- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Polymeric Concrete Market Size, Share & Growth Forecast 2034 | 7.5% CAGR

Global Polymeric Concrete Market Size, Share, Analysis Report By Type (PIC, PMC, PCC), Polymer Type(Epoxy, Vinylester, Polyester, Furan, Acrylate, Latex, Others), Application(Flooring Blocks, Trench Drains, Pump Bases, Waste Containers, Chemical Containments, Others), End-use(Commercial, Industrial, Residential, Municipal, Infrastructure), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

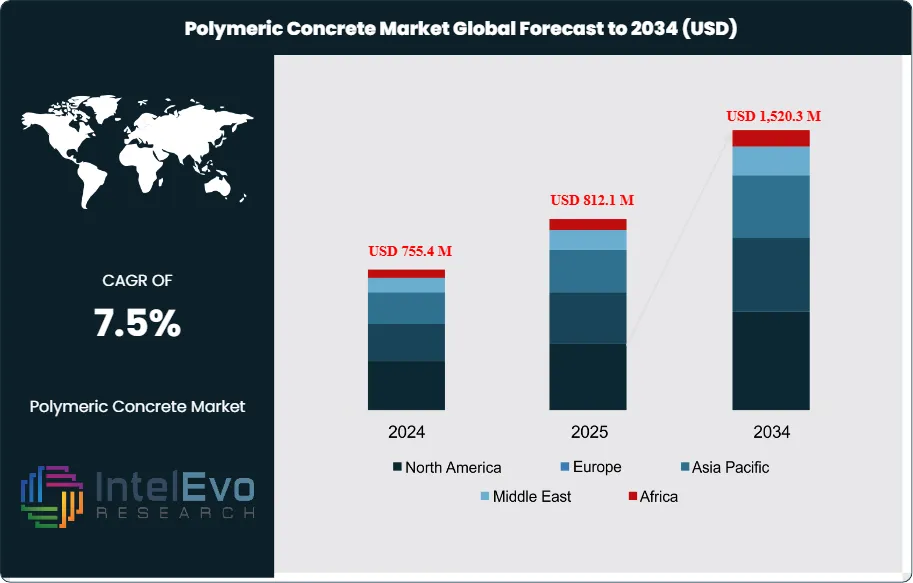

The Polymeric Concrete Market size is expected to reach USD 1,520.3 million by 2034, up from USD 755.4 million in 2024, growing at a CAGR of 7.5% during the forecast period from 2025 to 2034. The market growth is driven by the increasing demand for high-performance, durable, and chemical-resistant construction materials across infrastructure, industrial, and commercial projects. Rising adoption in bridge construction, industrial flooring, and repair applications is further fueling expansion. Additionally, innovations in eco-friendly polymeric binders and rapid-curing concrete solutions are enhancing sustainability and efficiency in the construction sector, making polymeric concrete a key material in modern infrastructure development.

Get More Information about this report -

Request Free Sample ReportPolymer concrete is a composite material comprising a polymer binder mixed with aggregates such as gravel, sand, or crushed stone. Unlike traditional cement-based concrete, polymer concrete utilizes polymer resins as the binding agent, offering enhanced properties like superior chemical resistance, high strength, and reduced permeability. These attributes make it an ideal choice for applications requiring durability and resistance to harsh environmental conditions.

The polymer concrete market is poised for significant growth, driven by the demand for sustainable and durable construction materials. While challenges like higher initial costs and limited awareness exist, the opportunities presented by emerging economies and technological advancements are substantial. With its superior properties and alignment with modern construction needs, polymer concrete is set to play a pivotal role in the future of the construction industry.

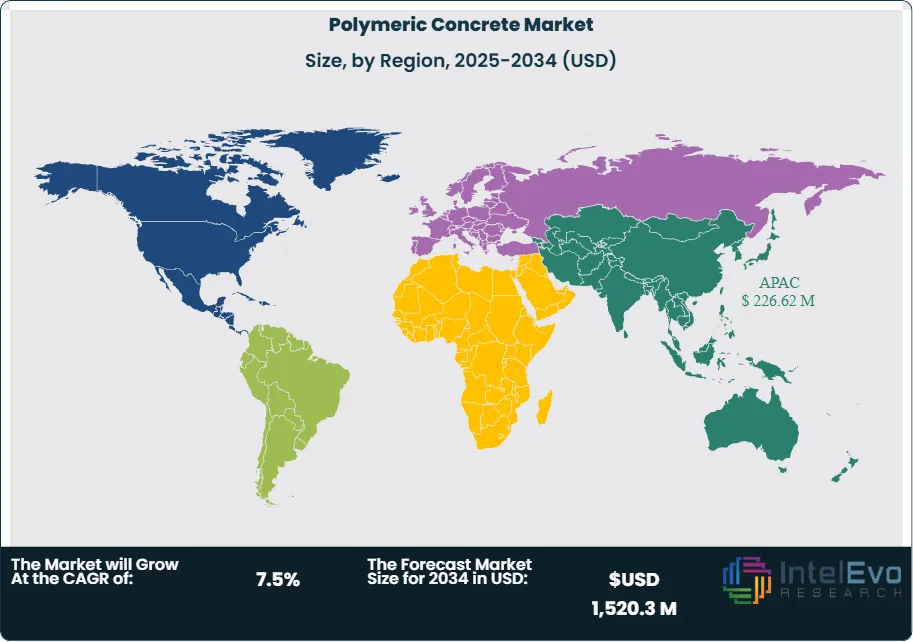

Asia Pacific dominated the polymer concrete market in 2024, accounting for a significant revenue share. This dominance is attributed to rapid industrialization, urbanization, and substantial infrastructure investments in countries like China and India. The region's focus on sustainable construction practices and pollution control further propels the demand for polymer concrete.

The COVID-19 pandemic adversely affected the polymer concrete market due to halted construction activities, disrupted supply chains, and labor shortages. However, as economies recover and infrastructure projects resume, the market is expected to regain momentum. The pandemic also highlighted the importance of resilient and low-maintenance construction materials, potentially accelerating the adoption of polymer concrete in future projects.

, Polymer Type(Epoxy, Vinylester, Polyester, Furan, Acrylate, Latex, Others), Application(Flooring Blocks, Trench Drains, Pump Bases, Waste Containers, Chemical Containments, Others), End-use(Commercial, Industrial, Residential, Municipal, Infrastructure), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The Polymeric Concrete Market is expected to reach USD 1,520.3 million by 2034, growing at a robust CAGR of 7.5% from 2024, growth is driven by increasing demand for sustainable and durable construction materials, rapid urbanization, and significant investments in infrastructure development across emerging economies.

- Type Dominance: The Polymer Impregnated Concrete (PIC) segment leads the polymeric concrete market due to its superior strength, reduced permeability, and enhanced durability compared to conventional concrete. PIC is widely used in structural repairs and high-performance applications where longevity and resistance to environmental stressors are critical. Its dominance is also attributed to growing infrastructure refurbishment projects globally.

- Polymer Type Dominance: Epoxy leads the polymeric concrete market due to its excellent adhesion, high mechanical strength, and superior chemical resistance. It is widely used in industrial and infrastructure applications that demand durability and resistance to harsh environmental and chemical exposures. Epoxy-based polymer concrete is also favored for flooring, pump bases, and containment structures due to its long service life and minimal maintenance requirements.

- Application Dominance: Flooring Blocks lead the polymeric concrete market owing to their extensive use in industrial, commercial, and infrastructure projects. These blocks offer superior strength, durability, and resistance to chemicals, making them ideal for heavy-duty flooring in warehouses, factories, and public facilities. Their ability to withstand mechanical loads and corrosive environments ensures long-lasting performance with minimal maintenance.

- End-use Dominance: Industrial applications leads due to the material's excellent resistance to corrosion, high strength, and durability in harsh environments. Industries such as chemical processing, manufacturing, and power generation prefer polymeric concrete for flooring, drainage systems, and containment areas because it outperforms traditional concrete under extreme conditions.

- Driver: Rising demand for durable, corrosion-resistant materials in infrastructure and industrial projects is propelling market growth. The need for low-maintenance and long-lasting construction solutions also fuels the adoption of polymeric concrete.

- Restraint: High initial costs and limited availability of specialized raw materials restrict widespread adoption. Lack of standardized codes and skilled workforce affects installation and design practices.

- Opportunity: Increasing investment in sustainable construction materials creates new market avenues. Growth in renovation and rehabilitation of aging infrastructure boosts future demand.

- Trend: Rising adoption of precast polymeric components is revolutionizing the construction process. Technological advancements in resin formulations are expanding application scope.

- Regional Analysis: North America is currently the leading region in the polymeric concrete market. The dominance can be attributed to a combination of factors such as a well-established construction industry, a growing focus on infrastructure maintenance and repair, and the adoption of advanced construction materials.

Type Analysis:

Polymer Impregnated Concrete (PIC) is currently the leading type in the polymeric concrete market due to its structural advantages over traditional concrete. The process of impregnating hardened concrete with a monomer and subsequently polymerizing it greatly improves its mechanical strength, reduces permeability, and enhances its resistance to chemical attacks and wear. These properties make PIC ideal for high-performance environments such as bridges, tunnels, marine structures, and industrial repair work. The increasing need for rehabilitation of aging infrastructure globally further fuels the demand for PIC. Given its extended service life and lower lifecycle maintenance, its dominance in the market is expected to persist. However, with rising innovation in construction composites, Polymer Resin Concrete (PMC) is anticipated to see growth in the future due to its moldability and quick curing time.

Product Class Analysis:

Epoxy Leads With more than 30% Market Share In Polymeric Concrete Market: Epoxy-based polymer concrete leads the market owing to its unparalleled chemical resistance, strong adhesive properties, and mechanical robustness. Epoxy is extensively used in environments where structural integrity and chemical durability are non-negotiable—such as in manufacturing plants, chemical facilities, and wastewater treatment stations. Its versatility in structural components like pump bases, flooring, and containment systems makes it a top choice among contractors. While epoxy continues to dominate due to its premium performance, Vinylester is expected to witness notable growth in the future due to its cost-effectiveness and balanced performance in moderate corrosive environments.

Application Analysis:

Among applications, flooring blocks dominate the polymeric concrete market, primarily because of their widespread adoption in heavy-use facilities like factories, warehouses, and commercial spaces. These blocks are valued for their ability to withstand constant mechanical stress, resist chemical spills, and maintain structural integrity over time. Their minimal maintenance and extended durability make them a cost-effective solution for long-term infrastructure investments. Moving forward, chemical containment structures are expected to gain traction due to increasing safety regulations and demand for efficient hazardous waste handling.

End-use Analysis:

The industrial sector is the largest end-use segment in the polymeric concrete market. This dominance is driven by the material’s resilience in corrosive and high-stress environments found in sectors like chemical processing, mining, oil & gas, and power generation. Polymeric concrete’s resistance to extreme pH conditions, chemicals, and thermal cycling makes it ideal for harsh industrial operations. Moreover, its role in reducing downtime through less frequent repairs gives it an edge over conventional concrete. As sustainability and resilience become key considerations, the infrastructure segment is poised for future growth due to increased investments in public works, smart cities, and resilient urban infrastructure.

Region Analysis:

Asia-Pacific holds over 30% Market Share In Polymeric Concrete Market: North America is a key player in the polymeric concrete market, with the U.S. leading the demand due to a strong construction sector and a focus on infrastructure upgrades. The region benefits from technological advancements and the adoption of high-performance concrete in industrial and commercial applications. The growing demand for infrastructure repairs, particularly in the U.S., has increased the adoption of polymeric concrete in highway, bridge, and sewage systems.

Europe is driven by the increasing demand for sustainable construction materials. Countries like Germany, France, and the U.K. are leading the way in adopting polymeric concrete, particularly in industrial and infrastructure applications.

Asia-Pacific is expected to experience the highest growth in the polymeric concrete market due to rapid urbanization, industrial growth, and infrastructure development in countries such as China, India, and Japan.

Latin America is gaining traction, driven by the construction boom and the need for infrastructure upgrades in countries like Brazil and Mexico. The Middle East & Africa (MEA) region is witnessing steady growth in the driven by infrastructure expansion, particularly in the UAE, Saudi Arabia, and South Africa.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product Class

- Polymer Impregnated Concrete (PIC)

- Polymer Resin Concrete (PMC)

- Polymer Cement Concrete (PCC)

By Polymer Type (Binder)

- Epoxy

- Vinyl Ester

- Polyester

- Furan

- Acrylate

- Latex

- Methyl Methacrylate (MMA)

- Others

By Application

- Flooring Blocks

- Trench Drains

- Pump Bases

- Waste Containers

- Chemical Containments

- Others

By End-use

- Commercial

- Industrial

- Residential

- Municipal

- Infrastructure

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 812.1 M |

| Forecast Revenue (2034) | USD 1,520.3 M |

| CAGR (2025-2034) | 7.5% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Class (Polymer Cement Concrete (PCC), Polymer Resin Concrete (PMC), Polymer Impregnated Concrete (PIC)), By Polymer Type (Epoxy, Vinylester, Polyester, Furan, Acrylate, Latex, Others), By Application (Flooring Blocks, Trench Drains, Pump Bases, Waste Containers, Chemical Containments, Others), By End-use (Commercial, Industrial, Residential, Municipal, Infrastructure) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Interplastic Corporation, Wacker Chemie AG, Lidco Building Technologies, ULMA Architectural Solutions, BASF SE, TPP Manufacturing Sdn. Bhd, Carborundum Universal Limited, ACO FUNKI A/S, Forte Composites Inc,, Polycare Namibia, Sika AG, Dudick Inc., Kwik Bond Polymers, ErgonArmor |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Polymer Type(Epoxy, Vinylester, Polyester, Furan, Acrylate, Latex, Others), Application(Flooring Blocks, Trench Drains, Pump Bases, Waste Containers, Chemical Containments, Others), End-use(Commercial, Industrial, Residential, Municipal, Infrastructure), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Polymer Type(Epoxy, Vinylester, Polyester, Furan, Acrylate, Latex, Others), Application(Flooring Blocks, Trench Drains, Pump Bases, Waste Containers, Chemical Containments, Others), End-use(Commercial, Industrial, Residential, Municipal, Infrastructure), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Polymer Type(Epoxy, Vinylester, Polyester, Furan, Acrylate, Latex, Others), Application(Flooring Blocks, Trench Drains, Pump Bases, Waste Containers, Chemical Containments, Others), End-use(Commercial, Industrial, Residential, Municipal, Infrastructure), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date