- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

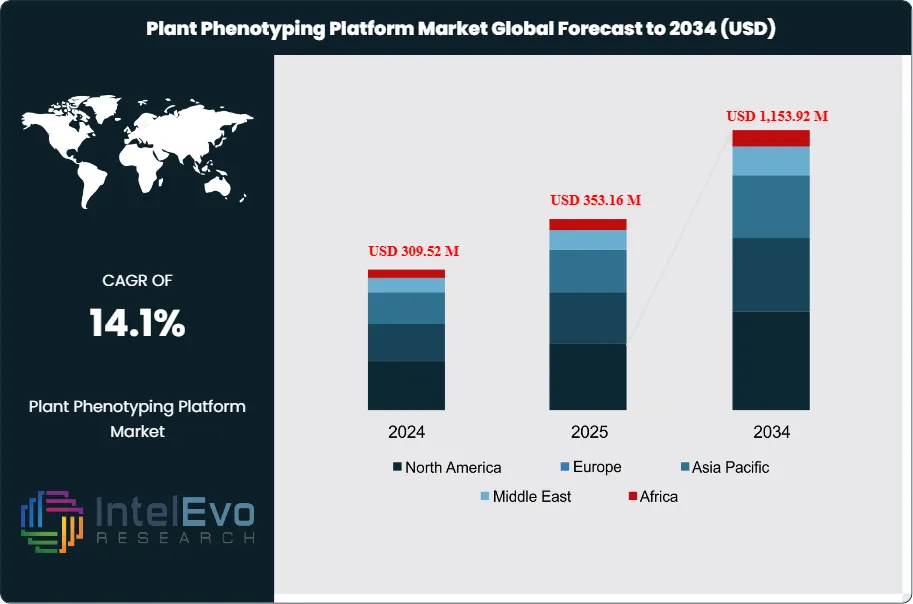

Global Plant Phenotyping Platform Market Size, Share | CAGR 14.1%

Global Plant Phenotyping Platform Market Size, Share, Analysis By Product (Imaging Systems, Sensors and Measurement Systems, Software and Analytics Platforms, Automated Phenotyping Platforms, Data Management Solutions, Accessories and Consumables), By Application (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic and Biotic Stress Phenotyping, Precision Agriculture), By End-User Industry, Market Dynamics & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 353.16 Million | USD 1,153.92 Million | 14.1% | Europe, 43.9% |

The Plant Phenotyping Platform Market was valued at approximately USD 309.52 Million in 2024 and reached USD 353.16 Million in 2025. The market is projected to grow to USD 1,153.92 Million by 2034, expanding at a CAGR of 14.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 800.76 Million over the analysis period. The Plant Phenotyping Platform Market covers the commercial space for hardware, software, and services that measure, analyze, and quantify plant traits including growth, morphology, physiology, biomass, root architecture, and stress tolerance. The market encompasses high-throughput imaging systems, automated conveyor platforms, field-based drone and sensor systems, controlled environment phenotyping chambers, and AI-powered data analytics platforms.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in three structural shifts. First, the United Nations Food and Agriculture Organization (FAO) projects over 600 million people facing hunger by 2030, driving government investment in climate-resilient crop breeding programs. Second, rapid technological advancement in artificial intelligence, machine learning, and deep learning-based image analysis enables high-throughput phenotypic data collection at unprecedented scale and accuracy. Third, climate change and extreme weather events require accelerated breeding cycles for drought-tolerant, heat-resistant, and disease-resistant crop varieties, with phenotyping platforms reducing traditional breeding timelines from 10 to 15 years down to 5 to 8 years.

Major launches and partnerships accelerated market development through 2024-2025. In September 2025 LemnaTec GmbH launched a new line of automated phenotyping systems designed for high-throughput analysis, responding to growing demand for precision agriculture tools. In August 2025 Phenome Networks announced a collaboration with a leading agricultural university to develop a machine learning-integrated phenotyping platform. In July 2025 KeyGene N.V. acquired a startup specializing in genomic data analysis to enhance genetic research capabilities. In 2025 AI-powered plant phenotyping platforms such as ChronoRoot 2.0 were introduced, enabling real-time monitoring of plant growth and multi-organ tracking with enhanced accuracy. Norway launched a national plant phenotyping infrastructure network in 2025 aimed at accelerating research in climate-resilient crops.

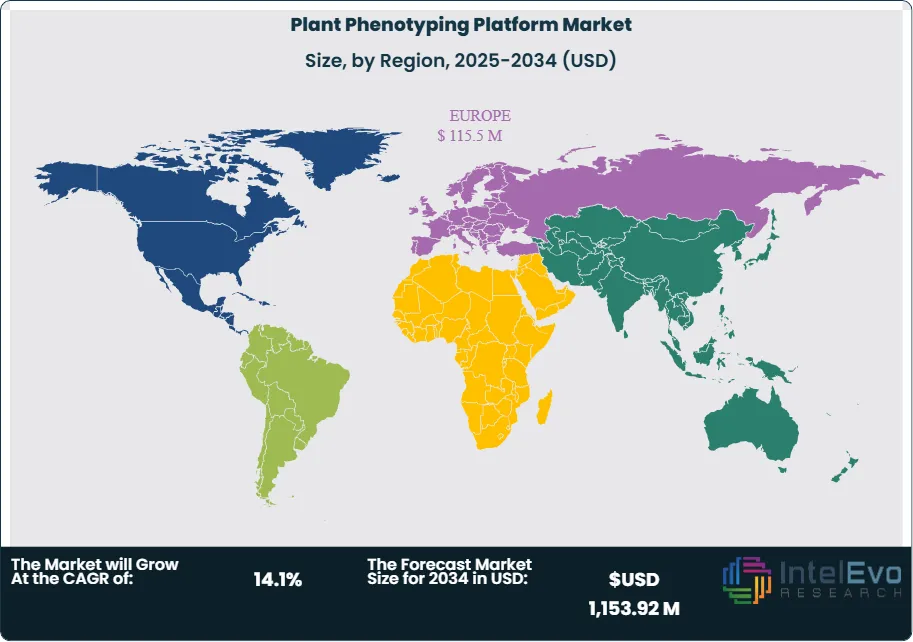

Europe held 43.9% of global Plant Phenotyping Platform Market revenue in 2025, equivalent to USD 155.03 Million, anchored by Germany, the Netherlands, France, the United Kingdom, and the Nordic countries. European dominance reflects decades of public research infrastructure investment through the European Plant Phenotyping Network (EPPN2020), the EMPHASIS research infrastructure under the European Strategy Forum on Research Infrastructures (ESFRI), and national programs in Germany's IPK Gatersleben, France's INRAE, and the Netherlands' Wageningen University and Research. North America captured approximately 28% share at USD 98.88 Million. Asia Pacific held 19% share at USD 67.10 Million and is projected to grow fastest at approximately 16% CAGR through 2034.

Forward visibility through 2034 rests on three catalysts. First, integration of artificial intelligence and machine learning with hyperspectral imaging, LiDAR, and thermal imaging enables automated analysis of plant traits across large genetic populations with unprecedented throughput. Second, expansion of UAV-based multispectral imaging platforms enables field-scale drought and nutrient stress assessment at commercial farming scale. Third, the emergence of CRISPR-guided phenotypic screening pipelines accelerates trait discovery in staple crops including wheat, rice, maize, and soybean. These forces together support the 14.1% forecast CAGR in the Plant Phenotyping Platform Market through 2034.

Market Definition & Scope

The Plant Phenotyping Platform Market is defined as the commercial space for integrated hardware, software, sensors, and services that measure, analyze, and quantify plant traits for research, breeding, and agricultural applications. The market encompasses five core technology categories: controlled environment phenotyping (growth chambers, conveyor systems), greenhouse phenotyping (automated imaging platforms), field phenotyping (ground robots, UAVs), remote sensing phenotyping (satellite and aerial multispectral imaging), and laboratory phenotyping (spectrometry, PAM fluorometry, gas exchange analysis).

This analysis includes equipment (imaging systems, sensors, robotics, growth chambers), software (image analysis, data management, machine learning platforms), sensors (RGB cameras, hyperspectral, thermal, LiDAR, chlorophyll fluorescence), and services (contract phenotyping, data analysis, consulting). The scope explicitly excludes standalone precision agriculture farm management systems without phenotyping modules, general-purpose microscopy equipment, genomic sequencing hardware without phenotype integration, and consumer-grade drones without multispectral imaging capability. The parent agricultural biotechnology market reached approximately USD 95 Billion in 2025, with the Plant Phenotyping Platform Market representing the specialized trait measurement subset alongside genomics, bioinformatics, and plant breeding services.

, By Application (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic and Biotic Stress Phenotyping, Precision Agriculture), By End-User Industry, Market Dynamics & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Plant Phenotyping Platform Market grew from USD 353.16 Million in 2025 to a projected USD 1,153.92 Million in 2034, expanding at a 14.1% CAGR.

- Segment Dominance (By Product): Equipment held 57.3% revenue share in 2024 per Market.us, anchored by imaging systems, sensors, and robotic conveyor platforms from LemnaTec, PHENOSPEX, and PSI.

- Segment Dominance (By Application): High-throughput screening captured 34.6% revenue share in 2024 per Market.us, reflecting efficient simultaneous evaluation of multiple phenotypic traits across large plant populations.

- Driver: Government funding including the Norway national plant phenotyping infrastructure network launched in 2025 and the European Strategy Forum on Research Infrastructures EMPHASIS program drive public research investment.

- Restraint: High capital costs of automated phenotyping platforms typically range from USD 200,000 for entry-level conveyor systems to USD 10 million for large-scale field phenotyping installations, limiting SME and emerging-market adoption.

- Opportunity: Asia Pacific is projected to grow fastest at approximately 16% CAGR through 2034, with China, India, Japan, and South Korea expanding domestic phenotyping infrastructure under national food security strategies.

- Trend: AI-powered platforms such as ChronoRoot 2.0 introduced in 2025 enable real-time monitoring of plant growth and multi-organ tracking with enhanced accuracy and scalability for root phenotyping applications.

- Regional: Europe held 43.9% revenue share in 2024 per Market.us at USD 115.5 Million, anchored by Germany, the Netherlands, France, and the United Kingdom research infrastructure.

Key Insights Summary

- In September 2025 LemnaTec GmbH, owned by Nynomic AG, launched a new line of automated phenotyping systems designed for high-throughput analysis, responding to growing demand for precision agriculture tools across European and North American research institutions.

- In August 2025 Phenome Networks announced a strategic collaboration with a leading agricultural university to develop a new phenotyping platform integrating machine learning algorithms for enhanced data analysis capabilities.

- In July 2025 KeyGene N.V. acquired a startup specializing in genomic data analysis, indicating strategic focus on enhancing genetic research capabilities and more effective breeding solutions across the phenotyping-genotyping integration continuum.

- In 2025 AI-powered plant phenotyping platforms including ChronoRoot 2.0 were introduced, enabling real-time monitoring of plant growth and multi-organ tracking with enhanced accuracy and scalability for root system architecture analysis.

- In 2025 Norway launched a national plant phenotyping infrastructure network aimed at accelerating research in climate-resilient crops and strengthening collaborative innovation in phenotyping technologies across Scandinavian research institutions.

- Equipment held 57.3% revenue share and high-throughput screening captured 34.6% application share in the Plant Phenotyping Platform Market in 2024 per Market.us analysis, with laboratory deployment at 48.9% share.

- LemnaTec GmbH commands up to 25% plant phenotyping market share per Future Market Insights, followed by PHENOSPEX, Delta-T Devices, and WIWAM as secondary leaders.

Competitive Landscape Overview

The Plant Phenotyping Platform Market is moderately fragmented with the top four companies including LemnaTec GmbH, PHENOSPEX, KeyGene, and Heinz Walz collectively holding an estimated 50 to 58% of global revenue in 2025. Competition is structured across three tiers: European hardware and integrated platform leaders dominated by German and Dutch vendors reflecting decades of public research infrastructure investment; software and data analytics specialists including Phenome Networks, Hiphen, and PhenoKey; and agrochemical corporate subsidiaries including BASF's CropDesign and Bayer-integrated breeding operations that use phenotyping for internal seed development.

The competitive environment shifted sharply through 2024-2025 toward AI integration and strategic partnerships between technology providers and research institutions. LemnaTec launched new automated phenotyping systems in September 2025. Phenome Networks announced a university collaboration for ML-integrated platform development in August 2025. KeyGene acquired a genomic data analysis startup in July 2025. Partnerships between technology providers and research institutions enhance the capabilities of phenotyping technologies and broaden applications across crop improvement, disease diagnostics, trait discovery, stress tolerance assessment, and yield prediction. Emerging regional competitors in China (Topgenics), India (Agribio Tech), and Brazil (Phenomax) target localized markets with lower-cost platforms suited to domestic research budgets.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| LemnaTec GmbH (Nynomic AG) | Aachen, Germany | Leader | Scanalyzer HTS; PlantEye; automated phenotyping systems | Europe, Global | Launched new line of automated phenotyping systems for high-throughput analysis in September 2025 |

| PHENOSPEX B.V. | Heerlen, Netherlands | Leader | PlantEye F600 3D laser scanner; TraitFinder software | Europe, Global | Continued PlantEye F600 multispectral 3D scanner expansion across European research institutes 2025 |

| KeyGene N.V. | Wageningen, Netherlands | Leader | KeyPhene phenotyping platform; molecular breeding services | Europe, Global | Acquired genomic data analysis startup in July 2025 to enhance genetic research capabilities |

| Heinz Walz GmbH | Effeltrich, Germany | Challenger | PAM fluorometry; IMAGING-PAM; MINI-PAM | Europe, Global | Continued chlorophyll fluorescence imaging instrument expansion for plant stress research 2025 |

| PSI (Photon Systems Instruments) | Drasov, Czech Republic | Challenger | PlantScreen automated phenotyping platforms | Europe, Global | Continued PlantScreen Compact and Modular system deployments across European plant science institutes 2025 |

| Delta-T Devices Ltd | Cambridge, United Kingdom | Challenger | SunScan canopy analyzer; WET sensor; soil moisture instruments | Europe, Global | Continued environmental sensor portfolio expansion for field and greenhouse phenotyping 2025 |

| Qubit Systems Inc. | Kingston, ON, Canada | Niche | Q-Box gas exchange; photosynthesis instruments | North America, Global | Continued photosynthesis and gas exchange instrumentation development for research applications 2025 |

| WIWAM (CropDesign/BASF) | Ghent, Belgium | Niche | WIWAM conveyor phenotyping; CropDesign TraitMill | Europe | Continued WIWAM imaging phenotyping conveyor system expansion in Ghent-based BASF facility 2025 |

| Phenome Networks Ltd. | Raanana, Israel / France | Niche (Software) | Phenome One breeding and phenotyping software | Global | Announced collaboration with leading agricultural university in August 2025 for ML-integrated platform |

| BASF SE | Ludwigshafen, Germany | Leader (Seed) | CropDesign TraitMill; integrated seed breeding platforms | Global | Continued integration of phenotyping across BASF Agricultural Solutions seed breeding operations 2025 |

Segmentation Analysis

The Plant Phenotyping Platform Market segments across product, technology, application, crop type, and end-user. Procurement leaders at research institutes, seed companies, and agrochemical firms building a plant phenotyping platform procurement checklist should benchmark vendors on throughput capacity (plants per day), imaging modality coverage (RGB, hyperspectral, thermal, LiDAR, fluorescence), AI analytics depth, integration with laboratory information management systems (LIMS), and total cost of ownership including maintenance, reagents, and training across each segmentation dimension.

By Product

Equipment led the Plant Phenotyping Platform Market with 57.3% revenue share in 2024 per Market.us, equivalent to approximately USD 202 Million in 2025. Equipment includes automated conveyor platforms from LemnaTec Scanalyzer and WIWAM, 3D laser scanners from PHENOSPEX PlantEye, chlorophyll fluorescence imaging from Heinz Walz IMAGING-PAM, and PSI PlantScreen modular systems. Sensors captured approximately 24% share, including hyperspectral cameras from Headwall Photonics, thermal imaging from FLIR, LiDAR from Velodyne, and environmental sensors from Delta-T Devices. Software and analytics platforms held 14% share, dominated by image analysis software, data management platforms, and emerging AI-powered platforms. Services captured the remaining 5%, including contract phenotyping, data analysis consulting, and implementation services.

Per Coherent Market Insights, equipment is expected to contribute 81.9% share of the market in 2025 under broader equipment definitions including sensors. The higher concentration reflects capital-intensive installations where hardware dominates total project cost, with software and services increasingly bundled rather than standalone. Cost benchmarks include entry-level greenhouse conveyor systems at USD 200,000 to USD 500,000, mid-tier field phenotyping installations at USD 1 million to USD 3 million, and flagship research infrastructure at USD 5 million to USD 15 million for national programs including IPK Gatersleben's PhenoCenter and INRAE's Phenome-Emphasis facilities.

By Application

High-throughput screening led the Plant Phenotyping Platform Market with 34.6% revenue share in 2024 per Market.us, anchored by conveyor-based systems that evaluate hundreds to thousands of plants daily across multiple imaging modalities. Trait identification captured 22% share, supporting mapping-population phenotyping for quantitative trait locus (QTL) discovery. Photosynthetic performance assessment held 16% share, dominated by Heinz Walz PAM fluorometry and PSI FluorCam imaging systems. Morphology analysis captured 13%, including LiDAR-based canopy structure quantification. Disease diagnostics held 8% share under advancing machine learning-based image classification, and yield prediction captured 7% share through UAV-based multispectral imaging.

By End-User

Laboratory deployment led the Plant Phenotyping Platform Market with 48.9% revenue share in 2024 per Market.us, anchored by universities, government research institutes, and agricultural research centers conducting fundamental plant biology research. Greenhouse deployment captured approximately 32% share, dominated by conveyor-based imaging systems for controlled-environment screening. Field deployment held 19% share, growing fastest as UAV-based multispectral imaging platforms reach commercial scale. End-user segmentation by organization type shows seed companies at 28% share (Bayer Crop Science, Corteva, Syngenta, Limagrain, KWS, BASF), agricultural research institutes at 32% (INRAE, IPK Gatersleben, Rothamsted Research, USDA ARS, EMBRAPA), universities at 22% (Wageningen UR, University of Nebraska, University of Arizona, CSIRO), government organizations at 12%, and agrochemical companies at 6%.

Regional Analysis

The Plant Phenotyping Platform Market divides across Europe, North America, Asia Pacific, Latin America, and Middle East & Africa, with Europe leading in 2025 and Asia Pacific growing fastest through 2034.

Europe

Europe held 43.9% of global Plant Phenotyping Platform Market revenue in 2024 per Market.us at USD 115.5 Million, expanding to approximately USD 155.03 Million in 2025. Germany anchors the regional market with approximately 25% of European revenue, driven by IPK Gatersleben, Forschungszentrum Julich, and Max Planck Institute for Plant Breeding Research. The Netherlands contributes 22% of European revenue through Wageningen University and Research, Utrecht University, and KeyGene. France holds 18% share through INRAE, CIRAD, and the Phenome-Emphasis research infrastructure. The European Plant Phenotyping Network (EPPN2020) and the EMPHASIS European Strategy Forum on Research Infrastructures (ESFRI) program coordinate continental investment. Horizon Europe funding through 2027 sustains public-sector demand.

North America

North America captured approximately 28% share in 2025 at USD 98.88 Million, with the United States contributing 84% of regional revenue, Canada at 12%, and Mexico at 4%. The U.S. Department of Agriculture Agricultural Research Service (USDA ARS) operates major phenotyping facilities at the Maricopa Agricultural Center (Arizona), the Beltsville Agricultural Research Center (Maryland), and partnerships with land grant universities. The USDA National Institute of Food and Agriculture (NIFA) Agriculture and Food Research Initiative (AFRI) funds university-based phenotyping research. Canada's Global Institute for Food Security (GIFS) at the University of Saskatchewan operates the P2IRC phenotyping facility. Major U.S. players include Qubit Systems (Canadian with U.S. operations), Phenomix, HM Clause, and Corteva Agriscience.

Asia Pacific

Asia Pacific captured 19% share in 2025 at approximately USD 67.10 Million and is projected to grow fastest at 16% CAGR through 2034. China leads regional adoption, with the Chinese Academy of Agricultural Sciences (CAAS) Institute of Crop Sciences, the Huazhong Agricultural University, and the Shanghai Academy of Agricultural Sciences operating major phenotyping facilities. The National Precision Agriculture Application Project and 14th Five-Year Plan allocate substantial funding to precision breeding infrastructure. Japan's National Agriculture and Food Research Organization (NARO) operates the RIKEN Plant Phenotyping Platform. South Korea's Rural Development Administration (RDA) expands domestic phenotyping capacity. Australia's CSIRO Plant Industry operates the Australian Plant Phenomics Network (APPN) coordinated across multiple state research sites. India's Indian Council of Agricultural Research (ICAR) expands phenotyping under the National Agricultural Higher Education Project.

Latin America

Latin America held 5.5% share in 2025 at approximately USD 19.42 Million, led by Brazil, Argentina, Mexico, and Chile. Brazil's Empresa Brasileira de Pesquisa Agropecuaria (EMBRAPA) operates the largest Latin American phenotyping facility at Embrapa Informatica Agropecuaria in Campinas. Argentina's Instituto Nacional de Tecnologia Agropecuaria (INTA) partners with Bioceres for commercial phenotyping services. Mexico's CIMMYT (International Maize and Wheat Improvement Center) operates major phenotyping platforms supporting global wheat and maize breeding programs. Chile's Instituto de Investigaciones Agropecuarias (INIA) maintains phenotyping capabilities across viticulture, fruits, and field crops. Regional growth is driven by agricultural export competitiveness and climate adaptation imperatives, particularly for soybean, maize, and coffee breeding programs.

Middle East & Africa

The Middle East & Africa region held 3.6% share in 2025 at approximately USD 12.71 Million. Israel leads regional innovation, with the Volcani Center, Hebrew University's Robert H. Smith Faculty of Agriculture, and companies including Phenome Networks and Saillog anchoring the domestic ecosystem. The United Arab Emirates' International Center for Biosaline Agriculture (ICBA) operates specialized salt-tolerance phenotyping under the Mohamed bin Zayed University of Artificial Intelligence partnership. Saudi Arabia's King Abdullah University of Science and Technology (KAUST) operates the Center for Desert Agriculture. Egypt's Agricultural Research Center (ARC) supports phenotyping under the African Union Comprehensive Africa Agriculture Development Programme (CAADP). South Africa's Agricultural Research Council (ARC) operates phenotyping facilities at the Vegetable and Ornamental Plants Institute and the Plant Health and Protection Institute.

Country Analysis

The Plant Phenotyping Platform Market concentrates in four national markets that together contribute more than 55% of 2025 global revenue: the United States, Germany, the Netherlands, and France.

United States

The United States generated approximately USD 83.06 Million in Plant Phenotyping Platform Market revenue in 2025, with a country CAGR of approximately 12.5% through 2034 per Future Market Insights. The U.S. Department of Agriculture Agricultural Research Service (USDA ARS) operates phenotyping facilities at Maricopa Agricultural Center in Arizona, Beltsville Agricultural Research Center in Maryland, and partnerships with land grant universities. The USDA National Institute of Food and Agriculture (NIFA) Agriculture and Food Research Initiative (AFRI) committed USD 215 million to crop genomics and phenotyping in fiscal year 2024. Major U.S. buyers include the University of Nebraska-Lincoln Carson Center for Plant Phenomics, the Donald Danforth Plant Science Center, and the Noble Research Institute. Impending 2025 U.S. tariffs on imported research equipment drive domestic sourcing preferences for hardware previously imported from European vendors.

Germany

Germany contributed approximately USD 38.76 Million in Plant Phenotyping Platform Market revenue in 2025, with a country CAGR of 14.5% through 2034. Germany leads European plant phenotyping through IPK Gatersleben (Leibniz Institute of Plant Genetics and Crop Plant Research), Forschungszentrum Julich's Institute of Bio- and Geosciences (IBG-2), Max Planck Institute for Plant Breeding Research, and the Leibniz Institute for Crop Science. The German Plant Phenotyping Network (DPPN) coordinates national research infrastructure. German domestic vendors LemnaTec GmbH (Aachen) and Heinz Walz GmbH (Effeltrich) are global market leaders. The Federal Ministry of Education and Research (BMBF) and the German Research Foundation (DFG) provide substantial research funding. Major German buyers include KWS Saat, BASF Agricultural Solutions, Bayer Crop Science, and Limagrain Germany.

Netherlands

The Netherlands accounted for approximately USD 34.10 Million in Plant Phenotyping Platform Market revenue in 2025, with a country CAGR of 14.3% through 2034. Wageningen University and Research operates the NPEC (Netherlands Plant Eco-phenotyping Centre) and the Unifarm facility, among the largest plant phenotyping infrastructures globally. KeyGene N.V. in Wageningen leads commercial molecular breeding services combined with phenotyping, and acquired a genomic data analysis startup in July 2025. PHENOSPEX B.V. in Heerlen provides PlantEye F600 3D laser scanners to European and global customers. Major Dutch buyers include Rijk Zwaan, Enza Zaden, BASF Vegetable Seeds (formerly Nunhems), and Bejo Zaden. The Dutch Topsector Agri & Food program funds public-private research partnerships.

France

France generated approximately USD 27.90 Million in Plant Phenotyping Platform Market revenue in 2025, with a country CAGR of 13.8% through 2034. Institut National de Recherche pour l'Agriculture, l'Alimentation et l'Environnement (INRAE) operates the Phenome-Emphasis research infrastructure with sites at Montpellier, Clermont-Ferrand, Dijon, and Versailles. CIRAD (Centre de Cooperation Internationale en Recherche Agronomique pour le Developpement) operates tropical crop phenotyping. The Agence Nationale de la Recherche (ANR) France 2030 plan committed EUR 2.8 billion to agricultural innovation through 2030. Phenome Networks (French operations) and Hiphen lead the domestic commercial phenotyping technology ecosystem. Major French buyers include Limagrain, Florimond Desprez, Vilmorin-Mikado, and RAGT Semences.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product

- Imaging Systems

- RGB Imaging Systems

- Hyperspectral Imaging Systems

- Multispectral Imaging Systems

- Thermal Imaging Systems

- Fluorescence Imaging Systems

- 3D Imaging Systems

- Sensors and Measurement Systems

- Software and Analytics Platforms

- Automated Phenotyping Platforms

- Data Management and Processing Solutions

- Accessories and Consumables

By Application

- Plant Breeding and Crop Improvement

- Genotype-to-Phenotype Research

- Abiotic Stress Phenotyping

- Biotic Stress Phenotyping

- Precision Agriculture and Smart Farming

- Functional Genomics Studies

- Crop Physiology Research

- Seed and Trait Evaluation

- High-Throughput Screening

- Agricultural Biotechnology Research

By End-User

- Academic and Research Institutes

- Agricultural Biotechnology Companies

- Plant Breeding Companies

- Seed Companies

- Contract Research Organizations (CROs)

- Government and Agricultural Research Organizations

- Food and Agribusiness Companies

- Others (Non-Profit Organizations and Environmental Research Centers)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 353.16 M |

| Forecast Revenue (2034) | USD 1,153.92 M |

| CAGR (2025-2034) | 14.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Imaging Systems, Sensors and Measurement Systems, Software and Analytics Platforms, Automated Phenotyping Platforms, Data Management and Processing Solutions, Accessories and Consumables), By Application, (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic Stress Phenotyping, Biotic Stress Phenotyping, Precision Agriculture and Smart Farming, Functional Genomics Studies, Crop Physiology Research, Seed and Trait Evaluation, High-Throughput Screening, Agricultural Biotechnology Research), By End-User, (Academic and Research Institutes, Agricultural Biotechnology Companies, Plant Breeding Companies, Seed Companies, Contract Research Organizations (CROs), Government and Agricultural Research Organizations, Food and Agribusiness Companies, Others (Non-Profit Organizations and Environmental Research Centers)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LEMNATEC GMBH (NYNOMIC AG), PHENOSPEX B.V., KEYGENE N.V., HEINZ WALZ GMBH, PSI (PHOTON SYSTEMS INSTRUMENTS), DELTA-T DEVICES LTD, QUBIT SYSTEMS INC., WIWAM (CROPDESIGN/BASF), PHENOME NETWORKS LTD., BASF SE, ROTHAMSTED RESEARCH, WPS B.V., PLANT-DITECH LTD., VIENNA BIOCENTER, HIPHEN SAS, PHENOMIX CORP., SMO BV, LI-COR BIOSCIENCES, SAILLOG LTD., PHENOKEY SA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic and Biotic Stress Phenotyping, Precision Agriculture), By End-User Industry, Market Dynamics & Forecast 2026-2034")

, By Application (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic and Biotic Stress Phenotyping, Precision Agriculture), By End-User Industry, Market Dynamics & Forecast 2026-2034")

, By Application (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic and Biotic Stress Phenotyping, Precision Agriculture), By End-User Industry, Market Dynamics & Forecast 2026-2034")

Frequently Asked Questions

How big is the Plant Phenotyping Platform Market?

The Global Plant Phenotyping Platform Market was valued at USD 309.52 Million in 2024 and is projected to reach USD 1,153.92 Million by 2034, growing at a CAGR of 14.1% from 2026 to 2034. Growth is driven by increasing investments in precision agriculture, rising demand for climate-resilient and high-yield crops, and the adoption of advanced imaging, sensor-based analytics, and AI technologies in plant breeding and crop research. Expanding sustainable agriculture initiatives and food security efforts continue to accelerate market growth worldwide.

Who are the major players in the Plant Phenotyping Platform Market?

LEMNATEC GMBH (NYNOMIC AG), PHENOSPEX B.V., KEYGENE N.V., HEINZ WALZ GMBH, PSI (PHOTON SYSTEMS INSTRUMENTS), DELTA-T DEVICES LTD, QUBIT SYSTEMS INC., WIWAM (CROPDESIGN/BASF), PHENOME NETWORKS LTD., BASF SE, ROTHAMSTED RESEARCH, WPS B.V., PLANT-DITECH LTD., VIENNA BIOCENTER, HIPHEN SAS, PHENOMIX CORP., SMO BV, LI-COR BIOSCIENCES, SAILLOG LTD., PHENOKEY SA, Others

Which segments covered the Plant Phenotyping Platform Market?

By Product, (Imaging Systems, Sensors and Measurement Systems, Software and Analytics Platforms, Automated Phenotyping Platforms, Data Management and Processing Solutions, Accessories and Consumables), By Application, (Plant Breeding and Crop Improvement, Genotype-to-Phenotype Research, Abiotic Stress Phenotyping, Biotic Stress Phenotyping, Precision Agriculture and Smart Farming, Functional Genomics Studies, Crop Physiology Research, Seed and Trait Evaluation, High-Throughput Screening, Agricultural Biotechnology Research), By End-User, (Academic and Research Institutes, Agricultural Biotechnology Companies, Plant Breeding Companies, Seed Companies, Contract Research Organizations (CROs), Government and Agricultural Research Organizations, Food and Agribusiness Companies, Others (Non-Profit Organizations and Environmental Research Centers))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Plant Phenotyping Platform Market

Published Date : 09 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date