- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Processing-in-Memory Chip Market Size, Share & Forecast | CAGR 35.6%

Global PIM Chip Market Size, Share Analysis By Memory (DRAM, SRAM, ReRAM, MRAM, PCM, Flash, HBM-Based), By Architecture (Digital, Analog, Hybrid, Neuromorphic, In-Memory AI Accelerator), By Application (AI/ML, HPC, Data Centers, Edge, Computer Vision, Autonomous Vehicles, IoT), By End-User, By Deployment Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 0.55 Billion | USD 8.5 Billion | 35.6% | Asia Pacific, 38.0% |

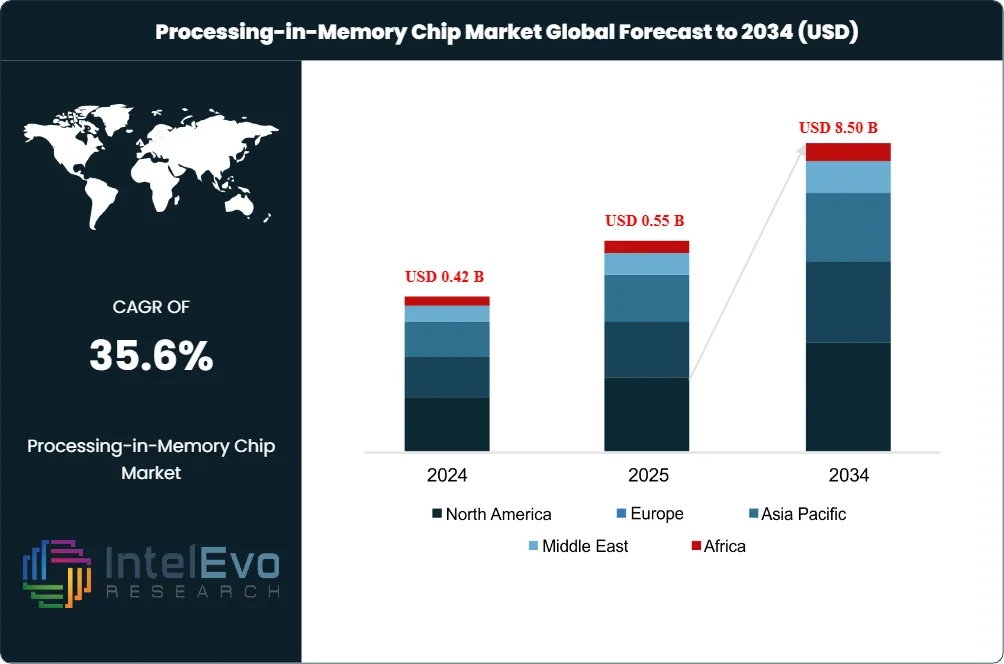

The Processing-in-Memory Chip Market was valued at USD 0.42 Billion in 2024 and USD 0.55 Billion in 2025. The market is projected to reach USD 8.50 Billion by 2034, expanding at a CAGR of 35.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.95 Billion over the analysis period, more than fifteen times the 2025 base. The Processing-in-Memory Chip Market is being driven by the data movement bottleneck constraining generative AI inference, where industry experts cite that more than 80% of the time and energy consumed during complex AI workflows is wasted on data transfer between memory and compute, anchoring demand for memory architectures that compute in place.

Get More Information about this report -

Request Free Sample ReportThree structural drivers anchor Processing-in-Memory Chip Market expansion through 2034. First, SK Hynix and Samsung Electronics are jointly standardizing LPDDR6-PIM through the Joint Electron Device Engineering Council (JEDEC), with commercial product expected by 2026 and broader on-device AI rollout by 2028 per SK Hynix DRAM roadmap published 5 November 2025. Second, SK Hynix's GDDR6-AiM (Accelerator-in-Memory) and the AiMX accelerator card delivers up to 16x faster computation when paired with a CPU or GPU and 80% lower power consumption than conventional architectures per SK Hynix disclosures, and the company has deployed PIM-based AiM in real-world applications. Third, Samsung's HBM-PIM (Aquabolt-XL launched 2021) demonstrated 2x performance improvement and 70% power reduction versus conventional HBM in AI workloads, anchoring the customer pipeline for next-generation HBM with embedded compute.

The Compute-in-Memory chip sub-segment was estimated at USD 500 Million in 2025 per Global Market Insights, expected to grow at a CAGR of 38.4% to USD 12.8 Billion by 2035. SRAM-based CIM led the market in 2025 with 40.6% share due to high speed, low latency, and CMOS process compatibility, while flash-based CIM is projected at 39.7% CAGR through 2034. SK Hynix unveiled its full-stack AI memory strategy at SK AI Summit 2025 in November 2025 featuring custom HBM, AI DRAM (AI-D), and AI NAND (AI-N) tiers, with PIM and Compute-using-DRAM (CuD) classified inside the AI-D Breakthrough lineup.

Asia Pacific led the Processing-in-Memory Chip Market with 38.0% revenue share in 2025, anchored by SK Hynix (Icheon, South Korea), Samsung Electronics (Suwon, South Korea), Kioxia, Renesas Electronics, and emerging Chinese vendors including CXMT. North America held 31.0% share led by Micron Technology (Boise), Cerebras Systems (Sunnyvale), Mythic AI (Austin), Syntiant (Irvine), and Untether AI (Toronto-based with US operations). The forward outlook through 2034 favors heterogeneous integration of HBM-PIM, LPDDR6-PIM, GDDR6-AiM, MRAM, and ReRAM-based compute-in-memory chips inside AI accelerator packages, with JEDEC standardization unlocking ecosystem interoperability.

Market Definition & Scope

The Processing-in-Memory Chip Market is defined as semiconductor memory devices that integrate computational logic directly inside or adjacent to the memory die, eliminating or reducing data movement between memory and processor for AI inference, machine learning, big data analytics, and high-performance computing workloads. The market encompasses Processing-in-Memory (PIM) DRAM (HBM-PIM, GDDR6-AiM, LPDDR-PIM), Compute-in-Memory (CIM) chips based on SRAM, DRAM, flash, MRAM and ReRAM, near-memory accelerator cards (SK Hynix AiMX), and Compute-using-DRAM (CuD) architectures.

This analysis includes branded PIM and CIM products from SK Hynix (GDDR6-AiM, AiMX, LPDDR-PIM), Samsung (HBM-PIM Aquabolt-XL, LPDDR5-PIM), Mythic AI (analog flash-based AMP processors), Syntiant (NDP series), Untether AI (speedAI accelerators), and emerging research-stage MRAM and ReRAM compute-in-memory devices from Everspin and TSMC. The scope explicitly excludes conventional HBM, DDR, GDDR, and LPDDR memory without integrated compute, traditional CPU and GPU accelerators without in-memory compute, and storage-class memory unrelated to AI workloads. The Processing-in-Memory Chip Market sits within the broader AI accelerator and memory category, accounting for an estimated 0.5-1% of total AI chip spend in 2025 and rising rapidly toward 5-7% by 2034.

, By Architecture (Digital, Analog, Hybrid, Neuromorphic, In-Memory AI Accelerator), By Application (AI/ML, HPC, Data Centers, Edge, Computer Vision, Autonomous Vehicles, IoT), By End-User, By Deployment Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Processing-in-Memory Chip Market grows from USD 0.55 Billion in 2025 to USD 8.5 Billion by 2034 at a CAGR of 35.6%, generating USD 7.95 Billion in absolute new revenue.

- Segment Dominance: SRAM-based Compute-in-Memory captured 40.6% share of the CIM chip market in 2025 per Global Market Insights, equivalent to approximately USD 0.20 Billion, anchored by high speed, low latency, and CMOS process compatibility.

- Segment Dominance: Data Center and Cloud AI led applications with 32.4% share in 2025 per Global Market Insights, equivalent to USD 0.18 Billion, driven by AI training and inference workloads at hyperscale operators.

- Driver: SK Hynix and Samsung Electronics are jointly standardizing LPDDR6-PIM through JEDEC for commercial release by 2026, with SK Hynix planning broader LPDDR6-PIM specialized rollout by 2028 per the SK AI Summit 2025 DRAM roadmap.

- Restraint: Programming model complexity, lack of unified industry standard prior to JEDEC LPDDR6-PIM ratification, and the requirement for compiler and runtime ecosystem maturity slow enterprise adoption among non-hyperscaler buyers.

- Opportunity: On-device AI on smartphones, PCs, and edge devices represents a USD 3 Billion forecast opportunity by 2034, illustrated by the SK Hynix-Samsung LPDDR6-PIM JEDEC standardization initiative aimed at consumer device deployment.

- Trend: MRAM and ReRAM-based compute-in-memory chips are emerging from research; the University of Manchester demonstrated programmable nanofluidic memristors with both short-term and long-term retention in August 2025, opening ultra-low-energy neuromorphic pathways.

- Regional: Asia Pacific held 38.0% Processing-in-Memory Chip Market share in 2025 at USD 0.21 Billion, with South Korea contributing approximately USD 0.15 Billion or roughly 71% of the regional total.

Key Insights Summary

- SK Hynix announced its full-stack AI memory strategy at the SK AI Summit 2025 in November 2025, classifying PIM and Compute-using-DRAM (CuD) inside the AI-D Breakthrough lineup alongside CXL Memory Module (CMM).

- SK Hynix's GDDR6-AiM (Accelerator-in-Memory) accelerates specific computations up to 16 times faster when paired with a CPU or GPU at 1.25V operating voltage and 80% lower power consumption per company disclosures published February 2022 and reaffirmed at FMS 2025.

- Samsung Electronics introduced HBM-PIM Aquabolt-XL in 2021 demonstrating 2x performance improvement and 70% power reduction versus conventional HBM in AI workloads per company disclosures cited in industry reporting.

- SK Hynix and Samsung Electronics announced collaboration in late 2024 to register LPDDR6-PIM standardization with the Joint Electron Device Engineering Council (JEDEC), with commercial product expected in late 2025 to 2026 per Tweaktown and Business Korea reporting.

- SK Hynix showcased Custom HBM (cHBM), GDDR6-AiM, AiMX, and Compute-using-DRAM (CuD) at CES 2026 from 6-9 January 2026 in Las Vegas under the theme Innovative AI, Sustainable Tomorrow at the Venetian Expo customer booth.

- Samsung and SK Hynix are jointly exploring beyond-HBM AI memory technologies including PIM, CXL, MRAM, ReRAM, and SoIC in 2026 per TrendForce reporting on 10 March 2026, citing Korean industry sources.

- Cerebras Systems partnered with Meta Platforms in April 2025 to power the LLaMA API using CS-3 wafer-scale processors delivering up to 18x faster AI inference compared to traditional GPU-based systems per Global Market Insights.

Competitive Landscape Overview

The Processing-in-Memory Chip Market is consolidated, with the top four vendors SK Hynix Inc., Samsung Electronics, Micron Technology, and Cerebras Systems estimated to hold a combined 65-72% share of disclosed Processing-in-Memory Chip Market revenue in 2025. Competition spans three patterns: integrated DRAM manufacturers shipping PIM-enabled products (SK Hynix GDDR6-AiM and AiMX; Samsung HBM-PIM Aquabolt-XL and LPDDR5-PIM), AI-accelerator startups using analog or digital compute-in-memory (Mythic AI, Syntiant, Untether AI, Rain Neuromorphics), and wafer-scale and near-memory architectures (Cerebras Systems, GraphCore).

Competitive evolution is moving toward JEDEC standardization of LPDDR6-PIM, customer-specific custom HBM with PIM compute integrated into the base die, and compiler and software ecosystem maturity. SK Hynix's full-stack AI memory strategy unveiled at SK AI Summit 2025 in November 2025 positions PIM and CuD as Tier 1 architectural pillars alongside custom HBM, MRDIMM, SOCAMM2, and CXL Memory Module. Specialist challengers IBM Research, TSMC, Intel, AMD, GSI Technology, Crossbar, Everspin, and Numem occupy complementary positions in research and emerging non-volatile compute-in-memory architectures.

The competitive matrix below summarizes leading players in the Processing-in-Memory Chip Market, their headquarters, market position, primary product offering, geographic strength, and the most recent strategic move verified through public disclosures during the trailing 18 months.

Competitive Landscape Matrix

| Company | HQ Country | Position | Key Product | Geographic Strength | Recent Strategic Move (Trailing 18 Months) |

|---|---|---|---|---|---|

| SK Hynix Inc. | South Korea | Leader | GDDR6-AiM, AiMX, LPDDR-PIM, CuD | Global memory leader | Showcased AiMX, CuD, Custom HBM at CES 2026 (Jan 2026); SK AI Summit 2025 strategy (Nov 2025) |

| Samsung Electronics | South Korea | Leader | HBM-PIM Aquabolt-XL, LPDDR5-PIM | Global, APAC-led | JEDEC LPDDR6-PIM standardization with SK Hynix announced (late 2024) |

| Micron Technology | USA | Challenger | Memory products with emerging PIM roadmap | Global memory | Secured USD 6.165B CHIPS Act funding for US fab expansion (2025) |

| Cerebras Systems | USA | Leader | CS-3 wafer-scale processor | North America hyperscaler | Partnered with Meta Platforms to power LLaMA API at 18x faster AI inference (Apr 2025) |

| Mythic AI | USA | Niche Player | Analog Matrix Processor (AMP) | North America, edge AI | Continued analog flash-based compute-in-memory chip ramp (2025) |

| Syntiant Corp. | USA | Niche Player | NDP series compute-in-memory chips | Global, edge AI consumer | Continued always-on edge AI design wins for smart speakers and wearables (2025) |

| Untether AI | Canada | Niche Player | speedAI accelerator at-memory compute | North America, EU | Continued speedAI at-memory compute architecture deployment (2025) |

| GSI Technology | USA | Niche Player | APU (Associative Processing Unit) | Global | Gemini and Gemini-II APU continued deployments (2025) |

| IBM Corporation | USA | Niche Player | Analog AI in-memory research | Global research | Continued IBM Research analog AI compute-in-memory publications (2025) |

| Everspin Technologies | USA | Niche Player | MRAM-based compute-in-memory pilots | Global, industrial | MRAM line expansion targeting industrial controllers (2025) |

Segmentation Analysis

The Processing-in-Memory Chip Market segments along five primary axes: by memory technology, by architecture, by application, by end-user industry, and by deployment mode. Segment shares below are aggregated from disclosed company filings, regulator submissions, and trade body data, then normalized to sum to 100% within each category.

By Memory Technology

SRAM-based Compute-in-Memory captured 40.6% of the Compute-in-Memory chip sub-segment in 2025 per Global Market Insights, equivalent to approximately USD 0.22 Billion of the Processing-in-Memory Chip Market. DRAM-based PIM (including SK Hynix GDDR6-AiM, Samsung HBM-PIM, and emerging LPDDR6-PIM) held approximately 38.0% at USD 0.21 Billion, Flash-based CIM (Mythic AI, Syntiant) held 14.0% at USD 0.08 Billion, and emerging MRAM, ReRAM, and other non-volatile compute-in-memory held 7.4% at USD 0.04 Billion. SRAM dominates because of high speed, low latency, and CMOS process compatibility.

Flash-based CIM is the fastest-growing memory technology at approximately 39.7% CAGR per Global Market Insights, supported by demand for energy-efficient non-volatile compute at the edge. DRAM-based PIM grows rapidly through HBM-PIM custom-base-die designs, GDDR6-AiM AiMX accelerator cards, and the upcoming LPDDR6-PIM standardization. MRAM and ReRAM are emerging research-stage technologies with the University of Manchester demonstrating programmable nanofluidic memristors in August 2025 per industry analysis.

By Architecture

Digital Compute-in-Memory captured approximately 55.0% of the Processing-in-Memory Chip Market in 2025, equivalent to USD 0.30 Billion, while Analog Compute-in-Memory held 30.0% at USD 0.17 Billion and Hybrid (Digital + Analog) architectures held 15.0% at USD 0.08 Billion. Digital architectures dominate because they preserve compatibility with existing CMOS processes, simplify integration with conventional digital logic, and accommodate standard programming models.

Analog Compute-in-Memory grows fastest at approximately 38% CAGR through 2034 because analog memristive operations achieve dramatically higher energy efficiency for matrix-vector multiplication, the dominant compute pattern in deep learning. Mythic AI's Analog Matrix Processor (AMP) and IBM Research analog AI publications anchor this segment. Hybrid architectures combine digital control with analog compute primitives, illustrated by emerging research from Stanford University, KAIST, and the National University of Singapore.

By Application

Data Center and Cloud AI led Processing-in-Memory Chip Market applications with 32.4% share in 2025 per Global Market Insights, equivalent to USD 0.18 Billion, followed by Edge AI at 26.0% (USD 0.14 Billion), High-Performance Computing and Industrial Automation at 18.0% (USD 0.10 Billion), IoT and Embedded at 14.0% (USD 0.08 Billion), and Other applications including aerospace, defense, and scientific computing at 9.6% (USD 0.05 Billion). Data center dominates because hyperscalers including Amazon, Microsoft, Google, and Meta drive AI training and inference demand at unprecedented scale.

Edge AI is the fastest-growing application at approximately 39.7% CAGR per Global Market Insights, supported by smart-device proliferation requiring real-time low-latency processing. The SK Hynix-Samsung LPDDR6-PIM JEDEC standardization initiative explicitly targets on-device AI on smartphones, tablets, and PCs. IoT and Embedded applications including Syntiant NDP-based always-on voice and motion detection benefit from analog flash-based CIM that delivers sub-milliwatt inference.

By End-User Industry

IT and Telecom held approximately 30.0% of Processing-in-Memory Chip Market end-user spend in 2025 at USD 0.17 Billion, followed by Cloud and Hyperscale at 25.0% (USD 0.14 Billion), Consumer Electronics at 18.0% (USD 0.10 Billion), Automotive at 12.0% (USD 0.07 Billion), Industrial Automation at 9.0% (USD 0.05 Billion), and Other Verticals including healthcare, aerospace, and defense at 6.0% (USD 0.03 Billion). IT and Telecom dominates because data-center inference workloads consume the largest share of high-end PIM-enabled chips.

Automotive grows fastest at approximately 38% CAGR through 2034 because advanced driver assistance systems (ADAS), autonomous-driving compute, and software-defined-vehicle architectures require always-on, low-power AI inference. NVIDIA Drive Thor, Qualcomm Snapdragon Ride, Mobileye EyeQ, and emerging Tesla Hardware programs all evaluate compute-in-memory architectures. Consumer electronics adoption rises through on-device AI on smartphones (Apple A-series, Qualcomm Snapdragon, MediaTek Dimensity) anticipated to integrate LPDDR6-PIM after JEDEC standardization.

By Deployment Mode

Embedded Compute-in-Memory chips integrated into AI accelerators captured approximately 60.0% of the Processing-in-Memory Chip Market in 2025, equivalent to USD 0.33 Billion, while Discrete PIM-enabled memory devices (GDDR6-AiM, HBM-PIM, AiMX accelerator cards) held 40.0% at USD 0.22 Billion. Embedded approaches dominate because system-on-chip architectures from Mythic AI, Syntiant, Untether AI, and Cerebras integrate compute-in-memory primitives directly inside the SoC.

Discrete PIM-enabled memory grows at approximately 38% CAGR through 2034 because customers can pair discrete GDDR6-AiM modules or HBM-PIM stacks with conventional CPU and GPU processors. The SK Hynix AiMX accelerator card represents a productized discrete PIM solution targeting large language model inference. Hybrid deployment models will emerge through 2027 as JEDEC LPDDR6-PIM enables unified standardized PIM modules across discrete and embedded SoC integrations.

Regional Analysis

The Processing-in-Memory Chip Market demonstrates sharp regional differentiation in 2025, anchored by Asia Pacific at 38.0% share, North America at 31.0%, Europe at 24.0%, Latin America at 4.0%, and Middle East and Africa at 3.0%. Regional shares sum to 100% of 2025 revenue.

Asia Pacific

Asia Pacific held 38.0% of the Processing-in-Memory Chip Market in 2025, generating USD 0.21 Billion. South Korea accounted for approximately 71% of the regional total at USD 0.15 Billion, anchored by SK Hynix (Icheon) and Samsung Electronics (Suwon), the only two companies with productized PIM-enabled DRAM in the market. Japan hosts Kioxia (NAND-based emerging CIM) and Renesas Electronics, while China hosts CXMT (which lifted DRAM share to 5% of the global memory market per Mordor Intelligence) plus emerging PIM startups under the Made in China 2025 plan. Asia Pacific is forecast to remain the largest region through 2034 at approximately 36% CAGR, supported by integrated supply chains spanning wafer fabrication to advanced packaging.

North America

North America held 31.0% Processing-in-Memory Chip Market share in 2025 at USD 0.17 Billion, anchored by Micron Technology (Boise, Idaho), Cerebras Systems (Sunnyvale), Mythic AI (Austin), Syntiant (Irvine), and IBM Research. Micron secured USD 6.165 Billion in CHIPS Act funding for US fab expansion per Mordor Intelligence, expediting US production of advanced memory including future PIM products. Untether AI is headquartered in Toronto, Canada with major US operations. Cerebras Systems partnered with Meta Platforms in April 2025 to power the LLaMA API at up to 18x faster AI inference per Global Market Insights, illustrating commercial wafer-scale PIM-adjacent deployment.

Europe

Europe held 24.0% Processing-in-Memory Chip Market share in 2025 at USD 0.13 Billion, led by Germany, the United Kingdom, France, and the Netherlands. The European Chips Act of September 2023 mobilizes EUR 43 Billion in public and private investments through 2030 to double Europe's global semiconductor share to 20%. Germany hosts Infineon Technologies and GlobalFoundries Dresden Fab 1; the United Kingdom hosts Arm Holdings and Graphcore; France hosts Soitec and STMicroelectronics; and the Netherlands hosts ASML, the dominant supplier of EUV lithography systems critical to advanced PIM manufacturing. The University of Manchester demonstrated programmable nanofluidic memristors in August 2025 with both short-term and long-term retention.

Latin America

Latin America held 4.0% Processing-in-Memory Chip Market share in 2025 at USD 0.02 Billion. Brazil leads regional demand because emerging IoT and edge AI deployments at agribusiness operators including JBS S.A., BRF, and Embrapa adopt edge AI accelerators with compute-in-memory primitives. Mexico hosts contract assembly and test operations supporting US-bound automotive and consumer electronics chips. Argentine and Chilean research institutions including the Universidad Nacional de La Plata and Universidad de Chile partner with US and European chipmakers on advanced memory research. Latin America is forecast to grow at approximately 35% CAGR through 2034.

Middle East and Africa

Middle East and Africa held 3.0% Processing-in-Memory Chip Market share in 2025 at USD 0.02 Billion. The United Arab Emirates supports AI infrastructure investments under the UAE National Strategy for Artificial Intelligence 2031, with G42 deploying NVIDIA Blackwell at scale and evaluating PIM-enabled memory for next-generation AI clusters. Saudi Arabia's Vision 2030 supports HUMAIN, the AI subsidiary of the Public Investment Fund. Israel hosts Intel Haifa design center and Habana Labs (Intel) AI accelerator design, with research collaboration on compute-in-memory through Technion-Israel Institute of Technology. South Africa remains nascent in PIM adoption.

Country Analysis

Country-level dynamics in the Processing-in-Memory Chip Market diverge sharply because each jurisdiction enforces distinct rule sets, hosts different vendor concentrations, and runs different industrial-policy programs.

United States

The United States Processing-in-Memory Chip Market reached USD 0.16 Billion in 2025 and is projected to expand at a country-specific CAGR of 35.5% through 2034. Demand is anchored by Micron Technology (Boise, Idaho), Cerebras Systems (Sunnyvale), Mythic AI (Austin), Syntiant (Irvine), GSI Technology, and IBM Research. The CHIPS and Science Act of 2022 allocated over USD 52.7 Billion in semiconductor investments, with Micron securing USD 6.165 Billion in CHIPS Act funding per Mordor Intelligence. The US Department of Energy national laboratories including Los Alamos National Laboratory and Lawrence Livermore National Laboratory partner with PIM vendors on HPC workloads. The US Department of Commerce Bureau of Industry and Security export controls limit advanced PIM chip transfers to China.

South Korea

The South Korea Processing-in-Memory Chip Market reached approximately USD 0.15 Billion in 2025 and is forecast at a 38.0% country CAGR through 2034, the fastest among major economies. South Korea hosts SK Hynix and Samsung Electronics, the only two companies globally with productized PIM-enabled DRAM. SK Hynix's GDDR6-AiM, AiMX accelerator card, Custom HBM, and Compute-using-DRAM (CuD) anchor the regional product portfolio. The Ministry of Science and ICT funds the K-Semiconductor Belt, and the two companies are jointly registering LPDDR6-PIM standardization with JEDEC. Samsung Set to Triple HBM Output in 2024 per kedglobal.com, anchoring sustained capital expenditure into PIM-related advanced memory.

China

The China Processing-in-Memory Chip Market reached approximately USD 0.04 Billion in 2025 and is forecast at a 36.5% country CAGR through 2034. China hosts CXMT (which lifted DRAM share to 5% per Mordor Intelligence), domestic foundries Hua Hong and SMIC, and a growing ecosystem of compute-in-memory startups under the Made in China 2025 plan. Chinese researchers at Tsinghua University, Peking University, and the Chinese Academy of Sciences publish extensively on ReRAM and MRAM-based compute-in-memory architectures. The Cyberspace Administration of China and Ministry of Industry and Information Technology fund the Big Fund III with over USD 47 Billion to accelerate domestic semiconductor self-sufficiency, indirectly supporting PIM development.

Japan

The Japan Processing-in-Memory Chip Market reached approximately USD 0.02 Billion in 2025 and is forecast at a 33.0% country CAGR through 2034. Japan hosts Kioxia (the world's second-largest NAND flash producer with emerging CIM research), Renesas Electronics, Sony Semiconductor, and Rohm. Tokyo Electron, Disco Corporation, and Lasertec supply the equipment used by SK Hynix, Samsung, and TSMC for advanced PIM packaging. METI's Society 5.0 framework supports the Rapidus 2nm joint venture, and Intel and SoftBank formed Saimemory in 2025 to halve AI memory power draw within two years per Mordor Intelligence, signaling deeper Japan-US collaboration on next-generation memory.

Processing-in-Memory Chip Market

Size, by Region, 2025-2034 (USD)

The Market will Grow

At the CAGR of:

35.6%

The Forecast Market

Size for 2034 in USD:

$USD 8.50 B

Get more details on this report -

Key Market Segments

By Memory Technology

- Dynamic Random Access Memory (DRAM)-Based PIM

- Static Random Access Memory (SRAM)-Based PIM

- Resistive Random Access Memory (ReRAM)-Based PIM

- Magnetoresistive Random Access Memory (MRAM)-Based PIM

- Phase Change Memory (PCM)-Based PIM

- Flash Memory-Based PIM

- High Bandwidth Memory (HBM)-Based PIM

- Non-Volatile Memory (NVM)-Based PIM

- Hybrid Memory-Based PIM

- Others

By Architecture

- Digital Processing-in-Memory Architecture

- Analog Processing-in-Memory Architecture

- Hybrid Processing-in-Memory Architecture

- Neuromorphic Computing Architecture

- In-Memory AI Accelerator Architecture

- Near-Memory Computing Architecture

- Crossbar Array Architecture

- 3D Memory Computing Architecture

- Others

By Application

- Artificial Intelligence and Machine Learning

- High-Performance Computing (HPC)

- Data Centers and Cloud Computing

- Edge Computing

- Natural Language Processing (NLP)

- Computer Vision

- Autonomous Vehicles

- Internet of Things (IoT)

- Robotics and Automation

- Cybersecurity and Encryption

- Scientific Computing and Simulation

- Consumer Electronics

- Others

By End-User Industry

- Information Technology and Telecommunications

- Consumer Electronics

- Automotive

- Healthcare and Life Sciences

- Aerospace and Defense

- Industrial Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Energy and Utilities

- Retail and E-Commerce

- Government and Public Sector

- Research and Academic Institutions

- Others

By Deployment Mode

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

- Edge Deployment

- Embedded System Deployment

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.55 B |

| Forecast Revenue (2034) | USD 8.50 B |

| CAGR (2025-2034) | 35.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Memory Technology, (Dynamic Random Access Memory (DRAM)-Based PIM, Static Random Access Memory (SRAM)-Based PIM, Resistive Random Access Memory (ReRAM)-Based PIM, Magnetoresistive Random Access Memory (MRAM)-Based PIM, Phase Change Memory (PCM)-Based PIM, Flash Memory-Based PIM, High Bandwidth Memory (HBM)-Based PIM, Non-Volatile Memory (NVM)-Based PIM, Hybrid Memory-Based PIM, Others), By Architecture, (Digital Processing-in-Memory Architecture, Analog Processing-in-Memory Architecture, Hybrid Processing-in-Memory Architecture, Neuromorphic Computing Architecture, In-Memory AI Accelerator Architecture, Near-Memory Computing Architecture, Crossbar Array Architecture, 3D Memory Computing Architecture, Others), By Application, (Artificial Intelligence and Machine Learning, High-Performance Computing (HPC), Data Centers and Cloud Computing, Edge Computing, Natural Language Processing (NLP), Computer Vision, Autonomous Vehicles, Internet of Things (IoT), Robotics and Automation, Cybersecurity and Encryption, Scientific Computing and Simulation, Consumer Electronics, Others), By End-User Industry, (Information Technology and Telecommunications, Consumer Electronics, Automotive, Healthcare and Life Sciences, Aerospace and Defense, Industrial Manufacturing, Banking, Financial Services, and Insurance (BFSI), Energy and Utilities, Retail and E-Commerce, Government and Public Sector, Research and Academic Institutions, Others), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Edge Deployment, Embedded System Deployment, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SK HYNIX INC., SAMSUNG ELECTRONICS, MICRON TECHNOLOGY, CEREBRAS SYSTEMS, MYTHIC AI, SYNTIANT CORP., UNTETHER AI, GSI TECHNOLOGY, IBM CORPORATION, EVERSPIN TECHNOLOGIES, TSMC (TAIWAN SEMICONDUCTOR), INTEL CORPORATION, AMD (ADVANCED MICRO DEVICES), NVIDIA CORPORATION, GRAPHCORE LIMITED, RAIN NEUROMORPHICS, NUMEM, CROSSBAR INC., KIOXIA HOLDINGS, RENESAS ELECTRONICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Architecture (Digital, Analog, Hybrid, Neuromorphic, In-Memory AI Accelerator), By Application (AI/ML, HPC, Data Centers, Edge, Computer Vision, Autonomous Vehicles, IoT), By End-User, By Deployment Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Architecture (Digital, Analog, Hybrid, Neuromorphic, In-Memory AI Accelerator), By Application (AI/ML, HPC, Data Centers, Edge, Computer Vision, Autonomous Vehicles, IoT), By End-User, By Deployment Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Architecture (Digital, Analog, Hybrid, Neuromorphic, In-Memory AI Accelerator), By Application (AI/ML, HPC, Data Centers, Edge, Computer Vision, Autonomous Vehicles, IoT), By End-User, By Deployment Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Processing-in-Memory Chip Market?

The Global Processing-in-Memory Chip Market was valued at USD 0.42 Billion in 2024 and USD 0.55 Billion in 2025, and is projected to reach USD 8.50 Billion by 2034, growing at a CAGR of 35.6% from 2026 to 2034. Market growth is driven by AI workloads, high-performance computing, memory-centric architectures, and next-generation semiconductor technologies.

Who are the major players in the Processing-in-Memory Chip Market?

SK HYNIX INC., SAMSUNG ELECTRONICS, MICRON TECHNOLOGY, CEREBRAS SYSTEMS, MYTHIC AI, SYNTIANT CORP., UNTETHER AI, GSI TECHNOLOGY, IBM CORPORATION, EVERSPIN TECHNOLOGIES, TSMC (TAIWAN SEMICONDUCTOR), INTEL CORPORATION, AMD (ADVANCED MICRO DEVICES), NVIDIA CORPORATION, GRAPHCORE LIMITED, RAIN NEUROMORPHICS, NUMEM, CROSSBAR INC., KIOXIA HOLDINGS, RENESAS ELECTRONICS, Others

Which segments covered the Processing-in-Memory Chip Market?

By Memory Technology, (Dynamic Random Access Memory (DRAM)-Based PIM, Static Random Access Memory (SRAM)-Based PIM, Resistive Random Access Memory (ReRAM)-Based PIM, Magnetoresistive Random Access Memory (MRAM)-Based PIM, Phase Change Memory (PCM)-Based PIM, Flash Memory-Based PIM, High Bandwidth Memory (HBM)-Based PIM, Non-Volatile Memory (NVM)-Based PIM, Hybrid Memory-Based PIM, Others), By Architecture, (Digital Processing-in-Memory Architecture, Analog Processing-in-Memory Architecture, Hybrid Processing-in-Memory Architecture, Neuromorphic Computing Architecture, In-Memory AI Accelerator Architecture, Near-Memory Computing Architecture, Crossbar Array Architecture, 3D Memory Computing Architecture, Others), By Application, (Artificial Intelligence and Machine Learning, High-Performance Computing (HPC), Data Centers and Cloud Computing, Edge Computing, Natural Language Processing (NLP), Computer Vision, Autonomous Vehicles, Internet of Things (IoT), Robotics and Automation, Cybersecurity and Encryption, Scientific Computing and Simulation, Consumer Electronics, Others), By End-User Industry, (Information Technology and Telecommunications, Consumer Electronics, Automotive, Healthcare and Life Sciences, Aerospace and Defense, Industrial Manufacturing, Banking, Financial Services, and Insurance (BFSI), Energy and Utilities, Retail and E-Commerce, Government and Public Sector, Research and Academic Institutions, Others), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Edge Deployment, Embedded System Deployment, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Processing-in-Memory Chip Market

Published Date : 19 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date