- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Post-Quantum Cryptography Market Size, Share | CAGR 36.5%

Global Post-Quantum Cryptography Market Size, Share, Analysis By Algorithm Type (Lattice-Based Cryptography, Code-Based Cryptography, Hash-Based Cryptography, Multivariate Cryptography, Isogeny-Based Cryptography, Hybrid Post-Quantum Cryptography Solutions), By Solution (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, End-User Vertical and Enterprise Size Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 1.02 Billion | USD 16.80 Billion | 36.5% | North America, 39.8% |

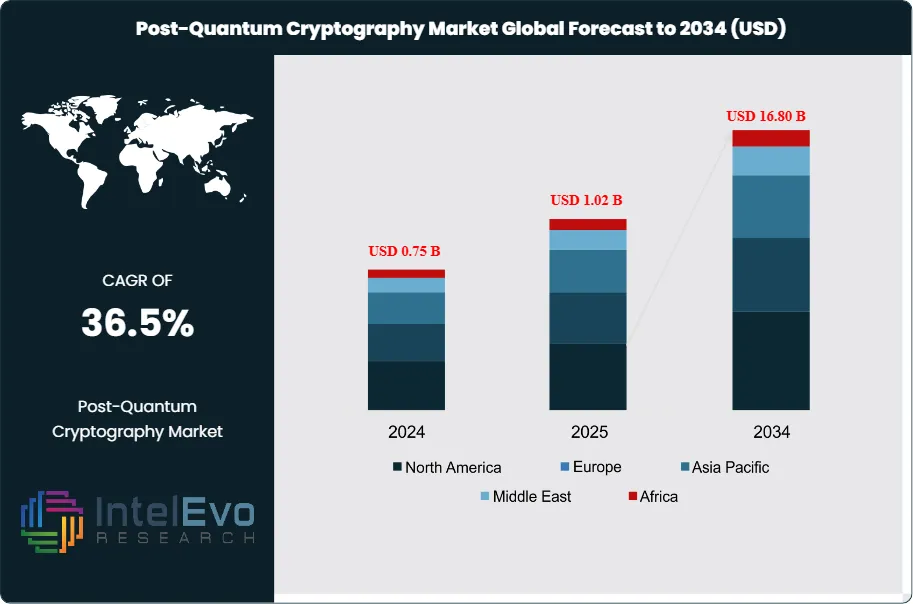

The Post-Quantum Cryptography Market was valued at approximately USD 0.75 Billion in 2024 and reached USD 1.02 Billion in 2025. The market is projected to grow to USD 16.80 Billion by 2034, expanding at a CAGR of 36.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.78 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportGrowth in the post-quantum cryptography market is anchored in three structural forces. First, the US National Institute of Standards and Technology finalized the first three post-quantum cryptography standards on August 13, 2024, with FIPS 203 covering ML-KEM (derived from CRYSTALS-Kyber), FIPS 204 covering ML-DSA (derived from CRYSTALS-Dilithium), and FIPS 205 covering SLH-DSA (derived from SPHINCS+), effectively setting the procurement baseline for federal and enterprise migration. Second, NIST selected HQC (Hamming Quasi-Cyclic) on March 11, 2025 as a fifth algorithm and backup key encapsulation mechanism to ML-KEM, with final standardization expected in 2027. Third, the harvest-now-decrypt-later threat model has moved encryption replacement forward for data with retention value beyond 2030, accelerating procurement across BFSI, defense, and critical infrastructure.

The regulatory environment for post-quantum cryptography is now framed by four binding instruments. The NSA's Commercial National Security Algorithm Suite 2.0 (CNSA 2.0) mandates migration of US national security systems beginning in 2025, with full compliance required by 2030 to 2035 depending on system class. A White House executive order required the CISA Director to publish, within 180 days of its July 14, 2025 issuance, a list of product categories where PQC support is widely available, and required federal agencies within 90 days (October 12, 2025) to ensure solicitations in those categories support PQC. The EU's NIS2 Directive (Directive (EU) 2022/2555), transposed across member states through 2024, raises cryptographic due-diligence bars for essential and important entities. Korea selected HAETAE and AIMer for digital signatures plus SMAUG-T and NTRU+ as KEMs in January 2025, and China is pursuing an autonomous PQC standardization track outside NIST.

Demand is consolidating around measurable deployment milestones. Cloudflare reported that hybrid post-quantum key agreements, combining ML-KEM with X25519, secured approximately 43% of human-generated TLS connections to its network by mid-September 2025, rising above 50% by late October 2025. More than 6 million Cloudflare-protected domains shipped quantum-safe by default by September 2025. PQShield co-authored all four initial NIST standards and raised USD 37 Million in 2024 Series B funding led by Addition, with customers including AMD, Microchip Technologies, Collins Aerospace, Lattice Semiconductor, Sumitomo Electric, NTT Data, and Mirise Technologies (Toyota/Denso R&D). The Linux Foundation launched the Post-Quantum Cryptography Alliance in February 2024 with AWS, Cisco, Google, IBM, and NVIDIA as founding members.

North America held the largest post-quantum cryptography market share at 39.8% in 2025, approximately USD 406 Million, anchored by IBM, Microsoft, AWS, SandboxAQ, Cloudflare, Palo Alto Networks, Entrust, and QuSecure. Europe held 26.4% through Thales, PQShield, NXP Semiconductors, IDEMIA, and Utimaco, and Asia Pacific held 25.8% through Samsung SDS, Korean PQC standardization under the Ministry of Science and ICT, and Chinese autonomous PQC programs. The technology roadmap through 2034 tilts toward lattice-based schemes led by ML-KEM and ML-DSA, complemented by code-based HQC and hash-based SLH-DSA for crypto-agility and algorithm diversification.

Market Definition & Scope

The post-quantum cryptography market is defined as the global commercial activity in cryptographic algorithms, libraries, hardware, services, and managed platforms designed to resist cryptanalytic attacks by sufficiently powerful quantum computers. The market encompasses NIST-standardized schemes including ML-KEM (FIPS 203), ML-DSA (FIPS 204), SLH-DSA (FIPS 205), FN-DSA (draft FIPS 206), and HQC selected March 11, 2025; quantum-safe hardware security modules from Thales, Entrust, Utimaco, and Crypto4A; PQC migration services; quantum-safe VPN and TLS platforms; and cryptographic inventory and discovery tooling.

Included in the scope are solution revenues (software libraries, SDKs, HSMs, orchestration platforms), service revenues (design, implementation, consulting, migration, risk assessment), and recurring subscription revenues tied to PQC-enabled products. Explicitly excluded are Quantum Key Distribution (QKD) hardware, classical symmetric cryptography such as AES-256, academic research without commercial product linkage, and general-purpose cybersecurity where PQC is not the primary delivered control. The post-quantum cryptography market is a subset of the broader global cryptography and encryption market and is adjacent to the larger managed cybersecurity services category.

, By Solution (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, End-User Vertical and Enterprise Size Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The post-quantum cryptography market expands from USD 1.02 Billion in 2025 to USD 16.80 Billion by 2034, a CAGR of 36.5% over the forecast period.

- Segment Dominance by Algorithm Type: Lattice-based cryptography led in 2025 with 49.3% share, anchored by ML-KEM (CRYSTALS-Kyber) and ML-DSA (CRYSTALS-Dilithium) under FIPS 203 and FIPS 204.

- Segment Dominance by Solution: Software libraries and SDKs held 41.2% of 2025 revenue, covering quantum-safe cryptographic libraries from PQShield, IBM, Microsoft, and open-source OpenSSL integrations.

- Driver: CNSA 2.0 mandates US national security system PQC migration from 2025 with full compliance by 2030 to 2035, and the White House July 14, 2025 executive order compressed federal procurement timelines.

- Restraint: Approximately 48% of organizations in North America and Europe are unprepared for quantum cybersecurity risks per a 2025 Keyfactor survey, constraining implementation velocity despite regulatory urgency.

- Opportunity: Migration services represent the fastest-growing sub-segment at approximately 46% CAGR through 2030, as enterprises require consulting, integration, and cryptographic-inventory expertise.

- Trend: Hybrid PQC deployment scaled through 2025, with Cloudflare exceeding 50% hybrid ML-KEM plus X25519 TLS 1.3 traffic share by late October 2025 across more than 6 million protected domains.

- Regional: North America led the post-quantum cryptography market with 39.8% share and approximately USD 406 Million in revenue in 2025, followed by Europe at 26.4%.

Key Insights Summary

- NIST released the first three finalized post-quantum cryptography standards on August 13, 2024, publishing FIPS 203 for ML-KEM (from CRYSTALS-Kyber), FIPS 204 for ML-DSA (from CRYSTALS-Dilithium), and FIPS 205 for SLH-DSA (from SPHINCS+), establishing the procurement baseline that underpins the 2025-2034 post-quantum cryptography market forecast.

- NIST selected HQC (Hamming Quasi-Cyclic) as the fifth post-quantum encryption algorithm on March 11, 2025, serving as a code-based backup key encapsulation mechanism to ML-KEM, with the final HQC standard expected for release in 2027 following a 90-day public comment period and NIST Post-Quantum Cryptography project leadership under mathematician Dustin Moody.

- Cloudflare reported that the majority of human-initiated TLS traffic on its network was secured by hybrid ML-KEM plus X25519 post-quantum key agreement by late October 2025, crossing the 50% threshold after Cloudflare automatically upgraded more than 6 million protected domains to hybrid PQC by default through 2025, per Cloudflare's research blog and SSL/TLS documentation.

- The White House issued an executive order on July 14, 2025 requiring the CISA Director to publish a list of product categories where PQC is widely available within 180 days, and requiring federal agencies by October 12, 2025 to ensure solicitations in those categories support PQC, with agencies directed to implement PQC or hybrid PQC key establishment where supported by existing network security products.

- Korea's Ministry of Science and ICT selected two KpqC signature algorithms (AIMer and HAETAE) and two KpqC KEM algorithms (SMAUG-T and NTRU+) for further development in January 2025, under a multi-stage PQC transition plan with pilot transitions scheduled between 2025 and 2028, per Korea's independent KpqC roadmap outside the NIST track.

- Approximately 48% of organizations across North America and Europe were unprepared for quantum cybersecurity risks per a 2025 Keyfactor survey, with roughly 85 US institutions participating in national PQC standardization work, 39% of US banks conducting crypto-agility assessments, and federal agencies managing more than 4.4 billion daily encrypted transactions requiring PQC upgrades, per 360 Research Reports.

- The Post-Quantum Cryptography Coalition (PQCC), co-founded by IBM Quantum, Microsoft, MITRE, PQShield, and SandboxAQ, and the Post-Quantum Cryptography Alliance (PQCA), launched in February 2024 by the Linux Foundation with AWS, Cisco, Google, IBM, and NVIDIA, collectively coordinate open-source PQC reference implementations and broader enterprise adoption.

Competitive Landscape Overview

The post-quantum cryptography market is fragmented with a rising incumbent-plus-specialist structure. The top four companies, IBM Corporation, Thales Group, NXP Semiconductors, and SandboxAQ, accounted for an estimated 41.6% of combined 2025 revenue based on public disclosures, partnership announcements, and cryptographic-IP installed-base positioning. Competition is technology-depth and standards-leadership led rather than price-led, because NIST standardization contributions and hardware-software co-design determine government and critical-infrastructure procurement outcomes more than sticker price on a PQC procurement checklist.

Competitive dynamics shifted materially through 2025 as hybrid PQC deployment crossed the 50% threshold on Cloudflare's network, the White House compressed federal PQC procurement timelines, and NIST selected HQC as the code-based backup. Strategic partnerships expanded: IBM-Vodafone integrated PQC into Vodafone Secure Net in March 2025, Thales-NxtGen brought PQC to India's sovereign cloud in May 2025, Korean Quantum Computing-Crypto4A partnered in July 2025 to commercialize PQC in Asia, and Quside-PQShield partnered in September 2024 to combine quantum random number generation with post-quantum key encapsulation. The Post-Quantum Cryptography Coalition and the Post-Quantum Cryptography Alliance aligned incumbents, specialists, and open-source projects around interoperable reference implementations and migration playbooks.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| IBM Corporation (NYSE: IBM) | United States | Leader | IBM Quantum Safe portfolio; HPCS PQC library; HSM integrations | North America, Europe | Partnered with Vodafone in March 2025 to integrate PQC into Vodafone Secure Net across mobile networks |

| Thales Group (EPA: HO) | France | Leader | Thales Luna HSM; CipherTrust Data Security Platform with ML-KEM | Europe, North America, APAC | Partnered with NxtGen in May 2025 to bring PQC to India's sovereign cloud for regulated workloads |

| NXP Semiconductors N.V. (NASDAQ: NXPI) | Netherlands | Leader | NXP SE05x secure elements; quantum-safe automotive chips | Europe, North America, APAC | Expanded quantum-safe semiconductor IP across automotive, industrial, and IoT lines through 2025 |

| SandboxAQ | United States | Leader | AQtive Guard; Cryptographic Inventory; AQProtect | North America, Europe | Co-founded the Post-Quantum Cryptography Coalition and hosted RWPQC 2025; raised over USD 1 Billion to date |

| PQShield Ltd | United Kingdom | Challenger | PQPlatform quantum-safe hardware IP and software SDKs | Europe, North America, APAC | Closed USD 37 Million Series B in 2024 led by Addition; co-authored NIST ML-KEM, ML-DSA, SLH-DSA standards |

| Cloudflare, Inc. (NYSE: NET) | United States | Challenger | Cloudflare One; hybrid ML-KEM TLS 1.3 at the edge | North America, Europe, APAC | Exceeded 50% hybrid post-quantum human TLS traffic share by late October 2025 across Cloudflare's network |

| Microsoft Corporation (NASDAQ: MSFT) | United States | Challenger | SymCrypt PQC library; Azure Key Vault ML-KEM; Microsoft Research PQC | North America, Europe, APAC | Co-founded the Post-Quantum Cryptography Coalition with IBM Quantum, MITRE, PQShield, and SandboxAQ |

| Palo Alto Networks, Inc. (NASDAQ: PANW) | United States | Challenger | Prisma SASE; Strata NGFW with PQC integrations | North America, Europe, APAC | Integrated PQC capabilities into security platforms through 2025 in alignment with CNSA 2.0 guidance |

| Entrust Corporation | United States | Niche Player | nShield HSM; Entrust Certificate Solutions with PQC roots | North America, Europe | Extended nShield HSM quantum-safe algorithm support and certificate lifecycle management through 2025 |

| QuSecure, Inc. | United States | Niche Player | QuProtect post-quantum orchestration platform | North America | Scaled QuProtect deployments across US federal and defense customers under CNSA 2.0 timelines |

Segmentation Analysis

The post-quantum cryptography market segments by algorithm type, solution, service, end-user vertical, and enterprise size. Each segmentation type maps to distinct buying criteria on a post-quantum cryptography procurement checklist, including NIST standardization status, algorithm diversity, hardware-software deployment footprint, and regulatory alignment with CNSA 2.0, NIS2, and national PQC roadmaps.

By Algorithm Type

Lattice-based cryptography led the post-quantum cryptography market at 49.3% share in 2025, approximately USD 503 Million, anchored by ML-KEM under FIPS 203 (derived from CRYSTALS-Kyber) and ML-DSA under FIPS 204 (derived from CRYSTALS-Dilithium). Lattice-based schemes dominate because of balanced performance, compact key sizes, and mature NIST third-round evaluation. Hash-based cryptography held 16.8%, anchored by SLH-DSA under FIPS 205 (derived from SPHINCS+), a stateless hash-based digital signature designed as a backup to ML-DSA with distinct mathematical foundations, and held by CSRC as a recommended backup for long-lifetime signatures.

Code-based cryptography held 12.4% of 2025 revenue and is among the fastest-growing sub-segments at approximately 45.3% CAGR through 2030, moving from academic niche to commercial deployment after NIST's March 11, 2025 selection of HQC (Hamming Quasi-Cyclic) as the fifth algorithm and Classic McEliece retaining its role for archival storage and satellite command links. Multivariate cryptography held 8.6%, anchored in specialty deployments, and isogeny-based cryptography held 2.1% after the SIKE failure shifted demand away from isogeny-based options. Other and hybrid combinations held 10.8%, including FN-DSA (FALCON) under the draft FIPS 206 standard.

By Solution

Software libraries and SDKs led the post-quantum cryptography market at 41.2% share in 2025, approximately USD 420 Million, including PQShield's PQPlatform libraries, IBM's quantum-safe open-source crypto libraries, Microsoft's SymCrypt PQC implementations, AWS's open-source PQC libraries, and open-source liboqs from the Open Quantum Safe project. Quantum-safe hardware held 22.8%, approximately USD 233 Million, including Thales Luna HSM PQC support, Entrust nShield HSM PQC cipher suites, Utimaco HSMs, Crypto4A quantum-safe HSMs, and quantum-safe secure elements from NXP.

Quantum-safe authentication and digital signatures held 13.4%, including DigiCert, Sectigo, and Entrust PQC-ready certificate solutions. Quantum-safe VPN and secure communications held 11.2%, including Cloudflare One SASE hybrid ML-KEM and American Binary CNSA 2.0-compliant enterprise VPN. Quantum-safe blockchain solutions held 6.8%, including Starkware and ISARA-aligned toolkits, and quantum-safe email and messaging held 4.6% across specialty platforms. The post-quantum cryptography ROI calculation typically combines regulatory avoidance cost, data-breach cost reduction, and crypto-agility premium into a weighted migration business case.

By Service

Design, implementation, and consulting services held the largest service share at 48.6% in 2025, approximately USD 496 Million, as enterprises lacked in-house cryptography skills to plan PQC migration. Migration services held 33.5% and represent the fastest-growing service sub-segment at approximately 46% CAGR through 2030, covering legacy-to-PQC transitions for cloud environments, IoT fleets, and critical infrastructure. Quantum risk assessment and cryptographic discovery held 12.3%, including SandboxAQ AQtive Guard deployments, InfoSec Global's Cryptographic Inventory, and Arqit Encryption Intelligence. Training, certification, and managed services held 5.6%, supporting the reported annual training of 2,400+ PQC migration professionals per 360 Research Reports.

By End-User Vertical

Government and defense held the largest post-quantum cryptography vertical share at 30.2% in 2025, approximately USD 308 Million, driven by CNSA 2.0 mandates, the July 14, 2025 White House executive order, and similar frameworks in the United Kingdom, Germany, France, Japan, and South Korea. BFSI held 26.4%, approximately USD 269 Million, as banks, insurers, and card networks prioritized PQC for financial-data retention beyond 2030 and began HSM refresh cycles. IT and ITES held 18.7%, led by Cloudflare, AWS, Microsoft Azure, and Google Cloud hyperscaler deployments.

Telecommunications held 11.2% and is positioned for the highest 44.07% CAGR through 2030 per Mordor Intelligence, driven by PQC integration across 5G-to-6G transport, as exemplified by Vodafone's partnership with IBM announced in March 2025. Healthcare held 7.4%, covering HIPAA-aligned long-term patient data retention. Retail and e-commerce held 3.8%, and other verticals including energy, utilities, and transportation held 2.3%. The post-quantum cryptography compliance requirements vary by vertical, with CNSA 2.0 in defense, NYDFS 23 NYCRR 500 in US financial services, and ENISA technical guidance applying to critical infrastructure in the EU.

By Enterprise Size

Large enterprises held 79.6% of the post-quantum cryptography market in 2025, approximately USD 812 Million, matching Vertex Market Research's estimate that large enterprises represent around 80% of PQC spend because they operate critical infrastructure and long-retention data that must survive the harvest-now-decrypt-later threat model. Small and medium enterprises held 20.4%, approximately USD 208 Million, with adoption lagging due to cryptography skill gaps and upfront migration cost. The fastest-growing enterprise-size sub-segment is mid-market BFSI and healthcare firms adopting managed PQC services from QuSecure, SandboxAQ, and specialist MSSPs, addressing the 48% of North American and European organizations reported unprepared for quantum cybersecurity risks per Keyfactor's 2025 survey.

Regional Analysis

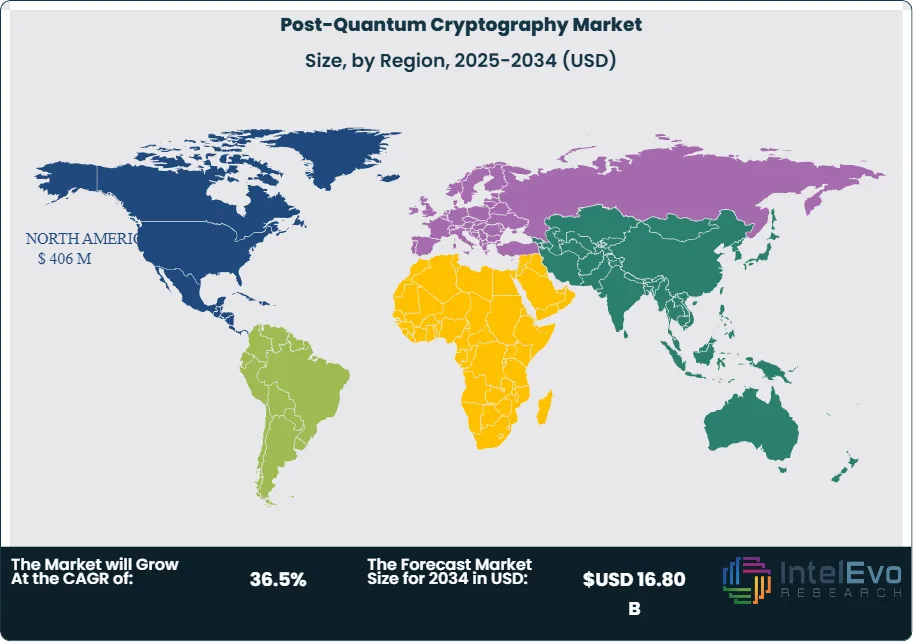

The post-quantum cryptography market is geographically led by North America, Asia Pacific, and Europe, together accounting for 92.0% of 2025 revenue. Regional dynamics differ on regulatory posture, sovereign cryptography programs, and vendor ecosystem maturity, with North America leading on standardization leadership and Asia Pacific recording the fastest growth.

North America

North America held 39.8% of the post-quantum cryptography market in 2025, approximately USD 406 Million. The United States dominates through IBM in Armonk, Microsoft in Redmond, AWS in Seattle, SandboxAQ in California, Cloudflare in San Francisco, Palo Alto Networks in Santa Clara, Entrust in Minneapolis, DigiCert in Lehi, and QuSecure in California. Canada hosts ISARA in Waterloo and evolutionQ. The NSA's CNSA 2.0 mandate requires US national security system PQC migration beginning in 2025, and the White House executive order of July 14, 2025 required federal agencies by October 12, 2025 to ensure PQC-supporting solicitations. The White House earmarked approximately USD 7.1 Billion for agency-wide PQC migration, mandating asset inventories and transition plans by 2026 per Mordor Intelligence's analysis. The US influences 41% of global PQC standardization decisions per 360 Research Reports.

Europe

Europe accounted for 26.4% of the post-quantum cryptography market in 2025, approximately USD 269 Million. France leads through Thales Group in Paris, IDEMIA, and CryptoNext Security; the United Kingdom leads through PQShield in Oxford, Arqit Quantum, and Post-Quantum Ltd; the Netherlands leads through NXP Semiconductors in Eindhoven; Germany hosts Utimaco; and Finland hosts Xiphera. The EU's NIS2 Directive (Directive (EU) 2022/2555) raised cryptographic due-diligence bars for essential and important entities through national transpositions in 2024. The European Union Agency for Cybersecurity (ENISA) published post-quantum cryptography integration technical guidance aligned with NIST's FIPS 203, 204, and 205. The EU AI Act's general-purpose AI provisions applied from August 2, 2025 and intersect with AI-enhanced cryptographic audit tools.

Asia Pacific

Asia Pacific held 25.8% of the post-quantum cryptography market in 2025, approximately USD 263 Million, and recorded the fastest regional growth at an estimated 46.55% CAGR through 2030 per Mordor Intelligence. South Korea leads through Samsung SDS and a Ministry of Science and ICT-led PQC transition plan with pilot transitions scheduled 2025 through 2028. Japan hosts NTT Data and Sumitomo Electric as PQShield customers and Fujitsu as a domestic cryptography supplier. China pursues an autonomous PQC standardization track outside NIST, with government-led investment in quantum computing and domestic cryptographic alternatives. Korean Quantum Computing partnered with Crypto4A in July 2025 to commercialize PQC and strengthen Korea's quantum security sovereignty. India's NxtGen-Thales partnership announced in May 2025 brings PQC to India's sovereign cloud for regulated AI and enterprise workloads.

Latin America

Latin America held 4.8% of the post-quantum cryptography market in 2025, approximately USD 49 Million. Brazil leads through federal banking modernization under Banco Central do Brasil guidance and enterprise adoption at Itau, Bradesco, and Banco do Brasil. Mexico follows with CNBV-regulated banking adoption, and Argentina and Colombia contribute smaller but growing deployments. Regional partnerships typically leverage IBM, Thales, Microsoft, and AWS as primary PQC suppliers, with limited domestic specialist vendors. Brazil's General Personal Data Protection Law (LGPD) and Mexico's Federal Law on Protection of Personal Data Held by Private Parties both influence cryptographic due-diligence obligations.

Middle East & Africa

Middle East & Africa accounted for 3.2% of the post-quantum cryptography market in 2025, approximately USD 33 Million. The United Arab Emirates leads regional adoption through the UAE Cybersecurity Council's national cybersecurity strategy, followed by Saudi Arabia supporting Vision 2030 digital transformation and Israel through its cybersecurity ecosystem including QED-it and QuantLR. South Africa leads sub-Saharan adoption, and Egypt contributes through Cairo-led fintech and telecoms. Regional sovereign cloud initiatives, including Thales's partnerships with regional system integrators, anchor the deployment roadmap. The Saudi National Cybersecurity Authority (NCA) and UAE NESA regulatory frameworks align with NIST FIPS 203, 204, and 205 baselines.

Country Analysis

Four national post-quantum cryptography markets, the United States, the United Kingdom, Germany, and China, collectively accounted for approximately 60.5% of 2025 revenue. These countries concentrate vendor headquarters, sovereign standardization programs, and the regulatory frameworks that set post-quantum cryptography procurement timelines.

United States

The United States represented approximately USD 365 Million in 2025 post-quantum cryptography revenue, with a country CAGR estimated at 36.1% through 2034. NIST under the Department of Commerce leads global PQC standardization through FIPS 203, 204, and 205 finalized August 13, 2024 and HQC selected March 11, 2025. The NSA issued CNSA 2.0 mandating US national security system PQC migration from 2025 with full compliance between 2030 and 2035, and the White House issued an executive order on July 14, 2025 compressing federal procurement timelines. CISA's October 2025 milestones required agencies to ensure PQC-supporting solicitations. IBM, Microsoft, AWS, SandboxAQ, Cloudflare, Palo Alto Networks, Entrust, DigiCert, and QuSecure anchor national supplier leadership. The United States leads PQC adoption with approximately 45% of global PQC patents and more than 190 federally supported quantum-resilient research programs per 360 Research Reports.

United Kingdom

The United Kingdom represented approximately USD 81 Million in 2025 post-quantum cryptography revenue, with a country CAGR estimated at 37.4% through 2034. PQShield in Oxford, Arqit Quantum Inc listed on NASDAQ, Post-Quantum Ltd, Quantum Dice, and KETS Quantum Security anchor national supplier leadership. The UK National Cyber Security Centre (NCSC) published PQC migration guidance aligned with NIST standards and timelines. The Information Commissioner's Office (ICO) oversees UK GDPR compliance for cryptographic data-protection. PQShield co-authored all four initial NIST standards including ML-KEM, ML-DSA, and SLH-DSA and advises the White House, European Parliament, and World Economic Forum. Government-led PQC investment under the UK National Quantum Strategy supports domestic specialist vendor scale-up.

Germany

Germany represented approximately USD 54 Million in 2025 post-quantum cryptography revenue, with a country CAGR estimated at 35.6% through 2034. Utimaco in Aachen anchors national HSM supplier leadership alongside Infineon Technologies' secure element PQC portfolio. The Bundesamt fur Sicherheit in der Informationstechnik (BSI) published PQC technical guidance aligned with NIST and ENISA benchmarks, and the BSI TR-02102 cryptographic recommendations updated through 2024 and 2025 provide German federal guidance for PQC algorithm selection. The Digital Services Act (DSA) and the EU Cyber Resilience Act (CRA), adopted in October 2024, jointly drive cryptographic-agility requirements across digital products sold into the German and wider EU market. Large enterprise adoption is led by SAP, Deutsche Bank, and Siemens.

China

China represented approximately USD 117 Million in 2025 post-quantum cryptography revenue, with a country CAGR estimated at 39.7% through 2034, the fastest among the four profiled countries. China pursues an autonomous PQC standardization track managed by the Office of State Commercial Cryptography Administration (OSCCA), separate from NIST. Domestic cryptographic suites including SM2, SM3, SM4, and SM9 are being evaluated for post-quantum hardening and hybrid PQC replacement. The Cyberspace Administration of China governs cross-border cryptographic data flows and enterprise deployment of PQC modules. Huawei, Alibaba, Tencent, and Baidu pilot PQC deployments in cloud, telecom, and fintech verticals, and government research institutes including the Institute of Information Engineering anchor national R&D leadership.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Algorithm Type

- Lattice-Based Cryptography

- Code-Based Cryptography

- Hash-Based Cryptography

- Multivariate Cryptography

- Isogeny-Based Cryptography

- Hybrid Post-Quantum Cryptography Solutions

By Solution

- Post-Quantum Encryption Solutions

- Quantum-Resistant Key Management Systems

- Secure Communication & VPN Solutions

- Digital Signature Solutions

- PKI Modernization & Certificate Management Solutions

- Cryptographic Discovery & Risk Assessment Platforms

By Service

- Consulting Services

- Integration & Deployment Services

- Migration & Cryptographic Modernization Services

- Managed Security Services

- Training & Support Services

By End-User Vertical

- BFSI

- Government & Defense

- IT & Telecommunications

- Healthcare & Life Sciences

- Energy & Utilities

- Manufacturing

- Retail & E-Commerce

- Aerospace & Critical Infrastructure

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.02 B |

| Forecast Revenue (2034) | USD 16.80 B |

| CAGR (2025-2034) | 36.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Algorithm Type, (Lattice-Based Cryptography, Code-Based Cryptography, Hash-Based Cryptography, Multivariate Cryptography, Isogeny-Based Cryptography, Hybrid Post-Quantum Cryptography Solutions), By Solution, (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, (Consulting Services, Integration & Deployment Services, Migration & Cryptographic Modernization Services, Managed Security Services, Training & Support Services), By End-User Vertical, (BFSI, Government & Defense, IT & Telecommunications, Healthcare & Life Sciences, Energy & Utilities, Manufacturing, Retail & E-Commerce, Aerospace & Critical Infrastructure), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IBM CORPORATION (NYSE: IBM), THALES GROUP (EPA: HO), NXP SEMICONDUCTORS N.V. (NASDAQ: NXPI), SANDBOXAQ, PQSHIELD LTD, CLOUDFLARE, INC. (NYSE: NET), MICROSOFT CORPORATION (NASDAQ: MSFT), AMAZON WEB SERVICES, INC. (AWS), PALO ALTO NETWORKS, INC. (NASDAQ: PANW), ENTRUST CORPORATION, QUSECURE, INC., ARQIT QUANTUM INC. (NASDAQ: ARQQ), DIGICERT, INC., IDEMIA SECURE TRANSACTIONS, CRYPTO4A TECHNOLOGIES, INC., UTIMACO MANAGEMENT GMBH, ISARA CORPORATION, INFOSEC GLOBAL, QUANTUM XCHANGE, INC., SAMSUNG SDS CO., LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Solution (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, End-User Vertical and Enterprise Size Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Solution (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, End-User Vertical and Enterprise Size Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Solution (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, End-User Vertical and Enterprise Size Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Post-Quantum Cryptography Market?

The Global Post-Quantum Cryptography Market was valued at USD 0.75 Billion in 2024 and is projected to reach USD 16.80 Billion by 2034, growing at a CAGR of 36.5% from 2026 to 2034. Growth is driven by rising quantum computing threats, adoption of quantum-resistant encryption, NIST post-quantum standards, cryptographic modernization initiatives, secure communications, quantum-safe cybersecurity solutions, government regulations, and increasing investments in next-generation data protection technologies.

Who are the major players in the Post-Quantum Cryptography Market?

IBM CORPORATION (NYSE: IBM), THALES GROUP (EPA: HO), NXP SEMICONDUCTORS N.V. (NASDAQ: NXPI), SANDBOXAQ, PQSHIELD LTD, CLOUDFLARE, INC. (NYSE: NET), MICROSOFT CORPORATION (NASDAQ: MSFT), AMAZON WEB SERVICES, INC. (AWS), PALO ALTO NETWORKS, INC. (NASDAQ: PANW), ENTRUST CORPORATION, QUSECURE, INC., ARQIT QUANTUM INC. (NASDAQ: ARQQ), DIGICERT, INC., IDEMIA SECURE TRANSACTIONS, CRYPTO4A TECHNOLOGIES, INC., UTIMACO MANAGEMENT GMBH, ISARA CORPORATION, INFOSEC GLOBAL, QUANTUM XCHANGE, INC., SAMSUNG SDS CO., LTD., Others

Which segments covered the Post-Quantum Cryptography Market?

By Algorithm Type, (Lattice-Based Cryptography, Code-Based Cryptography, Hash-Based Cryptography, Multivariate Cryptography, Isogeny-Based Cryptography, Hybrid Post-Quantum Cryptography Solutions), By Solution, (Post-Quantum Encryption Solutions, Quantum-Resistant Key Management Systems, Secure Communication & VPN Solutions, Digital Signature Solutions, PKI Modernization & Certificate Management Solutions, Cryptographic Discovery & Risk Assessment Platforms), By Service, (Consulting Services, Integration & Deployment Services, Migration & Cryptographic Modernization Services, Managed Security Services, Training & Support Services), By End-User Vertical, (BFSI, Government & Defense, IT & Telecommunications, Healthcare & Life Sciences, Energy & Utilities, Manufacturing, Retail & E-Commerce, Aerospace & Critical Infrastructure), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Post-Quantum Cryptography Market

Published Date : 03 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date