- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Privacy-Enhancing Computation Market Size, Share | CAGR 19.9%

Global Privacy-Enhancing Computation Market Size, Share, Analysis By Product (Homomorphic Encryption Solutions, Secure Multi-Party Computation Solutions, Federated Learning Platforms, Differential Privacy Solutions, Trusted Execution Environment Solutions, Zero-Knowledge Proof Solutions, Data Clean Rooms, Privacy-Preserving Synthetic Data Solutions), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, By End-User Industry, Market Dynamics, Competitive Strategies & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 5.27 Billion | USD 26.90 Billion | 19.9% | North America, 36.2% |

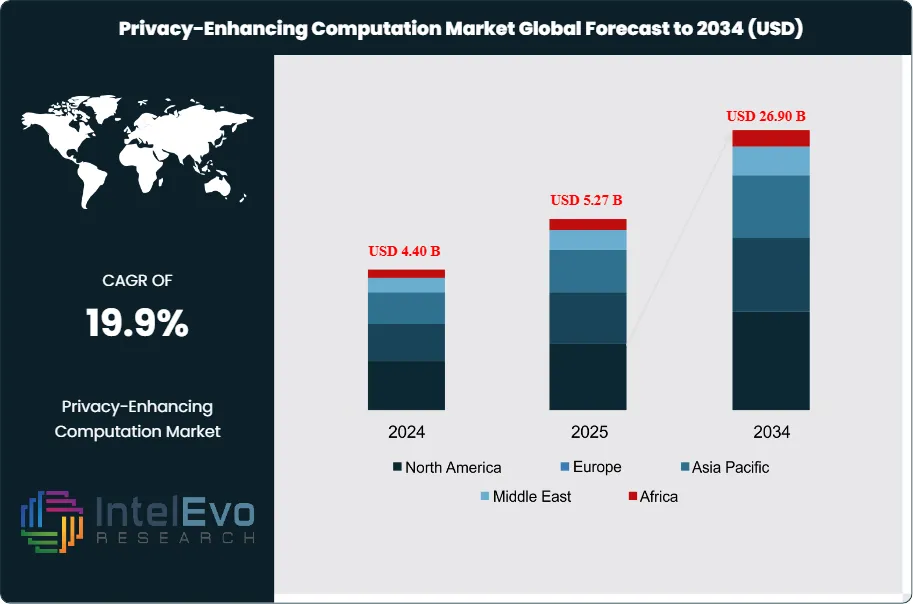

The Privacy-Enhancing Computation Market was valued at approximately USD 4.40 Billion in 2024 and reached USD 5.27 Billion in 2025. The market is projected to grow to USD 26.90 Billion by 2034, expanding at a CAGR of 19.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 21.63 Billion over the analysis period. The Privacy-Enhancing Computation Market covers the commercial space for cryptographic and hardware-based technologies that enable computation on sensitive data without exposing the underlying information, including homomorphic encryption (HE), secure multi-party computation (MPC), federated learning, differential privacy, zero-knowledge proofs (ZKP), and trusted execution environments (TEE) or confidential computing.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in three structural forces. First, regulatory pressure is intensifying globally with the EU AI Act entering force in 2024 and General Data Protection Regulation (GDPR) enforcement fining organizations over EUR 5.9 billion cumulatively through 2025. California's Consumer Privacy Act, PCI-DSS 4.0 effective 31 March 2025, FedRAMP High, and New York's SHIELD Act each require cryptographically enforced data protection. Second, the National Institute of Standards and Technology (NIST) published the first three finalized post-quantum cryptography (PQC) standards (ML-KEM, ML-DSA, SLH-DSA) in August 2024, and the U.S. Executive Order of January 2025 accelerated federal PQC migration ahead of the National Security Memorandum 10 (NSM-10) 2035 deadline. Third, AI training and inference on sensitive data has become a primary buyer-pull, with the EU AI Act compliance requirements taking effect through 2026.

Venture capital and strategic investment accelerated through 2025. Zama SAS, headquartered in Paris, raised USD 57 million in Series B funding on 25 June 2025 at a valuation above USD 1 billion, becoming the first fully homomorphic encryption unicorn with cumulative funding of USD 150 million. Intel announced TDX Connect support on Xeon 6 processors in January 2025 for encrypted CPU-to-GPU communications. Google Cloud and Swift began a federated anti-fraud network with 12 global banks under confidential computing in December 2024. Microsoft integrated Marvell FIPS 140-3 Level-3 hardware security modules into Azure Key Vault in December 2024 to harden quantum-safe key storage.

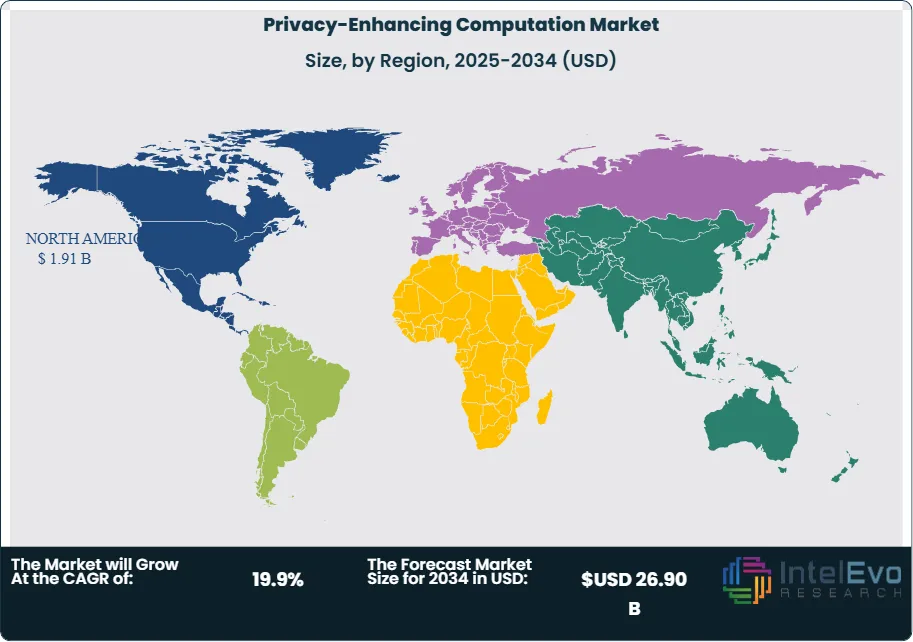

North America held 36.2% of global Privacy-Enhancing Computation Market revenue in 2025, equivalent to USD 1.91 Billion, with the United States contributing USD 1.50 Billion in 2024 and projected to reach USD 12.4 Billion by 2034 at a country CAGR of 23.5%. Europe captured approximately 27% share, driven by the EU AI Act, GDPR enforcement, GAIA-X federated data-sharing initiatives, and the European Health Data Space. Asia Pacific held 21% share in 2025 and is projected to grow fastest at approximately 25% CAGR through 2034, anchored by Japan's METI cybersecurity rules, India's Digital Personal Data Protection Act 2023, and China's Personal Information Protection Law (PIPL).

Forward visibility through 2034 rests on three catalysts. First, the NIST PQC migration deadline driven by U.S. federal agencies and Executive Order of January 2025 creates a cryptographically-enforced replacement cycle across regulated sectors. Second, the EU AI Act high-risk system requirements effective August 2026 mandate privacy-preserving training and inference for healthcare, finance, and critical infrastructure AI models. Third, the Department of Defense DARPA DPRIVE program funding Intel, Duality, SRI International, and Niobium for FHE accelerator development is driving a 100x performance improvement trajectory through 2028. These forces together support the 19.9% forecast CAGR in the Privacy-Enhancing Computation Market through 2034.

Market Definition & Scope

The Privacy-Enhancing Computation Market is defined as the commercial space for software platforms, hardware components, consulting services, and integration tools that enable data processing, analysis, and sharing without exposing the underlying sensitive information. The market encompasses seven technical primitives: fully homomorphic encryption (FHE), secure multi-party computation (MPC), federated learning (FL), differential privacy (DP), zero-knowledge proofs (ZKP), trusted execution environments (TEE) including Intel SGX, Intel TDX, AMD SEV-SNP, and Arm TrustZone, and personal data stores (PDS).

This analysis includes software licenses, cloud-based SaaS subscriptions, hardware-level TEE-enabled processors shipped with privacy-preserving capability, cryptographic accelerator cards, consulting services, and managed privacy-preserving analytics services. The scope explicitly excludes pure network-layer encryption (TLS, VPN), at-rest storage encryption without computation capability, data loss prevention (DLP) software, standalone identity and access management (IAM), and generic cybersecurity platforms without dedicated privacy-computing modules. The parent confidential computing market reached USD 24.24 Billion in 2025, while Privacy-Enhancing Computation represents the cryptographic and privacy-specific subset alongside, not inclusive of, the hardware-heavy parent category.

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, By End-User Industry, Market Dynamics, Competitive Strategies & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Privacy-Enhancing Computation Market grew from USD 5.27 Billion in 2025 to a projected USD 26.90 Billion in 2034, expanding at a 19.9% CAGR.

- Segment Dominance (By Product): Homomorphic encryption held 34% to 38.7% revenue share across 2024-2025 estimates, anchored by FHE-based encrypted analytics and the Zama TFHE-rs library with 3,000+ developer adoption.

- Segment Dominance (By Deployment): Cloud-based deployment captured 67% revenue share in 2024, reflecting hyperscaler-driven confidential VM availability across Azure, Google Cloud, and AWS.

- Driver: NIST finalized the first three post-quantum cryptography standards (ML-KEM, ML-DSA, SLH-DSA) in August 2024, driving a federal cryptographic replacement cycle ahead of NSM-10's 2035 full migration deadline.

- Restraint: FHE operations run approximately 100x slower than plaintext equivalents as of 2025, constraining high-throughput deployment and requiring GPU, FPGA, or purpose-built ASIC acceleration.

- Opportunity: Healthcare end-user segment is projected to grow at 31.6% CAGR through 2034, driven by the European Health Data Space and U.S. HIPAA Privacy Rule secondary-use compliance.

- Trend: Personal Data Stores (PDS) are projected to grow at 32.9% CAGR through 2034 as consumer data portability rules under GDPR, CCPA, and EU Data Act tighten through 2026.

- Regional: North America held 36.2% revenue share in 2025 at USD 1.91 Billion, supported by the U.S. Department of Defense USD 576 million secure chip foundry award to IBM in 2024.

Key Insights Summary

- Zama SAS raised USD 57 million Series B on 25 June 2025 co-led by Blockchange Ventures and Pantera Capital at a valuation above USD 1 billion, becoming the first fully homomorphic encryption unicorn with cumulative funding above USD 150 million.

- NIST published the first three finalized post-quantum cryptography standards (FIPS 203 ML-KEM, FIPS 204 ML-DSA, FIPS 205 SLH-DSA) in August 2024, establishing the federal PQC baseline replacing RSA and ECC vulnerable to Shor's algorithm.

- Intel announced TDX Connect support on Xeon 6 processors in January 2025, extending encrypted communication between confidential virtual machines and PCIe devices for AI GPU workloads.

- U.S. Department of Defense awarded IBM USD 576 million in 2024 for secure chip foundry expansion to harden microelectronics supply chain under NIST Provenance Chain Network provisions.

- Google Cloud and Swift launched a federated anti-fraud network with 12 global banks under confidential computing in December 2024, demonstrating production-scale privacy-preserving financial analytics.

- Microsoft integrated Marvell FIPS 140-3 Level-3 hardware security modules into Azure Key Vault in December 2024 to harden quantum-safe key storage for enterprise customers.

- EQTY Lab launched its Verifiable Compute AI framework with Intel and NVIDIA in January 2025 to ease EU AI Act compliance for high-risk AI systems deployed in regulated industries.

Competitive Landscape Overview

The Privacy-Enhancing Computation Market is moderately consolidated at the platform layer and fragmented at the specialist cryptography layer. The top four companies, including Microsoft, IBM, Intel, and Google, collectively held an estimated 48 to 54% of global revenue in 2025 through their hyperscaler confidential computing services and hardware TEE shipments. AMD, NVIDIA, and Arm Limited anchor the hardware TEE ecosystem with AMD SEV-SNP, NVIDIA Confidential Computing on H100 and H200 GPUs, and Arm TrustZone for edge deployments. Specialist vendors including Zama, Duality Technologies, Enveil, and Arcium fill protocol-level gaps in FHE, MPC, and encrypted search.

The competitive landscape shifted sharply through 2025 toward AI-workload optimization and post-quantum readiness. Intel paired Xeon 6 and Gaudi 2 accelerators with TDX Connect, while NVIDIA collaborated on verifiable compute attestations with EQTY Lab. Hardware alliances are reshaping go-to-market economics: startups increasingly partner with chipmakers and cloud hyperscalers rather than building stand-alone offerings. Mergers and acquisitions activity centered on capability aggregation, with cloud vendors acquiring niche FHE and ZKP teams to integrate cryptography into developer-friendly SDKs. Arcium acquired Inpher's technology and talent in November 2024 to bolster decentralized confidential computing via MPC. Competition will intensify as post-quantum deadlines near, and buyers favor vendors with certified quantum-safe stacks.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Microsoft Corporation | Redmond, WA, USA | Leader | Azure Confidential Computing; SEAL FHE library; Presidio | Global | Integrated Marvell FIPS 140-3 Level-3 HSMs into Azure Key Vault December 2024 |

| International Business Machines Corp. | Armonk, NY, USA | Leader | IBM Hyper Protect; HElib FHE library; IBM Quantum Safe | Global | Awarded USD 576 million DoD secure chip foundry expansion contract in 2024 |

| Intel Corporation | Santa Clara, CA, USA | Leader (Hardware) | Intel SGX; Intel TDX; TDX Connect on Xeon 6 | Global | Announced TDX Connect support on Xeon 6 processors in January 2025 for CPU-GPU encrypted communication |

| Alphabet Inc. (Google LLC) | Mountain View, CA, USA | Leader | Google Cloud Confidential VMs; Confidential Federated Computations | Global | Launched federated anti-fraud network with Swift and 12 global banks December 2024 |

| Advanced Micro Devices, Inc. | Santa Clara, CA, USA | Leader (Hardware) | AMD SEV-SNP; EPYC confidential VM extensions | Global | Continued SEV-SNP expansion across EPYC Genoa and Turin server CPU lines 2025 |

| NVIDIA Corporation | Santa Clara, CA, USA | Leader (AI) | Confidential Computing on H100/H200 GPUs; verifiable compute attestations | Global | Expanded verifiable compute attestations partnership with EQTY Lab in January 2025 |

| Zama SAS | Paris, France | Leader (FHE pure-play) | TFHE-rs; Concrete ML; FHEVM; Zama Protocol | Global | Raised USD 57M Series B on 25 June 2025 at USD 1 Billion valuation; Ethereum mainnet launched December 2025 |

| Duality Technologies, Inc. | Hoboken, NJ, USA | Challenger (MPC/FHE) | Duality SecurePlus; DARPA-funded FHE accelerator | North America | Continued DARPA DPRIVE FHE accelerator development and enterprise deployment through 2025 |

| Enveil, Inc. | Fulton, MD, USA | Niche (Encrypted Search) | ZeroReveal Search and Compute | North America | Continued In-Q-Tel-backed expansion for encrypted search in intelligence community 2025 |

| Arcium (formerly Elusiv) | Zurich, Switzerland | Niche (MPC) | Decentralized confidential computing network | Global | Acquired Inpher technology and talent November 2024 for MPC capability expansion |

Segmentation Analysis

The Privacy-Enhancing Computation Market segments across product type, deployment mode, enterprise size, and end-user vertical. Procurement leaders building a privacy-enhancing computation procurement checklist should benchmark vendors on FIPS 140-3 certification, post-quantum cryptography roadmap, performance benchmarks versus plaintext baseline, attestation support, and regulatory framework alignment (GDPR, HIPAA, PCI-DSS 4.0, FedRAMP High) across each segmentation dimension.

By Product

Homomorphic encryption led the Privacy-Enhancing Computation Market with 34% revenue share in 2024 per Precedence Research and 38.7% per Market.us estimates, equivalent to approximately USD 1.79 Billion to USD 2.04 Billion in 2025. The product category enables computation on encrypted data without decryption, with Zama TFHE-rs, Microsoft SEAL, IBM HElib, and Duality SecurePlus as the leading implementations. Zama's Concrete ML and FHEVM libraries had 3,000+ developer adopters by 2025, and Zama signed more than USD 50 million in contract value within six months of commercialization.

Secure multi-party computation (MPC) held approximately 22% revenue share in 2025, anchored by Duality Technologies, Arcium, Inpher (acquired by Arcium November 2024), Partisia Blockchain, and academic spin-outs. The global secure multiparty computation market sub-segment reached USD 993 million in 2025 per Precedence Research, with 11.83% CAGR through 2034. Federated learning captured approximately 18% share, dominated by Google (Confidential Federated Computations), Apple (on-device MM1 training), Meta, and NVIDIA FLARE. Trusted execution environments hosted on Intel SGX, Intel TDX, AMD SEV-SNP, and NVIDIA Hopper architecture contributed approximately 15% share. Differential privacy held 6%, zero-knowledge proofs 4%, and Personal Data Stores 3%.

By Deployment Mode

Cloud-based deployment led the Privacy-Enhancing Computation Market with 67% revenue share in 2024 and 58.4% per Market.us estimates, equivalent to USD 3.53 Billion in 2025. Azure Confidential Computing, Google Cloud Confidential VMs, and AWS Nitro Enclaves provide the dominant cloud-native deployment paths. On-premise deployment captured 33% in 2024 and is expected to grow faster than cloud through 2034 as regulated-industry buyers retain sovereign data custody under EU Data Act and jurisdiction-specific data localization rules. Hybrid deployment remains common among financial services buyers combining on-premise HSMs with cloud-based confidential VMs for analytics workloads. Privacy-enhancing computation implementation timelines typically range from 12 to 24 weeks for mid-market deployments and 9 to 18 months for Fortune 500 enterprise rollouts.

By Enterprise Size

Large enterprises held approximately 74% revenue share in 2025, reflecting the concentration of demand among regulated industries with dedicated cryptographic teams and budgets exceeding USD 500,000 per annual deployment. Small and medium enterprises (SMEs) held 26% share and are growing as cloud-native confidential VM pricing models and SaaS wrappers reduce the barrier to entry. Fortune 100 enterprise deployments regularly exceed USD 5 million annual run-rate spanning software, hardware, and integration services. SME-targeted offerings from Zama (open-source libraries), Duality (SDK), and cloud hyperscaler confidential VM services provide entry-level on-ramps below USD 50,000 annual run-rate.

By End-User

Banking, financial services, and insurance (BFSI) led end-user revenue share at 29% in 2025, equivalent to approximately USD 1.53 Billion, anchored by fraud detection (Google-Swift federated anti-fraud network), PCI-DSS 4.0 compliance, anti-money-laundering collaboration, and tokenized asset settlement. Healthcare held 18% share and is projected to grow fastest at 31.6% CAGR through 2034, driven by the European Health Data Space, U.S. HIPAA secondary-use research, and genomic data collaboration. Government and defense captured 16% share under NIST PQC migration, NSM-10, and DoD DPRIVE program funding. Technology and telecommunications held 14%, retail and e-commerce 9%, manufacturing 6%, and remaining verticals 8%. Privacy-enhancing computation ROI calculation models typically factor regulatory fine avoidance (GDPR fines up to 4% of global turnover) as the largest contributor to business case justification.

Regional Analysis

The Privacy-Enhancing Computation Market divides across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with North America leading in 2025 and Asia Pacific growing fastest through 2034.

North America

North America held 36.2% of global Privacy-Enhancing Computation Market revenue in 2025, equivalent to USD 1.91 Billion. The United States accounted for USD 1.50 Billion in 2024 and is projected to reach USD 12.4 Billion by 2034 at a country CAGR of 23.5%. The U.S. Department of Defense awarded IBM USD 576 million in 2024 for secure chip foundry expansion, and the U.S. Executive Order of January 2025 accelerated federal post-quantum cryptography migration ahead of NSM-10's 2035 deadline. NIST FIPS 203 ML-KEM, FIPS 204 ML-DSA, and FIPS 205 SLH-DSA standards of August 2024 define the federal baseline. FedRAMP High, CMMC 2.0, and HIPAA Privacy Rule enforcement each drive PEC procurement. Canada's Communications Security Establishment (CSE) and Mexico's INAI provide supplementary regulatory pressure.

Europe

Europe held 27.0% share in 2025 at approximately USD 1.42 Billion, with Germany, the United Kingdom, France, the Netherlands, and Switzerland leading adoption. The EU AI Act entered force in 2024 with high-risk system requirements effective August 2026, requiring privacy-preserving training and inference for healthcare, finance, and critical infrastructure AI. GDPR enforcement has generated over EUR 5.9 billion in cumulative fines through 2025. The European Health Data Space, GAIA-X, and Horizon Europe funding programs anchor federated data-sharing initiatives. Germany's BSI post-quantum migration guidelines, France's ANSSI PQC recommendations, and Switzerland's FADP revision each compound cryptographic replacement demand. The UK's National Cyber Security Centre (NCSC) published its Post-Quantum Cryptography migration guidance in 2024.

Asia Pacific

Asia Pacific captured 21.0% share in 2025 at approximately USD 1.11 Billion and is projected to grow fastest at approximately 25% CAGR through 2034, reaching 66.1% CAGR for the confidential computing sub-segment per Mordor Intelligence. China, Japan, South Korea, and Taiwan lead regional adoption. China's Personal Information Protection Law (PIPL) of November 2021, the state-backed quantum initiatives, and MEE cybersecurity rules drive demand. Japan's METI cybersecurity rules for semiconductor fabrication plants and Taiwan's post-quantum cryptography migration guide accelerated regional PQC procurement through 2025. Acompany established the Confidential Computing Lab (CC Lab) in Japan in March 2025 for hardware-driven confidential computing research. India's Digital Personal Data Protection Act 2023 and Australia's Critical Infrastructure Act drive enterprise TEE adoption.

Latin America

Latin America held 9.0% share in 2025 at approximately USD 474 Million, led by Brazil, Mexico, and Argentina. Brazil's Lei Geral de Protecao de Dados (LGPD) continues enforcement expansion, with ANPD issuing updated guidance on international data transfers through 2025. The Brazilian Association of Software Companies (ABES) reported Brazil's security spending at approximately USD 1.3 billion in 2023, up 13% year-over-year. Mexico's INAI federal privacy oversight supports cross-border PEC deployment, while Argentina's Decree 746/2017 on data protection aligns with GDPR principles. Regional growth is constrained by currency volatility and budget pressure, though multinational subsidiaries deploy corporate-standard TEE platforms.

Middle East & Africa

The Middle East & Africa region held 6.8% share in 2025 at approximately USD 358 Million. The United Arab Emirates' Personal Data Protection Law (Federal Decree-Law No. 45 of 2021), Saudi Arabia's Personal Data Protection Law under the Saudi Data and AI Authority (SDAIA), and Qatar's Data Protection Law No. 13 of 2016 anchor regional compliance demand. South Africa's POPIA (Protection of Personal Information Act) enforcement and Kenya's Data Protection Act 2019 provide sub-Saharan African regulatory tailwinds. Regional PEC growth is driven by sovereign cloud initiatives in Saudi Arabia (National Cybersecurity Authority), UAE (G42 partnerships), and Israel (cybersecurity export leadership).

Country Analysis

The Privacy-Enhancing Computation Market concentrates in four national markets that together contribute more than 55% of 2025 global revenue: the United States, China, Germany, and the United Kingdom.

United States

The United States generated USD 1.50 Billion in Privacy-Enhancing Computation Market revenue in 2024 and is projected to reach approximately USD 1.80 Billion in 2025 and USD 12.4 Billion by 2034 at a country CAGR of 23.5%. The U.S. Executive Order of January 2025 accelerated federal post-quantum cryptography migration, and the Department of Defense awarded IBM USD 576 million in 2024 for secure chip foundry expansion. National Security Memorandum 10 (NSM-10) sets the complete PQC migration deadline at 2035. NIST FIPS 203, 204, and 205 post-quantum standards of August 2024 establish the federal baseline. California's CCPA, New York's SHIELD Act, and the HIPAA Privacy Rule drive complementary sectoral pressure. Major buyers include JPMorgan Chase, Google, Microsoft, Meta, UnitedHealth Group, and federal agencies.

China

China contributed approximately USD 685 Million in Privacy-Enhancing Computation Market revenue in 2025, growing at a country CAGR of 25.8% through 2034. The Personal Information Protection Law (PIPL) of 1 November 2021, the Data Security Law of September 2021, and the Cybersecurity Law of 2017 collectively form the regulatory baseline. The Cyberspace Administration of China (CAC) issued cross-border data transfer rules in March 2024 requiring Security Assessment, Standard Contract, or Certification for outbound data. China continues significant state-backed investment in quantum computing and post-quantum cryptography through the 14th Five-Year Plan. Domestic vendors including Alibaba Cloud, Tencent, Ant Group, and Huawei compete alongside global platforms in the Chinese PEC market.

Germany

Germany accounted for approximately USD 425 Million in Privacy-Enhancing Computation Market revenue in 2025, with a projected country CAGR of 21.5% through 2034. The Bundesamt fur Sicherheit in der Informationstechnik (BSI) published post-quantum migration guidelines for federal and regulated-industry systems through 2025. The German confidential computing market is projected to reach USD 2.8 Billion by 2026 per Fortune Business Insights regional breakdown. GAIA-X federated data-sharing infrastructure is headquartered in Germany, and the German AI Act implementation schedule aligns with EU AI Act requirements effective August 2026. Major German buyers include SAP, Siemens, Deutsche Bank, Allianz, and BMW. Bundesdruckerei, SAP SE, and Rohde & Schwarz lead the domestic vendor ecosystem alongside global hyperscalers.

United Kingdom

The United Kingdom generated approximately USD 340 Million in Privacy-Enhancing Computation Market revenue in 2025, with a country CAGR of 22.0% through 2034. The UK confidential computing market is projected to reach USD 2.59 Billion by 2026 per Fortune Business Insights regional breakdown. The National Cyber Security Centre (NCSC) published its Post-Quantum Cryptography migration guidance in 2024, establishing UK federal timelines. The Information Commissioner's Office (ICO) enforces the UK GDPR and Data Protection Act 2018. The Financial Conduct Authority (FCA) supports privacy-preserving analytics pilots through its Regulatory Sandbox. Major UK buyers include HSBC, Barclays, Lloyds Banking Group, AstraZeneca, GlaxoSmithKline, and BP. Arm Limited, headquartered in Cambridge, anchors the TrustZone hardware ecosystem globally.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product

- Homomorphic Encryption Solutions

- Secure Multi-Party Computation (SMPC) Solutions

- Federated Learning Platforms

- Differential Privacy Solutions

- Trusted Execution Environment (TEE) Solutions

- Zero-Knowledge Proof (ZKP) Solutions

- Data Clean Rooms

- Privacy-Preserving Synthetic Data Solutions

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By End-User

- BFSI

- Healthcare & Life Sciences

- Government & Public Sector

- IT & Telecommunications

- Retail & E-Commerce

- Manufacturing

- Energy & Utilities

- Media & Entertainment

- Research & Academic Institutions

- Others (Transportation & Logistics, Legal Services, Insurance)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.27 B |

| Forecast Revenue (2034) | USD 26.90 B |

| CAGR (2025-2034) | 19.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Homomorphic Encryption Solutions, Secure Multi-Party Computation (SMPC) Solutions, Federated Learning Platforms, Differential Privacy Solutions, Trusted Execution Environment (TEE) Solutions, Zero-Knowledge Proof (ZKP) Solutions, Data Clean Rooms, Privacy-Preserving Synthetic Data Solutions), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User, (BFSI, Healthcare & Life Sciences, Government & Public Sector, IT & Telecommunications, Retail & E-Commerce, Manufacturing, Energy & Utilities, Media & Entertainment, Research & Academic Institutions, Others (Transportation & Logistics, Legal Services, Insurance)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT CORPORATION, INTERNATIONAL BUSINESS MACHINES CORP., INTEL CORPORATION, ALPHABET INC. (GOOGLE LLC), ADVANCED MICRO DEVICES, INC., NVIDIA CORPORATION, ZAMA SAS, DUALITY TECHNOLOGIES, INC., ENVEIL, INC., ARCIUM, AMAZON WEB SERVICES, INC., ORACLE CORPORATION, THALES GROUP, COSMIAN TECH, INPHER, INC. (ARCIUM), CORNAMI, INC., CRYPTOLAB INC., NETSKOPE, INC., FORTANIX, INC., ANJUNA SECURITY, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, By End-User Industry, Market Dynamics, Competitive Strategies & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, By End-User Industry, Market Dynamics, Competitive Strategies & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, By End-User Industry, Market Dynamics, Competitive Strategies & Forecast 2026-2034")

Frequently Asked Questions

How big is the Privacy-Enhancing Computation Market?

The Global Privacy-Enhancing Computation Market was valued at USD 4.40 Billion in 2024 and is projected to reach USD 26.90 Billion by 2034, growing at a CAGR of 19.9% from 2026 to 2034. Growth is driven by rising data privacy concerns, stringent regulatory compliance requirements, and increasing adoption of homomorphic encryption, federated learning, secure multi-party computation, and differential privacy solutions across BFSI, healthcare, government, and enterprise sectors worldwide.

Who are the major players in the Privacy-Enhancing Computation Market?

MICROSOFT CORPORATION, INTERNATIONAL BUSINESS MACHINES CORP., INTEL CORPORATION, ALPHABET INC. (GOOGLE LLC), ADVANCED MICRO DEVICES, INC., NVIDIA CORPORATION, ZAMA SAS, DUALITY TECHNOLOGIES, INC., ENVEIL, INC., ARCIUM, AMAZON WEB SERVICES, INC., ORACLE CORPORATION, THALES GROUP, COSMIAN TECH, INPHER, INC. (ARCIUM), CORNAMI, INC., CRYPTOLAB INC., NETSKOPE, INC., FORTANIX, INC., ANJUNA SECURITY, INC., Others

Which segments covered the Privacy-Enhancing Computation Market?

By Product, (Homomorphic Encryption Solutions, Secure Multi-Party Computation (SMPC) Solutions, Federated Learning Platforms, Differential Privacy Solutions, Trusted Execution Environment (TEE) Solutions, Zero-Knowledge Proof (ZKP) Solutions, Data Clean Rooms, Privacy-Preserving Synthetic Data Solutions), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User, (BFSI, Healthcare & Life Sciences, Government & Public Sector, IT & Telecommunications, Retail & E-Commerce, Manufacturing, Energy & Utilities, Media & Entertainment, Research & Academic Institutions, Others (Transportation & Logistics, Legal Services, Insurance))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Privacy-Enhancing Computation Market

Published Date : 08 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date