- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Pressure Gauge Market Size, Share & Forecast 2025–2034 | 3.19% CAGR

Global Pressure Gauge Market Size, Share, Analysis By Output Type (Analog Pressure Gauges, Digital Pressure Gauges), By Technology (Piezoresistive Pressure Gauges, Capacitive Pressure Gauges, Electromagnetic Pressure Gauges, Optical Pressure Gauges, Other Technologies), By Application (Aerospace & Defense, Automotive, Healthcare, Other Industrial Applications) Industry Region & Key Players – Market Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034

Report Overview

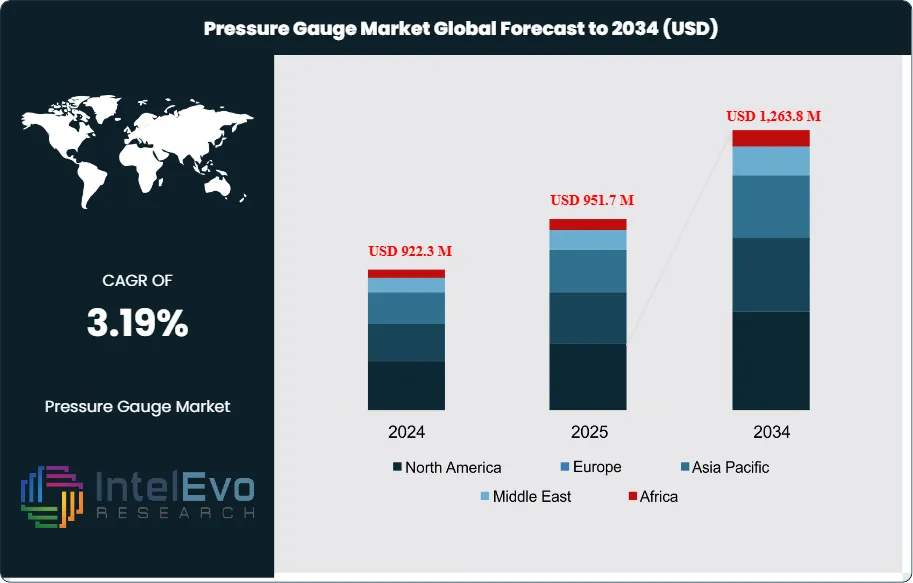

The Pressure Gauge Market was valued at USD 922.3 Million in 2024 and is estimated to reach approximately USD 951.7 Million in 2025. Driven by increasing demand for reliable pressure monitoring across industries such as oil & gas, manufacturing, power generation, and chemical processing, the market is projected to grow from about USD 982.0 Million in 2026 to nearly USD 1,263.8 Million by 2034, registering a compound annual growth rate (CAGR) of around 3.19% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportPressure gauges remain core to safe, compliant control of fluids and gases across oil and gas, manufacturing, automotive, aerospace, and process industries. Demand is rising as plants tighten tolerances, standardize maintenance, and expand instrumented assets. In 2024, oil and gas accounts for an estimated 28% of global revenue, followed by manufacturing at 24% and automotive and aerospace combined near 18%, with the balance spread across power, chemicals, water, and HVAC. Replacement cycles drive a large share of unit volumes, while new-build capacity supports value growth through higher-spec materials, certifications, and calibration requirements.

Market supply is concentrated among global instrument makers and specialized regional manufacturers, with price competition most visible in analog mechanical gauges. Input costs for stainless steel, specialty alloys, and bourdon-tube components influence margins, while lead times for electronics affect digital variants. Regulatory pressure acts as a structural tailwind. Safety and quality frameworks in oil and gas, chemicals, and pressure systems increasingly require verified accuracy, traceability, and periodic recalibration, which accelerates upgrades from older gauges to tighter-tolerance models. Key risks include capex cyclicality in heavy industry, counterfeit or low-grade imports that increase failure rates, and downtime exposure from calibration backlogs.

Technology is shifting the value pool toward digital and smart gauges. Digital formats are estimated at 22% of 2024 revenue and could approach 35% by 2034 as sites adopt IoT connectivity, automated diagnostics, and AI-assisted anomaly detection for early leak and overpressure signals. Automation programs also favor gauges that integrate with SCADA and asset-management platforms, reducing manual rounds and improving audit readiness. Energy-sector activity reinforces this trajectory: U.S. natural gas production rose 4% in 2023 to an average 125.0 billion cubic feet per day, and U.S. oil supply exceeded 20 million barrels per day, expanding measurement points across basins and midstream assets. Global crude output rose 5.4% in 2022, with growth centered in the Middle East, North America, and Latin America, supporting sustained instrument demand.

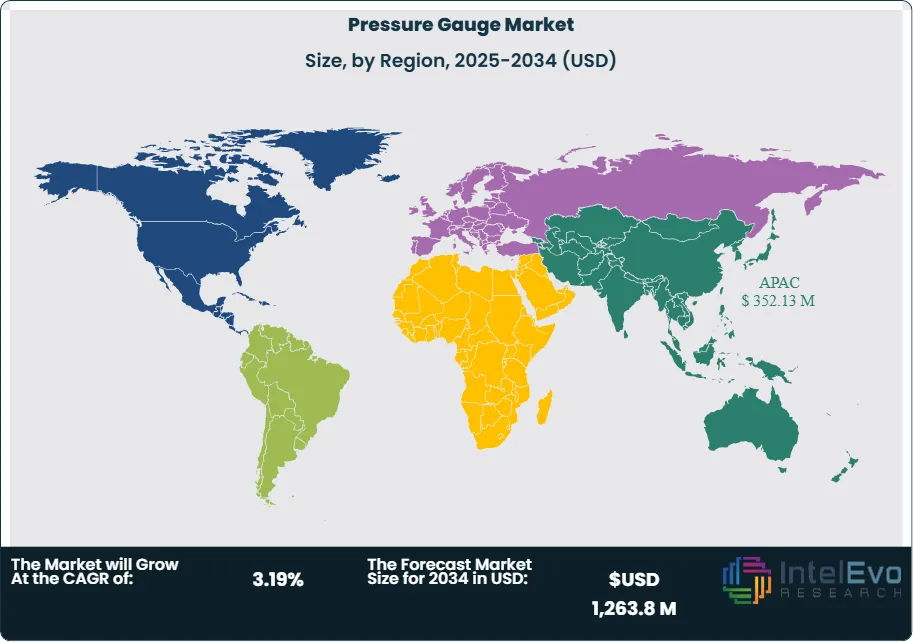

Regionally, Asia-Pacific leads with an estimated 38% share in 2024, supported by factory expansion and infrastructure buildout in China, India, and Southeast Asia. North America holds about 27% on the back of shale, LNG, and industrial retrofits, while Europe represents roughly 23% with strong compliance-driven replacement demand. Investment hotspots include U.S. Appalachia, Permian, and Haynesville, Middle East downstream and gas processing, and Latin American offshore developments, alongside fast-growing renewable applications such as hydrogen, biofuels, and grid-scale thermal systems.

, By Technology (Piezoresistive Pressure Gauges, Capacitive Pressure Gauges, Electromagnetic Pressure Gauges, Optical Pressure Gauges, Other Technologies), By Application (Aerospace & Defense, Automotive, Healthcare, Other Industrial Applications) Industry Region & Key Players – Market Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 0.9 billion USD, 2024 to 1.2 billion USD, 2034, at 3.19% CAGR, 2026-2034. It sustains steady demand across industrial instrumentation at estimated: 1.0 billion USD, 2029.

- Segment Dominance : Asia-Pacific leads with 37.0% share, 2024 and anchors volume growth through industrial activity at estimated: 0.3 billion USD, 2024. It supports incremental demand at estimated: 0.1 billion USD, 2030.

- Segment Dominance: Digital pressure gauges dominate with 57.0% share, 2024 and capture most upgrade budgets at estimated: 0.5 billion USD, 2024. Piezoresistive technology leads with 33.0% share, 2024 and drives standardized deployments at estimated: 0.3 billion USD, 2024.

- Driver: IoT integration accelerates adoption of connected gauges at estimated: 45.0% of new installations, 2030. It improves monitoring frequency and supports asset programs at estimated: 20.0% efficiency uplift, 2030.

- Restraint: Price pressure and replacement deferrals constrain premium uptake at estimated: 12.0% budget compression, 2024. Supply variability for electronics increases lead-time risk at estimated: 8.0 weeks, 2024.

- Opportunity: Niche diversification and strategic collaborations expand addressable demand at estimated: 0.2 billion USD, 2034. OEM partnerships scale embedded sensing routes at estimated: 15.0% of shipments, 2032.

- Trend: The market shifts toward smart, software-enabled gauges with estimated: 35.0% share, 2034. Digitalization strengthens remote diagnostics and predictive service at estimated: 25.0% fewer failures, 2033.

- Regional Analysis: Asia-Pacific maintains the lead at 37.0% share, 2024, while North America and Europe scale compliance-driven upgrades at estimated: 28.0% share, 2024 and estimated: 23.0% share, 2024. Emerging industrial hubs lift growth outside mature regions at estimated: 0.4 billion USD, 2034.

By Type

Digital pressure gauges account for the majority of global demand as of 2025, representing approximately 57% of total market revenue. This dominance reflects sustained investment in automation, connected instrumentation, and real-time process visibility across energy, pharmaceuticals, food processing, and advanced manufacturing. Digital gauges deliver higher measurement resolution, onboard diagnostics, and seamless compatibility with control systems, which supports compliance, uptime, and predictive maintenance objectives. Adoption rates continue to rise as plants replace legacy equipment to meet tighter accuracy and reporting requirements.

Analog pressure gauges retain a material presence, accounting for roughly 43% of demand in 2025. These products remain preferred in harsh or remote environments where simplicity, mechanical robustness, and minimal power dependency are required. Utilities, basic manufacturing, and certain field operations continue to specify analog designs due to lower upfront cost and proven reliability. Growth in this segment remains modest and largely replacement-driven, with limited exposure to software-led upgrades.

Looking ahead, digital formats are expected to exceed 65% share by 2030 as IIoT penetration deepens and calibration intervals tighten. Suppliers increasingly prioritize digital portfolios to defend margins and align with long-term instrumentation roadmaps.

By Application

Aerospace and defense represent the largest application segment in 2025, supported by stringent certification standards and mission-critical performance requirements. Pressure gauges play a central role in aircraft systems, propulsion monitoring, hydraulics, and space platforms. Defense modernization programs and expanding commercial aircraft backlogs sustain steady demand, particularly for high-accuracy and temperature-stable designs.

Automotive and healthcare follow as secondary contributors. Automotive demand centers on engine testing, fluid systems, and validation environments rather than high-volume vehicle installation. Healthcare relies on pressure gauges for anesthesia systems, respiratory equipment, and diagnostic devices, where accuracy and regulatory compliance drive specification choices.

Other applications, including oil and gas, chemicals, utilities, and industrial processing, collectively represent a substantial revenue base. These sectors favor gauges that support continuous operation, hazardous-area certification, and remote monitoring as process control systems evolve.

By End-Use

Industrial buildings account for the majority of pressure gauge consumption, exceeding 60% share in 2025. Manufacturing plants, refineries, and power facilities rely on pressure measurement for safety, throughput control, and asset protection. Capital spending cycles and regulatory audits directly influence procurement volumes in this segment.

Commercial buildings represent a smaller but stable share, driven by HVAC systems, fire suppression, and energy management infrastructure. Demand tracks urban construction activity and retrofit programs focused on efficiency and compliance. Residential buildings contribute minimally, limited to specialized plumbing and utility monitoring applications.

Industrial end-use will continue to dominate through 2035, supported by energy transition projects, process electrification, and expansion of automated production facilities.

By Region

Asia Pacific leads the global pressure gauge market with an estimated 37% share in 2025. Rapid industrial expansion, infrastructure spending, and manufacturing scale in China, India, Japan, and Southeast Asia underpin sustained demand. Regional adoption of smart factories further accelerates digital gauge penetration.

North America and Europe remain mature but high-value markets, supported by strict safety standards and ongoing upgrades in oil and gas, aerospace, pharmaceuticals, and healthcare. Together, they account for approximately 45% of global revenue. Latin America and the Middle East & Africa show moderate growth, driven by energy, mining, and construction projects, though investment volatility tempers near-term expansion.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Output Type

- Analog

- Digital

By Technology

- Piezoresistive Pressure Gauge

- Capacitive Pressure Gauge

- Electromagnetic Pressure Gauge

- Optical Pressure Gauge

- Other Technologies

By Application

- Aerospace and Defense

- Automotive

- Healthcare

- Other Applications

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 951.7 M |

| Forecast Revenue (2034) | USD 1,263.8 M |

| CAGR (2025-2034) | 3.19% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Output Type (Analog, Digital), By Technology (Piezoresistive Pressure Gauge, Capacitive Pressure Gauge, Electromagnetic Pressure Gauge, Optical Pressure Gauge, Other Technologies), By Application (Aerospace and Defense, Automotive, Healthcare, Other Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AMETEK Inc., Newbow Aerospace Ltd, Industrial Quick Search, Inc., Honeywell International Inc., WINTERS INSTRUMENTS, CIRCOR Aerospace, Crane Company, Tavis Corporation, Emerson Electric Co., Meggitt PLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Piezoresistive Pressure Gauges, Capacitive Pressure Gauges, Electromagnetic Pressure Gauges, Optical Pressure Gauges, Other Technologies), By Application (Aerospace & Defense, Automotive, Healthcare, Other Industrial Applications) Industry Region & Key Players – Market Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

, By Technology (Piezoresistive Pressure Gauges, Capacitive Pressure Gauges, Electromagnetic Pressure Gauges, Optical Pressure Gauges, Other Technologies), By Application (Aerospace & Defense, Automotive, Healthcare, Other Industrial Applications) Industry Region & Key Players – Market Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

, By Technology (Piezoresistive Pressure Gauges, Capacitive Pressure Gauges, Electromagnetic Pressure Gauges, Optical Pressure Gauges, Other Technologies), By Application (Aerospace & Defense, Automotive, Healthcare, Other Industrial Applications) Industry Region & Key Players – Market Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Pressure Gauge Market?

Global Pressure Gauge Market valued at USD 922.3M in 2024 is projected to reach USD 1,263.8M by 2034, driven by demand for industrial pressure monitoring in oil & gas, power, and manufacturing sectors.

Who are the major players in the Pressure Gauge Market?

AMETEK Inc., Newbow Aerospace Ltd, Industrial Quick Search, Inc., Honeywell International Inc., WINTERS INSTRUMENTS, CIRCOR Aerospace, Crane Company, Tavis Corporation, Emerson Electric Co., Meggitt PLC

Which segments covered the Pressure Gauge Market?

By Output Type (Analog, Digital), By Technology (Piezoresistive Pressure Gauge, Capacitive Pressure Gauge, Electromagnetic Pressure Gauge, Optical Pressure Gauge, Other Technologies), By Application (Aerospace and Defense, Automotive, Healthcare, Other Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date