- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Prefilled Syringe Manufacturing Market Size & Forecast | CAGR 12.1%

Global Prefilled Syringe Manufacturing Market Size, Share, Growth & Industry Analysis By Material Type (Glass Borosilicate Type I Syringes, Polymer COP/COC Syringes, Dual-Chamber & Combination Systems), By Application (Biologics & Biosimilars including GLP-1, Vaccines, Small-Molecule Injectables, Ophthalmology), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 9.84 Billion | USD 27.62 Billion | 12.1% | Europe, 36.8% |

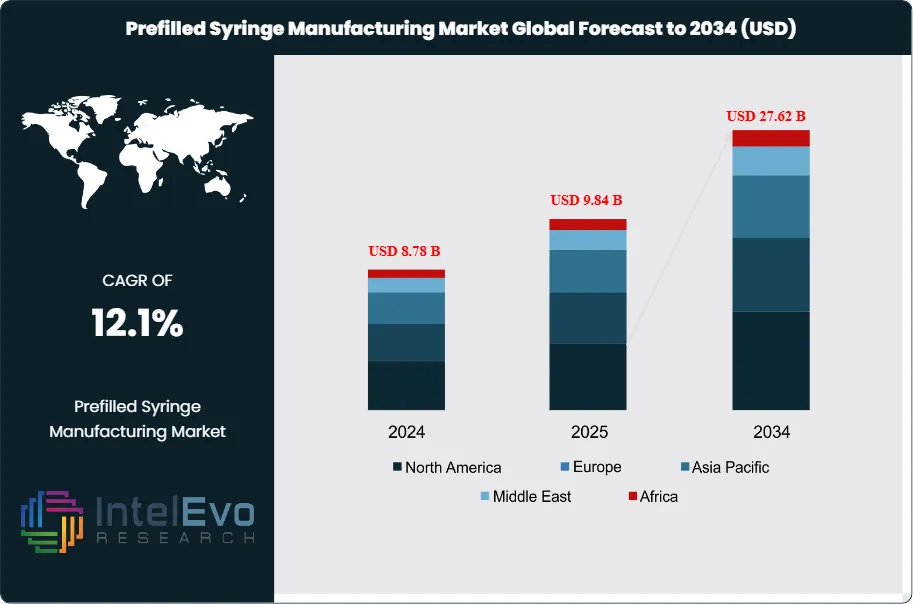

The Prefilled Syringe Manufacturing Market was valued at approximately USD 8.78 Billion in 2024 and reached USD 9.84 Billion in 2025. The market is projected to grow to USD 27.62 Billion by 2034, expanding at a CAGR of 12.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 17.78 Billion over the analysis period, driven by the convergence of three powerful commercial forces: the unprecedented commercial success of GLP-1 receptor agonist therapies, the continued expansion of biologic and biosimilar injectable drug markets, and a structural patient preference shift toward self-injection drug delivery formats that prefilled syringes and auto-injectors serve more effectively than vials.

Get More Information about this report -

Request Free Sample ReportPrefilled syringes are primary drug containers that arrive from the manufacturer pre-filled with a specified drug dose, eliminating the need for pharmacist or nurse reconstitution at the point of care. They are available in two primary configurations: glass syringes, which dominate commercial pharmaceutical manufacturing and have established regulatory precedent across FDA, EMA, and PMDA; and polymer (COP/COC) syringes, which are gaining adoption for biologics where silicone oil interactions or oxygen permeability concerns preclude glass. The prefilled syringe manufacturing market encompasses the fabrication, aseptic filling, stoppering, staked-needle assembly, inspection, packaging, and finished device release of these primary containers across both staked-needle and Luer-lock configurations.

The primary demand catalyst in the prefilled syringe manufacturing market is the commercial scale-up of GLP-1 receptor agonists. Semaglutide (Novo Nordisk's Ozempic and Wegovy) and tirzepatide (Eli Lilly's Mounjaro and Zepbound) collectively generated over USD 35 Billion in annual revenue in 2025, with volumes measured in hundreds of millions of prefilled auto-injector units per year. The manufacturing supply chain for these products is centered on prefilled syringe components — specifically the glass or polymer syringe barrel that serves as the primary container within the auto-injector device. Demand has materially outpaced supply, prompting a capital expenditure wave of historic proportions from Novo Nordisk, Eli Lilly, and their glass and device component suppliers including BD, Gerresheimer, and Schott.

Regulatory forces are tightening quality requirements for prefilled syringe manufacturing. FDA's guidance on container closure integrity and its evolving extractables and leachables (E&L) requirements under USP Chapter 1664 are raising the specification bar for glass syringe suppliers. EU GMP Annex 1 (effective August 2023) mandates isolator-based aseptic filling environments and automated container handling for all new prefilled syringe fill-finish lines, directly driving capital investment in modernized manufacturing infrastructure. ISO 11040, the international standard for prefilled syringes, continues to be updated to reflect new syringe configurations and testing requirements.

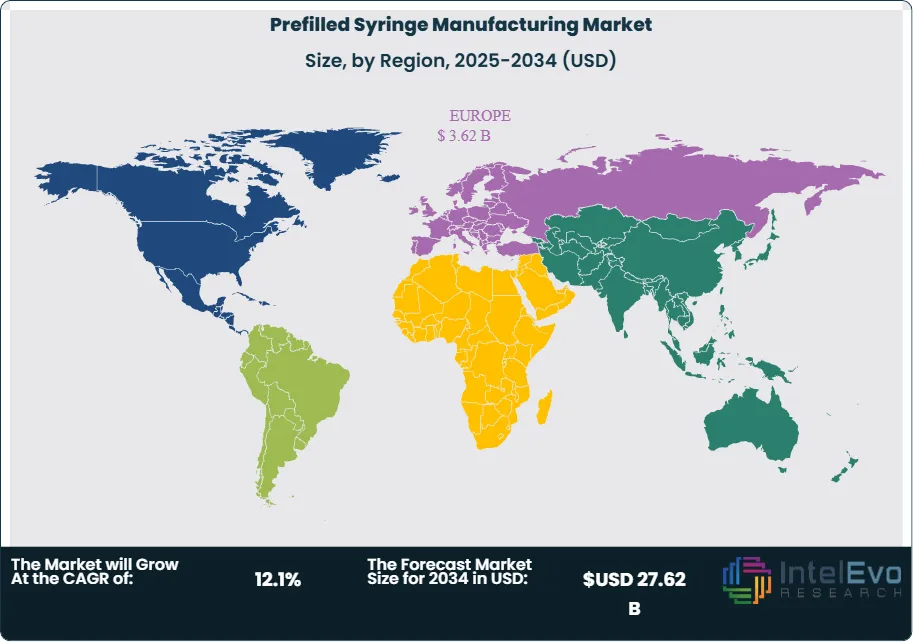

Europe leads the prefilled syringe manufacturing market with a 36.8% share in 2025, driven by Germany, France, and Italy as primary glass syringe manufacturing hubs and by Switzerland's large-scale biologic fill-finish operations. North America is the second-largest region at 32.4%, while Asia Pacific is the fastest-growing at a projected CAGR of 15.2% through 2034. The prefilled syringe manufacturing market is characterized by deep interdependency between glass primary container manufacturers, syringe component suppliers, and fill-finish CDMOs — a supply chain structure that is under acute capacity pressure through at least 2028 due to GLP-1 volume demands.

, By Application (Biologics & Biosimilars including GLP-1, Vaccines, Small-Molecule Injectables, Ophthalmology), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global prefilled syringe manufacturing market was valued at USD 9.84 Billion in 2025 and is projected to reach USD 27.62 Billion by 2034, growing at a CAGR of 12.1% over the forecast period 2026–2034.

- Segment Dominance: By material type, glass prefilled syringes lead with approximately 72.4% of market revenue in 2025, underpinned by their established regulatory acceptance, superior oxygen barrier properties, and compatibility with the broad portfolio of approved injectable biologic products.

- Segment Dominance: By application, biologics and biosimilars account for the largest application share at 54.6% of prefilled syringe manufacturing market revenue in 2025, as the proliferation of subcutaneous self-injection biologic formats — including mAb biosimilars and GLP-1 agonists — drives syringe volume demand.

- Driver: GLP-1 receptor agonist commercial demand — with semaglutide and tirzepatide generating over USD 35 Billion in combined annual revenue in 2025 — is the single most powerful demand catalyst in the prefilled syringe manufacturing market, creating an acute capacity shortage that primary container suppliers and fill-finish CDMOs are racing to address through multi-billion-dollar capital programs.

- Restraint: Glass primary container supply constraints, concentrated in a limited number of global glass tube manufacturers including Schott and Nipro, are creating 12–18 month lead-time extensions for pharmaceutical-grade borosilicate glass syringe barrels, limiting the rate at which new prefilled syringe fill-finish capacity can be brought online.

- Opportunity: The polymer (COP/COC) prefilled syringe segment represents an incremental addressable opportunity exceeding USD 4.8 Billion through 2034, as biologic drug developers and fill-finish CDMOs adopt polymer syringes for applications where silicone oil-free environments, break-resistance, and enhanced oxygen barrier properties are required.

- Trend: Integration of prefilled syringes into connected auto-injector and wearable drug delivery device platforms is accelerating, with approximately 28.4% of new prefilled syringe fill-finish projects in 2025 incorporating device integration specifications — compared to 11.6% in 2019 — as pharmaceutical companies develop combination drug-device products targeting chronic disease self-administration.

- Regional Analysis: Europe leads the global prefilled syringe manufacturing market with a 36.8% share in 2025, generating approximately USD 3.62 Billion in revenue, anchored by Germany's glass syringe manufacturing base and Switzerland's large-capacity biologic prefilled syringe fill-finish infrastructure.

Competitive Landscape Overview

The prefilled syringe manufacturing market is moderately consolidated at the primary container level, with the top four glass syringe suppliers — Becton Dickinson (BD), Gerresheimer AG, Schott Pharma, and NIPRO Corporation — collectively holding approximately 61.4% of global glass syringe supply revenue in 2025. On the fill-finish CDMO side, competition is more fragmented. The glass primary container supply is highly concentrated, with Schott and Nipro controlling the majority of global pharmaceutical borosilicate glass tube supply, creating significant upstream leverage. Competitive intensity has increased substantially since 2022 as GLP-1 demand has created acute capacity pressure, with all major glass syringe manufacturers running multi-billion-dollar capacity expansion programs simultaneously.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| Becton Dickinson (BD) | USA | Leader | BD Uniject Prefillable Drug Delivery System | North America / Global | Mar 2025: Announced USD 1.1 Billion investment in glass syringe manufacturing capacity expansion at US and European facilities to meet GLP-1 agonist demand. |

| Gerresheimer AG | Germany | Leader | Gx RTF Prefillable Glass Syringe | Europe / Global | Jan 2025: Commissioned a new high-speed glass syringe production line in Pfreimd, Germany, adding 200 Million syringe units per year of pharmaceutical-grade output. |

| Schott Pharma | Germany | Leader | SCHOTT adaptiQ Glass Syringe | Europe / Global | Jun 2025: Launched adaptiQ 2.0 — an optimized glass syringe platform with improved silicone coating uniformity targeting high-concentration biologic drug product compatibility. |

| NIPRO Corporation | Japan | Leader | NIPRO Prefilled Syringe Systems | Asia Pacific / Global | Apr 2025: Broke ground on a USD 320 Million glass syringe tube and barrel manufacturing facility in the United States to supply North American GLP-1 and biologic fill-finish demand. |

| West Pharmaceutical Services | USA | Challenger | West FluroTec Syringe Components | North America / Europe | Feb 2026: Launched an upgraded FluroTec plunger stopper series for high-concentration biologic prefilled syringes, targeting reduced silicone interaction in sensitive protein formulations. |

| Vetter Pharma | Germany | Challenger | Vetter Prefilled Syringe Fill-Finish | Europe / North America | Sep 2025: Commissioned new pre-filled syringe fill-finish capacity adding 30 Million syringe units per year at its Ravensburg facility, targeting GLP-1 and biosimilar fill demand. |

| SiO2 Medical Products | USA | Challenger | SiO2 Polymer-Glass Hybrid Syringe | North America | Nov 2024: Secured a multi-year supply agreement with a major biopharma company for SiO2-coated polymer prefilled syringes targeting silicone oil-free biologic drug applications. |

| Stevanato Group | Italy | Challenger | Nexa Prefillable Glass Syringe | Europe / Global | May 2025: Opened a new integrated glass syringe manufacturing campus in Piombino Dese, Italy, with annual capacity of 400 Million prefillable syringe units. |

| Catalent | USA | Niche Player | Catalent Biologics PFS Fill-Finish | North America | Jan 2025: Integrated Bloomington, Indiana PFS fill-finish capacity into Novo Holdings manufacturing network, primarily serving Novo Nordisk's GLP-1 syringe supply chain. |

| Owen Mumford | UK | Niche Player | Aidaptus Auto-Injector Platform | Europe / North America | Jul 2025: Expanded Aidaptus auto-injector platform compatibility to accommodate larger-volume (2 mL) prefilled syringes for high-dose biologic and GLP-1 drug applications. |

By Material Type

The prefilled syringe manufacturing market by material type is led by glass prefilled syringes, which account for approximately 72.4% of total market revenue in 2025, valued at USD 7.12 Billion. Borosilicate glass (Type I) is the established standard material for pharmaceutical primary containers, offering chemical resistance, optical clarity for visual inspection, and oxygen barrier properties that meet USP and EP pharmacopoeial requirements for parenteral drug packaging. Glass syringes are manufactured from tubing produced by a small number of specialized glass tube manufacturers — principally Schott and Nipro — which process pharmaceutical-grade borosilicate rods into precision tubular blanks that syringe manufacturers then form, wash, and siliconize. The dominance of glass reflects its decades of regulatory acceptance across FDA, EMA, PMDA, and NMPA — with a validated safety and compatibility track record for hundreds of approved parenteral drug products — and the investment pharmaceutical companies have made in glass-compatible formulation and container closure validation. Glass syringe demand is growing at approximately 11.4% annually through 2034, driven primarily by GLP-1 agonist volume requirements.

Polymer prefilled syringes, manufactured from cyclic olefin polymer (COP) or cyclic olefin copolymer (COC), represent 21.8% of market revenue in 2025 at USD 2.14 Billion and are the fastest-growing material segment with a projected CAGR of 15.8% through 2034. Polymer syringes offer critical advantages for specific applications: they are silicone oil-free when not siliconized, reducing the risk of silicone-induced protein aggregation in sensitive biologic formulations; they are break-resistant, improving safety in home self-injection settings; and they offer superior oxygen and moisture barrier properties in certain COP formulations. The polymer syringe market is primarily served by Daikyo Seiko (a DATWYLER subsidiary), West Pharmaceutical Services' Crystal Zenith product, and SiO2 Medical Products' hybrid glass-polymer platform. Combination and specialty syringe systems, including dual-chamber syringes for lyophilized drug reconstitution, account for the remaining 5.8% of market revenue.

By Application

By application, biologics and biosimilars account for 54.6% of prefilled syringe manufacturing market revenue in 2025 at USD 5.37 Billion. This segment encompasses subcutaneous monoclonal antibody products, bispecific antibodies, biosimilar adalimumab, etanercept, and bevacizumab products, GLP-1 receptor agonists, and a growing portfolio of emerging biologic modalities including peptide-drug conjugates and new protein therapeutics. The conversion of biologic drug products from intravenous to subcutaneous administration formats — a strategy pursued by virtually every major biologic drug developer to extend product lifecycle and improve patient convenience — directly increases prefilled syringe volume demand, as subcutaneous delivery requires a prefillable container rather than a multi-dose infusion bag. GLP-1 receptor agonists are the dominant individual product category within this segment, with the combined volume of Ozempic, Wegovy, Mounjaro, and Zepbound requiring hundreds of millions of prefilled syringe units annually from their fill-finish supply chains.

Small-molecule injectable drugs represent 26.8% of market revenue in 2025 at USD 2.64 Billion, encompassing analgesics, anticoagulants, hormones (including insulin, which uses cartridges as well as prefilled syringes), and other small-molecule parenterals where dose convenience drives prefilled syringe adoption. Vaccine applications account for 12.4% of market revenue at USD 1.22 Billion, with routine immunization programs, travel vaccines, and pandemic preparedness stockpiling all contributing to prefilled syringe procurement. The remaining 6.2% of market revenue is distributed across specialty and ophthalmology applications, including intravitreal injection syringes for anti-VEGF biologics such as ranibizumab and faricimab, where the miniaturized syringe format is a critical product specification.

By End-User

By end-user, pharmaceutical and biopharmaceutical manufacturers are the largest customer segment within the prefilled syringe manufacturing market, generating 50.8% of total revenue in 2025 at USD 5.00 Billion. These manufacturers procure glass and polymer syringe components from primary container suppliers and contract their filling to either internal fill-finish sites or CDMOs. Large integrated companies including Novo Nordisk, Eli Lilly, AbbVie, Amgen, and Pfizer are among the highest-volume prefilled syringe consumers globally, with combined annual syringe procurement volumes in the billions of units. CDMOs represent 34.6% of market revenue at USD 3.40 Billion, serving as fill-finish providers for pharmaceutical companies that outsource syringe filling operations. CDMO demand for prefilled syringe fill-finish services is growing rapidly as biotech companies and mid-sized pharmaceutical manufacturers without proprietary fill-finish infrastructure choose outsourced partners with established prefilled syringe capabilities. Institutional buyers including hospital pharmacies, government health agencies, and public vaccination programs account for the remaining 14.6% of market revenue.

Regional Analysis

Europe Prefilled Syringe Manufacturing Market

Europe holds the leading position in the global prefilled syringe manufacturing market with a 36.8% share in 2025, generating approximately USD 3.62 Billion in revenue. The region's leadership reflects its role as the primary manufacturing hub for glass syringe primary containers, with Germany hosting the global production facilities of Schott Pharma and Gerresheimer — the two most significant glass syringe suppliers globally by volume. Gerresheimer's Pfreimd and Bünde facilities and Schott Pharma's Müllheim and other European sites collectively produce billions of pharmaceutical-grade glass syringe units annually, serving both European fill-finish operations and export markets. France contributes significantly to European prefilled syringe manufacturing through its established pharmaceutical packaging industry and injectable drug fill-finish sector. Switzerland, hosting Novartis, Roche, and major CDMOs including Lonza, represents a high-value fill-finish market for prefilled syringes targeting biologics. Italy's Stevanato Group has invested USD 400 Million+ in glass syringe manufacturing capacity between 2022 and 2025, positioning the company to capture incremental demand from GLP-1 agonist and biosimilar supply chains. EU GMP Annex 1 compliance has driven widespread prefilled syringe fill-finish line modernization across European pharmaceutical manufacturers since 2023. Europe's prefilled syringe manufacturing market is projected to grow at a 11.4% CAGR through 2034.

North America Prefilled Syringe Manufacturing Market

North America represents 32.4% of the global prefilled syringe manufacturing market in 2025 at approximately USD 3.19 Billion. The United States is the dominant national market, hosting major prefilled syringe fill-finish CDMOs and the North American operations of all leading glass syringe primary container suppliers. BD's US manufacturing operations — including sites in New Jersey and South Carolina — represent the largest domestic glass syringe supply source. The FDA's regulatory framework for primary container integrity testing, extractables and leachables assessment, and container closure system validation under 21 CFR Part 211 drives consistent demand for FDA-compliant glass syringe qualification at fill-finish sites. The GLP-1 agonist supply chain has created extraordinary demand pressure on North American prefilled syringe fill-finish capacity, with Eli Lilly and Novo Nordisk both constructing dedicated US-based manufacturing sites for their GLP-1 products. NIPRO's announced USD 320 Million US glass syringe facility will add domestic glass primary container supply capacity from approximately 2027, partially relieving import dependency on European glass suppliers. Canada and Mexico contribute modestly to regional demand through pharmaceutical manufacturing exports. North America's prefilled syringe manufacturing market is projected to grow at a 12.4% CAGR through 2034.

Asia Pacific Prefilled Syringe Manufacturing Market

Asia Pacific accounts for 21.6% of the global prefilled syringe manufacturing market in 2025 at USD 2.13 Billion and is the fastest-growing region with a projected CAGR of 15.2% through 2034. Japan is the dominant national market within the region, hosting NIPRO Corporation — one of the world's largest glass syringe manufacturers — as well as Daikyo Seiko, which supplies polymer syringe systems (Crystal Zenith, in partnership with West Pharmaceutical Services) to global pharmaceutical markets. Japan's domestic pharmaceutical sector also generates meaningful prefilled syringe demand for biosimilars and specialty injectables. China is the fastest-growing individual country market, where domestic biologic manufacturers and CDMOs are investing in GMP-compliant prefilled syringe fill-finish capacity to serve both domestic market growth and global pharmaceutical outsourcing clients. China's growing domestic biosimilar pipeline — with NMPA approvals of monoclonal antibody biosimilars accelerating since 2022 — is a specific driver of prefilled syringe adoption. India's pharmaceutical sector, while primarily oriented toward tablet and capsule generic manufacturing, is building sterile injectable capacity including prefilled syringe fill-finish under the PLI scheme. South Korea's Samsung Biologics and Celltrion have each invested in prefilled syringe fill-finish capability to serve their global CDMO and biosimilar commercialization pipelines.

Latin America Prefilled Syringe Manufacturing Market

Latin America holds a 5.4% share of the prefilled syringe manufacturing market in 2025 at approximately USD 0.53 Billion. Brazil is the dominant regional market, with ANVISA-regulated pharmaceutical manufacturers and public health institutions procuring prefilled syringes primarily for vaccine programs and biologic drug distribution. Brazil's national immunization program, one of the largest in the world by dose volume, drives sustained prefilled syringe procurement for routine and campaign vaccination — though many vaccine prefilled syringe volumes are procured through international supply arrangements rather than domestic manufacturing. Mexico's pharmaceutical sector contributes to regional demand through its sterile injectable manufacturing and fill-finish capabilities. Argentina's domestic pharmaceutical industry includes several manufacturers with prefilled syringe fill-finish capacity for regional market supply. Latin America's prefilled syringe manufacturing market is primarily a procurement market rather than a primary container manufacturing market, as the region hosts no major glass syringe tube manufacturers. Growth is supported by biosimilar market development, expanding private healthcare access, and government biologic procurement programs. The region's market is projected to grow at a 10.2% CAGR through 2034.

Middle East & Africa Prefilled Syringe Manufacturing Market

The Middle East and Africa region accounts for 3.8% of global prefilled syringe manufacturing market revenue in 2025 at approximately USD 0.37 Billion. Saudi Arabia, the UAE, and South Africa are the primary markets within the region. GCC pharmaceutical manufacturing programs under Vision 2030 and equivalent national strategies are building sterile drug product manufacturing capacity that includes prefilled syringe fill-finish capability, with government-sponsored investment in GMP infrastructure creating early-stage domestic demand. Saudi Arabia's SFDA and UAE health regulators have adopted GMP standards aligned with international requirements, enabling regulatory acceptance of domestically filled prefilled syringes. South Africa's pharmaceutical manufacturing sector serves both domestic and pan-African distribution, with several manufacturers operating prefilled syringe fill-finish capacity for vaccine and injectable drug programs. The MEA region's prefilled syringe market remains primarily import-dependent for glass primary containers, as no glass syringe tube manufacturing capacity exists within the region. International suppliers including BD, Gerresheimer, and Schott serve MEA pharmaceutical manufacturers through distribution networks and direct supply agreements. MEA's prefilled syringe manufacturing market is projected to grow at a 12.6% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Glass Prefilled Syringes (Borosilicate Type I)

- Polymer Prefilled Syringes (COP/COC)

- Combination & Specialty Syringe Systems (Dual-Chamber, Hybrid)

By Application

- Biologics & Biosimilars (including GLP-1 Agonists)

- Small-Molecule Injectable Drugs

- Vaccines

- Specialty & Ophthalmology Applications

By End-User

- Pharmaceutical & Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Hospital Pharmacies & Institutional Buyers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.84 B |

| Forecast Revenue (2034) | USD 27.62 B |

| CAGR (2025-2034) | 12.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type, (Glass Prefilled Syringes (Borosilicate Type I), Polymer Prefilled Syringes (COP/COC), Combination & Specialty Syringe Systems (Dual-Chamber, Hybrid)), By Application, (Biologics & Biosimilars (including GLP-1 Agonists), Small-Molecule Injectable Drugs, Vaccines, Specialty & Ophthalmology Applications), By End-User, (Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Hospital Pharmacies & Institutional Buyers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BECTON DICKINSON (BD), GERRESHEIMER AG, SCHOTT PHARMA, NIPRO CORPORATION, WEST PHARMACEUTICAL SERVICES, VETTER PHARMA, SIO2 MEDICAL PRODUCTS, STEVANATO GROUP, CATALENT, OWEN MUMFORD, DAIKYO SEIKO (DATWYLER), APTAR PHARMA, HASELMEIER, TERUMO CORPORATION, HINDUSTAN SYRINGES & MEDICAL DEVICES (HMD), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Biologics & Biosimilars including GLP-1, Vaccines, Small-Molecule Injectables, Ophthalmology), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

, By Application (Biologics & Biosimilars including GLP-1, Vaccines, Small-Molecule Injectables, Ophthalmology), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

, By Application (Biologics & Biosimilars including GLP-1, Vaccines, Small-Molecule Injectables, Ophthalmology), By End-User (Pharma, CDMOs, Hospitals) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Prefilled Syringe Manufacturing Market?

Global Prefilled syringe manufacturing market valued at USD 8.78B in 2024, reaching USD 27.62B by 2034, growing at a CAGR of 12.1% from 2026–2034.

Who are the major players in the Prefilled Syringe Manufacturing Market?

BECTON DICKINSON (BD), GERRESHEIMER AG, SCHOTT PHARMA, NIPRO CORPORATION, WEST PHARMACEUTICAL SERVICES, VETTER PHARMA, SIO2 MEDICAL PRODUCTS, STEVANATO GROUP, CATALENT, OWEN MUMFORD, DAIKYO SEIKO (DATWYLER), APTAR PHARMA, HASELMEIER, TERUMO CORPORATION, HINDUSTAN SYRINGES & MEDICAL DEVICES (HMD), Others

Which segments covered the Prefilled Syringe Manufacturing Market?

By Material Type, (Glass Prefilled Syringes (Borosilicate Type I), Polymer Prefilled Syringes (COP/COC), Combination & Specialty Syringe Systems (Dual-Chamber, Hybrid)), By Application, (Biologics & Biosimilars (including GLP-1 Agonists), Small-Molecule Injectable Drugs, Vaccines, Specialty & Ophthalmology Applications), By End-User, (Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Hospital Pharmacies & Institutional Buyers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Prefilled Syringe Manufacturing Market

Published Date : 05 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date