- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Primary Edtech Market Size to Hit $98.7B by 2034 | 13.1% CAGR

Global Primary Edtech Market Size, Share, Analysis Report By Technology (Artificial Intelligence, Gamification, Adaptive Learning, Cloud-Based, Mobile Apps) Component (Software, Digital Content, Assessment Tools, Services) Verticals (Primary Schools(Public, Private), Homeschooling Networks) Enterprise Size (Small and Providers(Medium Edtech, Large Edtech)) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

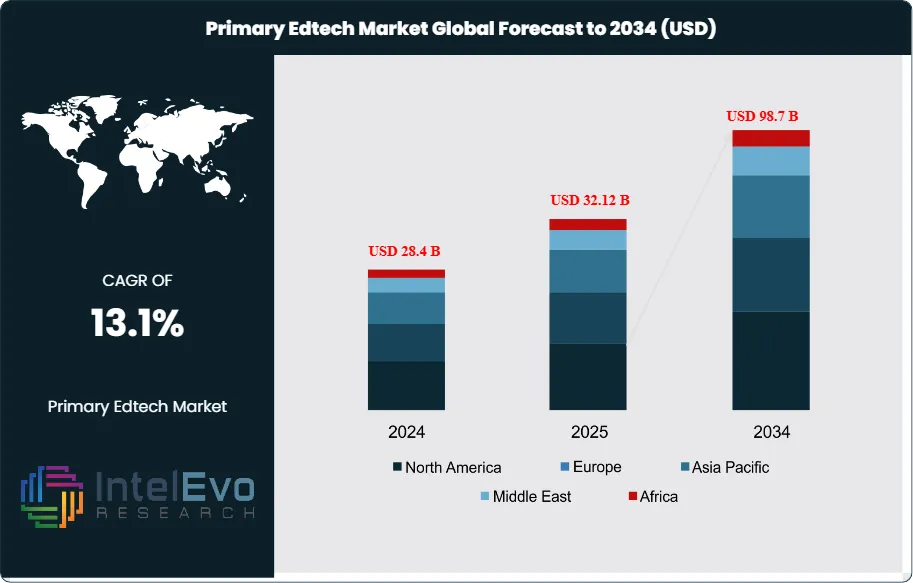

The Primary Edtech Market is projected to reach USD 98.7 Billion by 2034, up from USD 28.4 Billion in 2024, growing at a CAGR of 13.1% during the forecast period from 2024 to 2034. The primary edtech market encompasses a broad spectrum of digital solutions, platforms, and services designed to enhance learning outcomes, engagement, and accessibility for primary (K-6) students.

Get More Information about this report -

Request Free Sample ReportThis market includes interactive learning platforms, digital content, assessment tools, classroom management software, and integrated services for implementation and teacher training. The edtech ecosystem serves diverse educational stakeholders, including schools, teachers, students, parents, and education ministries, enabling personalized learning, real-time progress tracking, and collaborative classroom experiences worldwide.

The market is experiencing robust growth driven by the increasing demand for personalized and blended learning, the integration of advanced technologies such as artificial intelligence, gamification, and adaptive learning, and the need to bridge educational gaps. Key growth catalysts include the expansion of device access, government digital education initiatives, and the proliferation of cloud-based platforms that support remote and hybrid learning. The market also benefits from a growing emphasis on teacher professional development and the adoption of data-driven decision-making in primary education.

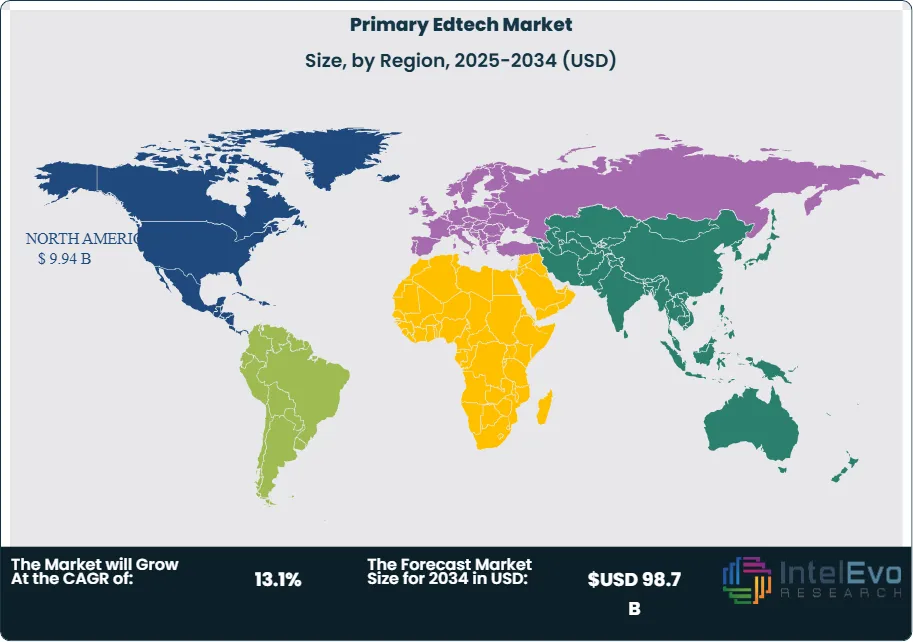

North America maintains its position as the leading regional market for primary edtech, commanding the largest global market share and generating the highest revenues within the sector. This dominance is attributed to early technology adoption, strong investment in digital infrastructure, and supportive education policies. The United States serves as the primary contributor to North America's market leadership, with substantial revenue generation and strong growth projections. Meanwhile, the Asia-Pacific region emerges as the most rapidly expanding market segment, propelled by large student populations, government-led digital learning programs, and increasing internet penetration.

The COVID-19 pandemic accelerated digital transformation in primary education, highlighting the importance of edtech for remote learning, student engagement, and educational continuity. The crisis underscored the value of scalable, accessible digital platforms and prompted schools to invest in robust edtech ecosystems. While initial challenges included device shortages and digital divides, the long-term impact has been positive, with increased recognition of edtech’s role in building resilient, future-ready education systems. Rising concerns about learning loss, equity, and student well-being are influencing product innovation and market competition. Edtech providers are investing in AI-driven analytics, social-emotional learning tools, and inclusive content to address diverse learner needs. Additionally, the growing focus on data privacy and cybersecurity is shaping procurement decisions and platform design.

Component (Software, Digital Content, Assessment Tools, Services) Verticals (Primary Schools(Public, Private), Homeschooling Networks) Enterprise Size (Small and Providers(Medium Edtech, Large Edtech)) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The Primary Edtech Market is expected to reach USD 98.7 Billion by 2034, fueled by growing demand for personalized learning, digital content, and hybrid classroom solutions.

- Technology Dominance: Enabling technologies such as AI, gamification, and adaptive learning lead the segment, due to their foundational role in driving engagement and learning outcomes.

- Component Dominance: Software platforms dominate, driven by their essential role in content delivery, assessment, and classroom management.

- Enterprise Size Dominance: Large education solution providers lead the segment, primarily due to higher investment capacity, global reach, and comprehensive product portfolios.

- Verticals Dominance: Public primary schools hold the largest share, owing to broad student bases and government funding for digital transformation.

- Driver: Key drivers accelerating growth include the demand for personalized learning and government digital education initiatives, which boost market expansion through improved access and engagement.

- Restraint: Growth is hindered by digital divides and budget constraints, which create barriers to adoption and equitable access.

- Opportunity: The market is poised for expansion due to opportunities like AI integration, emerging market penetration, and the development of inclusive, multilingual content.

- Trend: Emerging trends including hybrid learning models, social-emotional learning, and data-driven instruction are reshaping the market by enabling flexible, holistic education.

- Regional Analysis: North America leads owing to early technology adoption and established digital infrastructure. Asia-Pacific shows high promise due to large student populations and government investment.

Technology Analysis:

Enabling technologies such as artificial intelligence, gamification, and adaptive learning form the foundation of the primary edtech market. Artificial intelligence drives the creation of personalized learning paths, delivers real-time feedback, and supports predictive analytics that help teachers identify and address learning gaps early. Gamification techniques, including points, badges, and interactive challenges, significantly boost student engagement and motivation, making learning more enjoyable and effective. Adaptive learning platforms further enhance outcomes by dynamically adjusting content and pacing to suit each student’s unique needs, supporting differentiated instruction in diverse classrooms. The ongoing evolution of cloud computing, mobile applications, and data analytics continues to accelerate innovation and adoption, ensuring that edtech solutions remain accessible, scalable, and impactful across the sector.

Component Analysis:

Software platforms are at the heart of the primary edtech ecosystem, playing a crucial role in delivering digital content, managing classrooms, and assessing student progress. This category encompasses learning management systems (LMS), interactive content platforms, assessment tools, and teacher dashboards, all designed to streamline the educational process for both teachers and students. The dominance of software is driven by the need for solutions that are scalable, flexible, and user-friendly, capable of supporting a wide range of curricula and learning environments. As schools increasingly adopt blended and remote learning models, robust software platforms enable seamless integration of digital resources, real-time communication, and data-driven instruction.

Enterprise Size Analysis:

Large edtech companies and solution providers are the primary drivers of innovation and adoption in the primary edtech market. Their substantial resources allow for significant investment in research and development, enabling them to create comprehensive, integrated solutions that address the complex needs of schools and districts. These organizations are often at the forefront of digital transformation, leveraging technology to deliver scalable platforms, ensure data privacy compliance, and support large-scale deployments. Their global distribution networks and established reputations provide a competitive edge, allowing them to maintain leadership in a rapidly evolving and increasingly competitive industry.

Verticals Analysis:

Public primary schools constitute the largest segment of the primary edtech market, largely due to their broad student populations, access to government funding, and participation in national digital education initiatives. These schools are key adopters of digital textbooks, interactive lessons, formative assessments, and teacher professional development programs. The prominence of public schools in the market is further reinforced by significant investments in digital infrastructure, supportive policy frameworks, and strategic partnerships with edtech providers. These factors collectively drive widespread adoption and integration of technology in primary education, ensuring that digital learning benefits reach the largest possible number of students.

Region Analysis:

North America leads the global primary edtech market, accounting for over 35% of the market share, thanks to its advanced digital infrastructure, early embrace of educational technology, and robust policy support. The United States, in particular, plays a pivotal role by investing heavily in edtech startups, research, and large-scale digital learning initiatives that set industry benchmarks. Asia-Pacific is the fastest-growing region, propelled by its vast student populations, government-led digital learning programs, and rapidly increasing internet and device penetration. Countries like China, India, and Australia are at the forefront of this expansion, with schools rapidly adopting digital platforms and content to enhance learning outcomes. Europe maintains a strong presence in the market, supported by established education systems, high levels of digital literacy, and a strong emphasis on equity and inclusion. The region’s adoption of edtech is shaped by comprehensive regulatory frameworks, the need for multilingual content, and active engagement from leading solution providers, ensuring that technology-driven education is both accessible and inclusive.

Get More Information about this report -

Request Free Sample ReportMarket Key Segment

Technology

- Artificial Intelligence

- Gamification

- Adaptive Learning

- Cloud-Based Platforms

- Mobile Apps

Component

- Software Platforms

- Digital Content

- Assessment Tools

- Services

Verticals

- Public Primary Schools

- Private Primary Schools

- Homeschooling Networks

Enterprise Size

- Small and Medium Edtech Providers

- Large Edtech Providers

Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 32.12 B |

| Forecast Revenue (2034) | USD 98.7 B |

| CAGR (2025-2034) | 13.1% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Technology (Artificial Intelligence, Gamification, Adaptive Learning, Cloud-Based Platforms, Mobile Apps) Component (Software Platforms, Digital Content, Assessment Tools, Services) Verticals (Public Primary Schools, Private Primary Schools, Homeschooling Networks) Enterprise Size (Small and Medium Edtech Providers, Large Edtech Providers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Byju’s, Pearson, Kahoot!, Google for Education, Microsoft Education, Edmodo, Seesaw, ClassDojo, Discovery Education, Scholastic, SMART Technologies |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Component (Software, Digital Content, Assessment Tools, Services) Verticals (Primary Schools(Public, Private), Homeschooling Networks) Enterprise Size (Small and Providers(Medium Edtech, Large Edtech)) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Component (Software, Digital Content, Assessment Tools, Services) Verticals (Primary Schools(Public, Private), Homeschooling Networks) Enterprise Size (Small and Providers(Medium Edtech, Large Edtech)) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Component (Software, Digital Content, Assessment Tools, Services) Verticals (Primary Schools(Public, Private), Homeschooling Networks) Enterprise Size (Small and Providers(Medium Edtech, Large Edtech)) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date