard for wide-area dermatological treatments. The demand for portable and handheld devices is increasing, as clinics look to offer flexible outpatient services. Together, these hardware categories receive significant investment as healthcare providers upgrade their light delivery systems to meet new drug protocols.

By Application

Oncology accounts for 42.9 percent of total demand in 2025. The need for tissue-preserving treatments for skin, esophageal, and head-and-neck cancers drives continuous investment in PDT platforms. National cancer initiatives that prioritize minimally invasive surgery further support this segment. As clinical trials confirm PDT's effectiveness in treating drug-resistant tumors, its role in comprehensive cancer care is expected to strengthen.

Dermatology and acne treatment make up the next major group of applications. Photodynamic therapy is being used more frequently for actinic keratosis, moderate-to-severe acne, and psoriasis, offering a lasting alternative to long-term topical or systemic medications. Demand is increasing as the "wellness" trend encourages patients to seek light-based therapies that provide both therapeutic and aesthetic benefits. This segment is anticipated to grow quickly as younger populations look for advanced acne solutions.

By End-User

Hospitals account for 48.5 percent of total demand in 2025. Their specialized infrastructure and access to multi-disciplinary oncology teams make them the main setting for complex PDT procedures involving internal organs. Ongoing investments in "Smart Hospitals" are integrating PDT systems with electronic health records to improve patient tracking.

Cosmetics and dermatology clinics are the fastest-growing end-user group. These settings prefer PDT due to its outpatient efficiency and high patient turnover rates. As the cost of LED-based systems decreases, more private practices are adding PDT to their services for skin rejuvenation and precancerous lesion removal. This shift toward decentralized care is a key factor driving market volume.

By Region

North America holds 36.1 percent of the market in 2025, valued at 1.86 billion USD. The region benefits from an established reimbursement system and a high concentration of leading biopharmaceutical companies. Programs that focus on skin cancer screening and early intervention support North America's leadership.

Asia Pacific is experiencing the fastest growth due to increased healthcare spending and a significant rise in cancer diagnoses. Countries like China and Japan are heavily investing in local medical device manufacturing, reducing the cost of PDT hardware. Emerging hotspots in Southeast Asia present opportunities for vendors to establish a presence through public-private partnerships and medical tourism initiatives.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Photosensitizer Drugs (ALA, Porphyrins, Chlorins)

- PDT Devices (Diode Lasers, LED Systems)

- Light Delivery Accessories (Fiber Optics)

By Application

- Oncology (Skin, Lung, Esophageal Cancer)

- Dermatology (Actinic Keratosis, Acne, Psoriasis)

- Ophthalmology (AMD)

- Others (Dentistry, Infectious Diseases)

By End-User

- Hospitals

- Cosmetics and Dermatology Clinics

- Cancer Treatment Centers

- Research Institutions

By Regions

- North America

- Latin America

- East Asia and Pacific

- Sea and South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.17 B |

| Forecast Revenue (2034) | USD 10.1 B |

| CAGR (2025-2034) | 7.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Photosensitizer Drugs (ALA, Porphyrins, Chlorins), PDT Devices (Diode Lasers, LED Systems), Light Delivery Accessories (Fiber Optics)), By Application (Oncology (Skin, Lung, Esophageal Cancer), Dermatology (Actinic Keratosis, Acne, Psoriasis), Ophthalmology (AMD), Others (Dentistry, Infectious Diseases)), By End-User (Hospitals, Cosmetics and Dermatology Clinics, Cancer Treatment Centers, Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Galderma S.A., Biofrontera AG, Sun Pharmaceutical Industries Ltd., Bausch Health Companies Inc., Novartis AG, Lumibird (Quantel Medical), Photocure ASA, Biolitec AG, Theralase Technologies Inc., Modulight Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Oncology – Skin, Lung, Esophageal Cancer; Dermatology – Actinic Keratosis, Acne, Psoriasis; Ophthalmology – AMD), By End-User (Hospitals, Dermatology Clinics, Cancer Centers, Research Institutes) Industry Trends, Competitive Landscape & Forecast 2025–2034")

, By Application (Oncology – Skin, Lung, Esophageal Cancer; Dermatology – Actinic Keratosis, Acne, Psoriasis; Ophthalmology – AMD), By End-User (Hospitals, Dermatology Clinics, Cancer Centers, Research Institutes) Industry Trends, Competitive Landscape & Forecast 2025–2034")

, By Application (Oncology – Skin, Lung, Esophageal Cancer; Dermatology – Actinic Keratosis, Acne, Psoriasis; Ophthalmology – AMD), By End-User (Hospitals, Dermatology Clinics, Cancer Centers, Research Institutes) Industry Trends, Competitive Landscape & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date